|

시장보고서

상품코드

1851338

웨어러블 모션 센서 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Wearable Motion Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

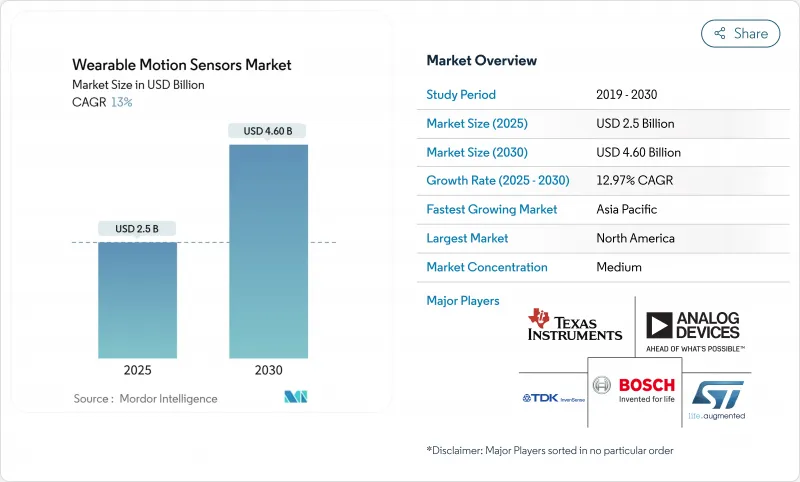

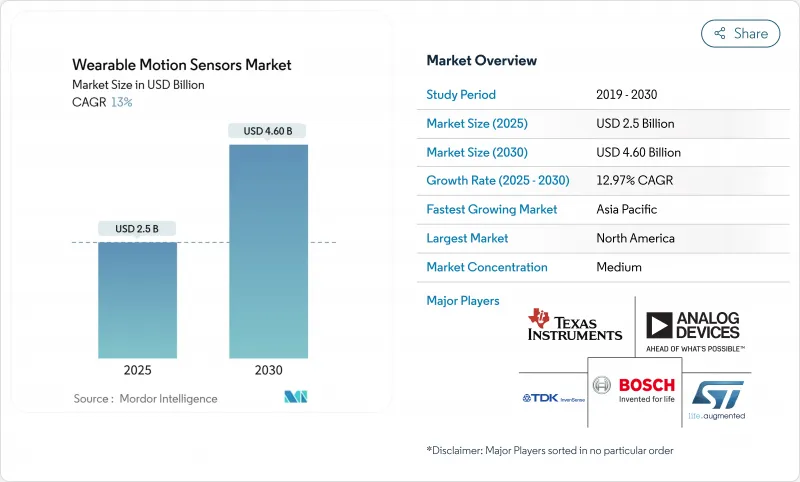

웨어러블 모션 센서 시장 규모는 2025년에 25억 달러, 2030년에는 46억 달러에 달할 것으로 예상되며, 기간 중 CAGR은 12.97%를 나타낼 전망입니다.

헬스케어, 소비자 일렉트로닉스, 산업 안전, 방위 분야에서의 채용 확대가 이 궤도를 유지하는 한편, 소형화와 온 디바이스 신호 처리의 획기적인 진보에 의해 과거에는 엉망이었던 컴퍼넌트가 커넥티드 제품의 필수 인에이블러로 변모합니다. 원격 환자 모니터링에 대한 규제 당국의 지원, 건강 지향 향상, 정확한 실시간 모션 데이터에 의존하는 원활한 휴먼 머신 인터페이스로의 전환으로 수요가 강화되고 있습니다. 시장 리더는 차별화를 도모하기 위해 센서 퓨전, 초저전력 설계, 엣지 AI를 중시하는 한편, 신흥 기업은 스마트 텍스타일이나 병사의 현대화 등 틈새 기회를 노리고 있습니다. MEMS 제조공급 측면 제약과 데이터 주권과 관련된 컴플라이언스 비용 증가는 적시에 생산 능력을 충족시키기 위해 가장 눈에 띄는 병목 현상이 되었습니다.

세계의 웨어러블 모션 센서 시장 동향과 인사이트

의료용 웨어러블을 견인하는 AI 대응 센서 퓨전

온센서 AI와 다축 관성 데이터의 통합은 소비자용 장치를 임상 등급 모니터로 변환하여 파킨슨병 및 기타 신경운동 장애와 관련된 미묘한 보행 및 떨림의 변화를 확실히 감지할 수 있게 합니다. 초기 파킨슨 병진전과 본태성 진전의 감별 정밀도가 84%에 달했다는 연구 보고도 있어, 재택에서의 지속적인 케어 모델을 확대해, 에피소드적인 임상 평가에의 의존을 경감하는 성과가 되고 있습니다. 알고리즘을 지원하는 진단에 대한 지불자 수락이 확대되고 병원 채용이 가속화되는 반면 소비자 브랜드는 의료 기능을 추가하여 생태계 계약 내 사용자를 유지합니다.

일본과 한국의 노인 의료용 서브 밀리와트 MEMS

전력 소비가 1mW 이하인 센서는 충전 없이 몇 주 동안 작동할 수 있으며, 장치의 유지보수를 잊을 수 있는 노인 사용자에게 필수 조건입니다. 이러한 센서에 의해 자동 전도 경보와 매일의 활동 프로파일링이 가능하게 되면, 일본의 전국 장기 간병 시스템에서는 입원이 23% 감소했습니다. 한국의 관민에 의한 시험 운용에서도 같은 절약 효과가 실증되고 있어, 지역 의료 네트워크 전체에의 스케일 업을 촉구해, 중국의 재택 고령화 대책에의 지역 수요의 파급을 촉구하고 있습니다.

떨림 감별 알고리즘적 한계

현재의 교사 없는 모델에서는 진전의 중증도를 복수 클래스로 분류하는 정밀도는 57.1%에 지나지 않고, 임상적인 역치를 크게 하회하고 있기 때문에 신경 웨어러블의 상환이 제한되고 있습니다. 작고 다양한 데이터 세트와 소음이 많은 실제 환경이 진보를 방해하여 유망한 연구 프로토타입에도 불구하고 병원으로의 도입이 늦어지고 있습니다.

부문 분석

웨어러블 모션 센서 시장에서 가속도계는 2024년에 32.4%의 점유율을 유지하며 활동량 트래커, 제스처 인터페이스, 기본적인 넘어짐 감지를 지원했습니다. 이 이점은 성숙한 비용 곡선과 마이크로암페어의 절전 전류를 반영합니다. 대조적으로, MEMS 콤보 센서는 가속도계, 자이로스코프 및 지자기 센서의 기능을 단일 ASIC에 통합하여 보드 레벨 집적도를 낮추고 CAGR 14.66%를 나타낼 전망입니다. 예를 들어, ST 마이크로 일렉트로닉스의 LSM6DSV16BX에는 6축 IMU와 히어러블 골전도 기반 명령용 오디오 가속도계가 내장되어 있습니다. 콤보의 채용에 의해 소비 전력을 억제하면서 이산 IMU와의 성능 차이를 줄일 수 있어 소형의 반지나 의료용 패치에 최적입니다.

자이로스코프는 AR/VR 헤드셋과 첨단 바이오메카닉스 분석에서도 이하의 방향 충실도를 지원합니다. 자력계는 GPS 다중 경로를 탐색하는 야외 스포츠 시계에 필수적인 절대 방위를 제공합니다. 압력 센서는 계단 위아래 카운트와 수영 랩 깊이에 대한 고도 변화를 교정하는 작지만 중요한 틈새 시장입니다. 미래의 로드맵은 생체 전위와 화학 채널이 운동축과 통합되어 관성 데이터와 생리적 데이터가 통합된 센서 노드에 집계되는 미래를 보여주며 웨어러블 모션 센서 시장이 더욱 강화될 것입니다.

피트니스 밴드는 확립된 브랜드 생태계, 낮은 진입 가격, 구독 애널리틱스 크로스셀링을 통해 2024년 용도 수익의 24%를 차지했습니다. 그러나 섬유에 내장된 센서사는 가젯에서 의복으로 모니터링을 변화시켜 2030년까지 연평균 복합 성장률(CAGR)을 14.91%를 나타낼 전망입니다. 전도사와 인쇄 스트레치 센서는 일상 생활에서 관절 운동학, 자세 및 호흡 수를 추적하는 셔츠를 허용하여 사용자를 전용 장치에서 해제합니다.

AR/VR 헤드셋은 몰입형 시뮬레이션을 위해 밀리초 이하의 레이턴시로 방위각을 갱신할 것을 요구하고 있으며, 계속해서 고성장을 계속하고 있습니다. 이어웨어는 핸즈프리 통화를 위해 헤드 제스처 감지를 통합하고 스마트 링은 작은 폼 팩터로 수면 연출을 실현합니다. 직물의 움직임과 전기화학 감지의 융합은 수분 공급, 전해질 손실, 열 응력 매개변수로 건강 대시보드를 확장하고 원활한 경험이 웨어러블 모션 센서 시장을 혁신의 단계를 넘어 계속 확장할 것을 강조합니다.

지역 분석

북미는 2024년 매출액의 42.7%를 차지하고 메디케어의 진료보수개혁에 의해 원격동작 모니터링이 주류가 되었습니다. 이 지역의 벤처 에코시스템은 에지 AI 실리콘에 자본을 쏟는 한편, 프라이버시에 관한 법규제는 사용자의 신뢰를 유지하기 위해 벤더를 디바이스상에서의 추론으로 향하게 합니다. 공급제약은 국내 MEMS 라인을 우대하는 니어쇼어링 정책과 국방생산법(Defense Production Act) 인센티브에 의해 완화되고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)이 16.91%로 가장 빠른 것은 아시아태평양입니다. 이는 에너지 수확 아키텍처를 채용하는 중국의 Tier2 팹과 노인 맨션에 모션 태그를 포함하는 한국의 스마트 시티 파일럿을 반영합니다. 정부 보조금이 원래의 부품 비용 상승을 상쇄하는 한편, 소비자의 기능 풍부한 웨어러블 단말에 대한 의욕은 쇠퇴를 보이지 않습니다. 일본 보험사는 스마트 셔츠를 기반으로 한 노인 리스크 스코어링을 환불하고 섬유 센서 투자에 박차를 가합니다.

유럽에서는 디지털 제품 여권의 의무화가 라이프사이클의 투명화를 촉진하고 프리미엄 애프터 판매 분석을 촉진하는 등 계획적인 확대가 계속되고 있습니다. GDPR(EU 개인정보보호규정) 대응으로 보안 엣지 펌웨어와 소블린 클라우드 브리지에 대한 투자가 증가. 라틴아메리카와 중동 및 아프리카는 도시의 사립 병원이 전도 검지 워치를 채용하는 것으로, 대수에서는 뒤를 차지하는 것, 2자리 성장을 달성합니다. 국경을 넘어서는 전자상거래와 다국적 OEM의 조립 라인은 각 지역을 세계 상호 의존하는 웨어러블 모션 센서 시장에 통합합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의료용 웨어러블을 견인하는 AI 대응 센서 퓨전

- 일본과 한국의 고령자 간병용 서브 밀리와트 MEMS

- 미국 RPM 상환 부스트

- EU 디지털 제품 여권 연동 이용 분석

- 중국의 초소형 에너지 수확 모듈

- NATO 병사의 근대화 수요

- 시장 성장 억제요인

- 트레머 차별화의 알고리즘적 한계

- MEMS 파운드리 생산 능력 부족

- 데이터 주권 준수 비용

- 스마트 텍스타일 인터커넥트의 실패

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 가속도계

- 자이로스코프

- 자력계

- 관성 측정 장치(IMU)

- MEMS 복합 센서

- 압력 센서

- 용도별

- 피트니스 밴드

- 활동 모니터

- 스마트 의류

- AR/VR 헤드셋

- 스마트 링 및 주얼리

- 이어웨어 및 보청기

- 최종 사용자 업계별

- 헬스케어 및 의료기기

- 소비자 가전 및 라이프스타일

- 산업 및 기업 안전

- 군사 및 방위

- 정부 및 유틸리티

- 소비 전력별

- 초저전력(1mW 미만)

- 저전력(1-10mW)

- 표준 전력(10-50mW)

- 고전력(50mW 이상)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Bosch Sensortec GmbH

- TDK InvenSense

- STMicroelectronics NV

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Panasonic Industry Co., Ltd.

- Infineon Technologies AG

- NXP Semiconductors NV

- Samsung Electronics Co. Ltd.

- Robert Bosch GmbH(Sensors)

- TE Connectivity

- Qualcomm Technologies Inc.

- Sensirion AG

- Xsens(Movella)

- Valencell Inc.

- OMRON Corporation

- Garmin Ltd.

- Polar Electro Oy

- Fitbit LLC(Google)

- Apple Inc.

- Oura Health Oy

- Xiaomi Corporation

- Goertek Inc.

- Huami(Zepp Health)

- Withings SA

제7장 시장 기회와 향후 전망

KTH 25.11.12The wearable motion sensors market size is valued at USD 2.5 billion in 2025 and is forecast to reach USD 4.6 billion by 2030, registering a 12.97% CAGR over the period.

Expanding adoption across healthcare, consumer electronics, industrial safety and defense sustains this trajectory, while breakthroughs in miniaturization and on-device signal processing convert once-discrete components into indispensable enablers of connected products. Demand is reinforced by regulatory support for remote patient monitoring, rising health-conscious consumer behavior, and the shift toward seamless human-machine interfaces that rely on precise real-time motion data. Market leaders emphasize sensor fusion, ultra-low-power design and edge AI to differentiate, whereas emerging players target niche opportunities such as smart textiles and soldier modernisation. Supply-side constraints in MEMS manufacturing and growing compliance costs tied to data sovereignty remain the most visible bottlenecks for timely capacity fulfilment.

Global Wearable Motion Sensors Market Trends and Insights

AI-enabled Sensor Fusion Driving Medical-Grade Wearables

Integrating on-sensor AI with multi-axis inertial data is converting consumer devices into clinical-grade monitors, enabling reliable detection of subtle gait or tremor changes linked to Parkinson's and other neuro-motor disorders. Studies report 84% accuracy in differentiating early Parkinson's tremor from essential tremor, an achievement that expands home-based, continuous care models and reduces reliance on episodic clinical evaluations. Growing payer acceptance of algorithm-supported diagnostics accelerates hospital adoption, while consumer brands add medical features to retain users within ecosystem subscriptions.

Sub-milliwatt MEMS for Eldercare in Japan & Korea

Sensors consuming below 1 mW allow multi-week operation without charging, a prerequisite for elderly users who may forget to maintain devices. Japan's national long-term care system saw 23% fewer hospitalisations when such sensors enabled automatic fall alerts and daily activity profiling. Korean public-private pilots demonstrate similar savings, encouraging scale-up across community health networks and driving regional demand spillover into China's ageing-at-home initiatives.

Algorithmic Limits on Tremor Differentiation

Current unsupervised models reach only 57.1% accuracy in multi-class tremor severity classification, well below clinical thresholds, limiting reimbursement for neurological wearables. Small, diverse data sets and noisy real-world environments hinder progress, slowing hospital uptake despite promising research prototypes.

Other drivers and restraints analyzed in the detailed report include:

- U.S. RPM Reimbursement Boost

- EU Digital Product Passport-Linked Usage Analytics

- MEMS Foundry Capacity Crunch

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The wearable motion sensors market saw accelerometers retain 32.4% share in 2024, underpinning activity trackers, gesture interfaces and basic fall detection. That dominance reflects mature cost curves and micro-amp sleep currents. In contrast, MEMS combo sensors post a 14.66% CAGR by fusing accelerometer, gyroscope and magnetometer functions within a single ASIC that off-loads board-level integration. STMicroelectronics' LSM6DSV16BX, for instance, embeds a 6-axis IMU plus an audio accelerometer for bone-conduction-based commands in hearables. Combo adoption narrows the performance gap with discrete IMUs while lowering power draw, ideal for tiny rings and medical patches.

Gyroscopes support sub-degree orientation fidelity in AR/VR headsets and advanced biomechanics analysis yet carry higher milliwatt budgets, so vendors pair duty-cycled modes with predictive algorithms to stretch per-charge runtime. Magnetometers deliver absolute heading, essential for outdoor sports watches navigating GPS multipath. Pressure sensors, a smaller but vital niche, calibrate altitude change for stair-climb counting and swimming lap depth. Forward-looking roadmaps integrate bio-potential or chemical channels alongside motion axes, signalling a future where inertial and physiological data converge inside unified sensor nodes, further strengthening the wearable motion sensors market.

Fitness bands led 24% of application revenues in 2024, benefiting from established brand ecosystems, low entry price and cross-selling of subscription analytics. However, textile-embedded sensor threads shift monitoring from gadget to garment, supporting a 14.91% CAGR through 2030. Conductive yarns and printed stretch sensors enable shirts that track joint kinematics, posture and respiratory rates during daily routines, freeing users from dedicated devices.

AR/VR headsets remain a high-growth enclave, demanding sub-millisecond latency orientation updates for immersive simulation. Ear-wear integrates head-gesture sensing for hands-free calls, while smart rings deliver sleep staging in tiny form factors. The convergence of motion and electrochemical sensing within fabrics widens health dashboards to hydration, electrolyte loss and thermal stress parameters, underscoring how seamless experiences keep the wearable motion sensors market expanding beyond novelty phases.

The Wearable Motion Sensor Market Report is Segmented by Type (Accelerometers, Gyroscopes, Magnetometers, and More), Application (Fitness Bands, Activity Monitors, Smart Clothing, and More ), End-User (Healthcare, Consumer Electronics, Industrial, Military, An More), Power Consumption (Ultra-Low Power (less Than 1mW), Standard Power (10-50mW), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.7% of 2024 revenue, anchored by Medicare reimbursement reform that locks remote motion monitoring into mainstream care pathways. The region's venture ecosystem funnels capital into edge-AI silicon, while privacy statutes push vendors toward on-device inference, preserving user trust. Supply constraints are mitigated by near-shoring policies and Defense Production Act incentives that favour domestic MEMS lines.

Asia Pacific registers the fastest 16.91% CAGR through 2030, reflecting China's tier-2 fabs embracing energy-harvesting architectures and Korea's smart-city pilots embedding motion tags in elder apartments. Government grants offset initial higher BOM costs, while consumer appetite for feature-rich wearables remains unabated. Japan's insurers reimburse smart-shirt-based risk scoring for seniors, spurring textile sensor investment.

Europe maintains methodical expansion, its Digital Product Passport mandate pushing life-cycle transparency and fostering premium after-sales analytics. GDPR compliance elevates spend on secure edge firmware and sovereign cloud bridges. Latin America and the Middle East & Africa trail in volumes yet notch double-digit growth where urban private hospitals adopt fall-detection watches. Cross-border e-commerce and multinational OEM assembly lines stitch regions into a globally interdependent wearable motion sensors market.

- Bosch Sensortec GmbH

- TDK InvenSense

- STMicroelectronics N.V.

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Panasonic Industry Co., Ltd.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Samsung Electronics Co. Ltd.

- Robert Bosch GmbH (Sensors)

- TE Connectivity

- Qualcomm Technologies Inc.

- Sensirion AG

- Xsens (Movella)

- Valencell Inc.

- OMRON Corporation

- Garmin Ltd.

- Polar Electro Oy

- Fitbit LLC (Google)

- Apple Inc.

- Oura Health Oy

- Xiaomi Corporation

- Goertek Inc.

- Huami (Zepp Health)

- Withings SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-enabled Sensor Fusion Driving Medical-Grade Wearables

- 4.2.2 Sub-milliwatt MEMS for Eldercare in Japan and Korea

- 4.2.3 U.S. RPM Reimbursement Boost

- 4.2.4 EU Digital Product Passport-Linked Usage Analytics

- 4.2.5 Micro Energy-Harvesting Modules in China

- 4.2.6 NATO Soldier Modernisation Demand

- 4.3 Market Restraints

- 4.3.1 Algorithmic Limits on Tremor Differentiation

- 4.3.2 MEMS Foundry Capacity Crunch

- 4.3.3 Data-Sovereignty Compliance Costs

- 4.3.4 Smart-Textile Interconnect Failures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Accelerometers

- 5.1.2 Gyroscopes

- 5.1.3 Magnetometers

- 5.1.4 Inertial Measurement Units (IMUs)

- 5.1.5 MEMS Combo Sensors

- 5.1.6 Pressure Sensors

- 5.2 By Application

- 5.2.1 Fitness Bands

- 5.2.2 Activity Monitors

- 5.2.3 Smart Clothing

- 5.2.4 AR/VR Headsets

- 5.2.5 Smart Rings and Jewelry

- 5.2.6 Ear-wear and Hearing Aids

- 5.3 By End-user Industry

- 5.3.1 Healthcare and Medical Devices

- 5.3.2 Consumer Electronics and Lifestyle

- 5.3.3 Industrial and Enterprise Safety

- 5.3.4 Military and Defense

- 5.3.5 Government and Public Utilities

- 5.4 By Power Consumption

- 5.4.1 Ultra-Low Power (Less than1mW)

- 5.4.2 Low Power (1-10mW)

- 5.4.3 Standard Power (10-50mW)

- 5.4.4 High Power (Greater than 50mW)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Bosch Sensortec GmbH

- 6.4.2 TDK InvenSense

- 6.4.3 STMicroelectronics N.V.

- 6.4.4 Analog Devices, Inc.

- 6.4.5 Texas Instruments Incorporated

- 6.4.6 Panasonic Industry Co., Ltd.

- 6.4.7 Infineon Technologies AG

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 Samsung Electronics Co. Ltd.

- 6.4.10 Robert Bosch GmbH (Sensors)

- 6.4.11 TE Connectivity

- 6.4.12 Qualcomm Technologies Inc.

- 6.4.13 Sensirion AG

- 6.4.14 Xsens (Movella)

- 6.4.15 Valencell Inc.

- 6.4.16 OMRON Corporation

- 6.4.17 Garmin Ltd.

- 6.4.18 Polar Electro Oy

- 6.4.19 Fitbit LLC (Google)

- 6.4.20 Apple Inc.

- 6.4.21 Oura Health Oy

- 6.4.22 Xiaomi Corporation

- 6.4.23 Goertek Inc.

- 6.4.24 Huami (Zepp Health)

- 6.4.25 Withings SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment