|

시장보고서

상품코드

1907219

해상 보안 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Maritime Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

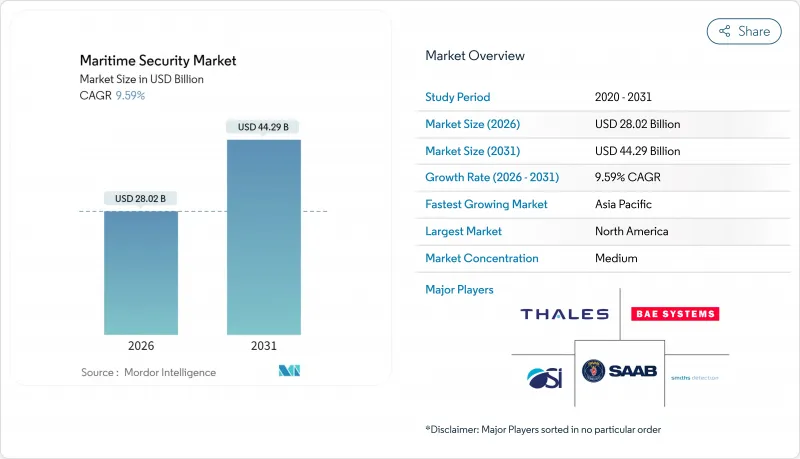

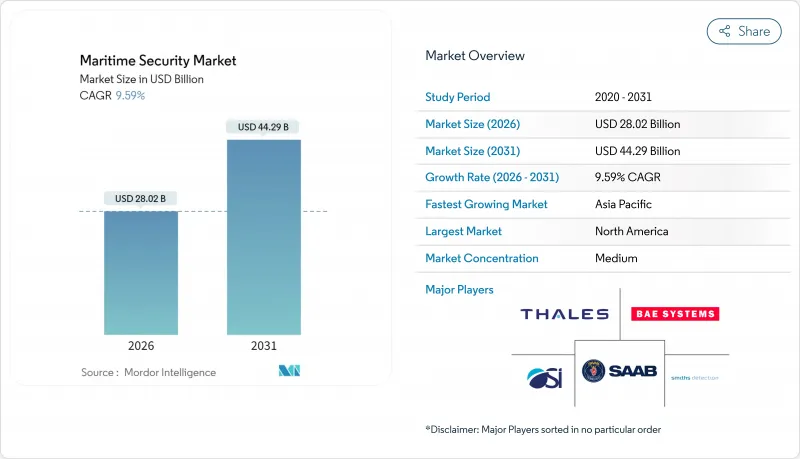

해상 보안 시장은 2025년 255억 7,000만 달러로 평가되었고, 2026년 280억 2,000만 달러에서 2031년까지 442억 9,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) 동안 CAGR은 9.59%로 성장이 전망됩니다.

해적 행위 증가, 사이버 기술을 이용한 방해 공작, 확대하는 규제 요건에 의해 통합 모니터링, 스크리닝 및 탄력 플랫폼에 대한 예산 배분이 진행되고 있습니다. 북미는 엄격한 규제 및 현대적인 항만 자산에 지지되어 주도적 지위를 유지하는 한편, 아시아태평양에서는 급속한 해상 에너지 개발 및 다국간 안보 프로그램이 2자리 성장을 견인하고 있습니다. 2023년 11월-2024년 11월 사이에 홍해만으로 69건의 공격이 발생해 기존의 순찰망의 커버 범위에 미비가 노출되었기 때문에 사업자들은 경비원에 의한 억제에서 AI 구동의 상황 인식으로 이행하고 있습니다. 고위험 항로 보험료는 3배로 뛰어 올라 예측 위협 감지 시스템의 상업적 합리성이 강화되었습니다. 현재의 지출은 레이더, AIS, 영상, 사이버 분석을 융합한 항만, 선박 및 연안역을 횡단하는 상호 운용 가능한 지휘 플랫폼을 우선하고 있습니다.

세계의 해상 보안 시장 동향 및 인사이트

해적 행위 및 해상 위협 증가

MV 룬호(2023년)와 MV 압둘라호(2024년)의 납치 사건은 소말리아 범죄 조직이 홍해에서 해군의 재배치를 악용하고 몸값 요구형 모델을 부활시킨 실태를 부각시켰습니다. 국제해사국(IMB) 기록에 따르면 2024년 해적 행위는 116건 발생했고 인질사건은 3배로 증가하여 126명의 선원이 구속되었습니다. 이에 따라 운항회사는 미국 해군 제59 임무부대가 감시하는 자율형 수상 드론의 채용을 강요받았으며, 그 무인 운용 시간은 50,000시간을 넘었습니다. 전쟁 리스크 보험 비용은 위기 전의 3배로 상승하고 AI 탑재 조기 경계 레이더와 지속적인 전기 광학 페이로드의 도입이 촉진되고 있습니다.

국제 안보 규제 강화

근대화된 국제 해상 조난 안전 시스템(GMDSS)이 2024년 1월에 시행되어 선박 및 해양 시설용 통신 기기의 디지털화가 의무화되었습니다. 이와 병행하여 미국 해안경비대가 2025년 7월에 도입하는 사이버보안 규칙에서는 전선박 및 시설에 사이버보안 책임자의 배치가 요구되어 6억 달러 규모의 컴플라이언스 시장이 창출되었습니다. 벨기에는 더욱 밟아 40개의 터미널에서 생체인증 게이트 관리를 의무화하고, 하루 4만 7,000건의 신원 확인을 실시했습니다.

높은 초기 비용 및 예산 제약

종합적인 경계 울타리, 생체 인증 게이트 및 다층화물 스크리닝은 터미널 당 200만 달러를 초과할 수 있으며 2025년 갱신으로 이미 보험료가 2.5-7.5% 상승한 중소 사업자를 괴롭히고 있습니다. 인플레이션으로 인한 이익률 저하로 자본 집약적 업그레이드의 자금 조달이 억제되고 세계 해상 보험료의 성장이 둔화되고 있습니다.

부문 분석

모니터링 및 추적 솔루션은 2025년 매출의 34.41%를 차지하며, 운항 사업자가 지속적인 영역 인식을 필요로 하는 해사 보안 시장의 기반이 되고 있습니다. 지휘 통제(C2) 제품군은 연간 11.28%의 성장이 예상되며 자율적인 수상 무인 항공기의 운영 조정과 위성 SAR 데이터의 통합 시각화 요구를 반영합니다. 서브와 ICEYE의 제휴는 클라우드를 통한 레이더 데이터가 전술적 판단을 어떻게 변화시키는지를 보여줍니다. 모니터링 솔루션의 해상 보안 시장 규모는 업계 전반에 걸쳐 확대되고 2030년까지 두 자리의 대폭적인 성장이 예상됩니다. 항법 레이더에 내장된 엣지 분석에 의해 하드웨어 교환 없이 소프트웨어 패치 적용이 가능해져 라이프 사이클 비용을 압축시킵니다. 예측 보전을 위한 해상 디지털 트윈 도입을 촉진합니다.

AI 능력의 향상은 스크리닝 능력도 높입니다. OSI Systems의 Eagle M60 계약은 피더 항구에서 이동식 고에너지 드라이브 스루형 스캐너 수요 증가를 시사합니다. 현대화된 GMDSS 규칙은 선박 라디오의 업데이트 사이클을 촉진하고 암호화된 데이터 링크의 교차 셀을 추진하고 있습니다. 벨기에 항만 전역에서 의무화된 사이버 강화형 접근 시스템은 생체 인증의 도입이 선택적 요건이 아니라 규제 요건임을 뒷받침합니다. 그 결과 해상 보안 시장은 사일로화된 하드웨어에서 모듈식 소프트웨어 정의 에코시스템으로 이행을 계속하여 주요 계약업체와 틈새 AI 기업에 병행한 성장 경로를 제공합니다.

지역별 분석

북미는 성숙한 항만 시설 및 엄격한 보안 코드에 의해 지원되었으며 2025년 수익의 37.41%를 차지했습니다. 미국 해안 경비대의 새로운 사이버 규칙은 6억 달러의 컴플라이언스 틈새 시장을 탄생시켰습니다. 동시에 록히드 마틴의 AN/TPQ-53 레이더는 오픈 아키텍처의 소프트웨어 업그레이드를 통해 육상 국경 경비 장치가 해안 감시에도 활용할 수 있음을 입증하고 있습니다. 캐나다의 잠수함 재자본화 계획 및 멕시코의 통합 연안 레이더의 채택도 대륙 수요에 박차를 가하고 있습니다.

아시아태평양은 중국이 해양 석유 개발을 확대하고 인도가 미국 해군과 1억 2,500만 달러의 영역 인식 프로젝트에 자금을 제공하는 등 11.05%의 연평균 복합 성장률(CAGR)로 성장하고 있는 가장 급성장하고 있는 지역입니다. 일본은 해상 라디오를 위한 최초의 DNV 사이버 인증을 획득했습니다. 한국은 해군의 강력한 연구개발을 반영한 드론 운반함의 컨셉 'HCX-23 Plus'를 발표했습니다. 이러한 노력과 싱가포르의 무인 항만 초계정의 도입은 기술 도입에 대한 국가 수준의 노력을 이야기하고 있습니다.

유럽은 규제 측면에서의 주도성 및 실용적인 전개의 균형을 도모하고 있습니다. EU는 홍해와 아덴만을 MARPOL 부속서 I의 특별 구역에 추가하고, 운항자에게 추가적인 오염 방지 및 보안 장비의 탑재를 의무화했습니다. 독일과 스웨덴은 그림자 선단 유조선에 대한 경계를 강화했으며 벨기에의 생체 인증 시스템 도입은 유럽 기준을 확립했습니다. 홍해의 정세 불안에 의해 2024년에는 중동 및 아프리카에서 19건의 해적 사건이 발생했습니다. 이를 통해 소말릴랜드의 벨베라 항구가 대체 대피 항구로 정비를 진행하고 있습니다(meforum.org). 지역별 리스크 프로파일에 따라 운항사업자는 물리적 억지력(해군 옵션)과 확장 가능한 감시망 중 어느 것을 선택할지 판단하지만, 모든 지역에서 AI를 활용한 상황 인식 능력이 핵심 기반으로 공통 인식이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 해적 행위 및 해사 위협 증가

- 보다 엄격한 국제 보안 규정

- 세계 해운 무역의 성장

- 통합 감시 및 스크리닝 시스템 도입

- 보안 연동형 보험료 인센티브

- ESG 연동형 금융이 사이버 레지리언스 추진

- 시장 성장 억제요인

- 높은 초기 비용 및 예산 제약

- 레거시 인프라 통합의 복잡성

- 데이터 프라이버시 및 주권에 대한 우려

- 해사 사이버 인재 부족

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 시스템별

- 스크리닝 및 스캐닝

- 통신 시스템

- 감시 및 추적

- 액세스 제어 및 생체 인증

- 지휘통제(C2) 플랫폼

- 항행 관리 및 AIS

- 유형별

- 항만 및 중요 인프라 보안

- 선박의 안전 대책

- 연안 및 국경 경비

- 최종 사용자별

- 상선 회사

- 항만 당국 및 터미널 운영 회사

- 해군 및 해안 경비대

- 석유 및 가스 해양 사업자

- 크루즈선 및 페리회사

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향 및 진전

- 시장 점유율 분석

- 기업 프로파일

- Saab AB

- Thales Group

- Leonardo SpA

- Elbit Systems Ltd.

- Airbus SE

- BAE Systems plc

- Kongsberg Gruppen ASA

- Terma A/S

- Westminster Group Plc

- Smiths Detection Group Limited(Smiths Group plc)

- OSI Maritime Systems

- Nuctech Technology Co., Ltd.

- ATLAS ELEKTRONIK GmbH

- ARES Security Corporation

- HGH Systemes Infrarouges SAS

- HALO Maritime Defense Systems

- Teledyne Technologies Incorporated

- Honeywell International Inc.

제7장 시장 기회 및 장래 전망

AJY 26.01.26The maritime security market was valued at USD 25.57 billion in 2025 and estimated to grow from USD 28.02 billion in 2026 to reach USD 44.29 billion by 2031, at a CAGR of 9.59% during the forecast period (2026-2031).

Heightened piracy, cyber-enabled sabotage, and expanding regulatory mandates are steering budgets toward integrated surveillance, screening, and resilience platforms. North America retains leadership, supported by rigorous rules and modern port assets, while rapid offshore energy development and multilateral security programmes propel Asia-Pacific's double-digit growth. Operators are shifting from guard-based deterrence to AI-driven situational awareness, as 69 attacks in the Red Sea alone during November 2023-November 2024 exposed gaps in conventional patrol coverage. Insurance premiums on high-risk routes tripled, strengthening the commercial case for predictive threat-detection suites. Spending now prioritizes interoperable command platforms across ports, vessels, and coastal zones that fuse radar, AIS, video, and cyber analytics.

Global Maritime Security Market Trends and Insights

Rising Piracy and Maritime Threats

The hijackings of MV Ruen (2023) and MV Abdullah (2024) underlined how Somali criminal networks exploited naval redeployments in the Red Sea, reviving ransom-based models. The International Maritime Bureau logged 116 piracy incidents in 2024, and hostage cases tripled to 126 seafarers. This pressured operators to adopt autonomous surface drones monitored by the US Navy's Task Force 59, which surpassed 50,000 unmanned operating hours. War-risk cover now costs three times pre-crisis levels, incentivising AI-enabled early-warning radars and persistent electro-optic payloads.

Stricter International Security Regulations

The modernised Global Maritime Distress and Safety System (GMDSS) entered force in January 2024, obliging fleets to replace legacy gear with digital communication suites for marine and offshore. In parallel, the US Coast Guard's July 2025 cybersecurity rule requires every vessel and facility to appoint a Cybersecurity Officer, unlocking a USD 600 million compliance opportunity. Belgium went further, mandating biometric gate control across 40 terminals handling 47,000 identities daily.

High Upfront Cost and Budget Constraints

Comprehensive perimeter fencing, biometric gates, and multilayer cargo screening can exceed USD 2 million per terminal, challenging smaller operators whose insurance bills already face 2.5-7.5% increases for 2025 renewals. Global marine insurance premium growth slowed as inflation eroded margins, curbing financing for capital-heavy upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Global Seaborne Trade

- Adoption of Integrated Surveillance and Screening

- Legacy Infrastructure Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surveillance and tracking held 34.41% revenue in 2025, anchoring the maritime security market as operators require continuous domain awareness. Command-and-control (C2) suites are projected to grow 11.28% annually, reflecting the need to orchestrate autonomous surface drones and integrate satellite SAR feeds into a single picture. Saab's pact with ICEYE underscores how cloud-delivered radar data reshapes tactical decisions. The maritime security market size for surveillance solutions is expected to scale with the broader industry, reaching significant double-digit gains by 2030. Edge analytics embedded in navigation radars allow software patching without hardware swaps, compressing lifecycle costs, and encouraging maritime digital twins for predictive maintenance.

Growing AI capability also elevates screening. OSI Systems' Eagle M60 contract signalled rising demand for mobile, high-energy drive-through scanners at feeder ports. Modernised GMDSS rules prompt a replacement cycle in maritime radios, driving cross-selling of encrypted data links. Cyber-hardened access systems mandated across Belgian ports validate biometric uptake as a regulatory rather than an optional requirement. As a result, the maritime security market continues to shift from siloed hardware toward modular, software-defined ecosystems, giving prime contractors and niche AI firms parallel growth avenues.

The Maritime Security Market Report is Segmented by System (Screening and Scanning, Communication Systems, Surveillance and Tracking, and More), Type (Port and Critical Infrastructure Security, and More), End User (Commercial Shipping Companies, Port Authorities and Terminal Operators, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 37.41% of 2025 revenue, underpinned by a mature port estate and stringent security codes. The new US Coast Guard cyber rule generates a USD 600 million compliance niche. At the same time, Lockheed Martin's AN/TPQ-53 radar demonstrates how open-architecture software upgrades extend land-border devices into littoral monitoring. Canada's submarine recapitalisation plan and Mexico's adoption of integrated coastal radars add to continental demand.

Asia-Pacific is the fastest-growing theatre, advancing at an 11.05% CAGR as China scales offshore oil and India funds a USD 125 million domain-awareness project with the US Navy. Japan secured the first DNV cyber certificate for maritime radios prtimes.jp. South Korea unveiled the HCX-23 Plus drone-carrier concept, reflecting heavy naval R&D. These initiatives and Singapore's rollout of uncrewed harbour patrol boats illustrate state-level commitment to technology adoption.

Europe balances regulatory leadership with pragmatic deployment. The EU added the Red Sea and Gulf of Aden to special areas under MARPOL Annex I, obliging operators to fit additional pollution-control and security gear. Germany and Sweden intensified patrols against shadow-fleet tankers, while Belgium's biometric rollout sets a continental benchmark. Red Sea turbulence produced 19 pirate incidents in the Middle East and Africa in 2024, prompting Somaliland's Berbera Port upgrade as an alternative haven, meforum.org. Regional risk profiles determine whether operators favour hard-kill naval options or scalable surveillance grids, but every region converges on AI-enabled situational awareness as the core enabler.

- Saab AB

- Thales Group

- Leonardo S.p.A

- Elbit Systems Ltd.

- Airbus SE

- BAE Systems plc

- Kongsberg Gruppen ASA

- Terma A/S

- Westminster Group Plc

- Smiths Detection Group Limited (Smiths Group plc)

- OSI Maritime Systems

- Nuctech Technology Co., Ltd.

- ATLAS ELEKTRONIK GmbH

- ARES Security Corporation

- HGH Systemes Infrarouges SAS

- HALO Maritime Defense Systems

- Teledyne Technologies Incorporated

- Honeywell International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising piracy and maritime threats

- 4.2.2 Stricter international security regulations

- 4.2.3 Growth of global seaborne trade

- 4.2.4 Adoption of integrated surveillance and screening

- 4.2.5 Security-linked insurance premium incentives

- 4.2.6 ESG-linked financing drives cyber-resilience

- 4.3 Market Restraints

- 4.3.1 High upfront cost and budget constraints

- 4.3.2 Legacy infrastructure integration complexity

- 4.3.3 Data-privacy and sovereignty concerns

- 4.3.4 Maritime-cyber talent shortage

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By System

- 5.1.1 Screening and Scanning

- 5.1.2 Communications Systems

- 5.1.3 Surveillance and Tracking

- 5.1.4 Access Control and Biometrics

- 5.1.5 Command and Control (C2) Platforms

- 5.1.6 Navigation Management and AIS

- 5.2 By Type

- 5.2.1 Port and Critical Infrastructure Security

- 5.2.2 Vessel Security

- 5.2.3 Coastal and Border Security

- 5.3 By End User

- 5.3.1 Commercial Shipping Companies

- 5.3.2 Port Authorities and Terminal Operators

- 5.3.3 Naval and Coast Guard

- 5.3.4 Oil and Gas Offshore Operators

- 5.3.5 Cruise and Ferry Lines

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Russia

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Saab AB

- 6.4.2 Thales Group

- 6.4.3 Leonardo S.p.A

- 6.4.4 Elbit Systems Ltd.

- 6.4.5 Airbus SE

- 6.4.6 BAE Systems plc

- 6.4.7 Kongsberg Gruppen ASA

- 6.4.8 Terma A/S

- 6.4.9 Westminster Group Plc

- 6.4.10 Smiths Detection Group Limited (Smiths Group plc)

- 6.4.11 OSI Maritime Systems

- 6.4.12 Nuctech Technology Co., Ltd.

- 6.4.13 ATLAS ELEKTRONIK GmbH

- 6.4.14 ARES Security Corporation

- 6.4.15 HGH Systemes Infrarouges SAS

- 6.4.16 HALO Maritime Defense Systems

- 6.4.17 Teledyne Technologies Incorporated

- 6.4.18 Honeywell International Inc.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment