|

시장보고서

상품코드

1851383

중국의 퍼스널케어 포장 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)China Personal Care Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

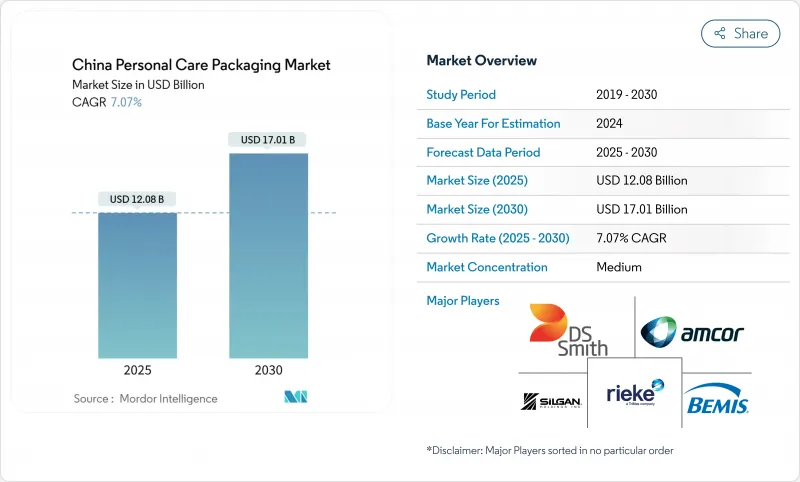

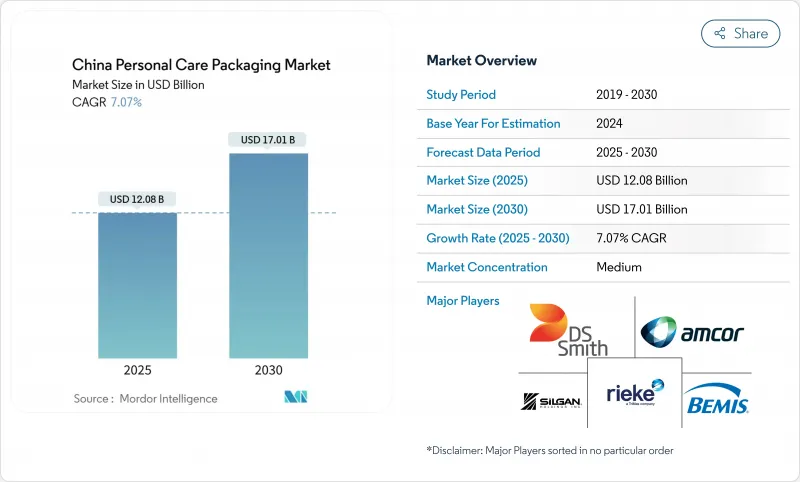

중국의 퍼스널케어 포장 시장은 2025년에 120억 8,000만 달러로 추정되고, 2030년에는 170억 1,000만 달러로 확대될 것으로 예측됩니다.

이 궤적은 과잉 포장을 억제하는 규제 조치, 소셜 커머스 채널로 미용 쇼핑의 급속한 전환, 탄소 중립 사업에 대한 브랜드 헌신에 의해 추진되고 있습니다. 지속가능한 소재 혁신, 전자상거래 대응 구조 설계, 프리미엄층 제품 출시는 밸류체인 전반에 걸쳐 경쟁력 있는 포지셔닝을 재정의하기 위해 집계되고 있습니다. 브랜드는 개발 사이클을 단축하기 위해 AI 지원 프로토타이핑에 투자하고, 패키징 컨버터는 전국 최종 마일 배송을 위해 경량화 및 내구성 요구의 균형을 맞추고 있습니다. GB 23350-2021 표준의 강화된 시행, 중국의 국가 탄소 거래 체계의 전개, 실시간 소셜 미디어 피드백 루프는 중국의 퍼스널케어 포장 시장의 재료 선택과 설계 매개변수를 계속 형성할 것으로 보입니다.

중국의 퍼스널케어 포장 시장 동향 및 인사이트

미용 및 퍼스널케어의 전자상거래 붐

소셜 커머스의 폭발적인 성장으로 브랜드는 사진이 잘 나오는 개봉의 순간을 연출하면서 광범위한 풀필먼트를 견딜 수 있는 팩의 설계를 강요하고 있습니다. Douyin의 미용 GMV는 2021년에서 2023년 사이에 두 배 이상으로 증가했으며, 플랫폼의 알고리즘 동향은 컨버터에게 거의 즉각적인 패키징 개요로 바뀌었습니다. 브랜드는 현재 내충격성, 치수 중량, 카메라에 비치는 미관을 똑같이 평가하게 되어 있습니다. 해안 지역 외에 풀필먼트 센터가 급증함에 따라 플렉서블 파우치 및 경량 골판지는 쿠션성과 운송의 절약이라는 특성으로부터 지지를 모아 중국의 퍼스널케어 포장 시장의 기세를 강화하고 있습니다.

레필 대응 소매업태의 상승

프리미엄 뷰티 메종의 서큘러리티 목표는 리필 포드, 풍부한 향 주머니, 매장 내 벌크 디스펜서의 평가판을 가속화했습니다. 시세이도는 2025년까지 100% 지속 가능한 패키징을 목표로 리필 옵션을 영웅 SKU로 확대하여 현지 ODM에 플러그인 카트리지용 사출 성형 라인의 재정비를 촉구하고 있습니다. 상하이 쇼핑몰에서의 초기 테스트 운영은 리필 스테이션이 POS에 인접한 경우 소비자가 재사용 가능한 코어를 수용하고, 반복 구매의 밀착성을 높이며, 머티리얼 실적를 줄이는 것으로 나타났습니다.

불안정한 수지 및 알루미늄 가격

원유 가격 변동과 지정학적 불확실성으로 인한 원료 변동은 컨버터 마진을 압박하고 있습니다. Wankai와 같은 PET 칩 제조업체는 2024년 후반에 가동률을 76%로 낮추고 공급을 단축하고, 컨버터에게 다월 계약에 의한 헤지나 HDPE나 PP 블렌드로의 다양화를 촉구하고 있습니다. 급여의 흡수를 걱정하는 소규모 기업이 인수 대상이 되어 중국의 퍼스널케어 포장 시장 내 점진적인 통합에 박차를 가할 수 있습니다.

부문 분석

2024년 중국의 퍼스널케어 포장 시장 점유율은 비용 효율성과 공정 민첩성으로 인해 플라스틱이 58.47%를 차지했습니다. 그러나 GB23350-2021의 인터스페이스 비율 캡으로 각 브랜드는 두께를 줄이고, 2차 팩용 판지 슬리브를 모색하고 있습니다. 종이 및 판지의 CAGR은 8.23%로, 소비자가 섬유 기반의 팩을 환경 보호와 동일시하고 있는 것에 뒷받침되어 두드러진 성장 엔진으로서 자리매김하고 있습니다. 유리는 무게가 고급감을 나타내는 프레스티지 스킨 케어로 수량이 안정되어 있는 반면, 금속 에어로졸은 무한히 재활용 가능한 이야기와 일치하기 때문에 프리미엄 탈취제로 지지를 모으고 있습니다. 불안정한 수지 가격은 중국의 퍼스널케어 포장 시장 전반에서 혼합 기재 전략의 경우를 더욱 증폭시키고 있습니다.

바이오계 폴리머의 안정적인 파이프라인이 나타나지만, 많은 블렌드는 산업적 퇴비화 조건을 필요로 하며, 그 조건은 여전히 희귀합니다. 결과적으로 생산자는 장벽 성능을 손상시키지 않고 재활용 가능한 임계 값을 충족하는 단일 소재 PP 튜브 및 PCR 리치 PET 병에 투자합니다. 국유 은행의 그린 파이낸스는 재활용 원료를 다룰 수 있는 라인의 개조에 걸리는 자본 비용을 낮추고, 머티리얼의 결정을 지속가능성 스코어 카드와 투입 비용 헤지 모두와 긴밀하게 링크시킬 것으로 기대됩니다.

플라스틱 병 및 단지는 2024년 매출의 41.63%를 차지했으며, 정착된 블로우 성형 자산과 소비자의 친숙함에 뒷받침됩니다. 그러나 플렉서블 플라스틱 파우치는 브랜드 경량화가 택배 요금 인하로 이어지기 때문에 CAGR 8.07%로 성장을 지속하고 있습니다. 인플루언서의 동영상에 클로즈업 되는 편평한 전면을 보이면서, 복수 노드에 대한 배송 루트에도 견딜 수 있도록, 개봉 방지 지퍼와 마치 첨부 베이스가 표준 장비되게 되었습니다. 튜브와 스틱은 남성 그루밍 붐과 함께 점차 인기를 끌고 리필 카트리지는 최고급 스킨 케어 풋 프린트를 줄일 수 있습니다. 펌프, 드로퍼 및 액추에이터는 금속 스프링 부품의 비용 압력에 직면하지만, 중국의 퍼스널케어 포장 시장에서 투여 정확도를 강조하는 프리미엄화의 이점을 누리고 있습니다.

골판지 쉬퍼는 일반 크래프트 큐브에서 소셜 미디어 스토리텔링을 위한 공동 브랜드인 프린트 온 디맨드 캔버스로 진화하고 있습니다. 그러나 중금속 함량을 제한하는 GB 43352-2023의 익스프레스팩 규정을 준수해야 하며, 컨버터를 수성 잉크나 전분 접착제로 향하게 하고 있습니다. 에어로졸 캔과 특수 유리는 수량에서 틈새 시장이지만 평균 판매 가격이 높은 향수 및 스파 등급 치료로 인해 금액에서 과잉 지수가 되었습니다.

중국의 퍼스널케어 포장 시장은 소재 유형별(플라스틱, 유리, 금속, 종이 및 판지, 바이오베이스 및 퇴비화 가능 플라스틱), 포장 유형별(플라스틱 병 및 단지, 튜브 및 스틱, 펌프, 스프레이 및 스포이드, 기타), 제품 유형별(스킨케어, 헤어케어, 오랄케어, 기타), 지속가능성 속성별(재활용 가능, 소비자 재생이용(PCR) 컨텐츠 후 생분해성 등)로 구분됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 미용 및 퍼스널케어의 전자상거래 붐

- 레필 대응 소매업태의 대두

- 스킨케어 및 화장품 SKU의 프리미엄화

- 저층도시에서 남성의 그루밍 붐 향상

- AI를 활용한 설계 및 래피드 프로토타이핑

- 과잉 포장 컴플라이언스의 의무화(GB 23350-2021)

- 시장 성장 억제요인

- 불안정한 수지 가격 및 알루미늄 가격

- 다층 라미네이트의 재활용 능력 병목

- 플라스틱에 대한 탄소원 단위 할당의 엄격화

- 2차 포장에서의 위조 위험

- 중요한 규제 프레임워크의 평가

- 밸류체인 분석

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 주요 이해관계자의 영향 평가

- 주요 이용 사례 및 사례 연구

- 시장의 거시경제 요인에 미치는 영향

- 투자 분석

제5장 시장 세분화

- 재료 유형별

- 플라스틱

- 유리

- 금속

- 종이 및 판지

- 바이오 베이스 및 컴포스트 가능 플라스틱

- 패키징 유형별

- 페트병 및 병

- 튜브 및 스틱

- 펌프, 스프레이, 스포이드

- 에어로졸 캔 및 금속 용기

- 접이식 판지

- 골판지 상자

- 플렉서블 플라스틱(파우치, 파우치, 랩)

- 캡과 마개

- 리필 및 재사용 시스템

- 제품 유형별

- 스킨 케어

- 헤어 케어

- 오랄 케어

- 컬러 화장품

- 남성용 그루밍

- 데오도란트 및 향수

- 아기 케어

- 지속가능성 속성별

- 재활용 가능(단일 소재)

- 소비자재생이용(PCR)율

- 생분해성 및 퇴비화 가능

- 리필 및 리터너블

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Albea SA

- Amcor plc

- Silgan Holdings Inc.

- HCP Packaging(Shanghai) Co., Ltd.

- Berry Global Group, Inc.

- Gerresheimer AG

- AptarGroup, Inc.

- RPC Group Ltd(Berry Consumer Packaging Intl.)

- DS Smith Plc

- Huhtamaki Oyj

- Quadpack Industries, SA

- Rieke Packaging Systems Ltd.

- Shanghai Luxe-Pack Co., Ltd.

- Zhejiang Jinsheng New-Material Holding Group Co., Ltd.

- Shandong Yuhua Packing Products Co., Ltd.

- Guangzhou Beauty Packaging Co., Ltd.

- Xiamen Hexing Packaging Co., Ltd.

- Taizhou Forest Color Printing Packing Co., Ltd.

- Yunnan Yuxi Paper Co., Ltd.

- Ningbo NBG Plastic Packaging Co., Ltd.

제7장 시장 기회 및 향후 전망

AJY 25.11.21The China personal care packaging market reached USD 12.08 billion in 2025 and is forecast to expand to USD 17.01 billion by 2030, reflecting a 7.07% CAGR over the period.

This trajectory is propelled by regulatory measures that curb excessive packaging, the rapid migration of beauty shopping to social-commerce channels, and brand commitments to carbon-neutral operations. Sustainable material innovation, e-commerce-ready structural designs, and premium-tier product launches are converging to redefine competitive positioning across the value chain. Brands are investing in AI-assisted prototyping to trim development cycles, while packaging converters balance lightweighting with durability demands for nationwide last-mile delivery. Heightened enforcement of the GB 23350-2021 standard, the roll-out of China's national carbon trading scheme, and real-time social media feedback loops will continue to shape material choices and design parameters for the China personal care packaging market.

China Personal Care Packaging Market Trends and Insights

E-commerce boom for beauty and personal care

Explosive social-commerce growth is forcing brands to engineer packs capable of surviving wide-radius fulfilment while staging a photogenic unboxing moment. Douyin's beauty GMV more than doubled between 2021 and 2023, turning platform algorithm trends into near-instant packaging briefs for converters. Brands now weigh impact resistance, dimensional weight, and camera-ready aesthetics in equal measure. As fulfillment centers proliferate outside coastal provinces, flexible pouches and lightweight corrugates gain favor for their cushioning and freight-saving attributes, reinforcing the momentum of the China personal care packaging market.

Rise of refill-ready retail formats

Circularity targets from premium beauty houses accelerated trials of refill pods, concentrate sachets, and in-store bulk dispensers. Shiseido aims for 100% sustainable packaging by 2025 and has extended refill options to hero SKUs, prompting local ODMs to retool injection-molding lines for plug-in cartridges. Early pilots in Shanghai malls show consumers accepting reusable cores when refill stations are adjacent to point-of-sale, unlocking repeat-purchase stickiness and trimming material footprints.

Volatile resin and aluminum prices

Feedstock swings, driven by oil price gyrations and geopolitical uncertainty, are compressing converter margins. PET chip producers such as Wankai trimmed operating rates to 76% in late 2024, tightening supply and pushing converters to hedge through multi-month contracts or diversify into HDPE and PP blends. Smaller firms struggling to absorb surcharges may become acquisition targets, spurring gradual consolidation within the China personal care packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization of skincare and cosmetic SKUs

- Male grooming uptake in lower-tier cities

- Recycling capacity bottlenecks for multi-layer laminates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic retained 58.47% of the China personal care packaging market share in 2024 owing to cost efficiency and process agility. Yet the GB 23350-2021 interspace ratio cap is prompting brands to trim wall thickness and explore paperboard sleeves for secondary packs. Paper and paperboard's 8.23% CAGR positions it as the standout growth engine, propelled by consumers equating fiber-based packs with environmental stewardship. Glass volumes are stabilizing in prestige skincare where weight signals luxury, while metal aerosols gain favor in premium deodorants as they align with infinitely recyclable narratives. Volatile resin prices further amplify the case for blended substrate strategies across the China personal care packaging market.

A steady pipeline of bio-based polymers has emerged, but many blends require industrial composting conditions that remain scarce. Consequently, producers are investing in mono-material PP tubes and PCR-rich PET bottles that meet recyclability thresholds without compromising barrier performance. State-owned banks' green finance instruments are expected to lower capital costs for retrofitting lines capable of handling recycled content, keeping material decisions tightly linked to both sustainability scorecards and input-cost hedging.

Plastic bottles and jars controlled 41.63% of 2024 revenues, backed by entrenched blow-molding assets and consumer familiarity. Flexible plastic pouches, however, are clocking an 8.07% CAGR as brands exploit weight savings that translate into lower courier tariffs. Tamper-evident zippers and gusseted bases are now standard to survive multi-node delivery routes while presenting flat fronts for influencer video close-ups. Tubes and sticks gain incremental traction alongside the male grooming boom, while refill cartridges enable footprint reduction in top-shelf skincare. Pumps, droppers, and actuators face cost pressure from metal spring components but benefit from premiumization that values dosage accuracy within the China personal care packaging market.

Corrugated shippers are evolving from plain kraft cubes into co-branded, print-on-demand canvases for social-media storytelling. Yet they must still comply with the GB 43352-2023 express-pack regulation limiting heavy-metal content, nudging converters toward water-based inks and starch adhesives. Aerosol cans and specialty glass remain niche by volume but over-index in value due to fragrance and spa-grade treatments that command higher averaged selling prices.

The China Personal Care Packaging Market is Segmented by Material Type (Plastic, Glass, Metal, Paper and Paperboard, and Bio-Based and Compostable Plastics), Packaging Type (Plastic Bottles and Jars, Tubes and Sticks, Pumps, Sprayers and Droppers, and More), Product Type (Skincare, Haircare, Oral Care, and More), and Sustainability Attribute (Recyclable, Post-Consumer Recycled (PCR) Content, Biodegradable, and More).

List of Companies Covered in this Report:

- Albea S.A.

- Amcor plc

- Silgan Holdings Inc.

- HCP Packaging (Shanghai) Co., Ltd.

- Berry Global Group, Inc.

- Gerresheimer AG

- AptarGroup, Inc.

- RPC Group Ltd (Berry Consumer Packaging Intl.)

- DS Smith Plc

- Huhtamaki Oyj

- Quadpack Industries, S.A.

- Rieke Packaging Systems Ltd.

- Shanghai Luxe-Pack Co., Ltd.

- Zhejiang Jinsheng New-Material Holding Group Co., Ltd.

- Shandong Yuhua Packing Products Co., Ltd.

- Guangzhou Beauty Packaging Co., Ltd.

- Xiamen Hexing Packaging Co., Ltd.

- Taizhou Forest Color Printing Packing Co., Ltd.

- Yunnan Yuxi Paper Co., Ltd.

- Ningbo NBG Plastic Packaging Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom for beauty and personal care

- 4.2.2 Rise of refill-ready retail formats

- 4.2.3 Premiumisation of skincare and cosmetic SKUs

- 4.2.4 Male grooming uptake in lower-tier cities

- 4.2.5 AI-enabled design and rapid prototyping

- 4.2.6 Mandatory "excessive-packaging" compliance (GB 23350-2021)

- 4.3 Market Restraints

- 4.3.1 Volatile resin and aluminum prices

- 4.3.2 Recycling capacity bottlenecks for multi-layer laminates

- 4.3.3 Stricter carbon-intensity quotas for plastics

- 4.3.4 Counterfeiting risk in secondary packaging

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Paper and Paperboard

- 5.1.5 Bio-based and Compostable Plastics

- 5.2 By Packaging Type

- 5.2.1 Plastic Bottles and Jars

- 5.2.2 Tubes and Sticks

- 5.2.3 Pumps, Sprayers and Droppers

- 5.2.4 Aerosol Cans and Metal Containers

- 5.2.5 Folding Cartons

- 5.2.6 Corrugated Boxes

- 5.2.7 Flexible Plastic (Pouches, Sachets, Wraps)

- 5.2.8 Caps and Closures

- 5.2.9 Refillable / Reuse Systems

- 5.3 By Product Type

- 5.3.1 Skincare

- 5.3.2 Haircare

- 5.3.3 Oral Care

- 5.3.4 Color Cosmetics

- 5.3.5 Men's Grooming

- 5.3.6 Deodorants and Fragrances

- 5.3.7 Baby Care

- 5.4 By Sustainability Attribute

- 5.4.1 Recyclable (Mono-material)

- 5.4.2 Post-Consumer Recycled (PCR) Content

- 5.4.3 Biodegradable / Compostable

- 5.4.4 Refillable / Returnable

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Albea S.A.

- 6.4.2 Amcor plc

- 6.4.3 Silgan Holdings Inc.

- 6.4.4 HCP Packaging (Shanghai) Co., Ltd.

- 6.4.5 Berry Global Group, Inc.

- 6.4.6 Gerresheimer AG

- 6.4.7 AptarGroup, Inc.

- 6.4.8 RPC Group Ltd (Berry Consumer Packaging Intl.)

- 6.4.9 DS Smith Plc

- 6.4.10 Huhtamaki Oyj

- 6.4.11 Quadpack Industries, S.A.

- 6.4.12 Rieke Packaging Systems Ltd.

- 6.4.13 Shanghai Luxe-Pack Co., Ltd.

- 6.4.14 Zhejiang Jinsheng New-Material Holding Group Co., Ltd.

- 6.4.15 Shandong Yuhua Packing Products Co., Ltd.

- 6.4.16 Guangzhou Beauty Packaging Co., Ltd.

- 6.4.17 Xiamen Hexing Packaging Co., Ltd.

- 6.4.18 Taizhou Forest Color Printing Packing Co., Ltd.

- 6.4.19 Yunnan Yuxi Paper Co., Ltd.

- 6.4.20 Ningbo NBG Plastic Packaging Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment