|

시장보고서

상품코드

1851335

아민 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Amines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

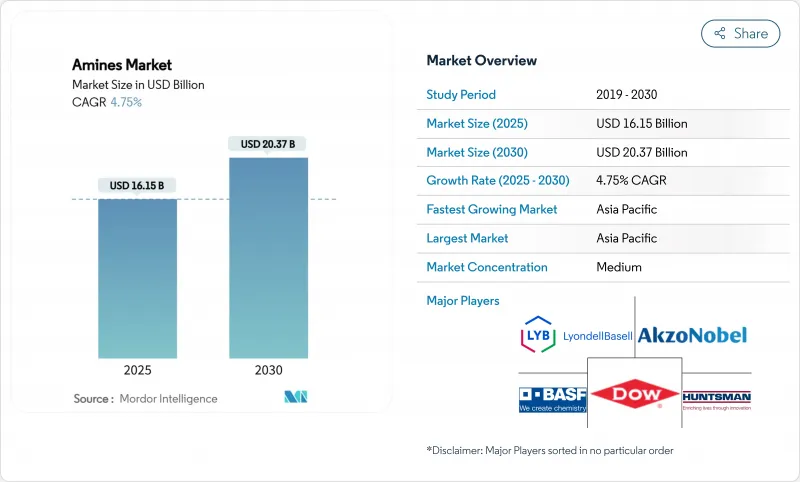

아민 시장 규모는 2025년에 161억 5,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 4.75%로 성장할 전망이며, 2030년에는 203억 7,000만 달러에 달할 것으로 예측됩니다.

이 지속적인 확대는 견조한 산업 수요, 보다 깨끗한 화학물질을 지지하는 환경 규제 강화, 탄소 포획용제와 같은 고가치 용도의 파이프라인 확대에 의해 지원되고 있습니다. 반도체 제조 투자 증가, 대규모 농업 근대화, 바이오 퍼스널케어 계면활성제의 광범위한 채택은 아민 시장의 수량과 금액 모두의 기회를 확대하고 있습니다. 생산자는 에너지 효율을 개선하고 재생 가능한 원료를 통합함으로써 암모니아와 에틸렌의 가격 변동을 다루는 한편, 주요 경제권에서 상승하고 있는 휘발성 유기 화합물 규제를 준수하고 있습니다. 주요 공급업체는 또한 차세대 칩에서 요구되는 까다로운 금속 사양을 충족하기 위해 초고순도 전자 제품의 생산 능력에 자본을 돌리고 있으며, 상품 생산에서 뛰어난 마진 잠재력을 제공하는 특수 솔루션으로 눈에 띄는 변화를 부각하고 있습니다.

세계의 아민 시장 동향 및 인사이트

아시아 퍼스널케어 포뮬레이터로부터 수요 급증

아미노산 계면활성제는 기존의 황산염계 계면활성제를 상회하여 2010년 이후 연평균 18%의 성장을 기록하고 있습니다. 아시아의 제제 제조업체는 저자극성이고 생분해성이 높은 글루탐산계와 알라닌산계를 주류로 하고 있으며, 아민계 제조업체는 국제적인 지속가능성과 탄소 인증(ISCC-PLUS)을 취득한 바이오 제품 라인의 확대를 강요하고 있습니다. Nouryon의 녹색 에틸렌 옥사이드와 에탄올 아민의 인증 생산은 플랜트 운영자가 클린 라벨 처방을 위해 포트폴리오를 재구성하는 방법을 보여줍니다. 동시에 다기능 아민 옥사이드는 샴푸, 바디 워시, 가정용 카테고리로 제조업체가 고발포이면서 온화한 프로파일을 추구하는 가운데 지보를 굳히고 있습니다. 중산계급 소비자가 100%에 가까운 천연 유래 지수를 자랑하는 제품에 끌려가는 가운데 아민 시장은 급성장하는 아시아의 클린 뷰티 에코시스템의 매우 중요한 실현자로서의 역할을 더욱 깊게 해 나갈 것으로 보입니다.

신흥 농업 허브에서 농약의 급속한 보급

아시아태평양과 남미에서는 현대적인 농법이 정밀한 화학 투입을 필요로 하고, 아민 기반의 농약염 및 유화제 수요를 인상하고 있습니다. 재생 가능한 전력을 동력원으로 하는 새로운 분산형 암모니아 플랜트는 특히 브라질과 인도에서 물류 비용을 낮추고 지역 공급 안정성을 향상시킵니다. CF 인더스트리즈와 POET사에 의한 저탄소 암모니아 비료의 파일럿 시험은 그린 수소 경로를 통합함으로써 농학적 및 지속가능성 이익을 입증하고 있습니다. 이러한 개발은 제초제, 살충제, 종자 처리제에 사용되는 에탄올 아민, 알킬 아민, 지방족 아민의 장기적인 오프테이크를 강화합니다.

비 목재 종이 및 디지털 문서로 이동

선진국의 사무용지 소비 감소는 아민계 펄프 표백제 및 종이용 코팅제 수요를 줄이고 있습니다. 각 회사는 장기적인 발목을 완화하기 위해 성장이 현저한 퍼스널케어 및 건축 분야에 판매량을 돌리고 있습니다. BASF가 기존의 아민자산을 특수화학용으로 재조합하기로 결정한 것은 이 구조 변화에 대한 업계의 적극적인 조정을 부각시키고 있습니다.

부문 분석

에탄올 아민은 가스 감미료, 퍼스널케어용 계면활성제, 부식방지제에 필수적인 역할을 하기 위해 2024년 아민 시장 전체의 42.55%를 차지했습니다. 천연가스 처리 및 트리에탄올 아민을 기반으로 하는 시멘트 첨가제로부터의 안정적인 수요는 탄소 포획 용매의 새로운 용도가 출현하더라도 견고한 기준선을 지원합니다. 이 부문은 규모가 크므로 주요 공급업체는 에톡실레이트에서 모르폴린에 이르는 유도체 체인 전체에서 비용 경쟁력과 비즈니스 시너지를 발휘합니다. 이와는 대조적으로 일렉트로닉스, 의약품, 첨단 복합재료 등의 틈새 용도에 밀려, 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠르게 5.01%를 보일 것으로 예측되는 것은 특수한 아민입니다.

생산자는 고순도 모르폴린, 디아민, 키랄아민 중간체 사이의 신속한 전환이 가능한 다목적 반응기를 설치하고 있습니다. 난징에서 에보닉의 확장은 이 고부가가치 분자에 축발을 보여줍니다. 동시에, 재생가능한 원료로 90%의 수율을 달성하는 루테늄 및 트리포스 촉매와 같은 학술적인 돌파구는 특수 등급의 지속가능한 원료 풀을 확대할 것을 약속합니다. 에탄올 아민의 규모와 특수 아민 성장의 상호 작용은 아민 시장의 균형 잡힌 장기 궤도를 지원합니다.

지역 분석

아시아태평양은 2024년 세계 매출의 38.91%를 창출했고, 2030년까지 연평균 복합 성장률(CAGR) 5.88%로 확대할 전망이며, 두 리더적 지위를 유지했습니다. 중국의 4,552만 톤의 암모니아 생산 능력은 이 지역의 원료 측면에서 우위를 뒷받침합니다. Alkyl 아민과 Balaji 아민을 포함한 인도의 특수 화학 챔피언은 20개 이상의 공장을 운영하고 비용 경쟁력있는 제조를 무기로 100개국 이상으로 수출하고 있습니다. 대만, 한국, 중국 본토에서는 반도체 확대가 일렉트로닉스급 아민 수요를 끌어올리고, 아세안 국가에서는 의약품, 농업 화학제품, 가정용 제품으로 더욱 성장하고 있습니다. BASF가 계획하고 있는 100억 달러의 Shanjiang Verbund 프로젝트는 재생 가능한 전력으로만 운영되며, 다국적 기업이 이 지역의 지속적인 업사이드를 어떻게 캡처하는지 보여줍니다.

북미는 성숙하면서도 전략적으로 중요한 클러스터로, 탄소 포획 시스템과 통합된 푸른 암모니아 시설에 대한 투자가 증가하고 있습니다. 미국은 2030년까지 암모니아 생산 능력을 4배로 확대할 것으로 예측됩니다. 이 확장은 국내 비료 공급을 보장하고 에탄올 아민과 우레아 유도체의 현지 원료 기반을 제공합니다. 한편 캐나다의 풍부한 수력 발전은 국내 시장 및 수출 시장 모두를 목표로 하는 저탄소 아민 생산의 경쟁국으로 자리매김하고 있습니다.

유럽은 계속해서 순환형 경제의 목표를 추구하고 바이오의 중간체와 에너지 효율이 높은 반응기의 기술 혁신을 추진하고 있습니다. Nouryon에 의한 녹색 에틸렌 옥사이드의 ISCC-PLUS 인증은 친환경 라벨이 붙은 계면활성제에 대한 지역 수요를 지원합니다. 유럽 위원회의 VOC 목표의 엄격화로 인해, 배합자는 기존의 휘발성 아민을 성능 기준을 충족하는 고인화점 유도체로 대체하도록 촉구되고 있습니다. 중동 및 아프리카는 천연가스 원료의 가용성으로 혜택을 누리고 있으며, 특히 사우디아라비아와 오만에서는 가격 경쟁력 있는 암모니아와 하류 아민 체인을 가능하게 합니다. 남미에서는 대두와 옥수수의 재배가 번성하고 브라질과 아르헨티나가 제초용 아민염의 안정된 소비를 확보하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아의 퍼스널케어 포뮬레이터 수요 급증

- 신흥 농업 거점에서의 농약의 급속한 보급

- 인프라 붐이 건설용 화학제품 촉진

- 첨단 반도체 공장용 일렉트로닉스 등급 아민

- 온사이트형 그린 수소 유래 아민의 파일럿 프로젝트

- 시장 성장 억제요인

- 비목재 종이 및 디지털 문서로의 시프트

- 휘발성 암모니아 및 에틸렌 원료의 가격 설정

- 아민 VOC 및 냄새 규제 강화

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- 현재의 기술

- 제올라이트 촉매 메틸아민 공정

- 이소부틸렌의 직접 아미노화

- 접촉 증류

- EDC의 암모놀리시스

- 향후 기술

- 현재의 기술

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 정도

- 가격 분석

- 생산 분석

제5장 시장 규모 및 성장 예측

- 유형별

- 에틸렌아민

- 알킬아민

- 지방아민

- 특수 아민

- 에탄올아민

- 최종 이용 산업별

- 고무

- 퍼스널케어 제품

- 청소 제품

- 접착제, 페인트 및 수지

- 아그로케미컬

- 석유 및 석유화학

- 기타 최종 용도

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Air Products and Chemicals, Inc.

- Akzo Nobel NV

- Alkyl Amines Chemicals Limited

- Arkema

- BASF SE

- Celanese Corporation

- Clariant

- Daicel Corporation

- Dow

- Eastman Chemical Company

- Huntsman International LLC

- INEOS

- Invista

- Kemipex

- LyondellBasell Industries Holdings BV

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- NIPPON SHOKUBAI CO., LTD.

- SABIC

- Solvay

- Tosoh Corporation

제7장 시장 기회 및 향후 전망

AJY 25.11.21The Amines Market size is estimated at USD 16.15 billion in 2025, and is expected to reach USD 20.37 billion by 2030, at a CAGR of 4.75% during the forecast period (2025-2030).

This sustained expansion is supported by resilient industrial demand, stricter environmental regulations that favor cleaner chemistries and a growing pipeline of high-value applications such as carbon-capture solvents. Rising investments in semiconductor fabrication, large-scale agricultural modernization and widespread adoption of bio-based personal-care surfactants are expanding both volume and value opportunities in the amines market. Producers are improving energy efficiency and integrating renewable feedstocks to manage volatile ammonia and ethylene prices while complying with emerging volatile organic compound limits across major economies. Leading suppliers are also channeling capital toward ultra-pure electronics-grade capacities to meet the stringent metal specifications required by next-generation chips, highlighting a visible shift from commodity production toward specialized solutions that offer superior margin potential.

Global Amines Market Trends and Insights

Surging Demand from Asian Personal-Care Formulators

Amino acid-based surfactants have outpaced traditional sulfate systems, recording 18% average annual growth since 2010. Asian formulators are mainstreaming glutamate and alaninate derivatives that offer low irritation and high biodegradability, forcing amine suppliers to expand bio-based lines with International Sustainability and Carbon Certification (ISCC-PLUS) credentials. Nouryon's certified production of green ethylene oxide and ethanolamines illustrates how plant operators are realigning portfolios toward clean-label formulations. In tandem, multifunctional amine oxides are gaining ground in shampoo, body-wash and household categories as manufacturers pursue high-foaming yet mild profiles. With middle-class consumers gravitating toward products boasting a natural-origin index approaching 100%, the amines market is set to deepen its role as a pivotal enabler of Asia's fast-growing clean-beauty ecosystem.

Rapid Pesticide Adoption in Emerging Agriculture Hubs

Modern farming practices in Asia Pacific and South America require precision chemical inputs, lifting demand for amine-based pesticide salts and emulsifiers. Novel decentralized ammonia plants powered by renewable electricity are lowering logistics costs and improving regional supply security, notably in Brazil and India. CF Industries and POET's pilot of low-carbon ammonia fertilizer demonstrates the agronomic and sustainability pay-off of integrating green hydrogen pathways. Such developments bolster long-term offtake for ethanolamines, alkylamines and fatty amines used in herbicides, insecticides and seed-treatment agents.

Shift to Wood-Free Paper & Digital Documentation

Declining office-paper consumption in developed economies is dampening demand for amine-based pulp bleaching agents and paper coatings. Companies are reallocating volumes toward faster-growing personal-care and construction segments to cushion the long-term drag. BASF's decision to reconfigure legacy amine assets toward specialty chemicals highlights the industry's proactive adjustment to this structural shift.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Boom Spurring Construction Chemicals

- Electronics-Grade Amines for Advanced Semiconductor Fabs

- Volatile Ammonia & Ethylene Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethanolamines captured 42.55% of the overall amines market in 2024, owing to their indispensable role in gas sweetening, personal-care surfactants and corrosion inhibitors. Steady demand from natural-gas treatment and triethanolamine-based cement additives underpins a robust baseline, even as newer uses in carbon-capture solvents emerge. The segment's scale gives leading suppliers cost leverage and operational synergies across derivative chains ranging from ethoxylates to morpholine. In contrast, specialty amines are projected to post the fastest 5.01% CAGR through 2030, propelled by niche applications in electronics, pharmaceuticals and advanced composites.

Producers are installing multipurpose reactors capable of quick changeovers between high-purity morpholines, diamines and chiral amine intermediates. Evonik's expansion in Nanjing exemplifies this pivot toward higher value-added molecules. Concurrently, academic breakthroughs such as ruthenium/triphos catalysts achieving 90% yields on renewable feedstocks promise to widen the sustainable feedstock pool for specialty grades. The interplay of scale in ethanolamines and growth in specialty amines underpins the balanced long-term trajectory of the amines market.

The Amines Market Report is Segmented by Type (Ethyleneamines, Alkylamines, Fatty Amines, Specialty Amines, Ethanolamines), End-Use Industry (Rubber, Personal Care Products, Cleaning Products, Adhesives/Paints/Resins, Agro-Chemicals, Oil/Petrochemicals, Other End-Uses), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained its dual leadership position, generating 38.91% of global revenue in 2024 and expanding at a 5.88% CAGR through 2030. China's 45.52 million t ammonia capacity anchors the region's raw-material advantage. India's specialty chemicals champions, including Alkyl Amines and Balaji Amines, operate more than 20 plants and export to over 100 countries, leveraging cost-competitive manufacturing. Semiconductor expansions across Taiwan, South Korea and mainland China are pushing demand for electronics-grade amines, while ASEAN nations add incremental growth through pharmaceuticals, agro chemicals and household products. BASF's planned USD 10 billion Zhanjiang Verbund project, powered entirely by renewable electricity, illustrates how multinationals intend to capture enduring regional upside.

North America represents a mature yet strategically vital cluster, with rising investments in blue ammonia facilities integrated with carbon-capture systems. The United States is expected to quadruple ammonia capacity by 2030. This expansion safeguards domestic fertilizer supply and provides a local feedstock base for ethanolamine and urea derivatives. Meanwhile, Canada's abundant hydropower positions it as a contender for low-carbon amine production targeting both domestic and export markets.

Europe continues to pursue circular-economy objectives, driving innovations in bio-based intermediates and energy-efficient reactors. Nouryon's ISCC-PLUS certification for green ethylene oxide supports regional demand for eco-labeled surfactants. The European Commission's stricter VOC targets are encouraging formulators to substitute conventional volatile amines with higher-flashpoint derivatives that meet performance criteria. The Middle East and Africa benefit from natural-gas feedstock availability, enabling competitively priced ammonia and downstream amine chains, especially in Saudi Arabia and Oman. South America's focus on soybean and corn cultivation assures steady consumption of herbicidal amine salts, with Brazil and Argentina leading uptake.

- Air Products and Chemicals, Inc.

- Akzo Nobel N.V.

- Alkyl Amines Chemicals Limited

- Arkema

- BASF SE

- Celanese Corporation

- Clariant

- Daicel Corporation

- Dow

- Eastman Chemical Company

- Huntsman International LLC

- INEOS

- Invista

- Kemipex

- LyondellBasell Industries Holdings B.V.

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- NIPPON SHOKUBAI CO., LTD.

- SABIC

- Solvay

- Tosoh Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand from Asian personal-care formulators

- 4.2.2 Rapid pesticide adoption in emerging agriculture hubs

- 4.2.3 Infrastructure boom spurring construction chemicals

- 4.2.4 Electronics-grade amines for advanced semiconductor fabs

- 4.2.5 On-site green-hydrogen-derived amines pilots

- 4.3 Market Restraints

- 4.3.1 Shift to wood-free paper and digital documentation

- 4.3.2 Volatile ammonia and ethylene feedstock pricing

- 4.3.3 Stricter amine VOC/odor regulations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Current Technologies

- 4.6.1.1 Zeolite-catalyzed methylamine processes

- 4.6.1.2 Direct amination of isobutylene

- 4.6.1.3 Catalytic distillation

- 4.6.1.4 Ammonolysis of EDC

- 4.6.2 Upcoming Technologies

- 4.6.1 Current Technologies

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Price Analysis

- 4.9 Production Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Ethyleneamines

- 5.1.2 Alkylamines

- 5.1.3 Fatty Amines

- 5.1.4 Specialty Amines

- 5.1.5 Ethanolamines

- 5.2 By End-use Industry

- 5.2.1 Rubber

- 5.2.2 Personal Care Products

- 5.2.3 Cleaning Products

- 5.2.4 Adhesives, Paints and Resins

- 5.2.5 Agro-Chemicals

- 5.2.6 Oil and Petrochemicals

- 5.2.7 Other End-uses

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Air Products and Chemicals, Inc.

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Alkyl Amines Chemicals Limited

- 6.4.4 Arkema

- 6.4.5 BASF SE

- 6.4.6 Celanese Corporation

- 6.4.7 Clariant

- 6.4.8 Daicel Corporation

- 6.4.9 Dow

- 6.4.10 Eastman Chemical Company

- 6.4.11 Huntsman International LLC

- 6.4.12 INEOS

- 6.4.13 Invista

- 6.4.14 Kemipex

- 6.4.15 LyondellBasell Industries Holdings B.V.

- 6.4.16 MITSUBISHI GAS CHEMICAL COMPANY, INC

- 6.4.17 NIPPON SHOKUBAI CO., LTD.

- 6.4.18 SABIC

- 6.4.19 Solvay

- 6.4.20 Tosoh Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment