|

시장보고서

상품코드

1851348

IoT 테스트 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)IoT Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

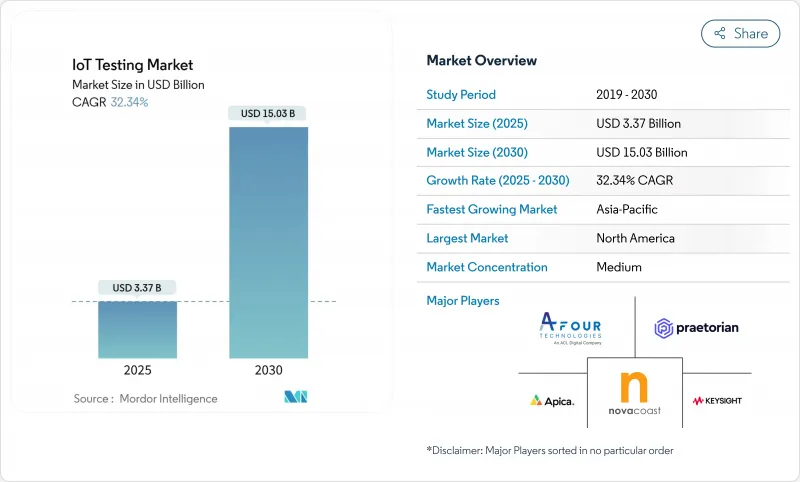

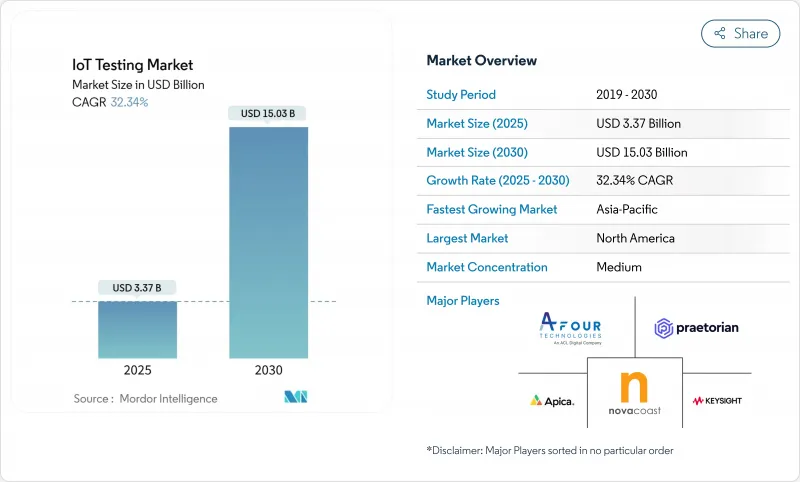

세계의 IoT 테스트 시장 규모는 2025년 33억 7,000만 달러로 추정되며, 예측 기간(2025-2030년) 중 CAGR은 32.34%로 확대되어, 2030년에는 150억 3,000만 달러에 달할 것으로 예측됩니다.

이러한 급속한 확대는 디지털 변혁 목표 증가, 사이버 보안의 의무화 강화, 산업계 및 소비자 환경에 침투하는 커넥티드 엔드포인트의 증대 등을 반영하고 있습니다. 기업은 단일 장치 고장이 생산 라인을 중단하고 안전 사고를 일으키고 수백만에 이르는 규제 처벌을 초래할 수 있으므로 반응형에서 예측형 검증 모델로 전환하고 있습니다. 5G 및 엣지 컴퓨팅에서 얻은 낮은 대기 시간 요구 사항은 미션 크리티컬 워크로드에서 밀리초 수준의 성능 변화를 포착할 수 있는 테스트 베드에 대한 수요를 강화하고 있습니다. 동시에 디지털 트윈 환경은 개발자가 실제 환경에 대한 추적성을 유지하면서 장치의 전체 라이프사이클을 소프트웨어로 모델링할 수 있게 함으로써 하드웨어 비용을 절감합니다.

세계 IoT 테스트 시장 동향과 통찰

연결된 IoT 엔드포인트의 폭발적 증가

중국에서는 2024년 8월까지 활성 IoT 단말기가 25억 7,000만대에 달하는 것으로 보고되고 있으며, 지수함수적으로 대규모 테스트 매트릭스를 추진하는 스케일 시프트가 부각되고 있습니다. 하나의 스마트 공장에 Zigbee 센서, LoRaWAN 게이트웨이, 5G RedCap 로봇이 혼재할 수 있으며, 검증 팀은 모든 프로토콜의 순열에서 원활한 상호 운용성을 보장해야 합니다. Hyundai와 Samsung은 이미 10ms 이하의 대기 시간 검증을 요구하는 사설 5G RedCap 생산 라인을 이미 입증했습니다. 세대가 혼재하는 플릿이 증가함에 따라, 새로운 디바이스의 SKU가 늘어날 때마다 인증되어야 하는 조합이 늘어나고, 기업은 커버리지를 희생하지 않고 확장할 수 있는 통합 테스트 자동화 프레임워크에 대한 투자를 강요하게 됩니다. 따라서 IoT 테스트 시장은 기존 4G 모듈과 향후 5G 엔드포인트를 하나의 구성 가능한 환경에서 지원해야 합니다.

향상되는 보안 및 개인 정보 보호 규정

2025년 8월부터 유럽 연합의 무선 장비 지침은 인터넷에 연결된 모든 제품에 대해 판매 전에 사이버 보안 적합성 시험을 통과해야 합니다. 일관된 EN 18031 시리즈는 네트워크 보호, 데이터 프라이버시 및 사기 방지 테스트 케이스를 규정하고 있으며, 컴플라이언스 작업 부하는 기능 점검 영역을 훨씬 넘어 확장되었습니다. 걸프 지역에서는 사우디아라비아와 아랍에미리트(UAE)에서 생체 인증 SIM 등록이 의무화되어 연결성 테스트 프로토콜이 재구성되고 있습니다. 사내에 보안 전문가를 배치할 수 없는 기업은 검증을 아웃소싱하는 경향이 강해지고 있으며, IoT 테스트 시장 내에서 관리 서비스 공급자에 대한 수요가 증가하고 있습니다.

장치/프로토콜 복잡화

현대 배포에는 Wi-Fi 6E 센서, Bluetooth 5.4 비콘, LoRaWAN 미터, NB-IoT 트래커, 5G RedCap 모뎀 등이 혼합되어 있으며, 각각 다른 도구가 필요합니다. 차량 탑재 반도체는 2030년까지 1대당 1,200달러에 달할 것으로 예측되며, 제어 유닛과 텔레매틱스 게이트웨이의 검증 포인트는 두 배가 됩니다. 모든 새로운 프로토콜은 기존 매트릭스에 쌓여 테스트 사이클을 길게 하고 자원에 제약이 있는 실험실에 과제를 던집니다. 자동화, 가상화 및 AI를 통한 우선순위화가 사이클 시간을 단축하지 않는 한, 이러한 복잡성은 IoT 테스트 시장의 소비를 감속시킬 수 있습니다.

부문 분석

전문 서비스는 2024년 매출의 61%를 차지했으며 기업이 다방면 프로토콜, 보안 및 규정 준수 요구를 충족하기 위해 외부 전문가를 활용했습니다. 전문 서비스의 강점은 5G, RedCap, EU 사이버 적합성 테스트에 익숙한 깊은 벤치에 있습니다. 그러나 매니지드 서비스는 제조업체와 플릿 운영자가 24시간 365일 실험실 용량을 보장하는 구독 계약을 선호하기 때문에 연간 18.7%의 상승을 예측합니다. HCL Technologies의 24년 매출은 133억 달러로 매니지드 테스트 포트폴리오가 호조를 보이고 있습니다. 이 전환은 전체 IoT 테스트 시장의 전달 모델을 재정의하여 완전히 아웃소싱된 검증 센터에 대한 수요를 확대하고 있습니다.

매니지드 서비스의 IoT 테스트 시장 규모는 2025년 13억 1,000만 달러에서 2030년 60억 5,000만 달러로 급증할 것으로 예측됩니다. 세계 시스템 통합사업자는 원격으로 액세스할 수 있는 장치 팜에 투자하고 있습니다.

기능 검증은 프로젝트가 여전히 연결성과 데이터 흐름 검사로 시작되어 2024년에도 최대 27.3%의 판매를 유지합니다. 그럼에도 불구하고 보안 테스트는 2030년까지 22.5%의 연평균 복합 성장률(CAGR)로 추이할 전망입니다. IoT 테스트 시장은 침입 시뮬레이션, 펌웨어 무결성 스캔, EN 18031 및 미국 FDA 시판 전 신청에 따라 암호화 채널 평가를 수행해야 합니다. Applus는 ETSI 303 645 인증 수요에 신속하게 대응하기 위해 2024년에 새로운 유럽 사이버 랩을 개설했습니다.

보안 서비스만으로도 2030년까지 31% 시장 점유율을 획득할 수 있습니다. 이와 병행하여 성능 스트레스와 네트워크 핸드오버 테스트는 5G의 URLLC 시나리오에 필수적이며, 급성장하지는 않지만, 그 관련성은 유지되고 있습니다.

IoT 테스트 시장 보고서는 서비스 유형(전문 및 관리), 테스트 유형(기능 테스트, 성능 테스트, 네트워크 테스트, 호환성 테스트, 보안 테스트, 사용성 테스트), 용도(스마트 빌딩 및 홈 오토메이션, 모세 혈관 네트워크 관리 등), 최종 사용자 산업(소매, 제조, 건강 관리, 에너지 및 유틸리티, IT 및 텔레콤), 지역으로 구분됩니다.

지역 분석

북미는 설계에서 생산까지 테스트를 통합하는 DevOps 파이프라인을 기업이 채용했기 때문에 2024년 매출이 38.6%로 촤고 부문이 되었습니다. San Antonio의 SmartSA 이니셔티브는 모든 가로등 센서가 현장 전개 전에 상호 운용성과 보안 게이트를 클리어해야 하는 지자체 등급 파일럿을 입증합니다. IoT 테스트 시장은 확립된 인증 생태계와 자금력 있는 항공우주, 자동차, 산업 자동화 고객으로부터 이익을 얻고 있습니다.

아시아태평양의 CAGR은 최고 속도로 15.8%가 될 것으로 예측됩니다. 중국의 Xiong'an 10Gbps 백본과 베이징의 차량 로드 클라우드 파일럿이 대규모 컴포맨스 실험실에 대한 수요를 높이고 있습니다. 일본의 Society 5.0과 한국의 1억 100만 달러의 국가 스마트 시티 펀드는 지역별 통신 및 프라이버시 규정에 따라 프로파일링되어야 하는 수천 개의 디바이스를 추가하고 있습니다. 아시아태평양의 IoT 테스트 시장 규모는 현지 공급업체가 클라우드 네이티브 자동화를 통합함으로써 2030년까지 50억 달러를 초과할 수 있습니다.

유럽은 규칙 우선 자세에 힘입어 견조한 성장을 유지하고 있습니다. 무선 장비 지침(Radio Equipment Directive)의 사이버 보안 조항에서는 CE 마킹 전에 타사 실험실에서 침입 테스트를 실시해야 합니다. 2023년에는 스마트 미터의 보급률이 전력으로 60%, 가스로 45%에 도달하여 유틸리티 공급업체의 지속적인 검증 작업이 촉진됩니다. 북유럽의 통신 사업자는 5G IoT 실험실의 공동 개설을 진행하고 있으며, Telenor의 칼스크로나 시설은 세계의 디바이스 제조업체에게 스웨덴의 네트워크에 대한 플러그 앤 플레이 액세스를 제공합니다. 이러한 프레임워크를 통해 유럽의 IoT 테스트 시장은 컴플라이언스 중심에서 탄력적입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 연결된 IoT 엔드포인트의 폭발적 증가

- 높아지는 보안과 프라이버시 규제

- DevOps와 지속적인 테스트 파이프라인으로의 이동

- 5G 및 엣지 컴퓨팅에 의한 저지연의 이용 사례

- 디지털 트윈 베이스의 '버추얼 검사' 채용

- 에너지 효율이 높은 기기에 대한 지속가능성 의무화

- 시장 성장 억제요인

- 기기 및 프로토콜의 복잡화

- 세계 상호 운용성 표준의 부족

- 멀티 액세스 엣지 테스트 베드의 부족

- 크로스 보더 검사를 지연시키는 데이터 주권규칙

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- 검사 유형의 개요

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- COVID-19의 평가와 팬데믹 후의 영향

제5장 시장 규모와 성장 예측

- 서비스 유형별

- 전문

- 매니지드

- 검사 유형별

- 기능 시험

- 성능 시험

- 네트워크 테스트

- 호환성 시험

- 보안시험

- 사용성 테스트

- 용도별

- 스마트 빌딩 및 홈 오토메이션

- 모세 혈관 네트워크 관리

- 스마트 유틸리티(에너지 및 물)

- 자동차 텔레매틱스와 커넥티드 비클

- 스마트 매뉴팩처링 및 산업용 IoT(IIoT)

- 최종 사용자 업계별

- 소매

- 제조업

- 헬스케어

- 에너지 및 유틸리티

- IT 및 통신

- 정부 및 스마트시티

- 운송 및 물류

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- Strategic Initiatives and Funding

- 시장 점유율 분석

- 기업 프로파일

- IBM

- Keysight Technologies

- HCL Technologies

- Cognizant

- Capgemini

- Infosys

- Tata Consultancy Services

- Accenture

- Wipro

- Qualitest Group

- Spirent Communications

- AFour(ACL Digital)

- Apica Systems

- Praetorian Security

- Novacoast

- Trustwave(Singtel)

- Happiest Minds

- Vector Informatik

- Eurofins Digital Testing

- SmartBear

- VIAVI Solutions

제7장 시장 기회와 장래의 전망

JHS 25.11.13The IoT Testing Market size is estimated at USD 3.37 billion in 2025, and is expected to reach USD 15.03 billion by 2030, at a CAGR of 32.34% during the forecast period (2025-2030).

This rapid expansion mirrors rising digital-transformation targets, stricter cybersecurity mandates, and the swelling universe of connected endpoints that now permeate industrial and consumer settings. Enterprises are migrating from reactive to predictive validation models because a single device failure can stall production lines, trigger safety incidents, and invite regulatory penalties running into millions. Low-latency requirements born of 5G and edge computing are intensifying demand for testbeds that can capture millisecond-level performance variations in mission-critical workloads. At the same time, digital-twin environments are cutting hardware costs by letting developers model full device lifecycles in software while maintaining traceability to real-world conditions.

Global IoT Testing Market Trends and Insights

Explosion in Connected IoT Endpoints

China reported 2.57 billion active IoT terminals by August 2024, underscoring the scale shift that now drives exponentially larger test matrices. A single smart factory can blend Zigbee sensors, LoRaWAN gateways, and 5G RedCap robots, forcing validation teams to assure seamless interoperability across every protocol permutation. Hyundai and Samsung have already proven private 5G RedCap production lines that demand sub-10 millisecond latency verification. As mixed-generation fleets proliferate, each new device SKU multiplies the combinations that must be certified, compelling enterprises to invest in unified test-automation frameworks able to scale without sacrificing coverage. The IoT testing market must therefore support legacy 4G modules and future 5G endpoints in one configurable environment.

Escalating Security and Privacy Regulations

From August 2025, the European Union's Radio Equipment Directive obliges every internet-connected product to pass cybersecurity conformance testing before sale. The harmonized EN 18031 series now prescribes network protection, data privacy, and fraud-prevention test cases, expanding compliance workloads well beyond functional checks. In the Gulf region, mandatory biometric SIM registration in Saudi Arabia and the UAE is reshaping connectivity-test protocols. Enterprises unable to field in-house security expertise are increasingly outsourcing validation, steering demand toward managed-service providers inside the IoT testing market.

Rising Device/Protocol Complexity

Contemporary deployments mix Wi-Fi 6E sensors, Bluetooth 5.4 beacons, LoRaWAN meters, NB-IoT trackers, and 5G RedCap modems, each demanding distinct tooling. Automotive semiconductor content is projected to hit USD 1,200 per car by 2030, doubling validation points across control units and telematics gateways. Every new protocol stacks onto the existing matrix, lengthening test cycles and challenging resource-constrained labs. Unless automation, virtualization, and AI-enabled prioritization shrink cycle times, this complexity could slow spend within the IoT testing market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward DevOps and Continuous Testing Pipelines

- 5G/Edge-Computing Driven Low-Latency Use-Cases

- Lack of Global Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Professional services dominated 2024 revenue with a 61% stake as enterprises leaned on external specialists for multifaceted protocol, security, and compliance needs. Their strength stems from deep benches versed in 5G, RedCap and EU cyber-conformance testing. Managed services, however, are forecast to rise 18.7% annually because manufacturers and fleet operators prefer subscription contracts that guarantee 24/7 lab capacity. HCL Technologies reported USD 13.3 billion FY24 revenue, attributing strong growth to its managed testing portfolios. This transition is redefining delivery models across the IoT testing market and widening demand for fully outsourced validation centers.

The IoT testing market size for managed services is projected to jump from USD 1.31 billion in 2025 to USD 6.05 billion by 2030, mirroring the steep complexity curve that favors dedicated external labs. Global system integrators are investing in remote-accessible device farms so clients can queue tests around the clock without shipping hardware.

Functional validation retained the largest 27.3% revenue slice in 2024 because projects still begin with connectivity and data-flow checks. Nevertheless, security testing is expected to post a 22.5% CAGR through 2030. The IoT testing market must now execute penetration simulations, firmware-integrity scans, and encrypted-channel evaluations aligned with EN 18031 and US FDA pre-market submissions. Applus+ opened a new European cyber-lab in 2024 to fast-track ETSI 303 645 certification demand.

Security services alone could capture 31% IoT testing market share by 2030 as regulatory fines push device makers to bake validation into every build. In parallel, performance-stress and network-handover tests stay critical for 5G URLLC scenarios, keeping them relevant, though not as fast-growing.

The IoT Testing Market Report is Segmented by Service Type (Professional and Managed), Testing Type (Functional Testing, Performance Testing, Network Testing, Compatibility Testing, Security Testing, and Usability Testing), Application (Smart Building and Home Automation, Capillary Networks Management, and More) End-User Industry (Retail, Manufacturing, Healthcare, Energy and Utilities, IT and Telecom, and More), and Geography.

Geography Analysis

North America led with 38.6% revenue in 2024 as enterprises adopted DevOps pipelines that embed testing from design through production. San Antonio's SmartSA initiative demonstrates municipal-grade pilots where every lamp-post sensor must clear interoperability and security gates before field deployment. The IoT testing market benefits from established certification ecosystems and well-funded aerospace, automotive, and industrial-automation clients.

Asia Pacific is predicted to post the fastest 15.8% CAGR. China's Xiong'an 10 Gbps backbone and Beijing's vehicle-road-cloud pilots elevate demand for massive-scale conformance labs. Japan's Society 5.0 and South Korea's USD 101 million national smart-city fund are adding thousands of devices that must be profiled under region-specific telecom and privacy rules. The IoT testing market size in Asia Pacific could cross USD 5 billion by 2030 as local vendors integrate cloud-native automation.

Europe maintains solid growth anchored in its rule-first posture. Radio Equipment Directive cybersecurity clauses require third-party labs to run penetration tests before CE marking. Smart-meter rollouts hit 60% for electricity and 45% for gas in 2023, driving sustained validation work for utility suppliers. Nordic telcos are opening shared 5G IoT labs, exemplified by Telenor's Karlskrona facility that grants global device makers plug-and-play access to Swedish networks. These frameworks ensure the IoT testing market in Europe remains compliance-centric and resilient.

- IBM

- Keysight Technologies

- HCL Technologies

- Cognizant

- Capgemini

- Infosys

- Tata Consultancy Services

- Accenture

- Wipro

- Qualitest Group

- Spirent Communications

- AFour (ACL Digital)

- Apica Systems

- Praetorian Security

- Novacoast

- Trustwave (Singtel)

- Happiest Minds

- Vector Informatik

- Eurofins Digital Testing

- SmartBear

- VIAVI Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion in connected IoT endpoints

- 4.2.2 Escalating security and privacy regulations

- 4.2.3 Shift toward DevOps and continuous testing pipelines

- 4.2.4 5G/edge-computing driven low-latency use-cases

- 4.2.5 Digital-twin-based "virtual testing" adoption

- 4.2.6 Sustainability mandates for energy-efficient devices

- 4.3 Market Restraints

- 4.3.1 Rising device/protocol complexity

- 4.3.2 Lack of global interoperability standards

- 4.3.3 Scarcity of multi-access edge test beds

- 4.3.4 Data-sovereignty rules slowing cross-border testing

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Testing Types Overview

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Assessment of COVID-19 and Post-Pandemic Impacts

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Professional

- 5.1.2 Managed

- 5.2 By Testing Type

- 5.2.1 Functional Testing

- 5.2.2 Performance Testing

- 5.2.3 Network Testing

- 5.2.4 Compatibility Testing

- 5.2.5 Security Testing

- 5.2.6 Usability Testing

- 5.3 By Application

- 5.3.1 Smart Building and Home Automation

- 5.3.2 Capillary Networks Management

- 5.3.3 Smart Utilities (Energy / Water)

- 5.3.4 Vehicle Telematics and Connected Vehicles

- 5.3.5 Smart Manufacturing / Industrial IoT (IIoT)

- 5.4 By End-user Industry

- 5.4.1 Retail

- 5.4.2 Manufacturing

- 5.4.3 Healthcare

- 5.4.4 Energy and Utilities

- 5.4.5 IT and Telecom

- 5.4.6 Government and Smart Cities

- 5.4.7 Transportation and Logistics

- 5.4.8 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Initiatives and Funding

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM

- 6.4.2 Keysight Technologies

- 6.4.3 HCL Technologies

- 6.4.4 Cognizant

- 6.4.5 Capgemini

- 6.4.6 Infosys

- 6.4.7 Tata Consultancy Services

- 6.4.8 Accenture

- 6.4.9 Wipro

- 6.4.10 Qualitest Group

- 6.4.11 Spirent Communications

- 6.4.12 AFour (ACL Digital)

- 6.4.13 Apica Systems

- 6.4.14 Praetorian Security

- 6.4.15 Novacoast

- 6.4.16 Trustwave (Singtel)

- 6.4.17 Happiest Minds

- 6.4.18 Vector Informatik

- 6.4.19 Eurofins Digital Testing

- 6.4.20 SmartBear

- 6.4.21 VIAVI Solutions

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment