|

시장보고서

상품코드

1851316

북미의 휴먼 머신 인터페이스 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)North America Human Machine Interface - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

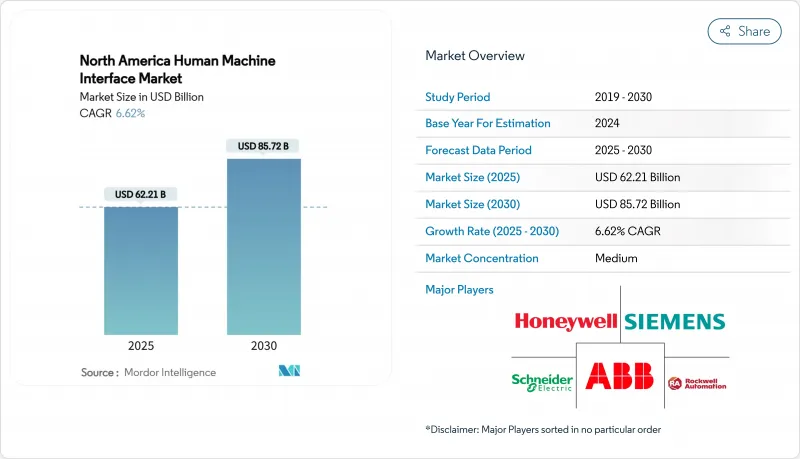

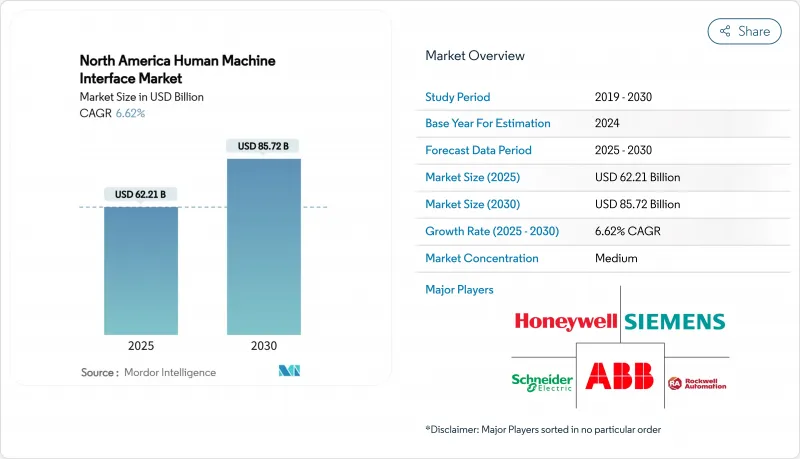

북미의 휴먼 머신 인터페이스 시장은 2025년 622억 1,000만 달러에 이르고, 2030년에는 857억 2,000만 달러에 달하며, CAGR 6.62%를 나타낼 것으로 예측됩니다.

이 지역의 인더스트리 4.0 추진, 사설 5G 배포, OSHA-NIST 사이버 물리적 규칙의 엄격화로 수요가 확대되고 제조업체는 레거시 운영자 패널을 안전한 데이터 중심 시스템으로 대체해야 합니다. 현대 공장에서는 HMI가 단순히 기계 상태를 전달할 뿐만 아니라 실시간 생산 데이터를 클라우드 분석에 스트리밍할 것으로 기대하고 있으며, 이 기대는 이산 및 공정 산업 전반의 조달 전략을 바꾸고 있습니다. 반도체공급 부족과 OT-IT 통합의 인력 부족이 당면의 부족이 되는 한편, EV 배터리의 기가팩토리를 비롯한 새로운 생산 능력 증강이, 다년간에 걸친 프로젝트·파이프라인을 계속 지지하고 있습니다. 그 결과, 하드웨어, 소프트웨어, 사이버 보안 기능을 융합한 벤더가, 북미의 휴먼 머신 인터페이스 시장에서 우위한 경쟁력을 차지하고 있습니다.

북미의 휴먼 머신 인터페이스 시장 동향과 인사이트

미국의 이산 제조에서 Industry 4.0 도입 증가는 커넥티드 머신 인터페이스 수요를 촉진

자동차, 일렉트로닉스 및 패키지 제품 라인의 공장 관리자는 현재 PLC 로직, MES 트랜잭션 및 품질 분석을 하나의 HMI 산하에 통합하는 단일 데이터 패브릭 전략을 추구하고 있습니다. 2025년 헤르메스 상을 수상한 지멘스의 Industrial Copilot은 코드의 견고성을 높이면서 엔지니어링 시간을 줄이는 제네레이티브 AI를 통합하고 있습니다. 포드는 루이빌의 조립 공장 전체에 소프트웨어 정의 SIMATIC Automation Workstation을 통합하여 생산 셀을 며칠이 아닌 몇 시간 내에 재구성할 수 있도록 했습니다. 중견 수탁 제조 기업에서의 유사한 도입은 고정 기능 패널에서 예측 유지 보수 및 에너지 최적화를 지원하는 확장 가능하고 소프트웨어 중심의 HMI로의 구조적 변화를 보여줍니다. 이러한 업그레이드는 북미의 휴먼 머신 인터페이스 시장의 대응 가능한 기반을 직접 확장합니다.

OSHA와 NIST 사이버 피지컬 컴플라이언스 지침이 HMI 업그레이드를 지원

규제 당국은 현재 보호되지 않은 HMI를 안전 위험으로 취급합니다. OSHA는 NIST SP 800-82를 참조하여 제약 회사 및 화학 회사에 원격 액세스 포인트를 강화하고 다중 요소 인증을 구현하도록 촉구합니다. 2024년 CISA 권고에서는 널리 배포되는 운영자 스테이션에 SQL 주입 결함이 있음을 지적했으며, 기업은 지원되지 않는 버전을 폐기하도록 촉구했습니다. 컴플라이언스 위반 비용은 현대화 예산을 능가하며 자본은 암호화된 프로토콜과 역할 기반 액세스로 향합니다. IEC 62443 표준에 패널을 사전 인증하는 공급업체는 북미의 휴먼 머신 인터페이스 시장 전반에 걸쳐 시장 이상 성장을 보고합니다.

레거시 HMI 통신 프로토콜에 뿌리를 둔 취약점

CISA의 2025년 카탈로그는 패치되지 않은 단말기에서 원격 코드 실행을 가능하게 하는 modbus-TCP와 DNP3의 취약성을 강조하고 있으며, 플랜트의 OT 위험에 대한 이사회 수준의 모니터링을 강화하고 있습니다. 북미 시설의 대부분은 여전히 에어 갭 일루전에 의존하고 있기 때문에 새로 공개된 취약성이 노후화된 패널의 교환 계획을 가속화하고 있습니다. 그러나, 브라운필드 배선의 복잡성과 라인 정지를 연출할 필요성이 더해져, 완전한 이행은 늦어지고 있습니다.

부문 분석

2024년 프로그래머블 로직 컨트롤러 시장 규모는 174억 2,000만 달러로 총 지출의 28%를 차지했습니다. MES 플랫폼은 규모가 작은 것, 폐쇄 루프 품질과 실시간 원가 계산에 대한 축족을 반영하여 2030년까지 매년 9.5% 성장합니다. 공급업체는 모션, 안전, 에지 애널리틱스를 차세대 PLC에 통합하여 캐비닛 설치 공간을 줄이는 동시에 엔터프라이즈 클라우드로의 데이터 처리량을 확대합니다. 일렉트로닉스 분야의 조기 도입 기업은 PLC 태그를 MES 대시보드에 통합한 후 12% 이상의 스크랩 삭감을 목표로 하고 있습니다. 프로세스 산업에서는 SCADA와 DCS 솔루션이 아성을 유지하면서 CFO는 자본 투자를 OPEX로 변환하는 구독 모델을 선호하기 때문에 클라우드 호스트의 HMI 소프트웨어가 영구 라이선스를 초과합니다. 이러한 기술의 수렴으로 기술은 공식하지 않고 상호 운용되고 북미의 휴먼 머신 인터페이스 시장의 각 레이어에서 단계적인 성장을 유지하고 있습니다.

현재 엔지니어링 변경이 즉시 제조 현장에 반영되도록 PLM 데이터와 운영자 인터페이스를 연계시키는 프로젝트가 증가하고 있습니다. 자동차 OEM은 CAD 개정이 HMI의 작업 지시서에 자동으로 반영됨으로써 엔지니어링 변경 롤아웃에 걸리는 일수가 2일 단축된 것을 들고 있습니다. 오픈소스 OPC UA over TSN은 일반적인 프로토콜로 보급되어 커스텀 미들웨어 비용을 18% 절감했습니다. 이러한 진보를 종합하면 제조업체는 북미 휴먼 머신 인터페이스 시장을 단순히 패널 수로 판단하는 것이 아니라 데이터를 실용적인 재무 결과로 변환하는 능력으로 판단하고 있음을 알 수 있습니다.

터치스크린 패널은 IP-65의 하우징과 범용 예비 부품 에코시스템이 입증되었기 때문에 2024년에는 북미의 휴먼 머신 인터페이스 시장의 26%를 차지했습니다. 그러나 모바일 및 웨어러블 인터페이스는 사설 5G의 성숙에 따라 연률 9.1%의 성장을 이룰 것으로 보입니다. 항공우주산업의 조립공장에서의 초기 전개는 검사관이 토크 사양과 공차를 오버레이 표시하는 AR 대응 스마트 글라스를 사용함으로써 패스트 피스 승인이 30% 빠르다는 것을 보여줍니다. 산업용 PC에는 NVIDIA GPU가 탑재되어, 비전 용도를 디바이스상에서 직접 실행할 수 있게 되어, 별도의 서버가 불필요하게 되었습니다. 키패드 모델은 폭발하기 쉬운 장소나 장갑을 끼운 채로 조작하는 장소에서도 적절하고 계속 촉각에 의한 확인이 오클릭을 방지합니다. 음성 제어의 HMI는 금속 성형 라인에서는 배경 노이즈가 장벽이 되고 있는 것, 조금씩 전진하고 있습니다.

중앙 패널은 안전 연동을 관리하고 운영자는 중요하지 않은 조정을 위해 태블릿을 휴대합니다. 결과적으로 인터페이스의 메쉬는 중복성으로 인해 가동 시간을 향상시킵니다. 패널이 고장나도 인증된 모바일 장치에서 라인을 조깅할 수 있습니다. 이러한 구성은 조달 범위를 넓히고, 디바이스 패밀리에 걸친 사이버 보안 인증의 지명도를 높이고, 북미의 휴먼 머신 인터페이스 시장 전체에서 벤더의 차별화를 강화합니다.

북미의 휴먼 머신 인터페이스 시장은 기술별(프로그래머블 로직 컨트롤러, SCADA 등), 구성 요소별(통신 부문, 제어 디바이스 등), 인터페이스별(터치 스크린, 키패드 등), 최종 사용자 산업별(자동차, 석유 및 가스 등), 국가별(미국, 캐나다)로 분류됩니다. 시장 규모와 예측은 달러로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 미국의 디스크리트 제조업에 있어서 인더스트리 4.0 도입 증가가 커넥티드·머신·인터페이스 수요를 촉진

- HMI 업그레이드를 뒷받침하는 OSHA와 NIST 사이버 피지컬 컴플라이언스의 의무화

- 미국 멕시코 걸프와 앨버타의 오일 샌드에서 노후화된 프로세스 플랜트의 개수

- 스마트 공장에서 실시간 HMI를 가능하게 하는 프라이빗 5G 네트워크 배포

- 이중 언어 HMI 패널 채택을 가속화하는 다국어 노동력 요구 사항

- 고급 인터페이스 솔루션이 필요한 북미 EV 배터리 기가 공장 확대

- 시장 성장 억제요인

- 사이버 보안의 우려를 높인다 레거시 HMI 통신 프로토콜의 취약성

- OT-IT 통합의 인력 부족이 심각해지고 도입 스케줄 증대

- 컨트롤러와 디스플레이의 리드 타임 급증을 일으키는 반도체 공급의 혼란

- 엄격한 FDA 재검증 비용이 제약 공장의 빈번한 업그레이드를 방해

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 분석(스마트 제조 인터페이스의 설비 투자 동향)

제5장 시장 규모와 성장 예측

- 기술별

- 프로그래머블 로직 컨트롤러(PLC)

- 모니터링 제어 및 데이터 수집(SCADA)

- 기업 자원 계획(ERP)

- 분산 제어 시스템(DCS)

- 휴먼 머신 인터페이스(HMI) 소프트웨어

- 제품 수명 주기 관리(PLM)

- 제조 실행 시스템(MES)

- 기타 기술

- 인터페이스 유형별

- 터치스크린 조작 패널

- 산업용 PC(패널 및 박스)

- 키패드/기능키 HMI

- 모바일 및 웨어러블 HMI

- 음성 및 AR 지원 HMI

- 구성 요소별

- 통신 부문

- 제어장치

- 머신 비전 시스템

- 로봇 공학

- 센서

- 기타 부품

- 최종 사용자 업계별

- 자동차

- 석유 및 가스

- 화학 및 석유화학

- 제약

- 식음료

- 금속 및 광업

- 기타 산업

- 국가별

- 미국

- 캐나다

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- Emerson Electric Company

- Fanuc Corporation

- General Electric Company

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Incorporated

- Yokogawa Electric Corporation

- Omron Corporation

- Advantech Co., Ltd.

- Beijer Electronics Group

- Red Lion Controls(Spectris plc)

- Maple Systems Inc.

- BandR Industrial Automation GmbH(ABB Group)

- Phoenix Contact GmbH and Co. KG

- Keyence Corporation

- Parker Hannifin Corporation

- Eaton Corporation plc

- Lenze SE

제7장 시장 기회와 향후 전망

KTH 25.11.12The North America human machine interface market reached USD 62.21 billion in 2025 and is forecast to touch USD 85.72 billion by 2030, advancing at a 6.62% CAGR.

Demand scales with the region's push toward Industry 4.0, private 5G roll-outs, and stricter OSHA-NIST cyber-physical rules that force manufacturers to replace legacy operator panels with secure, data-centric systems. Modern plants now expect an HMI to stream real-time production data into cloud analytics rather than simply relay machine status, and this expectation is changing procurement strategies across discrete and process industries. Semiconductor shortages and the lack of OT-IT integration talent form a near-term drag, yet fresh capacity build-outs-especially EV battery gigafactories-continue to anchor multi-year project pipelines. Consequently, vendors that blend hardware, software, and cybersecurity functions occupy a premium competitive position in the North America human machine interface market.

North America Human Machine Interface Market Trends and Insights

Increasing Industry 4.0 adoption in U.S. discrete manufacturing driving demand for connected machine interfaces

Plant managers in automotive, electronics, and packaged-goods lines now pursue single data fabric strategies that unify PLC logic, MES transactions, and quality analytics under one HMI umbrella. Siemens' Industrial Copilot, honored with the 2025 Hermes Award, embeds generative AI that cuts engineering hours while boosting code robustness. Ford integrated the software-defined SIMATIC Automation Workstation across Louisville assembly to reconfigure production cells within hours, not days. Similar deployments across mid-sized contract manufacturers indicate a structural shift from fixed-function panels to scalable, software-centric HMIs that support predictive maintenance and energy optimization. These upgrades directly enlarge the addressable base of the North America human machine interface market.

OSHA and NIST cyber-physical compliance mandates boosting HMI upgrades

Regulators now treat unsecured HMIs as safety risks. OSHA citations reference NIST SP 800-82 controls, compelling pharmaceutical and chemical operators to harden remote-access points and implement multi-factor authentication. CISA advisories in 2024 flagged SQL injection flaws in widely deployed operator stations, pushing firms to retire unsupported versions. The cost of non-compliance dwarfs modernization budgets, shunting capital toward encrypted protocols and role-based access. Vendors that pre-certify panels to IEC 62443 standards report above-market growth across the North America human machine interface market.

Persistent vulnerabilities in legacy HMI communication protocols

CISA's 2025 catalog highlights modbus-TCP and DNP3 weaknesses that permit remote code execution on unpatched terminals, intensifying board-level scrutiny of plant OT risk. Because many North American facilities still rely on air-gap illusions, each newly disclosed exploit accelerates plans to replace aging panels. However, complexity of brown-field wiring, combined with the need to stage line outages, slows full migration.

Other drivers and restraints analyzed in the detailed report include:

- Retrofitting aging process plants in U.S. Gulf Coast and Alberta oil sands

- Deployment of private 5G networks enabling real-time HMI in smart factories

- Acute shortage of OT-IT integration talent inflating implementation timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The North America human machine interface market size for Programmable Logic Controllers stood at USD 17.42 billion in 2024 and retained a 28% share of total spending. MES platforms, although smaller, will grow 9.5% annually to 2030, reflecting a pivot toward closed-loop quality and real-time costing. Vendors integrate motion, safety, and edge analytics into new PLC generations, compressing cabinet footprint while expanding data throughput to enterprise clouds. Early adopters in electronics witness scrap reductions above 12% after unifying PLC tags with MES dashboards. While SCADA and DCS solutions maintain strongholds in process industries, cloud-hosted HMI software outsells perpetual licenses as CFOs prioritize subscription models that convert capex to opex. This technology convergence keeps technologies interoperating rather than cannibalizing, sustaining incremental growth in every layer of the North America human machine interface market.

A growing subset of projects now marries PLM data with operator interfaces so that engineering changes flow instantly to the shop floor. Automotive OEMs cite reductions of two days per engineering change roll-out when CAD revisions automatically populate HMI work instructions. Open-source OPC UA over TSN gains traction as common protocol, trimming custom middleware costs by 18%. Collectively, these advances underline how manufacturers judge the North America human machine interface market not simply on panel counts but on the capacity to convert data into actionable financial outcomes.

Touch-screen panels preserved 26% of the North America human machine interface market in 2024 due to their proven IP-65 housings and universal spare-parts ecosystems. Yet mobile and wearable interfaces will compound 9.1% per year as private 5G matures. Early roll-outs at aerospace assembly plants indicate 30% faster first-piece approvals when inspectors use AR-enabled smart glasses that overlay torque specs and tolerances. Industrial PCs now ship with NVIDIA GPUs, letting vision apps run directly on-device and eliminating separate servers. Keypad models stay relevant in explosive or gloved-hand zones, where tactile affirmations prevent mis-clicks. Voice-controlled HMIs inch forward, although background noise remains a barrier in metal-forming lines.

Hybrid deployments become common: a central panel governs safety interlocks while operators carry tablets for non-critical adjustments. The resulting interface mesh boosts uptime through redundancy; if a panel fails, the line can still be jogged from a certified mobile unit. Such configurations widen procurement scope and elevate the profile of cybersecurity certifications that span device families, reinforcing vendor differentiation across the North America human machine interface market.

The North America Human Machine Interface Market is Segmented by Technology (Programmable Logic Controller, SCADA and More), Component (Communication Segment, Control Device and More), Interface (Touchscreen, Keypad and More), End-User Industry (Automotive, Oil and Gas and More), and Country (United States, Canada). Market Size and Forecasts are Provided in USD.

List of Companies Covered in this Report:

- ABB Ltd.

- Emerson Electric Company

- Fanuc Corporation

- General Electric Company

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Incorporated

- Yokogawa Electric Corporation

- Omron Corporation

- Advantech Co., Ltd.

- Beijer Electronics Group

- Red Lion Controls (Spectris plc)

- Maple Systems Inc.

- BandR Industrial Automation GmbH (ABB Group)

- Phoenix Contact GmbH and Co. KG

- Keyence Corporation

- Parker Hannifin Corporation

- Eaton Corporation plc

- Lenze SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Industry 4.0 adoption in U.S. discrete manufacturing driving demand for connected machine interfaces

- 4.2.2 OSHA and NIST cyber-physical compliance mandates boosting HMI upgrades

- 4.2.3 Retrofitting ageing process plants in U.S. Gulf Coast and Alberta oil sands

- 4.2.4 Deployment of private 5G networks enabling real-time HMI in smart factories

- 4.2.5 Multilingual workforce requirements accelerating bilingual HMI panel adoption

- 4.2.6 Expansion of North American EV battery gigafactories requiring advanced interface solutions

- 4.3 Market Restraints

- 4.3.1 Persistent vulnerabilities in legacy HMI communication protocols raising cybersecurity concerns

- 4.3.2 Acute shortage of OT-IT integration talent inflating implementation timelines

- 4.3.3 Semiconductor supply disruptions causing controller and display lead-time spikes

- 4.3.4 Stringent FDA re-validation costs discouraging frequent upgrades in pharma plants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis (Capital Expenditure Trends in Smart Manufacturing Interfaces)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Programmable Logic Controller (PLC)

- 5.1.2 Supervisory Control and Data Acquisition (SCADA)

- 5.1.3 Enterprise Resource Planning (ERP)

- 5.1.4 Distributed Control System (DCS)

- 5.1.5 Human Machine Interface (HMI) Software

- 5.1.6 Product Lifecycle Management (PLM)

- 5.1.7 Manufacturing Execution System (MES)

- 5.1.8 Other Technologies

- 5.2 By Interface Type

- 5.2.1 Touch-Screen Operator Panels

- 5.2.2 Industrial PCs (Panel and Box)

- 5.2.3 Keypad / Function-Key HMIs

- 5.2.4 Mobile and Wearable HMIs

- 5.2.5 Voice- and AR-Enabled HMIs

- 5.3 By Component

- 5.3.1 Communication Segment

- 5.3.2 Control Device

- 5.3.3 Machine Vision Systems

- 5.3.4 Robotics

- 5.3.5 Sensors

- 5.3.6 Other Components

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Oil and Gas

- 5.4.3 Chemical and Petrochemical

- 5.4.4 Pharmaceutical

- 5.4.5 Food and Beverage

- 5.4.6 Metals and Mining

- 5.4.7 Other Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Emerson Electric Company

- 6.4.3 Fanuc Corporation

- 6.4.4 General Electric Company

- 6.4.5 Honeywell International Inc.

- 6.4.6 Mitsubishi Electric Corporation

- 6.4.7 Robert Bosch GmbH

- 6.4.8 Rockwell Automation Inc.

- 6.4.9 Schneider Electric SE

- 6.4.10 Siemens AG

- 6.4.11 Texas Instruments Incorporated

- 6.4.12 Yokogawa Electric Corporation

- 6.4.13 Omron Corporation

- 6.4.14 Advantech Co., Ltd.

- 6.4.15 Beijer Electronics Group

- 6.4.16 Red Lion Controls (Spectris plc)

- 6.4.17 Maple Systems Inc.

- 6.4.18 BandR Industrial Automation GmbH (ABB Group)

- 6.4.19 Phoenix Contact GmbH and Co. KG

- 6.4.20 Keyence Corporation

- 6.4.21 Parker Hannifin Corporation

- 6.4.22 Eaton Corporation plc

- 6.4.23 Lenze SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment