|

시장보고서

상품코드

1851343

4K 디스플레이 해상도 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)4K Display Resolution - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

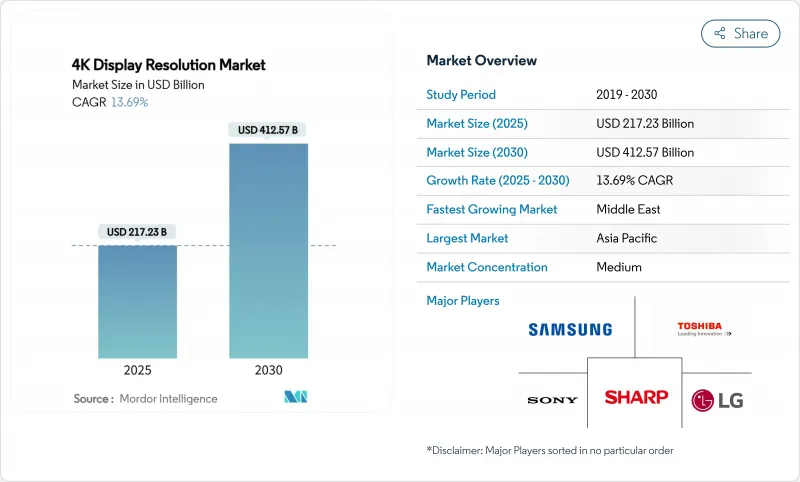

4K 디스플레이 해상도 시장 규모는 2025년에 2,172억 3,000만 달러로 추정되고, 2030년에는 4,125억 7,000만 달러에 이를 것으로 예측되며, CAGR 13.69%로 성장할 전망입니다.

패널 비용의 급격한 저하, 네이티브 4K 스트리밍 컨텐츠의 풍부한 공급, 기업의 이용 사례 확대에 의해 이 기술은 프리미엄의 위치 지정으로부터 대중적인 채용으로 이행하고 있습니다. 아시아태평양의 제조 규모는 평균 판매 가격을 낮게 억제하고 있는 한편, 이 지역의 소비자는 보다 대형의 스크린을 선호하는 경향이 현저합니다. 하이브리드 워크 수요와 몰입형 게임으로 리프레시 사이클이 더욱 엄격해지고, 각 브랜드는 점점 특화된 모델을 출시하게 되었습니다. 동시에 칩셋을 둘러싼 공급망 리스크 및 유럽에서 에너지 효율 규제의 진전으로 벤더는 부품 조달을 다양화하고 저전력 백라이트의 연구개발을 가속화할 필요가 있습니다.

세계의 4K 디스플레이 해상도 시장 동향 및 인사이트

북미에서 OTT 주도의 4K 스트리밍의 급속한 보급

스트리밍 플랫폼은 2024년에 새로운 컨텐츠의 60% 이상을 4K로 제공하여 가정 업그레이드에서 대응 스크린으로의 인수가 강해졌습니다. 최대 46Gbit/s의 데이터 속도를 지원하는 Wi-Fi 7로 대역폭을 확대하면 주류 4K의 보급을 제한했던 이전 병목 현상이 제거됩니다. 일본이 2027년까지 5만 기지국을 목표로 하고 있는 mm파대의 전개는 국경을 넘은 컨텐츠 프로바이더에 이익을 가져오는 용량을 한층 더 늘립니다. 그 결과 TV 및 모니터의 교체 사이클이 급격히 진행되고, 스트리밍 서비스는 HDR 성능과 넓은 색 영역을 중심으로 기능 로드맵을 형성합니다. 패널 발매를 초대작 컨텐츠의 프리미어 상영과 연동시키는 브랜드는 중요한 판매 분기 전에 조기 참가자의 관심을 모으고 있습니다.

중국과 한국에서 패널 보조금 및 생산 능력 확대

정부 우대 조치로 신규 LCD 및 QD-OLED 라인의 자본 비용이 절감되어 BOE Technology, Samsung Display 등의 기업이 공장을 고가동시킬 수 있게 되었습니다. 삼성디스플레이는 QD-OLED 모니터 패널의 출하량을 2025년 50% 증가한 143만 유닛으로 끌어올릴 계획으로 OEM 파트너에게 프리미엄 카탈로그를 쇄신할 여지를 주고 있습니다. 이러한 투자로 인한 스케일 메리트는 50-65인치 메인스트림 스위트 스팟의 경쟁력 있는 가격 설정을 지원하는 한편, 미니 LED 백라이트의 수율 주도에 따른 비용 저하에 의해 중위 모델에서의 채용이 확대됩니다. 보조금에 의한 수량 급증은 이미 세계 공급망에 침투하고 있으며, 강하의 어셈블러 재료비를 낮추고 있습니다.

HDMI 2.1 칩셋 부족 2024-2025년

주요 파운드리의 웨이퍼 출하가 제한되어 있기 때문에, HDMI 2.1 리타이머 IC와 스위치 IC공급이 제한되어 플래그쉽 게이밍 모니터와 하이엔드 TV의 대량 출하가 지연되고 있습니다. 하이맥스 테크놀로지에 따르면, 2024년 매출의 82.9%는 디스플레이 드라이버 IC에 의한 것으로, 좁은 부품 풀에 의존하고 있음이 밝혀졌습니다. 공급업체는 부족한 칩셋을 보다 거친 이자율을 가진 모델로 돌리면서 중간 SKU에 일시적인 품절이 발생했습니다. 또한, MSI의 새로운 QD-OLED 모니터에서 볼 수 있듯이, 품창은 DisplayPort 2.1의 채택을 가속화하고 공급이 정상화된 후에도 장기적인 인터페이스 다양화가 가능함을 보여줍니다.

부문 분석

게이밍 모니터는 2025-2030년 CAGR 예측치가 14.1%로 전망되며, 4K 디스플레이 해상도 시장 내에서 가장 빠른 속도로 추이하고 있습니다. 삼성은 2024년 세계 점유율 21.0%를 유지했으며, OLED 하위 부문에서는 34.6%를 차지하며 QD-OLED 스택의 상승으로 선행자 이익을 확보했습니다. 이 부문은 스포츠 스폰서의 지명도, 빈번한 모델 업데이트, 안정적인 4K/144Hz 게임 플레이를 가능하게 하는 NVIDIA GeForce RTX 4090과 같은 강력한 GPU와의 시너지 효과로 번창하고 있습니다. 모니터 브랜드는 프리미엄 SKU를 차별화하기 위해 더 높은 피크 휘도, 탠덤 OLED 레이어 및 DisplayPort 2.1 입력으로 사양을 향상시킵니다. 엔수지 어스트 레이어는 응답 속도, HDR 콘트라스트 및 색 재현성을 중시하기 때문에 수익성은 메인 스트림 TV보다 높게 유지됩니다.

스마트 TV는 폭넓은 4K 스트리밍 컨텐츠 라이브러리와 BOM 비용 하락에 힘입어 2024년 매출 점유율은 68%로 선두를 유지했습니다. 기업의 비디오월 및 디지털 사이니지 스크린은 하이브리드 워크의 허브로서 광시야각과 고픽셀 밀도가 요구되어 중요성을 늘렸습니다. 의료용 디스플레이는 소니의 LMD-32M1MD와 같은 4K 수술용 모니터가 수술실용 VESA HDR1000 준수를 달성하여 이익률이 높은 틈새 시장을 형성했습니다. 네이티브 4K를 탑재한 스마트폰이나 태블릿은 소비 전력이 모바일의 장점을 상쇄하기 때문에 크리에이터를 위한 용도로 한정되어 있습니다. 전반적으로 보다 풍부한 엔터테인먼트 및 워크플레이스 협업에 대한 소비자의 욕구는 4K 디스플레이 해상도 시장의 다중 부문 기세를 지원합니다.

OLED 패널의 CAGR은 16.7%로 4K 디스플레이 해상도 시장에서 가장 빠르게 확대될 것으로 예측됩니다. 삼성디스플레이가 2025년에 143만장의 QD-OLED 모니터 패널을 출하할 계획은 플래그십 TV 이외의 광범위한 용도를 추진하는 용량 확장을 보여줍니다. 탁월한 콘트라스트, 픽셀 레벨 디밍, 탠덤 OLED 스택의 도입은 이제 게임용 모니터로 확장되어 ASP 프리미엄을 뒷받침하고 있습니다. 2025년 G5 TV는 165Hz의 네이티브 브리 프레쉬와 Micro Lens Array 광학계를 탑재한 LG의 OLED 연구 개발의 지속적인 페이스를 뒷받침하고 있습니다.

2024년 LCD 기술이 71%의 점유율을 유지한 것은 엄청난 수의 금형이 설치되어, 공급망이 성숙하고 미드레인지 세트로 비용 경쟁력이 있기 때문입니다. 미니 LED 백라이트는 로컬 디밍과 고휘도를 추가해 OLED와의 성능 차이를 저비용으로 채웁니다. 소니 HDR1000 표준 수술 모니터는 특수 수직 시장에서 Mini-LED의 영향력을 보여줍니다. Micro-LED는 하이센스의 136인치에서 알 수 있듯이 제조 수율이 향상될 때까지 초대형 형식으로 제한됩니다. 여러 패널 유형이 공존함으로써 확장되는 4K 디스플레이 해상도 시장에서 게임, 사이니지, 헬스케어 등 각 용도가 비용, 휘도, 수명의 최적의 밸런스를 얻을 수 있습니다.

지역 분석

아시아태평양은 2024년 매출의 46%를 차지했으며, 4K 디스플레이 해상도 시장에서 가장 규모가 큰 지역으로 자리매김했습니다. 중국의 보조금이 신속한 생산 능력 증강을 가능하게 하고, 한국의 OLED 리더십이 이익률이 높은 패널을 세계에 공급했습니다. 일본은 2027년까지 5만기의 mm파 기지국을 설치하겠다는 목표를 내걸어 4K 스트리밍의 보급을 지원하는 지역의 네트워크 백본을 강화했습니다. 인도와 동남아시아는 ASP의 하락과 재량 소득의 상승이 일치하여 미개척의 대용량을 파고들어 새로운 채용 단계에 들어갔습니다.

중동은 2025-2030년 CAGR 13.6%로 가장 높은 성장이 예측됩니다. GCC 기업은 하이브리드 협업을 강화하기 위해 4K 비디오 월을 도입하여 미세 화소 피치 LED 어셈블리 수요를 밀어 올렸습니다. 소니 중동 및 아프리카는 현저한 매출 증가를 보고하고 2025년 내에 INZONE M9 4K 모니터의 출시를 목표로 하고 있습니다. 온라인 채널은 이미 이 지역의 TV 판매의 20%를 획득했으며, 각 브랜드는 전자상거래 로지스틱스를 미세 조정해야 합니다.

북미의 성숙한 설치 기반은 OTT 컨텐츠의 급속한 보급 및 게임 모니터의 견조한 업그레이드 사이클을 배경으로 계속 성장하고 있습니다. 의료기관은 4K 진단 제품군의 진입을 확대하고 가격 경쟁에 노출되기 어려운 유리한 하위 부문을 확대했습니다. 유럽에서는 기술에 민감한 소비자가 보다 큰 OLED 세트를 채택하는 반면, 에코디자인 기준의 엄격화로 인해 65인치 이상 패널의 컴플라이언스 비용이 상승하여 공급업체는 에너지 효율적인 Mini-LED 설계로 조타를 끊었습니다. 라틴아메리카 및 아프리카는 여전히 신흥 프론티어입니다. 사하라 이남의 아프리카 일부에서는 4K 방송 주파수대가 제한되어 있기 때문에 광대역 보급률의 상승이 장래의 상승을 시사하고 있는 반면, 성장은 억제되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미의 OTT 주도 4K 스트리밍의 급속한 보급

- 중국과 한국의 패널 보조금 및 생산 능력 확대

- 유럽에서의 4K/144Hz 게이밍 모니터의 Esports 수요

- 미국과 일본에서 4K 수술 및 진단용 디스플레이의 채용 상황

- 걸프 협력 회의 국가의 기업 도입을 견인하는 하이브리드 워크 LED 비디오 월

- 미니 LED의 수율이 대만제 50-65인치

- 시장 성장 억제요인

- 2024-2025년 HDMI 2.1 칩셋의 부족

- EU의 에코 디자인 규칙이 65인치 TV의 컴플라이언스 비용 인상 초래

- 사하라 이남의 아프리카에서 한정된 4K 방송 스펙트럼

- 일본과 한국의 프리미엄 8K의 카니발리제이션

- 생태계 분석

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 스마트 TV

- 모니터

- 스마트폰

- 태블릿

- 노트북 PC

- 디지털 사이니지 및 비디오 월

- 프로젝션 스크린

- 헤드 마운트 디스플레이(HMD)

- 의료용 디스플레이

- 기타

- 패널 기술별

- 액정 디스플레이(IPS/VA/TN)

- OLED

- 미니 LED

- 마이크로 LED

- 기타

- 스크린 사이즈별

- 32인치 이하

- 32-49인치

- 50-65인치

- 66-84인치

- 84인치 이상

- 최종 사용자 업계별

- 가전 제품(가정용)

- 게임 및 E 스포츠 회장

- 비즈니스 및 교육

- 소매 및 광고

- 미디어 및 엔터테인먼트 제작

- 헬스케어

- 항공우주 및 방위

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가(덴마크, 스웨덴, 노르웨이, 핀란드)

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향 및 전개

- 시장 점유율 분석

- 기업 프로파일

- Samsung Electronics Co. Ltd

- LG Display Co. Ltd

- BOE Technology Group Co. Ltd

- TCL Technology(CSOT)

- Sony Group Corporation

- Toshiba Corporation

- Panasonic Holdings Corporation

- Sharp Corporation

- Hisense Group

- Koninklijke Philips NV

- Innolux Corporation

- AU Optronics Corp.

- Dell Technologies Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Vizio Inc.

- Skyworth Group Ltd

- Barco NV

- Eizo Corporation

- ViewSonic Corporation

- BenQ Corporation

제7장 시장 기회 및 향후 전망

AJY 25.11.21The 4K display resolution market size is estimated at USD 217.23 billion in 2025 and is forecast to reach USD 412.57 billion by 2030, advancing at a 13.69% CAGR.

Fast-declining panel costs, a richer supply of native 4K streaming content, and expanding corporate use cases are allowing the technology to move from premium positioning into mass adoption. Asia Pacific's manufacturing scale keeps average selling prices low while the region's consumers display a marked preference for larger screens. Hybrid-work demand and immersive gaming are further tightening refresh cycles, encouraging brands to launch increasingly specialized models. At the same time, supply chain risks around chipsets and evolving energy-efficiency rules in Europe urge vendors to diversify component sourcing and accelerate R&D in low-power backlighting.

Global 4K Display Resolution Market Trends and Insights

Rapid OTT-led Uptake of 4K Streaming in North America

Streaming platforms delivered more than 60% of their new content in 4K during 2024, setting a stronger pull for compatible screens in household upgrades. Bandwidth gains from Wi-Fi 7, which supports data rates up to 46 Gbit/s, remove the previous bottlenecks that limited mainstream 4K adoption. Millimeter-wave rollouts, with Japan targeting 50,000 base stations by 2027, add further capacity that benefits cross-border content providers. The result is a steeper replacement cycle for television sets and monitors, with streaming services shaping feature roadmaps around HDR performance and wider color gamuts. Brands that synchronize panel launches with blockbuster content premieres are capturing early-adopter interest ahead of key sales quarters.

Panel Subsidies and Capacity Expansion in China and South Korea

Government incentives trimmed capital costs for new LCD and QD-OLED lines, enabling firms such as BOE Technology and Samsung Display to run plants at high utilization. Samsung Display plans to raise QD-OLED monitor panel shipments by 50% to 1.43 million units in 2025, giving OEM partners more scope to refresh premium catalogs. Economies of scale flowing from these investments support competitive pricing in the 50-65" mainstream sweet spot, while yield-driven cost erosion in Mini-LED backlights widens adoption in mid-tier models. The subsidy-induced volume surge is already filtering through global supply chains, lowering bill-of-materials outlays for downstream assemblers.

HDMI 2.1 Chipset Shortages 2024-25

Constrained wafer starts at leading foundries have a limited supply of HDMI 2.1 retimer and switch ICs, delaying volume shipments of flagship gaming monitors and high-end TVs. Himax Technologies reported that 82.9% of 2024 revenue came from display driver ICs, underscoring dependence on a narrow component pool. Vendors redirected scarce chipsets to models with higher gross margins, creating temporary stockouts in mid-tier SKUs. The scarcity also accelerated DisplayPort 2.1 adoption, as seen in MSI's new QD-OLED monitor, signaling possible long-term interface diversification even after supply normalizes.

Other drivers and restraints analyzed in the detailed report include:

- Esports Demand for 4K/144 Hz Gaming Monitors in Europe

- Adoption of 4K Surgical and Diagnostic Displays in U.S. and Japan

- EU Eco-design Rules Raising Compliance Costs for >65" TVs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gaming monitors accounted for a 14.1% CAGR forecast between 2025 and 2030, the fastest trajectory within the 4K display resolution market. Samsung upheld a 21.0% global share in 2024, while its 34.6% slice of the OLED sub-segment confirmed a first-mover advantage in emerging QD-OLED stacks. The segment thrives on esports sponsorship visibility, frequent model refreshes, and the synergy with powerful GPUs such as NVIDIA GeForce RTX 4090 that unlocked stable 4K/144 Hz gameplay. Monitor brands elevate specifications with higher peak brightness, tandem OLED layers, and DisplayPort 2.1 input to differentiate premium SKUs. Profitability remains thicker than mainstream TVs because enthusiast buyers value response time, HDR contrast, and color coverage.

Smart TVs preserved leadership with a 68% revenue share in 2024, supported by wide 4K streaming content libraries and falling BOM costs. Corporate video walls and digital signage screens gained importance as hybrid-work hubs required wide viewing angles and high pixel density. Medical displays formed a high-margin niche, with 4K surgical monitors like Sony's LMD-32M1MD achieving VESA HDR1000 compliance for operating theaters. Smartphones and tablets with native 4K remain limited to creator-focused uses because energy draw offsets mobile benefits. Overall, consumer appetite for richer entertainment and workplace collaboration sustains multi-segment momentum within the 4K display resolution market.

OLED panels are projected to expand at a 16.7% CAGR, the swiftest run in the 4K display resolution market. Samsung Display's plan to ship 1.43 million QD-OLED monitor panels in 2025 exemplifies the capacity scaling that propels wider use beyond flagship TVs. Superior contrast, pixel-level dimming, and the introduction of tandem OLED stacks now reach gaming monitors, encouraging ASP premiums. LG's 2025 G5 TV, with a 165 Hz native refresh and Micro Lens Array optics, underscores the continued pace of OLED R&D.

LCD technology retained 71% share in 2024 because of vast installed tooling, mature supply chains, and cost competitiveness for mid-range sets. Mini-LED backlighting adds local dimming and higher luminance, bridging performance gaps with OLED at a lower cost. Sony's HDR1000-rated surgical monitor demonstrates Mini-LED influence in specialty verticals. Micro-LED remains confined to ultra-large formats, evidenced by Hisense's 136-inch showpiece, until manufacturing yields improve. The coexistence of multiple panel types ensures that each application - gaming, signage, healthcare - receives an optimal balance of cost, brightness, and longevity within the expanding 4K display resolution market.

The 4K Display Resolution Market Report is Segmented by Product Type (Smart TV, Monitor, Smartphone, Tablet, and More), Panel Technology (LCD, OLED, Mini-LED, and Micro-LED), Screen Size (Sub 32 Inch, 32-49 Inch, 50-65 Inch, 66-84 Inch, and Above 85 Inch), End-User Vertical (Consumer Electronics, Gaming and Esports Venues, Business and Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated 46% of 2024 revenue, cementing its position as the largest territory in the 4K display resolution market. China's subsidies enabled swift capacity ramps, while South Korea's OLED leadership supplied high-margin panels globally. Japan's goal of installing 50,000 millimeter-wave bases by 2027 reinforces the regional network backbone supporting 4K streaming uptake. India and Southeast Asia entered a new adoption phase as falling ASPs aligned with rising discretionary income, unlocking large untapped volumes.

The Middle East is forecast to post the highest CAGR at 13.6% between 2025 and 2030. GCC corporations rolled out 4K video walls to enhance hybrid collaboration, boosting demand for fine-pixel-pitch LED assemblies. Sony Middle East and Africa reported notable sales gains and aims to release the INZONE M9 4K monitor within 2025, reflecting the region's appetite for premium displays. Online channels have already captured 20% of regional TV sales, prompting brands to fine-tune e-commerce logistics.

North America's mature installed base still grew on the back of fast OTT content adoption and a robust gaming monitor upgrade cycle. Healthcare institutions expanded to 4K diagnostic suites, widening a lucrative sub-segment less exposed to price wars. Europe faced a dual narrative: tech-savvy consumers embraced larger OLED sets while stricter Eco-design norms raised compliance costs for panels over 65", nudging suppliers toward energy-efficient Mini-LED designs. Latin America and Africa remained emergent frontiers; limited 4K broadcast spectrum in parts of Sub-Saharan Africa tempered growth, though rising broadband coverage signals future upside.

- Samsung Electronics Co. Ltd

- LG Display Co. Ltd

- BOE Technology Group Co. Ltd

- TCL Technology (CSOT)

- Sony Group Corporation

- Toshiba Corporation

- Panasonic Holdings Corporation

- Sharp Corporation

- Hisense Group

- Koninklijke Philips N.V.

- Innolux Corporation

- AU Optronics Corp.

- Dell Technologies Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Vizio Inc.

- Skyworth Group Ltd

- Barco NV

- Eizo Corporation

- ViewSonic Corporation

- BenQ Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid OTT?led Uptake of 4K Streaming in North America

- 4.2.2 Panel Subsidies and capacity Expansion in China and South Korea

- 4.2.3 Esports Demand for 4K/144 Hz Gaming Monitors in Europe

- 4.2.4 Adoption of 4K Surgical and Diagnostic Displays in United States and Japan

- 4.2.5 Hybrid-Work LED Videowalls Driving Gulf Cooperation Council Countries Corporate Installations

- 4.2.6 Mini-LED Yield-Driven Price Erosion in Taiwan-made 50-65? Panels

- 4.3 Market Restraints

- 4.3.1 HDMI 2.1 Chipset Shortages 2024-25

- 4.3.2 EU Ecodesign Rules Raising Compliance Costs for Above 65? TVs

- 4.3.3 Limited 4K Broadcast Spectrum in Sub-Saharan Africa

- 4.3.4 Premium 8K Cannibalisation in Japan and South Korea

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Smart TV

- 5.1.2 Monitor

- 5.1.3 Smartphone

- 5.1.4 Tablet

- 5.1.5 Laptop

- 5.1.6 Digital Signage/Videowall

- 5.1.7 Projection Screen

- 5.1.8 Head-Mounted Display (HMD)

- 5.1.9 Medical Display

- 5.1.10 Others

- 5.2 By Panel Technology

- 5.2.1 LCD (IPS/VA/TN)

- 5.2.2 OLED

- 5.2.3 Mini-LED

- 5.2.4 Micro-LED

- 5.2.5 Others

- 5.3 By Screen Size

- 5.3.1 Below 32 inch

- 5.3.2 32-49 inch

- 5.3.3 50-65 inch

- 5.3.4 66-84 inch

- 5.3.5 Above 84 inch

- 5.4 By End-user Vertical

- 5.4.1 Consumer Electronics (Household)

- 5.4.2 Gaming and Esports Venues

- 5.4.3 Business and Education

- 5.4.4 Retail and Advertisement

- 5.4.5 Media and Entertainment Production

- 5.4.6 Healthcare

- 5.4.7 Aerospace and Defence

- 5.4.8 Others

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Gulf Cooperation Council Countries

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co. Ltd

- 6.4.2 LG Display Co. Ltd

- 6.4.3 BOE Technology Group Co. Ltd

- 6.4.4 TCL Technology (CSOT)

- 6.4.5 Sony Group Corporation

- 6.4.6 Toshiba Corporation

- 6.4.7 Panasonic Holdings Corporation

- 6.4.8 Sharp Corporation

- 6.4.9 Hisense Group

- 6.4.10 Koninklijke Philips N.V.

- 6.4.11 Innolux Corporation

- 6.4.12 AU Optronics Corp.

- 6.4.13 Dell Technologies Inc.

- 6.4.14 ASUSTeK Computer Inc.

- 6.4.15 Acer Inc.

- 6.4.16 Vizio Inc.

- 6.4.17 Skyworth Group Ltd

- 6.4.18 Barco NV

- 6.4.19 Eizo Corporation

- 6.4.20 ViewSonic Corporation

- 6.4.21 BenQ Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment