|

시장보고서

상품코드

1851425

열교환기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Heat Exchanger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

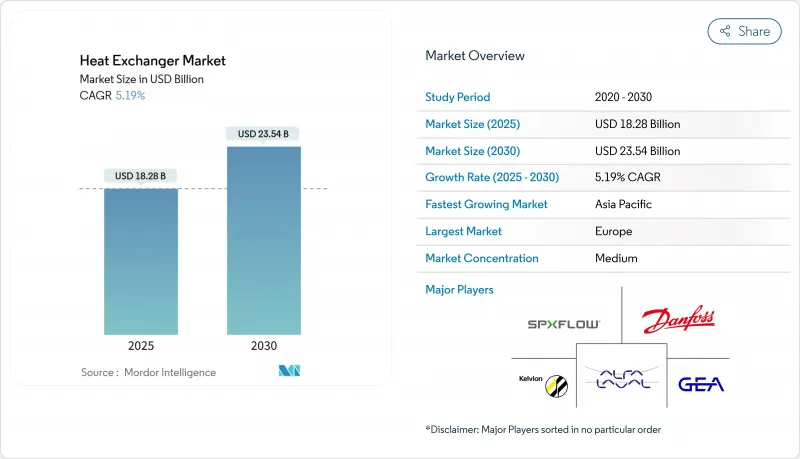

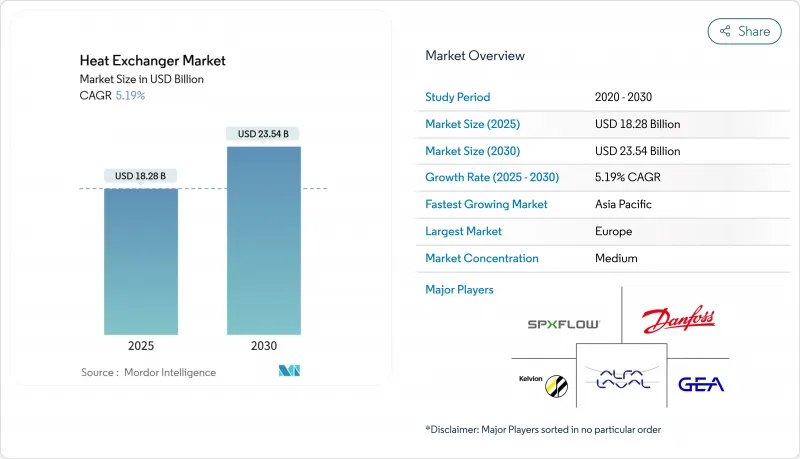

열교환기 시장 규모는 2025년에 182억 8,000만 달러, 2030년에는 235억 4,000만 달러에 이르고, 예측기간(2025-2030년)의 CAGR은 5.19%를 나타낼 전망입니다.

성장의 원동력이 되고 있는 것은 LNG 인프라의 구축, 데이터센터의 액냉 채택, 산업용 보일러나 지역 에너지·네트워크의 효율 업을 촉진하는 규제 등입니다. 쉘 앤 튜브 방식이 고압 용도의 주력인 것에 변함은 없지만, 절수가 조달 결정을 뒷받침하고 있기 때문에 공냉 장치가 급속하게 확대하고 있습니다. 수소의 파일럿 프로젝트와 초임계 CO2 전력 사이클에 따라 이국적인 합금에 대한 수요가 증가하는 반면, 극압과 공간 제약이 겹치는 곳에서는 모듈식 인쇄 회로 설계가 견인력을 증가시키고 있습니다. 한편, 전문 제조업체는 극저온 LNG 트레인이나 200 기압 수소 유닛 등의 틈새 시장을 타겟으로 하고 있습니다.

세계 열교환기 시장 동향과 통찰

LNG 액화 프로젝트의 급증으로 극저온 교환기 수요를 끌어올립니다.

세계적인 중형 및 대규모 LNG 트레인 건설은 -150°C 이하에서 성능을 발휘하는 코일 권취 유닛과 플레이트 핀 유닛이 요구되는 반면, 엄격한 열적 접근도 유지되므로 고품질 스테인리스 스틸 및 알루미늄 합금 조달이 가속화되고 있습니다. 모듈식 열교환기 스키드는 건설 스케줄을 단축하고 비용 초과를 억제하며 경량화 및 난류 강화를 위해 3D 프린팅된 플로우 플레이트를 통합하는 제조업체에게 이익을 제공합니다. 2025년부터 2026년까지는 멕시코 걸프와 카타르의 메가 프로젝트가 열교환기 시장의 중심이 될 것으로 예상되며 아시아 전역의 브라운필드의 디보틀 네킹에 의한 2차 수요도 전망됩니다. ASME 섹션 VIII 인증을 받고 12주 납기를 제공하는 공급업체는 EPC 기업이 시설 목록을 표준화하여 타임라인 위험을 줄이기 위해 프레임워크 계약을 확보할 것으로 보입니다.

GCC와 동남아시아 지역 냉각의 확대가 플레이트 프레임 판매를 견인

두바이, 리야드, 싱가포르와 같은 습도가 높은 도시에서는 지역 냉방 시스템에 대한 보조금이 지속적으로 피크 전력 부하를 줄이기 위해 유틸리티 회사는 컴팩트한 설치 면적과 용이한 용량 확장을 통해 개스킷식 플레이트 프레임 교환기를 지정하게 되었습니다. 이러한 배치는 소금물 부식을 줄이기 위해 스테인레스 스틸과 티타늄 플레이트에 의존하며 지구 운영자는 99%의 가용성 보증을 요구합니다. 상태 모니터링 센서를 번들로 제공하는 OEM은 컨세션 운영자가 성능 기반 유지보수 모델로 전환하여 정기적인 서비스 수익을 얻을 수 있는 것으로 보입니다.

니켈과 티타늄의 가격 변동이 내식성 장치 가격 상승

1급 니켈과 항공우주 등급의 티타늄 가격은 2024년 이후 전분기 대비 최대 35% 변동하여 소재를 다운스펙할 수 없는 수소, 해양, 해양 프로젝트의 주문 파이프라인을 약화시켰습니다. 패브리케이터는 EPC 고객에게 과금을 전가하지만, 예산 초과는 프로젝트 연기의 방아쇠가 되고 열교환기 시장의 단기 수량은 줄어들고 있습니다. 스테인레스 스틸 클래드 플레이트는 노출을 부분적으로 상쇄하지만 이종 금속의 확산 접합은 용접의 무결성 인증을 복잡하게 합니다.

부문 분석

2024년 열교환기 시장 점유율은 쉘 및 튜브 설계가 35%를 차지했고 압력이 60bar를 초과하며 파울링 마진이 높을 때 기본 옵션으로 자리를 유지합니다. 표준화된 TEMA 분류는 정유소, LNG 전처리 트레인, 황 회수 장치의 사양을 간소화하고 애프터마켓 수익을 지원하는 튜브 번들과 개스킷의 반복 주문을 지원합니다. 동시에 인도, 텍사스, 중동의 물 부족 전력 회사가 폐수 무방류 전략을 우선해 강제 통풍 팬과 저소음 기어 박스를 탑재한 유닛을 구동하고 있기 때문에 공냉형 CAGR이 6% 상승하고 있습니다.

2025년부터 2030년까지는 설계자가 종래의 쉘에서는 대응할 수 없는 컴팩트한 풋 프린트를 요구하고 있기 때문에 프린트 회로나 나선형 감기의 포맷이 고압 수소나 초임계 CO2 사이클의 쉐어를 긁는다고 생각됩니다. 그럼에도 불구하고, 열교환기 시장에서는 기존의 노즐 위치가 개조 번들에 적합하고 라이프 사이클 비용을 예측하기 쉽기 때문에 브라운필드의 개수에는 계속 쉘&튜브가 선호될 것입니다. 스테인레스 스틸 쉘과 구리 니켈 튜브를 혼합한 선박용 스크러버는 IMO2020의 컴플라이언스 예산을 획득하여 수량에 약간의 상승을 가져올 것으로 보입니다.

스테인레스 스틸은 2024년 열교환기 시장 규모의 30%를 유지합니다. 식음료, 제약 라인에서는 위생 마무리와 저탄소 함량을 통해 고비용 합금을 사용하지 않고도 규제를 충족시킬 수 있습니다. 티타늄, 니켈, 잉콜로이, 하스테로이 등의 이국적인 합금은 2030년까지 연평균 복합 성장률(CAGR)이 6.5%로 성장을 지속하여, 염화물을 많이 포함한 염수나 수소 취화에 의해 스테인리스를 선택할 수 없는 수소, 해수 담수화, 해상 풍력 컨버터 플랫폼을 도입하고 있습니다.

폴리머와 복합재료는 PTFE와 흑연 블록이 특히 반도체 습식 에칭 및 리튬 이온 배터리 재활용에서 강산성 또는 불화물을 포함하는 흐름 아래 금속을 능가하기 때문에 작은 기초에서 성장합니다. Additive Manufacturing은 부식이 심한 부분에만 높은 합금 재료를 배치하는 듀얼 머티리얼 격자를 구현하여 비용과 무게를 줄입니다. 이러한 기술 혁신을 통해 열교환기 업계는 기존의 스테인리스 카탈로그에 얽매이지 않고 응용 분야에 특화된 야금학으로 전환하고 있습니다.

열교환기 시장 보고서는 유형별(쉘&튜브, 플레이트 프레임, 공냉, 기타), 구조재료별(스테인리스 스틸, 탄소강, 기타), 플로우 어레인지먼트별(향류, 병류, 크로스 플로우, 하이브리드/멀티패스), 최종 사용자 산업별(석유 및 가스, 발전, 물 및 폐수 처리, 기타), 지역별(북미, 아시아태평양, 남미 및 기타)로 세분화됩니다.

지역 분석

유럽은 2024년 세계 매출의 33%를 차지했으며, 보일러 리모델링과 지역 에너지 전개를 추진하는 EU의 에코디자인 지령에 힘쓰고 있습니다. 독일의 종합 수소 전략은 전해조 플랜트의 인쇄 회로 프로토타입에 자금을 유도하고 열교환 기 시장의 고가치 일각을 지원합니다. 프랑스는 소형 안전 클래스 교환기가 필요한 SMR 프로젝트를 가속화하고 북유럽 국가들은 티타늄 플레이트 팩을 사용하여 주변 해수를 이용하는 저온 지역 루프를 개척합니다. EN13445 압력 용기 인증을 유지하는 OEM 및 지역 내의 예비 부품 허브는 가동 시간 보증이 입찰 점수의 상위를 차지하는 동안 점유율을 획득합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 5.9%를 기록해 중국의 석유화학 생산 능력 증강, 인도의 전력 플릿 확대, ASEAN의 지구 냉방 이권이 수량의 성장을 지지합니다. 국내 제조업체는 비용면에서 유리한 공급망을 활용하여 쉘 앤 튜브의 수주를 획득하고, 한일 기업은 암모니아 분해 파일럿용 티타늄과 니켈 PCHE에 주력하고 있습니다. 현지 EPC는 10주 이내에 출하되는 모듈식 스키드를 제공하는 공급업체를 높이 평가하며, 세계 브랜드는 제조의 현지화를 촉구하고 있습니다.

북미에서는 멕시코 걸프의 LNG 수출 터미널과 버지니아, 텍사스 및 퀘벡 주에서 데이터센터 캠퍼스 확장의 혜택을 누리고 있습니다. 미국 에너지부의 수소 허브는 확산 접합 니켈 합금을 사용한 PCHE 실증 시험에 보조금을 제공합니다. 캐나다의 오일 샌드 사업자는 에어 핀 유닛을 개수하여 취수량을 줄이고 팬 어시스트 장치에 2차적인 흡입력을 낳고 있습니다. 라틴아메리카에서는 채광 정광과 태양열 발전소가 부티크 수주를 견인하고 중동에서는 해수 담수화와 석유화학의 메가 컴플렉스가 수요를 지지하고 있습니다. 아프리카의 기세는 구리 벨트의 제련의 업그레이드와 맞물려 점진적이지만 안정적으로 유지되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 극저온 교환기 수요 증가를 위한 LNG 액화 프로젝트의 급증

- GCC와 동남아시아 지역 냉방 확대가 플레이트 프레임 판매를 견인

- 수소 파일럿 플랜트, 200bar의 서비스에 프린트 회로 교환기를 채택

- 개조 튜브 번들에 박차를 가하는 EU 산업용 보일러 필수 업그레이드

- SMR(소형 모듈로) 전개에는 소형의 안전급 교환기 필요

- 데이터센터의 액냉 도입이 마이크로채널 채택을 가속

- 시장 성장 억제요인

- 니켈 및 티타늄 가격 변동성 팽창 부식 방지 장치

- 바이오 정제소에서의 채택을 제한하는 바이오 공정 오염 문제

- 엔지니어링 투 오더 설계를 위한 12주 리드 타임 억제를 위한 EPC 수요

- 발전소의 직접 공랭 방식이 공랭식 열교환기를 잠식(대체)함

- 공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 쉘 및 튜브

- 플레이트&프레임(가스켓 플레이트, 브레이징 플레이트, 용접 플레이트)

- 공냉(핀 & 튜브, 플레이트 핀, 마이크로채널)

- 재생식(로터리 및 플레이트)

- 프린트 회로

- 기타(더블 파이프, 나선형, 코아키셜)

- 건설재료별

- 스테인리스

- 탄소강

- 비철(구리, 알루미늄)

- 이국적인 합금(티타늄, 니켈, 하스테로이)

- 폴리머 및 복합재료(PTFE, 그라파이트, 세라믹)

- 플로우 배열별

- 역전류

- 병렬

- 크로스 플로우

- 하이브리드/멀티패스

- 최종 이용 산업별

- 석유 및 가스

- 화학제품 및 석유화학제품

- 발전(원자력 포함)

- 식음료

- 펄프 및 종이

- 상하수도 처리

- 기타 산업(자동차 및 수송, 야금, 광업, HVACR, 제약 및 생명공학)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 칠레

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 파트너십, PPA)

- 시장 점유율 분석(주요 기업의 시장 순위/점유율)

- 기업 프로파일

- Alfa Laval AB

- Kelvion Holding GmbH

- Danfoss A/S

- SPX Flow Inc.

- GEA Group AG

- Hisaka Works Ltd.

- Xylem Inc.

- Thermax Ltd.

- Mersen SA

- API Heat Transfer Inc.

- GE Vernova Inc.

- Barriquand Technologies Thermiques SAS

- Koch Heat Transfer Company LP

- SWEP International AB

- Heatric

- Kobelco Steel Ltd.

- Accessen Group

- Funke Warmeaustauscher GmbH

- Tranter Inc.

- HRS Heat Exchangers Ltd.

- Hamon Thermal Europe SA

- Graham Corporation

- United Heat Transfer Ltd.

- KRN Heat Exchanger & Refrigeration Ltd.

제7장 시장 기회와 장래의 전망

SHW 25.11.21The Heat Exchanger Market size is estimated at USD 18.28 billion in 2025, and is expected to reach USD 23.54 billion by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

Growth is fueled by LNG infrastructure build-outs, data-center liquid-cooling adoption, and regulations that force efficiency upgrades in industrial boilers and district energy networks. Shell-and-tube systems remain the mainstay for high-pressure duties, yet air-cooled equipment is scaling rapidly as water conservation drives procurement decisions. Exotic alloy demand rises in line with hydrogen pilot projects and super-critical CO2 power cycles, while modular printed-circuit designs gain traction where extreme pressures converge with space constraints. Competitive dynamics stay moderately fragmented: global incumbents rely on broad portfolios and aftermarket reach, whereas specialists target niches such as cryogenic LNG trains and 200-bar hydrogen units.

Global Heat Exchanger Market Trends and Insights

Surge in LNG Liquefaction Projects Boosting Demand for Cryogenic Exchangers

Global build-outs of mid-scale and large LNG trains require coil-wound and plate-fin units that perform below -150 °C while maintaining tight thermal approaches, accelerating procurement of high-grade stainless steels and aluminum alloys . Modular exchanger skids shorten construction schedules and curb cost overruns, benefiting fabricators integrating 3D-printed flow plates for weight reduction and enhanced turbulence. During 2025-2026, Gulf Coast and Qatari megaprojects are expected to anchor the heat exchanger market, with secondary demand arising from brownfield debottlenecking across Asia. Suppliers that certify to ASME Section VIII while offering 12-week delivery windows will secure framework contracts as EPC firms standardize equipment lists to de-risk timelines.

District-Cooling Expansion in GCC & Southeast Asia Driving Plate-Frame Sales

High-humidity metros such as Dubai, Riyadh, and Singapore continue to subsidize district-cooling systems to shave peak power loads, prompting utilities to specify gasketed plate-frame exchangers owing to compact footprints and easy capacity scaling . These deployments rely on stainless and titanium plates to mitigate brine corrosion, with district operators demanding 99% availability guarantees. OEMs that bundle condition-monitoring sensors will capture recurring service revenue as concession operators pivot toward performance-based maintenance models.

Nickel and Titanium Price Volatility Inflating Corrosion-Resistant Units

Class 1 nickel and aerospace-grade titanium prices have swung by up to 35% quarter-on-quarter since 2024, undermining order pipelines for hydrogen, marine, and offshore projects that cannot down-spec materials. Fabricators pass surcharges to EPC clients, but budget overruns trigger project deferrals, trimming short-term volumes in the heat exchanger market. Stainless-steel clad plates partly offset exposure, yet diffusion bonding of dissimilar metals complicates weld integrity certification.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen Pilot Plants Adopting Printed-Circuit Exchangers for 200-Bar Service

- Data-Centre Liquid-Cooling Uptake Accelerating Micro-Channel Adoption

- Bio-Process Fouling Issues Limiting Adoption in Biorefineries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shell-and-tube designs retained 35% of the heat exchanger market share in 2024, upholding their position as the default choice where pressures exceed 60 bar and fouling margins are high. Their standardized TEMA classifications simplify specification for refineries, LNG pretreatment trains, and sulfur recovery units, supporting repeat orders for tube bundles and gaskets that underpin aftermarket revenues. At the same time, air-cooled variants are climbing at a 6% CAGR as water-stressed utilities in India, Texas, and the Middle East prioritize zero-liquid-discharge strategies, driving units with forced-draft fans and low-noise gearboxes.

Across 2025-2030, printed-circuit and spiral-wound formats will nibble share in high-pressure hydrogen and super-critical CO2 cycles as designers seek compact footprints that conventional shells cannot match. Nevertheless, the heat exchanger market will continue to favor shell-and-tube for brownfield revamps because existing nozzle locations fit retrofit bundles, keeping life-cycle costs predictable. Suppliers that blend stainless-steel shells with copper-nickel tubes for marine scrubbers will tap IMO 2020 compliance budgets, adding a modest lift to volumes.

Stainless steel maintained 30% of the heat exchanger market size in 2024 because grades such as 316L balance corrosion resistance and cost efficiency. In food, beverage, and pharmaceutical lines, sanitary finishes and low-carbon content fulfill regulatory mandates without premium alloy surcharges. Exotic alloys-titanium, nickel, Incoloy, and Hastelloy-are moving at a 6.5% CAGR through 2030, capturing hydrogen, desalination, and offshore wind converter platforms where chloride-rich brines or hydrogen embrittlement preclude stainless options.

Polymers and composites grow from a small base as PTFE and graphite blocks outperform metals under highly acidic or fluoride-laden streams, notably in semiconductor wet-etch and lithium-ion battery recycling. Additive manufacturing unlocks dual-material lattices that place high-alloy material only where corrosion is severe, trimming cost and weight. Such innovations cement the heat exchanger industry's transition toward application-specific metallurgy rather than defaulting to legacy stainless catalogues.

The Heat Exchanger Market Report is Segmented by Type (Shell and Tube, Plate Frame, Air-Cooled, and Others), Material of Construction (Stainless Steel, Carbon Steel and Others), Flow Arrangement (Counter-Current, Parallel, Cross-Flow, and Hybrid/Multi-Pass), End-User Industry (Oil and Gas, Power Generation, Water and Waste-Water Treatment, and Others), and Geography (North America, Europe, Asia-Pacific, South America and Others).

Geography Analysis

Europe commanded 33% of 2024 global revenue, propelled by EU Eco-design directives that push boiler retrofits and district energy rollouts. Germany's integrated hydrogen strategy channels funding toward printed-circuit prototypes for electrolyzer plants, anchoring a high-value corner of the heat exchanger market. France accelerates SMR projects that require compact safety-class exchangers, while Nordic countries pioneer low-temperature district loops using titanium plate packs to exploit ambient seawater. OEMs maintaining EN13445 pressure-vessel accreditations and in-region spare-parts hubs capture share as uptime guarantees dominate tender scoring.

Asia-Pacific posts the fastest 5.9% CAGR to 2030, with China's petrochemical capacity additions, India's expanding power fleet, and ASEAN district-cooling concessions underpinning volume growth. Domestic manufacturers leverage cost-advantaged supply chains to win shell-and-tube orders, while Japanese and Korean firms focus on titanium and nickel PCHEs for ammonia-cracking pilots. Local EPCs value suppliers that offer modular skids shipped within 10 weeks, compelling global brands to localize fabrication or risk losing relevance amid aggressive pricing.

North America benefits from LNG export terminals along the Gulf Coast and data-center campus expansions across Virginia, Texas, and Quebec. The US Department of Energy's hydrogen hubs funnel grants into PCHE demonstrations that use diffusion-bonded nickel alloys. Canada's oil-sands operators retrofit air-fin units to curtail water withdrawals, creating a secondary pull on fan-assisted equipment. Across Latin America, mining concentrates and solar-thermal plants drive boutique orders, whereas the Middle East leans on desalination and petrochemical mega-complexes to sustain demand. Africa's momentum remains gradual but steady, tied to copper-belt smelting upgrades.

- Alfa Laval AB

- Kelvion Holding GmbH

- Danfoss A/S

- SPX Flow Inc.

- GEA Group AG

- Hisaka Works Ltd.

- Xylem Inc.

- Thermax Ltd.

- Mersen SA

- API Heat Transfer Inc.

- GE Vernova Inc.

- Barriquand Technologies Thermiques SAS

- Koch Heat Transfer Company LP

- SWEP International AB

- Heatric

- Kobelco Steel Ltd.

- Accessen Group

- Funke WarmeaustauscherGmbH

- Tranter Inc.

- HRS Heat Exchangers Ltd.

- Hamon Thermal Europe SA

- Graham Corporation

- United Heat Transfer Ltd.

- KRN Heat Exchanger & Refrigeration Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in LNG liquefaction projects boosting demand for cryogenic exchangers

- 4.2.2 District-cooling expansion in GCC & SE-Asia driving plate-frame sales

- 4.2.3 Hydrogen pilot plants adopting printed-circuit exchangers for 200-bar service

- 4.2.4 Mandatory EU industrial boiler upgrades spurring retrofit tube bundles

- 4.2.5 SMR (small modular reactor) roll-out needing compact safety-class exchangers

- 4.2.6 Data-centre liquid cooling uptake accelerating micro-channel adoption

- 4.3 Market Restraints

- 4.3.1 Nickel & titanium price volatility inflating corrosion-resistant units

- 4.3.2 Bio-process fouling issues limiting adoption in biorefineries

- 4.3.3 EPC demand for 12-week lead-times curbing engineered-to-order designs

- 4.3.4 Direct air-cooling in power plants cannibalising air-cooled exchangers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Shell and Tube

- 5.1.2 Plate and Frame (Gasketed Plate, Brazed Plate, Welded Plate)

- 5.1.3 Air-Cooled (Fin and Tube, Plate-Fin, Micro-Channel)

- 5.1.4 Regenerative (Rotary and Plate)

- 5.1.5 Printed Circuit

- 5.1.6 Others (Double-Pipe, Spiral, Coaxial)

- 5.2 By Material of Construction

- 5.2.1 Stainless Steel

- 5.2.2 Carbon Steel

- 5.2.3 Non-Ferrous (Copper, Aluminium)

- 5.2.4 Exotic Alloys (Titanium, Nickel, Hastelloy)

- 5.2.5 Polymers and Composites (PTFE, Graphite, Ceramic)

- 5.3 By Flow Arrangement

- 5.3.1 Counter-Current

- 5.3.2 Parallel

- 5.3.3 Cross-Flow

- 5.3.4 Hybrid/Multi-Pass

- 5.4 By End-Use Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Power Generation (incl. Nuclear)

- 5.4.4 Food and Beverage

- 5.4.5 Pulp and Paper

- 5.4.6 Water and Waste-water Treatment

- 5.4.7 Other Industries (Automotive and Transportation, Metallurgy, Mining, HVACR, Pharmaceutical and Biotechnology)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordic Countries

- 5.5.2.7 Russia

- 5.5.2.8 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Colombia

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Alfa Laval AB

- 6.4.2 Kelvion Holding GmbH

- 6.4.3 Danfoss A/S

- 6.4.4 SPX Flow Inc.

- 6.4.5 GEA Group AG

- 6.4.6 Hisaka Works Ltd.

- 6.4.7 Xylem Inc.

- 6.4.8 Thermax Ltd.

- 6.4.9 Mersen SA

- 6.4.10 API Heat Transfer Inc.

- 6.4.11 GE Vernova Inc.

- 6.4.12 Barriquand Technologies Thermiques SAS

- 6.4.13 Koch Heat Transfer Company LP

- 6.4.14 SWEP International AB

- 6.4.15 Heatric

- 6.4.16 Kobelco Steel Ltd.

- 6.4.17 Accessen Group

- 6.4.18 Funke WarmeaustauscherGmbH

- 6.4.19 Tranter Inc.

- 6.4.20 HRS Heat Exchangers Ltd.

- 6.4.21 Hamon Thermal Europe SA

- 6.4.22 Graham Corporation

- 6.4.23 United Heat Transfer Ltd.

- 6.4.24 KRN Heat Exchanger & Refrigeration Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment