|

시장보고서

상품코드

1851392

와인 포장 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Wine Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

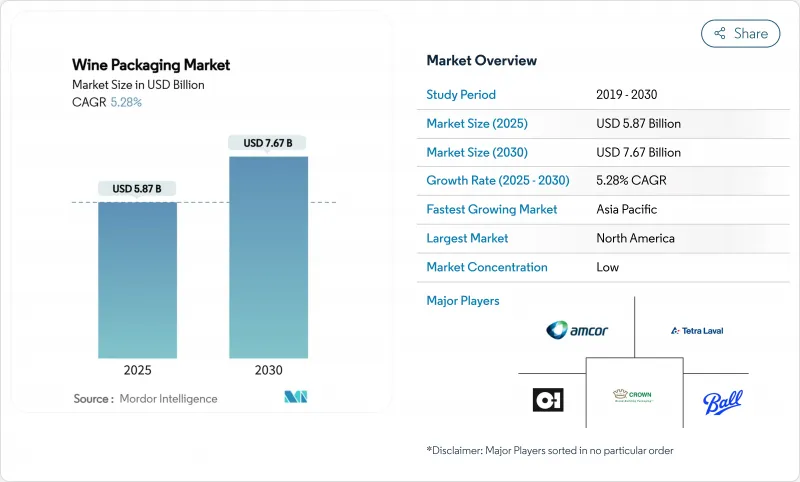

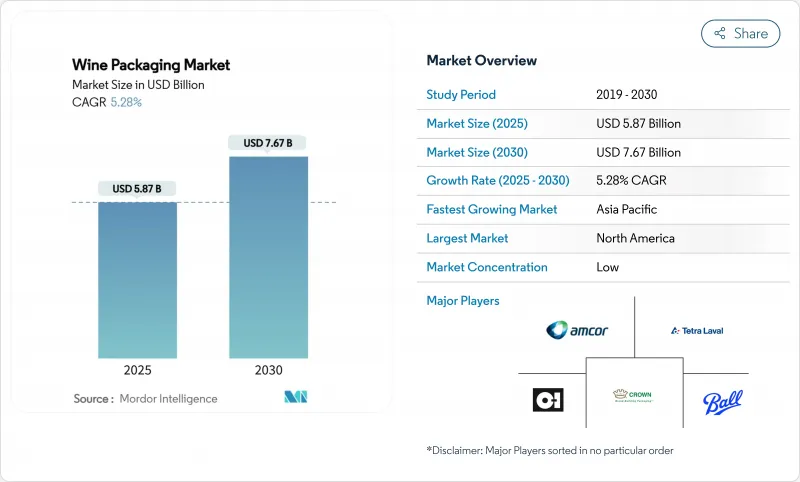

세계의 와인 포장 시장 규모는 2025년 58억 7,000만 달러에 달하고, 2030년에는 76억 7,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 5.28%로 추이합니다.

왕성한 유리병 수요, 경량 디자인에 대한 관심의 높아짐, 캔이나 백 인 박스 등의 대체 포맷의 급속한 채용이, 이 궤도를 이끌고 있습니다. 중국에서의 프리미엄화, 유럽에서의 경량 유리의 전개, 북미에서의 소비자에게 직접 판매(DtC)의 가속은 와인 포장 시장 전체의 생산 규모와 물류 경제성을 재구축하고 있습니다. EU의 2030년까지 100% 재활용 의무화부터 캘리포니아 주 상환가치 확대까지의 규제압력은 유리가격 변동이 계속되는 가운데 공급업체를 순환형 재료와 에너지 효율이 높은 퍼니스로 밀어주고 있습니다. 금속 패키지의 재활용성은 젊고 움직이는 소비자들에게 호소하며, 바이오 클로저는 포도원이 지속가능성 실천을 인증함에 따라 지지를 모으고 있습니다.

세계 와인 포장 시장 동향과 통찰

중국의 와인 프리미엄화가 디자이너스 병 수요를 높입니다.

중국의 젊은 도시 지역의 소비자들은 편의성과 합리적인 가격을 중시하면서도 정교한 디자인을 품질과 연결합니다. Huadong Winery의 배럴 와인과 Franzia의 박스 와인과 같은 혁신은 브랜드 에쿼티를 얇게 하지 않고 캐주얼한 모임을 지원하며 와인 포장 시장에서 프리미엄 스타일의 선택을 끌어올리고 있습니다.

CO2 감소를 위한 유럽 와이너리를 통한 경량 유리병 채택

Bourgogne의 탄소 중립 로드맵은 병의 무게가 중요한 배출 촉진요인임을 밝혔습니다. Verallia의 300g의 Bordeaux Air는 가벼운 병으로 전통을 유지하면서 CO2를 최대 40%까지 줄일 수 있음을 입증하여 와인 포장 시장 전반에 걸쳐 광범위한 채용을 촉진했습니다.

EU 플라스틱 포장세로 PET 솔루션 비용 상승

PFAS의 사용 금지와 재생재 함량의 의무화로 인해 PET의 컴플라이언스 비용이 상승하고 와인 포장 시장의 프리미엄 라인에서 경쟁력이 떨어지고 있습니다.

부문 분석

유리는 2024년 와인 포장 시장의 68.22%를 차지하는 불활성 특성과 고급 스러움을 가졌습니다. 경량로 업그레이드 및 컬릿 비율 향상은 배출량을 줄이면서 리더십을 유지하는 데 도움이 됩니다. 금속의 CAGR 8.43%는 알루미늄의 재활용성과 냉각 속도의 우위성을 반영하고 있어, 아웃도어 지향의 소비자를 매료해, 와인 포장 시장 전체의 장래의 기호를 형성하고 있습니다. Frugalpac의 종이병과 PET 하이브리드는 규제 당국이 100% 재활용 가능한 목표를 추진하면서 소재 분야의 폭을 넓히고 있습니다.

플라스틱과 종이의 진보는 오랜 히에라키를 시험합니다. Frugalpac의 섬유 쉘은 유리보다 플라스틱 사용량이 77% 적고, 탄소 실적도 84% 낮습니다. 유리 제조업체는 전기로와 초경량 설계를 시험적으로 도입함으로써 대응하고 있습니다. 알루미늄 병은 리실러블 톱을 활용하여 신선도를 오래 유지시키고, 바이오의 PET는 최대 30%의 rPET를 통합하고 있지만, 재활용 원료공급 확대를 기다리고 있습니다.

기존 병은 2024년 판매의 55.76%를 차지하며 저장 및 의식용 축입니다. 그래도 캔은 CAGR 7.88%로 성장하고 있으며, 와인 포장 시장 내 싱글 서브 편의성과 경기장 규제를 충족하고 있습니다. 백 인 박스 라인은 스케일 메리트를 달성하고 스웨덴 수량의 56%를 차지하며 프리미엄 등급의 진화를 이야기하고 있습니다.

PET병은 ALPLA의 장벽층에 의해 6개월의 유통기한에서 틈새 역할을 확보하고, 파우치는 페스티벌의 점유율을 획득하고 있습니다. EU의 디지털 의무에 대응한 스마트 라벨은 병에도 캔에도 붙여져, 추적 가능성를 충실시키고, 와인 포장 시장의 옴니 채널 전략을 강화하고 있습니다.

지역 분석

북미가 가장 큰 매출 공헌국임에 변화는 없습니다. 캘리포니아에서는 DtC법과 재활용 확대를 통해 5센트와 10센트의 보증금을 통합하여 와인 포장 시장을 커브사이드 대응 디자인으로 유도하고 있습니다. 유럽의 정책은 2030년까지 100%의 재활용을 가능하게 하고, 전기로에 대한 투자와 화물 배출량을 줄이는 백 박스 혁신에 박차를 가하고 있습니다.

아시아태평양은 2030년까지 성장을 이끌 것으로 보입니다. 중국의 프리미엄화는 디자이너스 유리와 비용 효율적인 상자를 믹스하고, 호주 보조금은 경량 PET 병과 종이 병을 지지해, 와인 포장 시장의 지역적인 기세를 가속시킵니다. 전자 식료품의 편의성이 환경 마케팅과 얽혀 젊은 소비자를 전환시킵니다.

중동 및 아프리카와 남미가 새로운 길을 제공합니다. 온난한 기후 지역에서는 더 가볍고 산화 배리어성이 높은 포장 형태가 선호되고 수출업체는 EU 규정을 충족하면서 운임을 최소화하는 포장을 채택하고 있습니다. 국내 생산자들은 새로운 음용자를 얻기 위해 rPET와 통조림 라인을 모색하여 와인 포장 업계의 혁신이 세계적으로 확산되고 있음을 보여줍니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중국에서의 와인의 프리미엄화가 디자이너스 병 수요를 견인

- 유럽 와이너리의 경량 유리병 채용으로 CO2 삭감

- 북유럽의 전자식료품 채널에서 백 인 박스의 급속한 보급

- 미국에서의 소비자 직접 판매(DtC) 채널의 대두가 On-Premise 포장을 가속

- 오세아니아에서 옥외 소비용 캔들이 와인과 PET 싱글 서브 와인의 급증

- 포도원의 지속가능성 인증이 바이오의 마개 채용을 촉진

- 시장 성장 억제요인

- EU 플라스틱 포장세가 PET 솔루션의 비용을 상승

- 세계의 재활용 원료 공급 부족이 rPET 와인 병의 전개를 제한

- 프리미엄 와인의 보급을 막는 대체 마개의 높은 산소 투과 리스크

- 소다 재의 가격 변동이 유리병 비용을 견인

- 공급망 분석

- 기술의 전망

- 규제 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 소재 유형별

- 유리

- 플라스틱

- 금속

- 종이

- 제품 유형별

- 유리병

- 페트병

- 백 인 박스

- 캔

- 파우치

- 클로저 유형별

- 천연 코르크

- 테크니컬 및 합성 코르크

- 스크류 캡

- 크라운 캡

- 기타(T 스토퍼, 비노록)

- 와인 유형별

- 스틸 와인

- 스파클링 와인

- 강화 와인 및 디저트 와인

- 저알코올 및 논알코올 와인

- 용량별

- 375mL 미만

- 375-750 mL

- 750-1,500 mL

- 1,500mL 이상

- 유통 채널별

- 직접 판매

- 간접 판매

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주, 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Owens-Illinois Inc.(OI)

- Verallia SA

- Ardagh Group SA

- Saverglass SAS

- Vetropack Holding AG

- BA Glass Group

- Consol Glass Pty Ltd

- Guala Closures Group

- Amorim Cork, SA

- Vinventions LLC(Nomacorc)

- Amcor plc

- Ball Corporation

- TricorBraun Inc.

- Tetra Laval International SA

- SIG Combibloc Group AG

- Scholle IPN(Sealed Air)

- Liqui-Box(Sealed Air)

- International Paper Company

- G3 Enterprises Inc.

- Maverick Enterprises Inc.

- Encore Glass Inc.

- Smurfit WestRock

- Crown Holdings, Inc.

제7장 시장 기회와 장래의 전망

JHS 25.11.13The wine packaging market size reached USD 5.87 billion in 2025 and is forecast to climb to USD 7.67 billion by 2030, advancing at a 5.28% CAGR over the period.

Strong glass bottle demand, growing interest in lightweight designs and the rapid adoption of alternative formats such as cans and bag-in-box options are steering this trajectory. Premiumisation in China, lightweight glass roll-outs in Europe, and direct-to-consumer (DtC) acceleration in North America are reshaping production scale and logistics economics across the wine packaging market. Regulatory pressure-from the European Union's 100%-recyclable-by-2030 mandate to California's redemption-value expansion-continues to push suppliers toward circular materials and energy-efficient furnaces, even as glass price volatility persists. Metal packaging's recyclability appeals to younger, mobile consumers while bio-based closures gain traction as vineyards certify sustainability practices.

Global Wine Packaging Market Trends and Insights

Premiumisation of Wine in China Elevating Demand for Designer Bottles

Young urban consumers in China value convenience and affordability yet still associate sophisticated design with quality. Innovations such as Huadong Winery's keg wine and Franzia's boxed offerings support casual gatherings without diluting brand equity, lifting premium-styled alternatives within the wine packaging market.

Lightweight Glass Bottle Adoption by European Wineries to Cut CO2

Bourgogne's carbon-neutral roadmap exposed bottle weight as a critical emissions driver; Verallia's 300 g Bordeaux Air proves that a lighter bottle can retain tradition while trimming up to 40% of CO2, propelling broader adoption across the wine packaging market.

EU Plastic Packaging Taxes Increasing Cost of PET Solutions

Mandatory recycled-content quotas and PFAS bans inflate compliance costs, making PET less competitive for premium lines within the wine packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Bag-in-Box Formats in the Nordics' E-grocery Channel

- Rise of DtC Channels in the US Accelerating On-premise Ready-to-Ship Packaging

- Global Recyclate Supply Shortages Limiting rPET Wine Bottle Roll-outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glass accounted for 68.22% of the wine packaging market in 2024 due to its inert nature and premium perception. Lightweight furnace upgrades and higher cullet ratios help maintain leadership while cutting emissions. Metal's 8.43% CAGR reflects aluminum's recyclability and chill-speed advantages, luring outdoor-oriented consumers and shaping future preference across the wine packaging market. Paper bottles from Frugalpac and PET hybrids broaden the material field as regulators push 100% recyclable targets.

Plastic and paper advances test longstanding hierarchies. Frugalpac's fibre shell uses 77% less plastic and holds an 84% lower carbon footprint than glass, making it an attractive alternative in the wine packaging industry. Glass manufacturers counter by piloting electric furnaces and ultra-light designs. Aluminum bottles leverage resealable tops to extend freshness, while bio-based PET integrates up to 30% rPET yet awaits greater recyclate supply.

Traditional bottles delivered 55.76% of 2024 revenue, an anchor for cellaring and ritual. Still, cans are growing at 7.88% CAGR, meeting single-serve convenience and stadium regulations within the wine packaging market. Bag-in-box lines achieve scale benefits and hold 56% of Swedish volume, illustrating premium-grade evolution.

PET bottles secure niche roles with six-month shelf life thanks to ALPLA's barrier layers, while pouches win festival share. Smart labels that satisfy EU digital mandates surface on bottles and cans alike, enriching traceability and reinforcing the wine packaging market's omnichannel strategy.

The Wine Packaging Market Report is Segmented by Material Type (Glass, Plastic, and More), Product Type (Glass Bottles, Plastic Bottles, and More), Closure Type (Natural Cork, and More), Wine Type (Still Wine, Sparkling Wine, and More), Capacity ( Less Than Equal To 375 ML, 375-750 ML, and More), Distribution Channel (Direct Sales, Indirect Sales), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remain the largest revenue contributor. Robust DtC laws and recycling expansion in California integrate 5- and 10-cent deposits that steer the wine packaging market toward curbside-compatible designs. European policies dictate 100% recyclability by 2030, sparking investment in electric furnaces and bag-in-box innovation that lowers freight emissions.

Asia-Pacific leads growth through 2030. China's premiumisation mixes designer glass with cost-effective boxes, while Australian grants back lightweight PET and paper bottles, accelerating regional momentum for the wine packaging market. E-grocery convenience intertwines with environmental marketing to convert younger consumers.

Middle East and Africa and South America provide emerging pathways. Warmer climates lean toward lighter, oxidation-barrier formats, and exporters deploy packaging that meets EU rules while minimizing freight. Domestic producers explore rPET and canning lines to reach new drinkers, illustrating the global spread of the wine packaging industry's innovations.

- Owens-Illinois Inc. (O-I)

- Verallia SA

- Ardagh Group SA

- Saverglass SAS

- Vetropack Holding AG

- BA Glass Group

- Consol Glass Pty Ltd

- Guala Closures Group

- Amorim Cork, S.A.

- Vinventions LLC (Nomacorc)

- Amcor plc

- Ball Corporation

- TricorBraun Inc.

- Tetra Laval International SA

- SIG Combibloc Group AG

- Scholle IPN (Sealed Air)

- Liqui-Box (Sealed Air)

- International Paper Company

- G3 Enterprises Inc.

- Maverick Enterprises Inc.

- Encore Glass Inc.

- Smurfit WestRock

- Crown Holdings, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumisation of Wine in China Elevating Demand for Designer Bottles

- 4.2.2 Light-weight Glass Bottle Adoption by European Wineries to Cut CO2

- 4.2.3 Rapid Uptake of Bag-in-Box Formats in the Nordics' E-grocery Channel

- 4.2.4 Rise of Direct-to-Consumer (DtC) Channels in the US Accelerating On-premise Ready-to-Ship Packaging

- 4.2.5 Surge in Canned and PET-Single-Serve Wines for Outdoor Consumption in Oceania

- 4.2.6 Vineyard Sustainability Certifications Driving Bio-based Closures Adoption

- 4.3 Market Restraints

- 4.3.1 EU Plastic Packaging Taxes Increasing Cost of PET Solutions

- 4.3.2 Global Recyclate Supply Shortages Limiting rPET Wine Bottle Roll-outs

- 4.3.3 Higher Oxygen Transmission Risk in Alternative Closures Capping Premium-Wine Penetration

- 4.3.4 Volatility in Soda-ash Pricing Inflating Glass Bottle Costs

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Glass

- 5.1.2 Plastic

- 5.1.3 Metal

- 5.1.4 Paper

- 5.2 By Product Type

- 5.2.1 Glass Bottles

- 5.2.2 Plastic Bottles

- 5.2.3 Bag-in-Box

- 5.2.4 Cans

- 5.2.5 Pouches

- 5.3 By Closure Type

- 5.3.1 Natural Cork

- 5.3.2 Technical/Synthetic Cork

- 5.3.3 Screw Caps

- 5.3.4 Crown Caps

- 5.3.5 Others (T-stoppers, Vino-Lok)

- 5.4 By Wine Type

- 5.4.1 Still Wine

- 5.4.2 Sparkling Wine

- 5.4.3 Fortified and Dessert Wine

- 5.4.4 Low and No-Alcohol Wine

- 5.5 By Capacity

- 5.5.1 Less than 375 mL

- 5.5.2 375-750 mL

- 5.5.3 750-1,500 mL

- 5.5.4 More than 1,500 mL

- 5.6 By Distribution Channel

- 5.6.1 Direct Sales

- 5.6.2 Indirect Sales

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia and New Zealand

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 Middle East

- 5.7.4.1.1 United Arab Emirates

- 5.7.4.1.2 Saudi Arabia

- 5.7.4.1.3 Turkey

- 5.7.4.1.4 Rest of Middle East

- 5.7.4.2 Africa

- 5.7.4.2.1 South Africa

- 5.7.4.2.2 Nigeria

- 5.7.4.2.3 Egypt

- 5.7.4.2.4 Rest of Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Owens-Illinois Inc. (O-I)

- 6.4.2 Verallia SA

- 6.4.3 Ardagh Group SA

- 6.4.4 Saverglass SAS

- 6.4.5 Vetropack Holding AG

- 6.4.6 BA Glass Group

- 6.4.7 Consol Glass Pty Ltd

- 6.4.8 Guala Closures Group

- 6.4.9 Amorim Cork, S.A.

- 6.4.10 Vinventions LLC (Nomacorc)

- 6.4.11 Amcor plc

- 6.4.12 Ball Corporation

- 6.4.13 TricorBraun Inc.

- 6.4.14 Tetra Laval International SA

- 6.4.15 SIG Combibloc Group AG

- 6.4.16 Scholle IPN (Sealed Air)

- 6.4.17 Liqui-Box (Sealed Air)

- 6.4.18 International Paper Company

- 6.4.19 G3 Enterprises Inc.

- 6.4.20 Maverick Enterprises Inc.

- 6.4.21 Encore Glass Inc.

- 6.4.22 Smurfit WestRock

- 6.4.23 Crown Holdings, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment