|

시장보고서

상품코드

1851333

석유 및 가스 자동화 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Oil & Gas Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

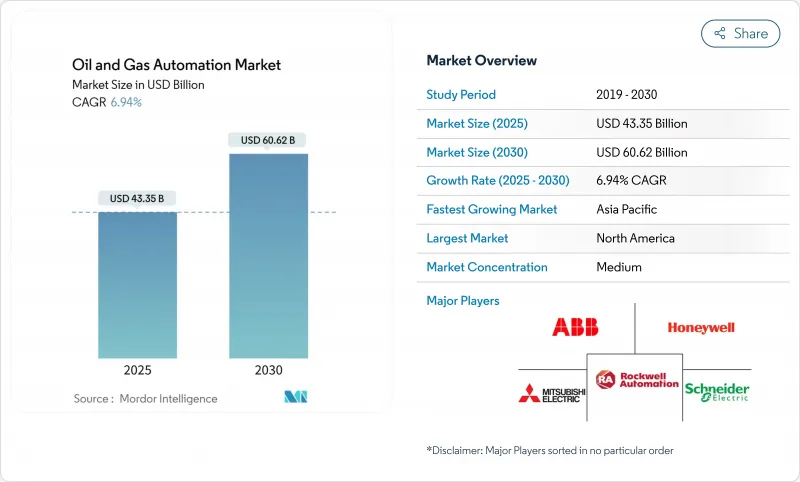

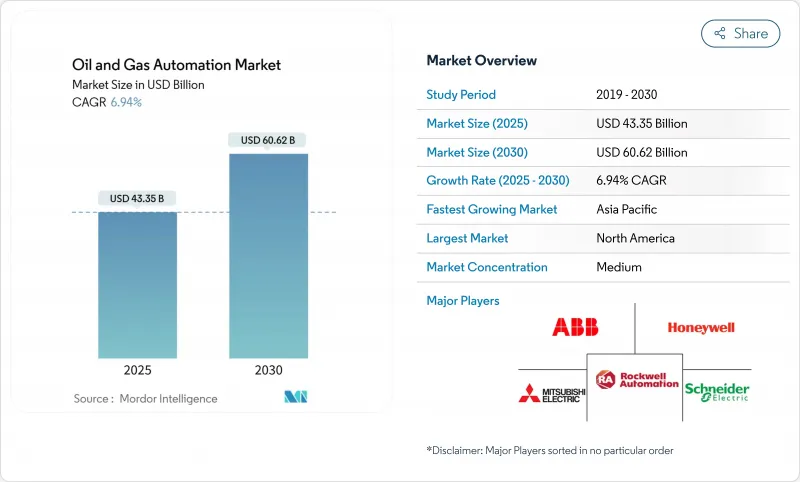

석유 및 가스 자동화 시장 규모는 2025년 433억 5,000만 달러에 이르고, 2030년에는 606억 2,000만 달러로 상승하며, 예측 기간 중 CAGR은 6.9%를 나타낼 전망입니다.

사업자는 공급망이 가까워지고 에너지 전환 목표가 강화되는 동안 다운타임을 억제하고 생산성을 향상시키기 위해 지능형 필드 플랫폼, 에지 AI 분석 및 자율 검사 도구를 도입하고 있습니다. 특히 IEC 61511과 ISA-84에 따른 안전 규제가 의무화되어 밀리초 단위로 위험에 대응하는 안전 계장 시스템의 도입이 가속되고 있습니다. 아시아태평양과 아프리카에서의 LNG 인프라의 확대는 고압, -160℃ 환경에 대응하는 극저온 등급 제어 시스템에 대한 새로운 수요를 끌어내고 있습니다. 마지막으로, 사업자가 랜섬웨어나 국가에 의한 공격에 대해 운용 기술(OT) 환경을 강화함에 따라 사이버 보안 예산이 증가하고 현재는 자동화 총 지출의 15-20%를 차지하게 되어 프로젝트의 경제성이 재구축되고 있습니다.

세계의 석유 및 가스 자동화 시장 동향과 인사이트

디지털 유전 플랫폼 채용 증가

실시간 디지털 플랫폼은 IoT 센서, 머신러닝 모델 및 클라우드 분석을 통합 대시보드에 융합하여 의사 결정주기를 몇 분에서 몇 초로 단축합니다. 데본에너지사는 AI에 의한 굴착조정을 도입한 후 갱정의 수명을 25% 연장했습니다. 라이브 운영 데이터와 동기화된 가상 트윈을 통해 엔지니어는 물리적 자산을 위험에 빠뜨리지 않고 시나리오를 테스트할 수 있습니다. 이 접근법은 다운홀 상태가 끊임없이 변화하는 비전통적인 저장층에서 특히 효과적입니다.

원격 모니터링 및 예측 유지 보수를 위한 현대화 CAPEX

운영자는 현장 방문을 줄이고 안전 노출을 줄이는 원격 모니터링 도구에 자본을 돌리고 있습니다. 엠브리지의 Azure 기반 파이프라인 분석은 위협 감지를 30% 개선했습니다. 예측 알고리즘이 진동과 열 동향을 조사하고 몇 주 전에 고장을 발견함으로써 신뢰성을 높이면서 정기 점검 비용을 최대 50% 절감했습니다.

원유 가격 변동이 OPEX 및 CAPEX 사이클에 영향

원유 가격 변동과 지출 이동 사이에 6개월의 시간 지연이 있기 때문에 소규모 생산자는 현금 흐름이 급박할 때 자동화 업그레이드를 지연시킬 수 없습니다. 요금 체계를 생산량에 맞추는 구독 기반의 자동화 서비스는 선행 리스크를 저감하고 불황시의 유동성을 유지하기 위해 지지를 모으고 있습니다.

부문 분석

이 소프트웨어는 2024년 매출의 66.7%를 차지하고 예지 보전과 자율적 운영을 강화하는 분석 엔진을 통해 석유 및 가스 자동화 시장을 지원했습니다. 금액 기준으로 이 구성 요소는 2024년 석유 및 가스 자동화 시장 규모의 289억 달러를 차지했습니다. 서비스는 규모가 작고 사업자가 AI 설정과 사이버 보안 강화를 아웃소싱하기 때문에 CAGR은 8.5%를 나타낼 것으로 예측되고 있습니다.

소프트웨어 성장은 드릴링 보급률을 35-45% 증가시키는 에지 AI 패키지로 강화됩니다. 한편, 24시간 모니터링과 성과 기반 보증을 번들한 서비스 계약은 공급자를 제품 공급자에서 성능 파트너로 이행시킵니다. 하드웨어는 센서 그리드나 견고한 에지 디바이스에 필수적인 것은 아니지만 가상화된 제어 로직이 소프트웨어 계층으로 이동함에 따라 점유율이 점차 감소할 것으로 예측됩니다.

업스트림 공정에서는 자율 드릴링 및 생산 최적화 플랫폼이 셰일 웰의 수천 개의 다운홀 파라미터를 보정하여 2024년 공정 수익의 59.1%를 벌어들였습니다. 이는 석유 및 가스 자동화 시장 규모의 약 256억 달러에 해당합니다. 중류 사업은 세계 LNG 터미널 건설 및 파이프라인 디지털화로 인해 규모는 작지만 CAGR 8.3%를 나타낼 전망입니다.

SLB와 같은 업스트림 회사는 1 래터럴에서 25회의 자동 지오스티어링 보정을 시연하여 완전 자율형 리그로의 변화를 시사했습니다. 중류 기업에서는 클라우드 링크된 SCADA 시스템을 통해 수천 킬로미터에 이르는 실시간 누수 감지 및 밸브 원격 조작이 가능하며 사고 대응 시간이 몇 시간에서 몇 분으로 단축됩니다. 하류 사업장에서는 에너지 사용량을 줄이고 배출량을 줄이는 AI 지향 증류탑을 시험적으로 도입하고 있습니다.

지역 분석

북미는 2024년 수익 점유율 37.1%로 석유 및 가스 자동화 시장을 선도해 AI 주도 굴착 및 패드 최적화의 선구자인 셰일 개발 기업에 지지를 받았습니다. 리그 수가 변동하더라도 학습 및 적용주기가 지속됨에 따라 이 지역의 생산성은 높게 유지됩니다. 이 지역의 사이버 보안 시스템도 성숙하고 있으며, 사업자는 연방 정부 가이드라인에서 의무화된 제로 트러스트 OT 프레임워크를 채택하고 있습니다.

아시아태평양의 2030년까지의 CAGR은 7.5%를 나타낼 전망입니다. 중국은 깨끗한 연료를 생산하기 위해 정유소의 현대화를 추진하고 있으며, 인도는 심해 광구에서 업스트림 디지털화를 가속화하고 있습니다. 동남아시아의 대규모 LNG 수입 프로젝트는 공급을 확보하고 간헐적인 재생에너지 및 전력망의 균형을 맞추기 위해 AI를 활용한 저온 제어를 의지하고 있습니다. 각국 정부는 배출량 억제와 안전성 강화를 위해 디지털 트윈을 지원하고 기술 채용을 추진하고 있습니다.

유럽은 엄격한 안전·환경규제 하에 안정된 지출을 유지합니다. 독일과 핀란드의 새로운 LNG 재기화 유닛은 SIL-3 안전 계층과 NIS 2.0 사이버 보안 지침을 충족하는 DCS 플랫폼을 통합합니다. 중동의 국영 석유회사는 정부 펀드의 지원을 받아 ADNOC의 9억 2,000만 달러의 ENERGYai 프로그램으로 대표되는 대로 성숙한 탄산염 저류층 전체에서 AI 주도의 갱정 모니터링을 확대하고 있습니다. 아프리카와 남미는 여전히 신흥 채용 기업이며, 기술 이전과 자금 조달을 위해 합작 파트너를 활용하는 경우가 많습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 디지털 유전 플랫폼의 채용 증가

- 원격 감시와 예지 보전을 위한 근대화 CAPEX

- 안전 시스템 규제의 의무화

- APAC와 아프리카에서 LNG와 미드스트림 건설

- 위험한 현장에서 실시간 분석을 위한 엣지 AI의 전개

- 해외 자산을 위한 자율 점검 드론과 로보틱스

- 시장 성장 억제요인

- 원유 가격 변동이 OPEX와 CAPEX 사이클에 미치는 영향

- 사이버 리스크와 OT 보안 컴플라이언스 비용 증가

- 고액의 자동화 초기 투자와 ROI의 불확실성

- 레거시 시스템의 상호 운용성

- 밸류체인 분석

- 기술의 전망

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자분석

- 거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 구성 요소별

- 하드웨어

- 소프트웨어

- 서비스

- 프로세스별

- 업스트림

- 미드스트림

- 다운스트림

- 기술별

- 센서 및 트랜스미터

- 분산 제어 시스템(DCS)

- 프로그래머블 로직 컨트롤러(PLC)

- 감시 제어 및 데이터 수집(SCADA)

- 안전 계장 시스템(SIS)

- 기타 기술

- 용도별

- 시추 및 완공

- 생산 및 유정 최적화

- 파이프라인 및 수송

- 정제 및 석유화학

- LNG 터미널 및 저장

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- Emerson Electric Co.

- Rockwell Automation Inc.

- Mitsubishi Electric Corp.

- Yokogawa Electric Corp.

- Eaton Corp.

- Dassault Systemes SE

- Bosch Rexroth AG

- Texas Instruments Inc.

- Johnson Controls International plc

- Halliburton Co.

- Schlumberger NV

- Baker Hughes Co.

- Weatherford International plc

- AVEVA Group plc

- Aspen Technology Inc.

- Flowserve Corp.

제7장 시장 기회와 향후 전망

KTH 25.11.12The oil & gas automation market size reached a value of USD 43.35 billion in 2025 and is set to climb to USD 60.62 billion by 2030, registering a 6.9% CAGR during the forecast period.

Operators are embracing intelligent field platforms, edge-AI analytics, and autonomous inspection tools to curb downtime and lift productivity as supply chains tighten and energy transition goals intensify. Mandatory safety regulations, especially those aligned with IEC 61511 and ISA-84, are accelerating uptake of Safety Instrumented Systems that respond to hazards in milliseconds. LNG infrastructure expansion across Asia-Pacific and Africa is unlocking new demand for cryogenic-grade control systems that handle high-pressure, -160 °C environments. Finally, growing cybersecurity budgets-now 15-20% of total automation spend-are reshaping project economics as operators harden operational technology (OT) environments against ransomware and state-sponsored attacks.

Global Oil & Gas Automation Market Trends and Insights

Rising Adoption of Digital-Oilfield Platforms

Real-time digital platforms fuse IoT sensors, machine-learning models, and cloud analytics into unified dashboards that shorten decision cycles from minutes to seconds. Devon Energy lifted well longevity by 25% after deploying AI-guided drilling adjustments. Virtual twins synchronised with live operating data let engineers test scenarios without risking physical assets, an approach that is especially potent in unconventional reservoirs where downhole conditions vary by the hour.

Modernisation CAPEX for Remote Monitoring and Predictive Maintenance

Operators are redirecting capital toward remote surveillance tools that cut site visits and shrink safety exposure. Enbridge's Azure-based pipeline analytics improved threat detection by 30%. Predictive algorithms study vibration and thermal trends to spot failures weeks in advance, trimming routine inspection costs up to 50% while boosting reliability.

Crude-Oil Price Volatility Impacting OPEX and CAPEX Cycles

Six-month lags between crude swings and spending shifts force smaller producers to delay automation upgrades when cash flows tighten. Subscription-based automation services that align fees with production volumes are gaining favour because they lower upfront risk and preserve liquidity during downturns.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Safety-System Regulations

- LNG and Mid-Stream Build-Out in Asia-Pacific and Africa

- Escalating Cyber-Risk and OT-Security Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 66.7% of 2024 revenue, anchoring the oil & gas automation market through analytics engines that power predictive maintenance and autonomous operations. In value terms, the component accounted for USD 28.9 billion of the oil & gas automation market size in 2024. Services, although smaller, are projected for an 8.5% CAGR as operators outsource AI configuration and cybersecurity hardening.

Software growth is reinforced by edge-AI packages that lift drilling rates of penetration by 35-45%. Meanwhile, service contracts that bundle 24-hour monitoring and outcome-based guarantees move providers from product suppliers to performance partners. Hardware remains essential for sensor grids and ruggedised edge devices; however, its share is expected to decline gradually as virtualised control logic migrates to software layers.

Upstream activities generated 59.1% of 2024 process revenue as autonomous drilling and production optimisation platforms calibrated thousands of downhole parameters at shale wells. This translated to roughly USD 25.6 billion of the oil & gas automation market size. Midstream operations, while holding a smaller base, are growing at 8.3% CAGR due to global LNG terminal build-outs and pipeline digitisation.

Upstream players like SLB demonstrated 25 automatic geosteering corrections on a single lateral, signalling a shift toward fully autonomous rigs. For midstream firms, cloud-linked SCADA systems enable real-time leak detection and remote valve actuation across thousands of kilometres, reducing incident response time from hours to minutes. Downstream sites are piloting AI-directed distillation columns that cut energy use and trim emissions.

The Oil & Gas Automation Market Report is Segmented by Component (Hardware, Software, and Services), Process (Upstream, Midstream, and Downstream), Technology (Sensors and Transmitters, Distributed Control Systems (DCS), and More), Application (Drilling and Completion, Production and Well Optimization, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the oil & gas automation market with 37.1% revenue share in 2024, buoyed by shale developers that pioneered AI-steered drilling and pad optimisation. Persistent learn-and-apply cycles keep regional productivity high even when rig counts fluctuate. The region's cybersecurity posture is also mature, with operators adopting zero-trust OT frameworks mandated by federal guidelines.

Asia-Pacific is poised for a 7.5% CAGR through 2030. China is modernising refineries to produce cleaner fuels, while India accelerates upstream digitisation across deep-water blocks. Massive LNG import projects in Southeast Asia rely on AI-enabled cryogenic controls to secure supply and balance power grids with intermittent renewables. Governments support digital twins to curb emissions and enhance safety, propelling technology adoption.

Europe maintains steady spending under stringent safety and environmental regulations. New LNG regasification units in Germany and Finland integrate DCS platforms that meet SIL-3 safety layers and NIS 2.0 cybersecurity mandates. Middle Eastern national oil companies, supported by sovereign funds, scale AI-driven well monitoring across mature carbonate reservoirs, exemplified by ADNOC's USD 920 million ENERGYai program. Africa and South America remain emerging adopters, often leveraging joint-venture partners for technology transfer and financing.

- ABB Ltd.

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- Emerson Electric Co.

- Rockwell Automation Inc.

- Mitsubishi Electric Corp.

- Yokogawa Electric Corp.

- Eaton Corp.

- Dassault Systemes SE

- Bosch Rexroth AG

- Texas Instruments Inc.

- Johnson Controls International plc

- Halliburton Co.

- Schlumberger NV

- Baker Hughes Co.

- Weatherford International plc

- AVEVA Group plc

- Aspen Technology Inc.

- Flowserve Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of digital-oilfield platforms

- 4.2.2 Modernization CAPEX for remote monitoring and predictive maintenance

- 4.2.3 Mandatory safety-system regulations

- 4.2.4 LNG and mid-stream build-out in APAC and Africa

- 4.2.5 Edge-AI deployment for real-time analytics at hazardous sites

- 4.2.6 Autonomous inspection drones and robotics for offshore assets

- 4.3 Market Restraints

- 4.3.1 Crude-oil price volatility impacting OPEX and CAPEX cycles

- 4.3.2 Escalating cyber-risk and OT-security compliance costs

- 4.3.3 High upfront automation expenditure and ROI uncertainty

- 4.3.4 Legacy-system interoperability

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Process

- 5.2.1 Upstream

- 5.2.2 Midstream

- 5.2.3 Downstream

- 5.3 By Technology

- 5.3.1 Sensors and Transmitters

- 5.3.2 Distributed Control Systems (DCS)

- 5.3.3 Programmable Logic Controllers (PLC)

- 5.3.4 Supervisory Control and Data Acquisition (SCADA)

- 5.3.5 Safety Instrumented Systems (SIS)

- 5.3.6 Other Technologies

- 5.4 By Application

- 5.4.1 Drilling and Completion

- 5.4.2 Production and Well Optimization

- 5.4.3 Pipeline and Transportation

- 5.4.4 Refining and Petrochemicals

- 5.4.5 LNG Terminals and Storage

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Honeywell International Inc.

- 6.4.3 Siemens AG

- 6.4.4 Schneider Electric SE

- 6.4.5 Emerson Electric Co.

- 6.4.6 Rockwell Automation Inc.

- 6.4.7 Mitsubishi Electric Corp.

- 6.4.8 Yokogawa Electric Corp.

- 6.4.9 Eaton Corp.

- 6.4.10 Dassault Systemes SE

- 6.4.11 Bosch Rexroth AG

- 6.4.12 Texas Instruments Inc.

- 6.4.13 Johnson Controls International plc

- 6.4.14 Halliburton Co.

- 6.4.15 Schlumberger NV

- 6.4.16 Baker Hughes Co.

- 6.4.17 Weatherford International plc

- 6.4.18 AVEVA Group plc

- 6.4.19 Aspen Technology Inc.

- 6.4.20 Flowserve Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment