|

시장보고서

상품코드

1851408

전기 수술 기기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Electrosurgical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

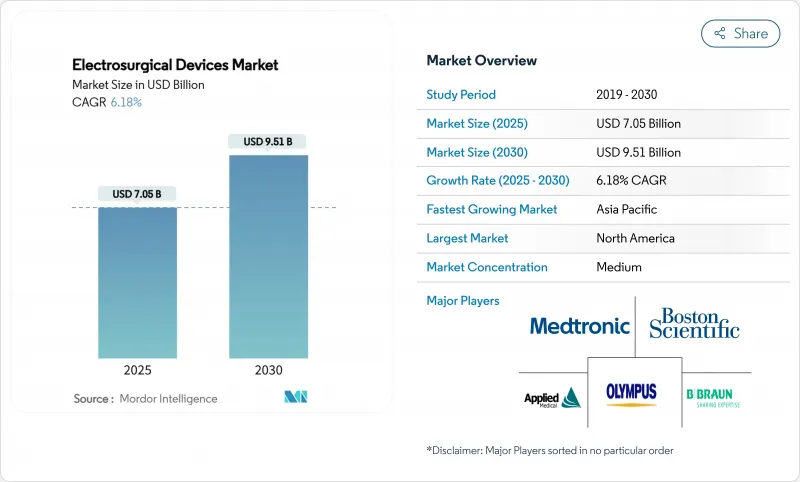

전기 수술 기기 시장 규모는 2025년에 70억 5,000만 달러, 2030년에는 95억 1,000만 달러에 이르고, CAGR은 6.18%를 나타낼 정도입니다.

인구 역학의 압력에 힘입어 병원과 외래 시설은 레거시 모노폴라 발전기에서 실시간으로 전력을 조정하는 통합 AI 가이드가 있는 에너지 플랫폼으로 빠르게 전환하고 있습니다. 낮은 침습 수술로의 꾸준한 이동은 외래수술센터(ASC)의 급증과 함께 작고 고정밀 시스템에 대한 일관된 수요를 지원합니다. 미국과 유럽연합(EU)에서 공급망의 현지화 촉진책이 국내 제조를 강화하는 한편, 희토류와 텅스텐의 가격 변동은 전기 수술 기기 시장 전체의 비용 관리를 강화하고 있습니다. 기존 기업은 인수, 지능형 장비 출시, 에너지 공급, 로봇 공학 및 배연을 단일 생태계에 통합하는 플랫폼의 번들 전략을 통해 점유율을 지키고 있기 때문에 경쟁 정보는 여전히 완만합니다.

세계의 전기 수술 기기 시장 동향과 통찰

만성 질환과 고령화 인구 증가

세계적인 장수화는 수술실에 들어가는 다질환 환자 증가를 의미하며, 당뇨병 이환율 증가에 따라 심장혈관 수술만으로도 급증할 것으로 예측되고 있습니다. 따라서 외과의사는 취약하고 합병증이 많은 조직 영역 내에서 지혈을 제어할 수 있는 바이폴라 플랫폼과 초음파 플랫폼이 필요합니다. 지능형 에너지 콘솔은 열 확산을 최소화하는 정확한 와트 수 조정을 제공하여 생리적 예비력이 부족한 노인 코호트의 우려를 완화합니다. 같은 인구 동향으로 인공 관절 치환술과 종양 절제술의 건수가 증가하고 있어 전기 수술용 기기 시장의 대응 가능한 밑단이 퍼지고 있습니다. 북미와 서유럽 병원은 조직의 임피던스 모니터링을 포함한 발전기 업그레이드를 두 배로 늘리고 있습니다. 장기적으로는 고령화와 만성질환의 복합효과에 의해 전체적인 CAGR 예측에 1.8%의 순풍이 더해집니다.

낮은 침습 수술에 대한 선호

지불자와 의료 제공업체는 보다 짧은 입원 기간과 더 빠른 직장 복귀를 주요 가치 지표로 만드는 경향이 커지고 있습니다. 복강경 수술, 흉강경 수술, 내시경 하 수술은 본질적으로 슬림하고 낮은 발열기구에 의존하기 때문에 첨단 바이폴라 전도 및 초음파 전도가 낮은 침습 수술실의 설비 예산의 대부분을 차지합니다. 이동식 타워 아래에 도킹할 수 있도록 설계된 소형 전기 수술 발전기는 혼잡한 OR 내의 귀중한 장소를 해제합니다. 아시아태평양에서 마이크로 절개의 도입은 한때 미국 특유의 성장 곡선에 가까워지고 있으며, 통합형 배연 장치 및 온도 제어 RF 전극의 수익 가능성을 확대하고 있습니다. 최근 4년간의 경제 모델에서 온도 관리 고주파 치료기는 계획 수준에서 2,000만 달러를 절약하고 치료 환자 1인당 3,531달러를 절약할 수 있음을 보여주며, 페이포 밸류의 논의가 강화되었습니다.

숙련된 전기 외과의 부족

SAGES의 FUSE 프로그램과 같은 시뮬레이션 기반 커리큘럼은 지식 점수를 향상 시켰지만, 완전히 인증된 전기 외과 의사 수요는 여전히 공급을 능가하고 있습니다. 저·중소득국에서는 많은 수술실에 프록터 제도가 없기 때문에 병원은 스태프의 능력이 향상될 때까지 제너레이터의 업그레이드를 늦추고 있습니다. 2023년에 행해진 관찰자 맹검하의 연구에 따르면, 연수의가 루프 전기 수술 절제술을 쾌적하게 실시할 수 있게 된 것은 10회의 가이드 첨부 연습을 실시한 후였습니다. 기술 부족은 전기 수술 기기 시장의 CAGR 예측에서 1.1% 포인트 뺍니다.

부문 분석

기구와 액세서리는 2024년 매출의 54.86%를 차지했고, 이 카테고리의 전기 수술 기기 시장 규모를 38억 7,000만 달러로 확대되었습니다. 일회용 바이폴라 포셉, 초음파 전도 및 배연 연필은 계절적 절차의 변동을 완화하는 정기적인 판매 플라이휠을 생산합니다. 현재, 기술이 복잡해짐에 따라 10ms 이내에 임피던스 데이터를 발전기에 전달하는 열 센서가 내장 된 활성 전극이 선호되고 있습니다. 이러한 지능형 칩을 구입하는 병원은 일반적으로 자체 케이블 생태계를 구축하고 있기 때문에 브랜드 충성도가 확립되어 공급업체의 평생 계정 가치가 향상되었습니다. 초음파 블레이드와 하이브리드 RF-초음파 블레이드는 기존의 모노폴라 아크가 신경 손상의 위험이 있는 경구강 갑상선 절제술과 로봇 갑상선 절제술과 같은 틈새 영역에서 증가하고 있습니다.

액티브 전극은 가장 급성장하는 하위 부문이며, 외과의사가 미주 에너지를 완화시키는 촉각 피드백이나 자동 정지 기능을 요구하고 있기 때문에 CAGR 7.86%로 성장하고 있습니다. 특수 액세서리의 전기 수술 기기 시장 점유율은 단일 사용 센서 칩으로 기울어 질 것으로 예상되는데, 이는 감염 관리 담당자가 완전한 추적 성이없는 재 가공 된 전극을 금지하는 경향이 강해졌기 때문입니다. 발전기 수요는 견고하지만, 2016년 이전에 제조된 콘솔에는 현장 업그레이드가 가능한 펌웨어 슬롯이 없기 때문에 교체 사이클이 빨라지고 있습니다. 한편, 배연 캡처 패드를 통합한 액세서리 번들은 미국의 외래 조달 파이프라인을 빠르게 통과하고 있으며, 주 금연 OR 의무화를 충족합니다.

이것은 표준화된 에너지 설정에 의존하는 맹장, 탈장, 담낭 적출 등의 다양한 사례를 반영합니다. 이것은 표준화된 에너지 설정에 의존하는 맹장, 탈장, 담낭 절제술의 사례의 광범위를 반영합니다. 이와 병행하여 미용정형외과의 선택적 수요가 증가하고 있으며, CAGR 8.16%로 성장할 것으로 예측되고 있습니다. 이 부문의 환자는 흉터가 적고 응고가 억제되는 것을 선호하기 때문에 초음파 박리기와 팁이 얇은 바이폴라 집게가 선택되었습니다.

심장혈관 수술과 뇌신경 외과 팀은 핸드피스를 교체하지 않고 1MHz 바이폴라 실링에서 47kHz 초음파 박리로 전환할 수 있는 듀얼 모달리티 콘솔에 기울고 있습니다. 부인과 종양의사는 복강경하 자궁절제술 시 장막 손상을 줄이기 위해 열 센서 전도를 채택하고 있습니다. 하이브리드 전문 수술실에서 파생된 전기 수술 기기 시장 규모는 분야 횡단 팀이 단일 완전한 기능을 갖춘 발전기 플랫폼을 선호하기 때문에 오른쪽 어깨 상승이 예상됩니다. 또한 임플란트 삽입 전 관절 공간을 최적화하기 위해 RF 기반 코팅 릴리스를 사용하는 정형외과 재치환술도 향후 성장할 것으로 보입니다.

전기 수술 기기 시장 보고서는 제품별(전기외과용 제너레이터, 기구 및 부속품(바이폴라 기구, 기타), 용도별(일반 수술, 뇌신경 외과, 기타), 에너지 모달리티별(모노폴라 고주파, 바이폴라 고주파, 기타), 최종 사용자별(병원, 외래수술센터(ASC), 기타), 지역별(북미)

지역별 분석

북미는 2024년 매출의 42.14%를 확보했습니다. 이는 미국 병원이 강력한 상환 제도와 광대한 ASC 네트워크를 활용하여 AI 대응 에너지 콘솔로 차량을 새로 고쳤기 때문입니다. 캐나다의 단일 지불 제도는 예산 제약이 있음에도 불구하고 새로 제정된 노동 안전 기준을 충족하기 위해 통합 배연 시설로 업그레이드되었습니다. 멕시코 사립 병원은 의료 관광의 경쟁력을 높이기 위해 고급 바이폴라 초음파 하이브리드에 투자했습니다. 미국에서는 공급망 현지화 보조금으로 인쇄회로기판과 페라이트 코어의 리드타임이 단축되어 연방정부의 회복력 목표에 부합하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2030년까지 연평균 복합 성장률(CAGR)은 8.89%를 나타낼 전망입니다. 중국이 이 지역 수요를 뒷받침하는 것은 야심찬 병원 근대화 추진책과 국내 OEM이 대학과 지능형 에너지 플랫폼을 공동 개발하도록 돕는 메이드 인 차이나 2025 장려금입니다. 세계에서 가장 급속하게 고령화가 진행되는 일본은 복강경하 대장 절제술용 정밀 초음파 암 시스템을 조달하고 있습니다. 인도의 민간 병원 체인은 전기 수술 타워를 턴키 수술 번들로 포장하고 외국인 의료 관광객에게 번들 된 투명한 가격으로 제공합니다. 호주와 한국은 비만 수술과 종양 수술 증가에 대응하기 위해 고급 양극 밀봉 장치를 수입하고 환태평양 지역의 전기 수술 기기 시장 규모를 더욱 확대하고 있습니다.

유럽에서는 독일, 프랑스, 영국이 EU-MDR 문서화의 장애물을 극복하면서 OR 스위트를 업그레이드하고 있으며 한 자리 대 중반의 안정적인 성장을 기록하고 있습니다. 남유럽 국가들은 배연·플룸 여과 시스템의 자본 구매를 부분적으로 보조하는 EU 부흥 기금의 혜택을 받고 있습니다. 북유럽 병원은 데이터 풍부한 수술 플랫폼을 신속하게 채택하고 발전기 데이터 스트림을 국가 수술 품질 등록에 통합하여 증거 기반 조달을 강화하고 있습니다. 그러나 사우디아라비아의 '비전 2030'과 아랍에미리트(UAE)의 의료 프리존에서 대규모 인프라 계획이 프리미엄 에너지 플랫폼에 새로운 길을 열고 있습니다. 남미와 아프리카는 현재의 점유율은 소폭이지만, 국민 모두 보험제도가 확대됨에 따라 상향할 가능성을 갖고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 증가와 고령화

- 저침습 수술의 기호

- 지능형 에너지 플랫폼으로의 기술 이동

- 외래수술센터(ASC) 붐(ASC건설 러쉬)

- 정밀 절단을 위한 AI 가이드 부착 조직 센싱

- 공급망의 현지화 인센티브(미국, EU)

- 시장 성장 억제요인

- 숙련된 전기외과의 부족

- 엄격한 기기 재인증(EU-MDR)

- 열상 소송 위험 급증

- 희토류와 텅스텐의 가격 변동

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 전기 수술용 발전기

- 액티브 전극

- 의료기기 및 부속품

- 바이폴라 기기

- 모노폴라 기기

- 초음파 & 첨단 에너지

- 액세서리(케이블, 칩, 훈제 에백)

- 용도별

- 일반 외과

- 뇌신경외과

- 부인과 수술

- 심장혈관 수술

- 정형외과

- 미용 정형외과

- 기타 특수 수술

- 에너지 양식별

- 모노폴라 고주파

- 바이폴라 고주파

- 초음파

- 하이브리드/고급 바이폴라 초음파

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉 & 오피스

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medtronic plc

- Johnson & Johnson(Ethicon)

- Olympus Corporation

- CONMED Corporation

- B. Braun SE

- Boston Scientific Corporation

- Stryker Corporation

- Smith & Nephew plc

- Applied Medical Resources Corp.

- ERBE Elektromedizin GmbH

- Kirwan Surgical Products LLC

- Symmetry Surgical Inc.(Aspen Surgical Products, Inc.)

- Apyx Medical Corporation

- Utah Medical Products Inc.

- KLS Martin Group

- De Soutter Medical Ltd.

- Teleflex Incorporated

- Steris plc

제7장 시장 기회와 장래의 전망

SHW 25.11.21The electrosurgical devices market size reached USD 7.05 billion in 2025 and is forecast to attain USD 9.51 billion by 2030, advancing at a 6.18% CAGR.

Spurred by demographic pressure, hospitals and ambulatory facilities are moving swiftly from legacy monopolar generators to integrated, AI-guided energy platforms that modulate power in real time. A steady shift toward minimally invasive procedures, coupled with the proliferation of ambulatory surgical centers (ASCs), is underpinning consistent demand for compact, high-precision systems. Supply-chain localization incentives in the United States and European Union reinforce domestic manufacturing, while rare-earth and tungsten price swings are tightening cost controls across the electrosurgical devices market. Competitive intensity remains moderate as incumbents defend share through acquisitions, intelligent instrument launches and platform bundling strategies that embed energy delivery, robotics and smoke evacuation into a single ecosystem.

Global Electrosurgical Devices Market Trends and Insights

Rise in Chronic Diseases & Ageing Population

Global longevity gains mean more poly-morbid patients entering operating rooms, and cardiovascular procedures alone are projected to climb sharply as diabetes incidence rises. Surgeons therefore require bipolar and ultrasonic platforms capable of controlled hemostasis inside fragile, comorbid tissue fields. Intelligent energy consoles deliver precise wattage adjustments that minimize thermal spread, easing concerns in elderly cohorts with limited physiologic reserve. The same demographic trend is escalating volume in joint-replacement revisions and oncologic resections, extending the addressable base of the electrosurgical devices market. Hospitals in North America and Western Europe are doubling down on generator upgrades that embed tissue-impedance monitoring so that any inadvertent rise in tissue temperature is recognized and corrected within milliseconds. Over the long term, the compounding effect of aging and chronic illness adds a 1.8 percentage-point tailwind to overall CAGR projections.

Minimally-Invasive Surgery Preference

Payers and providers increasingly rank shorter length of stay and faster return-to-work as prime value metrics. Laparoscopic, thoracoscopic and endoscopic approaches inherently depend on slim, low-heat instruments, which explains why advanced bipolar and ultrasonic shears dominate capital budgets for minimally invasive suites. Compact electrosurgical generators designed to dock under mobile towers free up valuable real estate inside crowded ORs. Micro-incision adoption in Asia-Pacific is now approaching growth curves once unique to the United States, broadening revenue potential for integrated smoke evacuation and temperature-controlled RF electrodes. A recent four-year economic model showed that temperature-controlled radiofrequency instruments yielded plan-level savings of USD 20 million and USD 3,531 per treated patient, reinforcing pay-for-value arguments.

Shortage of Skilled Electrosurgeons

Simulation-based curricula such as SAGES' FUSE program have improved knowledge scores, yet demand for fully credentialed electrosurgeons still outstrips supply. In low- and middle-income countries, many operating rooms lack proctorship, causing hospitals to delay generator upgrades until staff competencies rise. A 2023 observer-blinded study documented that residents' comfort performing Loop Electrosurgical Excision jumped only after 10 guided practice sessions, underscoring the steep learning curve. Skill scarcity subtracts 1.1 percentage points from the electrosurgical devices market CAGR forecast.

Other drivers and restraints analyzed in the detailed report include:

- Technology Shift to Intelligent Energy Platforms

- Outpatient Surgery Center Boom (ASC Build-Outs)

- Stringent Device Re-Certification (EU-MDR)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments and Accessories delivered 54.86% of 2024 revenue, anchoring the electrosurgical devices market size at USD 3.87 billion for the category. Disposable bipolar forceps, ultrasonically activated shears and smoke evacuation pencils create a recurring sales flywheel that cushions seasonal procedure swings. Rising procedure complexity now favors active electrodes embedded with thermal sensors that relay impedance data to generators in under 10 milliseconds. Hospitals purchasing these intelligent tips typically lock into proprietary cable ecosystems, which further entrenches brand loyalty and drives higher lifetime account value for vendors. Ultrasonic and hybrid RF-ultrasonic blades are gaining in niche domains such as trans-oral and robotic thyroidectomy where traditional monopolar arcs risk nerve damage.

Active Electrodes represent the fastest-growing subsegment, advancing at a 7.86% CAGR as surgeons seek tactile feedback and auto-stop features that mitigate stray energy. The electrosurgical devices market share within specialty accessories is expected to tilt toward single-use, sensor-enabled tips because infection-control officers increasingly bar reprocessed electrodes without full traceability. Generator demand remains steady; however, consoles built before 2016 lack field-upgradable firmware slots, accelerating replacement cycles. Meanwhile, accessory bundles that integrate smoke evacuation capture pads are moving rapidly through U.S. outpatient procurement pipelines, fulfilling state smoke-free OR mandates.

General Surgery generated 30.64% of 2024 sales, reflecting the breadth of appendectomy, hernia, and cholecystectomy cases that rely on standardized energy settings. This considerable base underpins predictable cash flow even when elective orthopedic or cosmetic volumes dip. In parallel, rising elective aesthetics demand lifts Cosmetic & Plastic Surgery, which is projected to clip along at an 8.16% CAGR. Patients in this segment prioritize low scarring and controlled coagulation, making ultrasonic dissectors and fine-tip bipolar forceps the instruments of choice.

Cardiovascular and Neurosurgery teams gravitate toward dual-modality consoles able to switch from 1 MHz bipolar sealing to 47 kHz ultrasonic dissection without changing handpieces. Gynecologic oncologists adopt thermal-sensor shears to reduce serosal injury during laparoscopic hysterectomy. The electrosurgical devices market size derived from hybrid specialty suites is expected to climb steadily because cross-disciplinary teams prefer a single, fully featured generator platform. Future procedure growth will also derive from orthopedic revisions that use RF-based capsular release to optimize joint space before implant insertion.

The Electrosurgical Devices Market Report is Segmented by Product (Electrosurgical Generators, Instruments and Accessories [Bipolar Instruments, and More], and More), by Application (General Surgery, Neurosurgery, and More), by Energy Modality (Monopolar Radio-Frequency, Bipolar Radio-Frequency, and More), by End User (Hospitals, Ambulatory Surgical Centers, and More), by Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America secured 42.14% of 2024 revenue as U.S. hospitals leveraged robust reimbursement schemes and an expansive ASC network to refresh fleets with AI-enabled energy consoles. Canada's single-payer system, under budget constraint, nonetheless upgraded to integrated smoke evacuation to meet newly enacted occupational safety standards. Mexico's private hospitals invested in premium bipolar-ultrasonic hybrids to boost medical-tourism competitiveness. Supply-chain localization grants in the United States are shortening lead times for printed circuit boards and ferrite cores, aligning with federal resilience goals.

Asia-Pacific is the fastest-growing theatre, posting an 8.89% CAGR forecast through 2030. China anchors regional demand thanks to an ambitious hospital-modernization drive and Made-in-China 2025 incentives that nudge domestic OEMs to co-develop intelligent energy platforms with universities. Japan, burdened by the world's most rapidly aging population, sources precision ultrasonic scalpel systems for laparoscopic colectomy. India's private hospital chains package electrosurgery towers within turnkey surgical bundles offered to international medical tourists at bundled, transparent pricing. Australia and South Korea import advanced bipolar sealing devices to tackle rising bariatric and oncologic surgery volumes, further expanding the electrosurgical devices market size across the Pacific Rim.

Europe registers stable, mid-single-digit growth as Germany, France and the United Kingdom upgrade OR suites while steering through EU-MDR documentation hurdles. Southern European countries benefit from EU recovery funds that partially subsidize capital purchases of smoke evacuation and plume filtration systems. Nordic hospitals, early adopters of data-rich surgical platforms, integrate generator data streams into national surgical quality registries, reinforcing evidence-based procurement. Eastern European and GCC growth remains opportunistic; however, large infrastructure programs in Saudi Arabia's Vision 2030 and the United Arab Emirates' medical free-zones are opening fresh avenues for premium energy platforms. South America and Africa collectively contribute a modest share today but hold upside potential as universal healthcare expansions unfold.

- Medtronic

- Johnson & Johnson

- Olympus

- Conmed

- B. Braun

- Boston Scientific

- Stryker

- Smiths Group

- Applied Medical Resources

- Erbe Elektromedizin

- Kirwan Surgical Products

- Symmetry Surgical Inc. (Aspen Surgical Products, Inc.)

- Apyx Medical

- Utah Medical Products

- KLS Martin Group

- De Soutter Medical Ltd.

- Teleflex

- Steris plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in chronic diseases & ageing population

- 4.2.2 Minimally-invasive surgery preference

- 4.2.3 Technology shift to intelligent energy platforms

- 4.2.4 Outpatient surgery center boom (ASC build-outs)

- 4.2.5 AI-guided tissue sensing for precision cutting

- 4.2.6 Supply-chain localization incentives (USA, EU)

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled electrosurgeons

- 4.3.2 Stringent device re-certification (EU-MDR)

- 4.3.3 Thermal injury litigation risk spike

- 4.3.4 Rare-earth & tungsten price volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Electrosurgical Generators

- 5.1.2 Active Electrodes

- 5.1.3 Instruments and Accessories

- 5.1.3.1 Bipolar Instruments

- 5.1.3.2 Monopolar Instruments

- 5.1.3.3 Ultrasonic & Advanced Energy

- 5.1.3.4 Accessories (Cables, Tips, Smoke Evac)

- 5.2 By Application

- 5.2.1 General Surgery

- 5.2.2 Neurosurgery

- 5.2.3 Gynecology Surgery

- 5.2.4 Cardiovascular Surgery

- 5.2.5 Orthopedic Surgery

- 5.2.6 Cosmetic & Plastic Surgery

- 5.2.7 Other Specialized Procedures

- 5.3 By Energy Modality

- 5.3.1 Monopolar Radio-frequency

- 5.3.2 Bipolar Radio-frequency

- 5.3.3 Ultrasonic

- 5.3.4 Hybrid/Advanced Bipolar-Ultrasonic

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Clinics & Offices

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Medtronic plc

- 6.3.2 Johnson & Johnson (Ethicon)

- 6.3.3 Olympus Corporation

- 6.3.4 CONMED Corporation

- 6.3.5 B. Braun SE

- 6.3.6 Boston Scientific Corporation

- 6.3.7 Stryker Corporation

- 6.3.8 Smith & Nephew plc

- 6.3.9 Applied Medical Resources Corp.

- 6.3.10 ERBE Elektromedizin GmbH

- 6.3.11 Kirwan Surgical Products LLC

- 6.3.12 Symmetry Surgical Inc. (Aspen Surgical Products, Inc.)

- 6.3.13 Apyx Medical Corporation

- 6.3.14 Utah Medical Products Inc.

- 6.3.15 KLS Martin Group

- 6.3.16 De Soutter Medical Ltd.

- 6.3.17 Teleflex Incorporated

- 6.3.18 Steris plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment