|

시장보고서

상품코드

1851313

LiDAR 드론 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)LiDAR Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

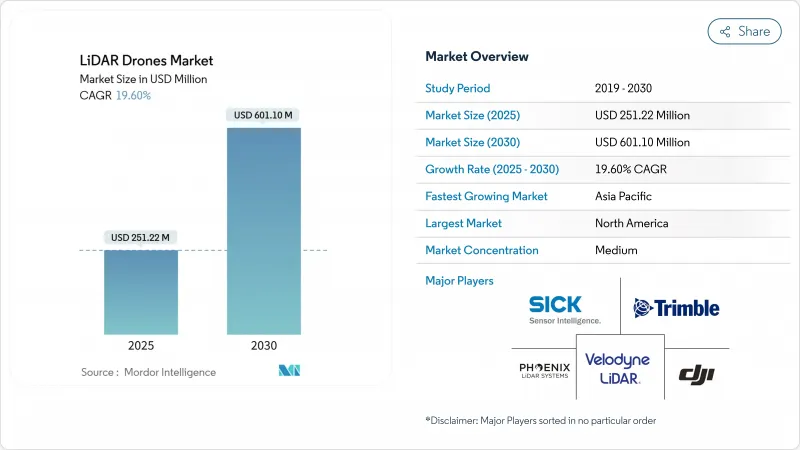

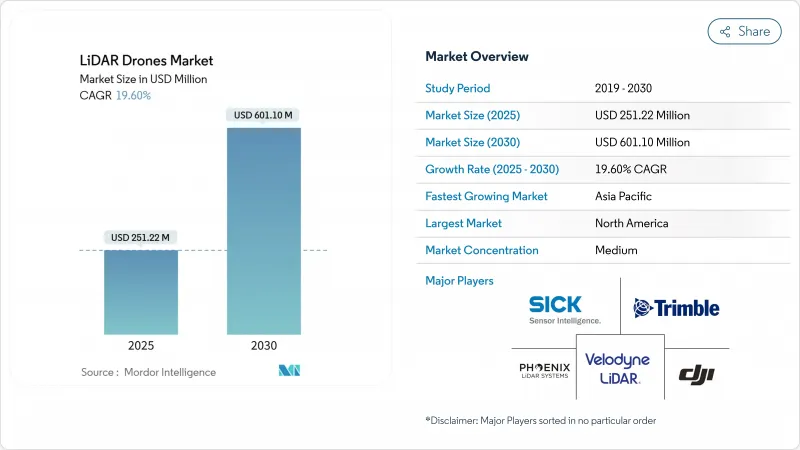

LiDAR 드론 시장은 2025년에 2억 5,122만 달러에 이르고, 2030년에는 6억 110만 달러에 달하며, CAGR 19.60%를 나타낼 것으로 예상됩니다.

400달러의 변곡점을 밑돌고 있는 솔리드 스테이트 비용의 돌파구, 주요 공역 시장에서의 지지적인 규제 개혁, 건설, 농업, 에너지에 대한 정밀 매핑 수요 증가가 이 확대를 지원하고 있습니다. 회전 날개 플랫폼 업그레이드, 클라우드 네이티브 데이터 파이프라인, 통합형 내비게이션 유닛으로 대응 가능한 사용자 기반이 확대되는 한편, 센서의 경량화로 도시와 마이크로 매핑의 새로운 기회가 탄생했습니다. 북미, 석유 및 가스, 아시아태평양의 대규모 인프라 계획에서는 계속 무인 시스템에 조사 예산이 할당되고 있어 메탄 누설 검지의 의무화에 의해 석유 및 가스 섹터에서는 LiDAR 페이로드의 도입이 가속하고 있습니다. 하드웨어 상용화는 분석 소프트웨어 및 LiDAR-as-a-Service 제공에 가치를 유도하고 경쟁 전략과 마진을 재구성합니다.

세계의 LiDAR 드론 시장 동향과 인사이트

고체형 라이다(LiDAR)의 손익분기점 비용이 400달러 미만으로 대량 시장용 드론 보급 가능

포토닉스의 통합과 제조 규모의 확대로 솔리드 스테이트 LiDAR의 단가는 400달러 미만으로, 소규모 계약자, 농가, 미국이 LiDAR 탑재기를 채용하는 것을 망설였던 역사적인 비용 장벽이 없어졌습니다. 헤세이의 연간 30만대 생산량은 현재 가능한 규모의 경제를 보여줍니다. 기계 부품의 제거는 신뢰성을 향상시키고 유지 보수를 줄이고 특허 출원은 빔 스티어링 최적화에 대한 열렬한 연구를 보여줍니다. 이러한 변화는 전문 조사 회사뿐만 아니라 주류 건설 및 환경 서비스로 조달을 확대하고 반복 업그레이드주기를 강화하고 있습니다.

EU 오픈 카테고리 규정이 뒷받침되는 250g 이하의 마이크로 매핑 드론 급증

유럽의 오픈 카테고리 규정은 조종사 면허 없이 250g 이하의 항공기를 비행할 수 있게 하고 클래스 C0 무인 항공기용으로 설계된 마이크로 LiDAR 페이로드 파도에 박차를 가하고 있습니다. 제조업체 각사는 현재, 중량 상한을 밑돌면서 50pt/m2 근처의 포인트 밀도에 이르고 있습니다. DJI의 Air 3S는 장애물 회피와 기본적인 매핑을 위한 전방향 LiDAR를 탑재한 소비자급 기체를 보여줍니다. 도시계획 담당자나 유산 보호 담당자는 저렴한 가격으로 신속하게 도입할 수 있는 툴로부터 이익을 얻고 있어, 캐나다나 일본에서도 같은 틀이 등장해, 대응 가능한 기반이 넓어지고 있습니다.

멀티 페이로드 리그의 1550nm 레이저 EMI 컴플라이언스 장애물

FAA 지침 AC 20-183은 고출력 1550nm 레이저가 라디오와 레이더와 기체를 공유 할 때 엄격한 EMI, 노출, 눈에 대한 위험을 계산해야합니다. 차폐 및 파장 선택 필터는 시스템 비용에 15-25% 가산되어 멀티 센서 플릿의 조달을 지연시킵니다. 특히 메탄 분광, 광대역 통신, GNSS를 하나의 리그에 통합하는 석유 및 가스 사업자에게는 인증 백로그가 리드 타임을 연장하고 있습니다.

부문 분석

레이저 스캐너는 포인트 클라우드 생성에서 탁월한 역할을 반영하여 2024년 LiDAR 드론 시장 점유율의 40%를 유지했습니다. 내비게이션과 포지셔닝 유닛은 센티미터급 관성-GNSS 퓨전이 긴밀하게 결합된 SLAM 워크플로우에 필수적이기 때문에 CAGR 22%를 나타낼 전망입니다. 이러한 정확한 기준 패키지는 프리미엄 조사 등급의 아티팩트를 제공하는 LiDAR 드론 시장 규모를 지원합니다. 열 조절 모듈과 에지 프로세서를 포함한 두 번째 레이어 구성 요소는 현재 비행 중 특징 추출을 처리하기 위해 AI 가속기를 통합하고 있습니다. 제조업체는 개발 사이클을 단축하고 현장 교환을 간소화하며 함대 운영자의 총 소유 비용을 줄이는 공통 전기 및 데이터 인터페이스를 배포합니다.

표준화는 LiDAR 코어와 함께 카메라, 멀티스펙트럼 또는 자력계 유닛을 플러그 앤 플레이로 업그레이드할 수 있는 오픈소스 미들웨어에 이르기까지 다양합니다. 배터리 관리 시스템은 장시간 비행이 셀 수명과 온도 한계에 스트레스를 가할수록 고도화되고 있습니다. 설계상의 주의는 고주파 트랜스미터와 광증폭 회로 사이의 전자기 결합에 대한 실드로 변화하고 있으며, 이 테마는 1550nm의 전개가 확대됨으로써 증폭되고 있습니다.

회전익 항공기는 호버링 안정성, 수직 이륙, 구조물 주변에서 정밀한 위치결정에 의해 선호되었으며, 2024년 총 출하량의 63%를 차지했습니다. 하이브리드 VTOL 기계는 새롭지만, 이러한 제어상의 이점과 고정 날개의 순항 효율을 결합하여 운영자는 하나의 배터리로 50km 이상의 항로를 모니터링할 수 있습니다. 고정날개 설계에는 현재 모듈식 노즈콘과 듀얼 센서 탑재 가능한 날개 하드 포인트가 있어 비행시간당 조사생산성을 높이고 있습니다.

LiDAR 드론 시장은 셀 타워, 외관, 제한된 위치 매핑을 위해 회전 날개의 다용도를 계속 평가하고 있지만, 호버링 시간과 관련된 보험료 상승으로 운영자는 지형이 발사 및 회수 스트립을 허용하는 고정 날개 출격을 고려하도록 권장합니다. 제품 유형은 퀵 스왑 기체 키트를 지원하며, 승무원은 플랫폼 유형간에 한 번의 변화 내에서 동일한 센서 스택을 재배포할 수 있게 되어 제품 클래스 간의 과거 경계가 모호해집니다.

지역 분석

북미는 확립된 BVLOS 면제 패스웨이, 견고한 GNSS 보정 그리드 및 100kg/h의 검출 임계값을 지정하는 연방 메탄 누출 규칙으로부터 혜택을 받아 2024년 세계 매출의 35.7%를 유지했습니다. 에너지 계수는 EPA 규정 준수를 충족하기 위해 함대 배치에 자금을 제공하고 주 DOT는 수리주기 이전에 다리와 도로를 스캔하기 위해 자본을 할당합니다. 트림블의 2025년 1분기 8억 4,100만 달러의 수익은 기계 제어 및 측량 자동화와 관련된 장비 수요의 지속을 밝혔습니다.

아시아태평양의 점유율은 22%이지만 중국의 LiDAR 생산 규모와 인도의 인프라 정비에 힘입어 가장 급경사의 성장을 기록하고 있습니다. Hesai만으로 2025년 1분기에 19만 5,818개의 센서를 출하했으며, 이 지역의 제조력을 뒷받침하고 있습니다. 인도의 관민 회랑은 토지 취득과 진행 추적을 위해 드론 매핑을 채용하고, 일본은 지방 지자체의 조사에 보조금을 내고 있습니다. BVLOS의 조화는 ASEAN 전역에서 늦어져 해상 파이프라인과 송전선의 정찰 확대를 억제하고 있습니다.

유럽에서는 EASA의 오픈 카테고리를 기반으로 한 통일 된 공역 규정이 도시 측량과 문화 유산 아카이브를위한 마이크로 플랫폼 도입을 자극하고 있습니다. 헥사곤은 2024년 3분기에 5억 6,490만 유로(6억 6,464만 달러)의 경상수익을 계상했습니다. 단일 광자의 진보는 효율적인 국가 매핑을 약속하고 그린 거래의 생물 다양성 목표는 임업과 서식지의 LiDAR 기준선에 대한 수요를 기릅니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고체형 라이다(LiDAR)의 손익분기점 비용이 400달러 미만으로 대량 시장용 드론 보급 가능

- EU의 오픈 카테고리 규칙이 뒷받침하는 250g 이하의 「마이크로 매핑」드론의 급증

- 수심계 LiDAR를 VTOL 드론에 탑재하여 아사미의 자산 조사를 실시

- 클라우드 네이티브인 SLAM/AI 포인트 클라우드 파이프라인이 후처리의 리드 타임을 단축

- 북미에서 LiDAR UAV를 사용한 석유 및 가스의 메탄 누설 검출이 60% 의무화

- African corridor finance(Af CFTA)가 유인 항공기보다 드론에 의한 지형 조사를 지지

- 시장 성장 억제요인

- 1550nm 레이저의 멀티 페이로드 리그에 있어서 EMI 컴플라이언스의 허들

- 항공 교통 관리의 분단이 ASEAN의 BVLOS 허가를 지연

- 탄소 전지 운송 규제가 서비스 제공업체의 물류 코스트를 인상

- 카리브해의 섬나라에서는 GNSS 보정 인프라가 한정

- 가치/공급망 분석

- 규제와 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 산업 밸류체인 분석

제5장 시장 규모와 성장 예측

- 구성 요소별

- 레이저 스캐너

- 905 nm 기계식

- 905 nm MEMS

- 1550nm 광섬유

- 내비게이션 및 위치 측정 시스템

- 관성 측정 장치(IMU)

- 카메라

- 전원 및 열 관리 모듈

- 기타 구성 요소

- 제품 형태별

- 회전익

- 고정익

- 하이브리드 VTOL

- 고도별

- 초저고도(120m 미만)

- 저고도(120-300m)

- 중고도(300-500m)

- 범위별

- 단거리(100m 미만)

- 중거리(100-500m)

- 장거리(500m 이상)

- 서비스 모델별

- 하드웨어 판매

- 턴키 LiDAR-as-a-Service

- 분석 SaaS

- 용도별

- 건설 및 인프라

- 환경 및 산림

- 정밀 농업

- 통로 매핑(도로, 철도, 파이프라인)

- 광업 및 채석

- 국방 및 보안

- 재난 관리 및 보험

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 자금 조달, 파트너십)

- 시장 점유율 분석

- 기업 프로파일

- DJI

- Leica Geosystems(Hexagon)

- RIEGL Laser Measurement

- Velodyne/Ouster

- Phoenix LiDAR Systems

- YellowScan SAS

- FARO Technologies

- Teledyne Optech

- Trimble Inc.

- Sick AG

- Microdrones GmbH

- senseFly SA

- Terra Drone Corp.

- Innoviz Technologies

- Luminar Technologies

- Parrot Drone SAS

- GeoCue Group Inc.

- Cepton Technologies

- Robosense(LeiShen)

- Topodrone LLC

제7장 시장 기회와 향후 전망

KTH 25.11.21The LiDAR drone market reached USD 251.22 million in 2025 and is forecast to climb to USD 601.10 million by 2030, advancing at a 19.60% CAGR.

Solid-state cost breakthroughs below the USD 400 inflection point, supportive regulatory reforms in major air-space markets, and expanding demand for precision mapping across construction, agriculture, and energy underpin this expansion. Rotary-wing platform upgrades, cloud-native data pipelines, and integrated navigation units are widening the addressable user base, while lower-weight sensors are opening new urban and micro-mapping opportunities. Large infrastructure programs in North America, the European Union, and Asia-Pacific continue to allocate survey budgets toward unmanned systems, and methane-leak detection mandates are accelerating LiDAR payload uptake in the oil and gas sector. Hardware commoditization is steering value toward analytics software and LiDAR-as-a-Service offerings, reshaping competitive strategies and margins.

Global LiDAR Drones Market Trends and Insights

Break-even of Solid-state LiDAR Cost Below USD 400 Enabling Mass-market Drones

Photonics integration and scaled manufacturing have pushed solid-state unit prices below USD 400, removing the historical cost barrier that discouraged smaller contractors, farmers, and municipalities from adopting LiDAR-equipped aircraft. Hesai's 300,000-unit annual volumes exemplify the economies of scale now possible. Mechanical parts elimination improves reliability and cuts maintenance, and patent filings show intense work on beam steering optimization. These shifts are expanding procurement beyond specialized survey firms into mainstream construction and environmental services, bolstering recurring upgrade cycles.

Surge in Sub-250 g Micro-mapping Drones Driven by EU Open-category Rules

Open-category regulations in Europe allow sub-250 g aircraft to be flown without a pilot license, spurring a wave of micro-LiDAR payloads engineered for class C0 drones. Manufacturers now reach point densities near 50 pts/m2 while staying under the weight ceiling. DJI's Air 3S shows how consumer-grade craft now host forward-facing LiDAR for obstacle avoidance and basic mapping. Urban planners and heritage conservators benefit from affordable, quick-deployment tools, and similar frameworks are emerging in Canada and Japan, broadening the addressable base.

EMI Compliance Hurdles for 1550 nm Lasers on Multi-payload Rigs

FAA guidance AC 20-183 requires rigorous EMI, exposure, and ocular hazard calculations when high-power 1550 nm lasers share airframes with radios and radars. Shielding and wavelength-selective filters add 15-25% to system cost, slowing procurement for multi-sensor fleets. Certification backlogs extend lead times, particularly for oil-and-gas operators integrating methane spectroscopy, broadband comms, and GNSS on one rig.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Bathymetric LiDAR on VTOL Drones for Shallow-water Asset Surveys

- Cloud-native SLAM/AI Point-cloud Pipelines Reducing Post-processing Lead-time

- Fragmented Air-traffic Management Delaying BVLOS Permits in ASEAN

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laser scanners retained 40% of LiDAR drone market share in 2024, reflecting their irreplaceable role in point-cloud generation. Navigation and positioning units are advancing at a 22% CAGR, as centimeter-grade inertial-GNSS fusion has become essential for tightly coupled SLAM workflows. These precise reference packages anchor the LiDAR drone market size for premium survey-grade deliverables. Second-tier components, including thermal regulation modules and edge processors, now incorporate AI accelerators to handle in-flight feature extraction. Manufacturers are rolling out common electrical and data interfaces that shorten development cycles and simplify field swaps, lowering total cost of ownership for fleet operators.

Standardization extends to open-source middleware that allows plug-and-play upgrades of camera, multispectral, or magnetometer units alongside the LiDAR core. Battery management systems gain sophistication as extended-endurance flights stress cell life and thermal limits. Design attention is shifting to shielding against electromagnetic coupling between high-frequency transmitters and light-amplification circuits, a theme amplified by growing 1550 nm deployment.

Rotary-wing aircraft provided 63% of total shipments in 2024, favored for their hover stability, vertical takeoff, and precision positioning around structures. Hybrid VTOL craft, though newer, combine those control benefits with fixed-wing cruise efficiency, allowing operators to surveil corridors exceeding 50 km on a single battery. Fixed-wing designs now include modular nose cones and wing hardpoints capable of hosting dual-sensor payloads, expanding survey productivity per flight hour.

The LiDAR drone market continues to value rotary-wing versatility for cell-tower, facade, and confined-site mapping, yet rising insurance premiums tied to hover time encourage operators to consider fixed-wing sorties where terrain allows launch and recovery strips. Manufacturers answer with quick-swap airframe kits enabling crews to redeploy the same sensor stack across platform types within a single shift, blurring historical boundaries between product classes.

Lidar Drones Market Report is Segmented by Component (Laser Scanners, 905 Nm Mechanical, and More), Product Form-Factor (Rotary-Wing, Fixed-Wing, and More), Operating Altitude (Very-Low, Low, and More), Range (Short, Medium, and More), Service Model (Hardware Sales, Turn-Key LiDAR-As-A-Service, and More), Application (Precision Agriculture, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved 35.7% of global revenues in 2024, benefiting from established BVLOS waiver pathways, robust GNSS correction grids, and federal methane-leak rules that specify 100 kg/h detection thresholds. Energy majors fund fleet rollouts to meet EPA compliance, and state DOTs allocate capital to scan bridges and roads ahead of rehabilitation cycles. Trimble's Q1 2025 USD 841 million earnings reveal sustained instrument demand tied to machine control and survey automation.

Asia-Pacific holds 22% share yet records the steepest growth slope, propelled by China's LiDAR production scale and India's infrastructure build-out. Hesai alone shipped 195,818 sensors in Q1 2025, underlining regional manufacturing muscle. India's public-private corridors embrace drone mapping for land acquisition and progress tracking, while Japan subsidizes local government rice-field surveys. BVLOS harmonization lags across ASEAN, tempering offshore pipeline and power-line reconnaissance expansion.

Europe benefits from uniform air-space provisions under EASA's Open-category, stimulating micro-platform uptake for urban surveying and cultural-heritage archiving. Hexagon reported EUR 564.9 million (USD 664.64 million) recurring revenue for Q3 2024, signaling strong digital reality adoption despite macro headwinds. Single-photon advances promise efficient national mapping, and the Green Deal's biodiversity targets feed demand for forestry and habitat LiDAR baselines.

- DJI

- Leica Geosystems (Hexagon)

- RIEGL Laser Measurement

- Velodyne / Ouster

- Phoenix LiDAR Systems

- YellowScan SAS

- FARO Technologies

- Teledyne Optech

- Trimble Inc.

- Sick AG

- Microdrones GmbH

- senseFly SA

- Terra Drone Corp.

- Innoviz Technologies

- Luminar Technologies

- Parrot Drone SAS

- GeoCue Group Inc.

- Cepton Technologies

- Robosense (LeiShen)

- Topodrone LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Break-even of solid-state LiDAR cost < USD 400 enabling mass-market drones

- 4.2.2 Surge in sub-250 g "micro-mapping" drones driven by EU Open-category rules

- 4.2.3 Integration of bathymetric LiDAR on VTOL drones for shallow-water asset surveys

- 4.2.4 Cloud-native SLAM/AI point-cloud pipelines reducing post-processing lead-time

- 4.2.5 60 % Oil-and-gas methane-leak detection mandates in N. America using LiDAR UAVs

- 4.2.6 African corridor finance (Af CFTA) favouring drone-based topo surveys over manned aircraft

- 4.3 Market Restraints

- 4.3.1 EMI compliance hurdles for 1550 nm lasers on multi-payload rigs

- 4.3.2 Fragmented air-traffic management delaying BVLOS permits in ASEAN

- 4.3.3 Carbon-battery transport regulations raising logistics cost for service providers

- 4.3.4 Limited GNSS correction infrastructure in Caribbean island nations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Industry Value-Chain Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Laser Scanners

- 5.1.2 905 nm Mechanical

- 5.1.3 905 nm MEMS

- 5.1.4 1550 nm Fiber

- 5.1.5 Navigation and Positioning Systems

- 5.1.6 Inertial Measurement Units

- 5.1.7 Cameras

- 5.1.8 Power and Thermal Modules

- 5.1.9 Other Components

- 5.2 By Product Form-Factor

- 5.2.1 Rotary-Wing

- 5.2.2 Fixed-Wing

- 5.2.3 Hybrid VTOL

- 5.3 By Operating Altitude

- 5.3.1 Very-Low (<120 m)

- 5.3.2 Low (120-300 m)

- 5.3.3 Medium (300-500 m)

- 5.4 By Range

- 5.4.1 Short (<100 m)

- 5.4.2 Medium (100-500 m)

- 5.4.3 Long (>500 m)

- 5.5 By Service Model

- 5.5.1 Hardware Sales

- 5.5.2 Turn-key LiDAR-as-a-Service

- 5.5.3 Analytics SaaS

- 5.6 By Application

- 5.6.1 Construction and Infrastructure

- 5.6.2 Environment and Forestry

- 5.6.3 Precision Agriculture

- 5.6.4 Corridor Mapping (Road, Rail, Pipeline)

- 5.6.5 Mining and Quarrying

- 5.6.6 Defense and Security

- 5.6.7 Disaster Management and Insurance

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia

- 5.7.4 Middle East

- 5.7.4.1 Israel

- 5.7.4.2 Saudi Arabia

- 5.7.4.3 United Arab Emirates

- 5.7.4.4 Turkey

- 5.7.4.5 Rest of Middle East

- 5.7.5 Africa

- 5.7.5.1 South Africa

- 5.7.5.2 Egypt

- 5.7.5.3 Rest of Africa

- 5.7.6 South America

- 5.7.6.1 Brazil

- 5.7.6.2 Argentina

- 5.7.6.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global?level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 DJI

- 6.4.2 Leica Geosystems (Hexagon)

- 6.4.3 RIEGL Laser Measurement

- 6.4.4 Velodyne / Ouster

- 6.4.5 Phoenix LiDAR Systems

- 6.4.6 YellowScan SAS

- 6.4.7 FARO Technologies

- 6.4.8 Teledyne Optech

- 6.4.9 Trimble Inc.

- 6.4.10 Sick AG

- 6.4.11 Microdrones GmbH

- 6.4.12 senseFly SA

- 6.4.13 Terra Drone Corp.

- 6.4.14 Innoviz Technologies

- 6.4.15 Luminar Technologies

- 6.4.16 Parrot Drone SAS

- 6.4.17 GeoCue Group Inc.

- 6.4.18 Cepton Technologies

- 6.4.19 Robosense (LeiShen)

- 6.4.20 Topodrone LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment