|

시장보고서

상품코드

1851445

목재 코팅 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Wood Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

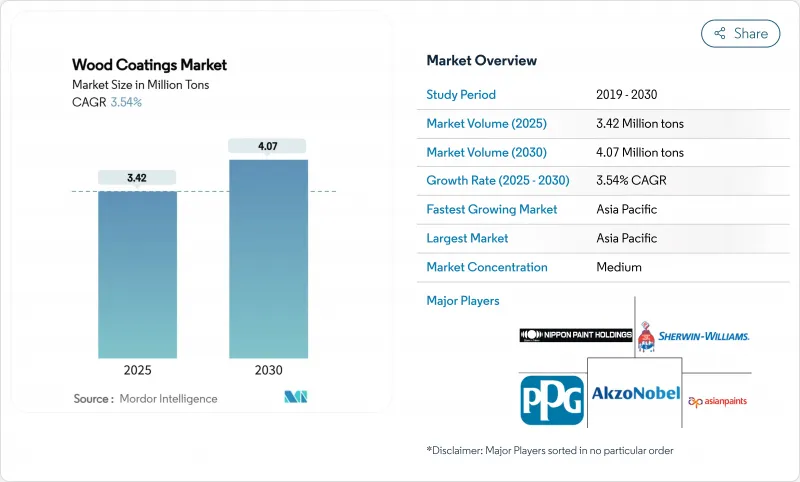

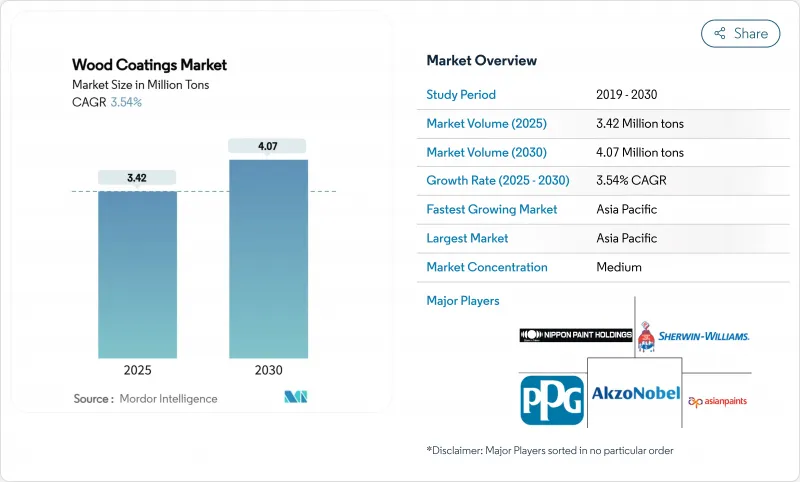

세계의 목재 코팅 시장 규모는 2025년 342만 톤으로 추계되며 예측기간 중(2025-2030년) CAGR은 3.54%를 나타낼 전망이며, 2030년에는 407만 톤에 달할 것으로 예측됩니다.

이 꾸준한 확대는 아시아태평양의 제조거점, 수성 화학물질로의 전환 가속화, 세계 가구 부문의 지속적인 수요에 의해 지원되고 있습니다. 폴리우레탄은 그 내구성에 의해 주요 수지 플랫폼인 것을 계속하고 있는 한편, 환경 규제에 의해 저 VOC 대체품의 채용이 급속히 진행되고 있습니다. 제조업체는 또한 배합의 유연성과 현지 조달에 투자함으로써 원료 가격의 변동(특히 이산화티탄)을 극복하고 있습니다. 최고 공급업체 간의 통합은 바이오 첨가제의 중견층 기술 혁신 증가와 함께 경쟁을 강화하는 동시에 중소기업이 준수해야 하는 성능 기준을 높입니다.

세계의 목재 코팅 시장 동향과 통찰

아시아태평양의 모듈식 가구와 RTA 가구의 붐

급속한 도시화와 아파트 면적의 축소로 중국, 인도, 인도네시아에서는 모듈식 가구와 조립식 가구의 급증에 박차를 가하고 있습니다. 이러한 대량 생산 가구는 긁힘에 강하고 경화가 빠른 마감재를 필요로 하고, 배합자는 MDF와 같은 인공 기재로의 침투를 최적화할 필요가 있습니다. 인도네시아 공장에서만 2024년 10월까지 100만 4,000톤의 페인트가 생산되었으며, 목재 코팅은 그 7%를 차지하고 있습니다. 속건성 폴리우레탄 아크릴 하이브리드를 지원하는 공급업체는 신규 계약을 획득했으며, 아시아태평양이 목재 코팅 시장에서 중심적인 역할을 하고 있습니다.

EU 주도의 저 VOC 수성 처방으로의 이동

유럽연합(EU)의 VOC 규제 강화로 용제계로부터의 이행이 가속화되고 있습니다. 최근 수성 폴리우레탄 디스퍼전의 내구성은 용제계에 필적하게 되어 역사적인 성능 차이는 해소되었습니다. 이러한 적합 제품을 북미와 아시아에 수출하는 유럽 포뮬레이터는 단일 제조법으로 세계 생산 라인을 가동함으로써 비용 시너지를 실현하고 다른 지역이 유사한 규칙을 목표로 하는 선행자 이익을 얻고 있습니다. 이러한 협력은 목재 코팅 시장의 주요 구조적 촉진요인이며 배출량을 더욱 줄이는 바이오 코바인더에 초점을 맞춘 연구 개발을 자극하고 있습니다.

수지 및 용매의 가격 변동

EU에 유입되는 중국제 산화티탄에 대한 11.4%-32.3%의 반덤핑 관세(2025년 1월 발효)에 의해 원재료 비용은 급상승하고 있습니다. 목재 코팅 시장의 소규모 제조업체는 마진 압축에 직면하고 일부 제조업체는 안료의 양을 줄이거나 대체 익스텐더를 사용하여 재제조를 수행하는 반면 다국적 기업은 장기 공급 계약을 통해 노출을 헤지하고 있습니다.

부문 분석

2024년 목재 코팅 시장 점유율은 폴리우레탄이 60%를 차지하고 2030년까지 연평균 복합 성장률(CAGR)은 3.79%가 될 것으로 예측됩니다. 폴리우레탄의 가교 밀도는 가구 수출업체가 엄격한 내구성 시험을 완료하기 위해 요구하는 내화학성을 실현합니다. 폴리우레탄은 2024년 기준에서 이미 수지의 목재 코팅 시장 규모의 최대 부분을 차지하고 있으며, 경도를 희생하지 않고 화석 함량을 줄이는 바이오폴리올 등급 도입으로 리드를 넓히고 있습니다. 아크릴 수지는 UV 안정성에 의해 여전히 외장용 수지의 주력이며, 니트로셀룰로오스는 안전 규제가 느슨한 지역에서는 여전히 클래식 가구에 사용되고 있습니다. Solus를 지원하는 바이오 시스템은 보다 안전한 드롭인 옵션으로 구매자를 유도합니다. 폴리에스테르는 피아노나 부티크 캐비닛용의 고광택 마무리에 틈새 시장을 차지하고 있어 그 특수한 위치를 이야기하고 있습니다. 신흥 리그닌계 바인더는 지속가능성 주도의 시험적 프로젝트를 포착하는 태세에 있지만 현재 총 수요의 1% 미만에 그치고 있습니다. 그러므로 폴리우레탄의 확고한 지위는 목재 코팅 시장에 진입하는 모든 주요 제조업체의 경쟁 배합 로드맵을 지원합니다.

습기 경화형 지방족 폴리우레탄의 진보에 의해 VOC 함유량은 50g/L 미만이 되어, 오픈 타임을 희생하지 않고 기존 사양을 웃도게 되었습니다. 베트남과 폴란드의 선도적인 OEM 가구 제조업체는 플랫 라인 스프레이 및 진공 코팅기로 이러한 시스템을 검증했으며 폴리 우레탄이 앞으로도 프리미엄 성능 층을 계속 형성할 것임을 보여줍니다. </p><h3><u>Geography Analysis</u></h3><p> 아시아태평양은 2024년 57%의 점유율로 목재 코팅 시장을 독점하여 가장 빠른 지역 CAGR 3.9%를 기록했습니다. 중국은 국내 소비와 수출 지향 가구 클러스터에 지지를 받고 여전히 기축인 반면, 인도에서는 중산계급이 상승하고 현지 프리미엄 부문을 견인하고 있습니다. 아시아태평양은 각국 정부가 배출규제를 강화함에 따라 물을 매체로 하는 제품의 채용이 가속화되고 있으며, 규모 주도의 기술 혁신에 있어 매우 중요한 무대가 되고 있습니다.

북미는 목재 코팅 시장에서 큰 점유율을 차지하며 기술 업그레이드로 이끌고 있습니다. DIY 참여와 고급 장식품 형식이 구매 패턴을 형성하고 대형 소매점의 개인 라벨 프로그램이 제3자의 지속가능성 인증을 요구하게 되었습니다. HIRI는 2025년 주택 설비 투자가 3.9% 회복될 것으로 예측하고 단기 사이클 수요 회복력을 강화하고 있습니다. 또한 기후 변화로 인해 사이딩 기초 전체의 습도 변화에 대응하는 유연한 막을 가진 외벽용 스테인에 대한 수요가 높아지고 있으며, 이 지역의 목재 코팅 시장의 SKU 수는 더욱 다양해지고 있습니다.

유럽에서는 엄격한 규제와 건축용 목재 채용이 결합되어 있습니다. EU의 Green Deal 장려책은 저탄소 건축자재를 우대하고 집합 주택의 CLT 부재를 보호하는 고성능 코팅 수요를 촉진하고 있습니다. 포름알데히드와 VOC 역치의 시행은 2022년 이후 지역 가구 마감 라인의 절반 가까이 수성 또는 UV 경화형 화학물질로 전환되었으며, 다른 지역보다 빨리 솔벤트 유형 베이스가 압축되었습니다. 이러한 역학으로 유럽은 규제의 벤치마크인 동시에 개발도상 시장을 위한 배합기술의 수출거점이기도 합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아태평양의 모듈식 가구와 RTA 가구의 붐

- EU 주도로 저 VOC 수성 배합으로 전환

- 북미에서 프리미엄 인테리어 데코의 동향

- DIY 홈센터 확대

- 유럽의 목조 다세대 주택

- 시장 성장 억제요인

- 수지와 용제의 가격 변동

- 포름알데히드 및 VOC 규제 강화

- 가구에서 라미네이트와 플라스틱으로 대체

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 수지 유형별

- 폴리우레탄

- 아크릴

- 니트로셀룰로오스

- 폴리에스테르

- 기타

- 기술별

- 수계

- 용제계

- UV 경화형

- 분체 코팅

- 용도별

- 가구 및 비품

- 문 및 창

- 캐비닛

- 기타 용도(바닥, 데크, 성형품 포함)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Akzo Nobel NV

- Asian Paints

- Axalta Coating Systems

- Benjamin Moore & Co.

- Ceramic Industrial Coatings

- Hempel A/S

- Jotun

- Kansai Nerolac Paints Limited

- KAPCI Coating

- MAS Paints

- National Paints Factories Co. Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- Ritver

- RPM International Inc.

- Teknos Group

- The Sherwin-Williams Company

제7장 시장 기회와 장래의 전망

JHS 25.11.13The Wood Coatings Market size is estimated at 3.42 Million tons in 2025, and is expected to reach 4.07 Million tons by 2030, at a CAGR of 3.54% during the forecast period (2025-2030).

This steady expansion is supported by the Asia-Pacific manufacturing base, accelerating shifts toward water-borne chemistries, and sustained demand from the global furniture sector. Polyurethane's durability keeps it the leading resin platform, while environmental regulations are fast-tracking adoption of low-VOC alternatives. Manufacturers are also navigating raw-material price swings-especially titanium dioxide-by investing in formulation flexibility and localized sourcing. Consolidation among top suppliers, paired with growing mid-tier innovation in bio-based additives, is strengthening competition while raising the performance baseline that smaller firms must match.

Global Wood Coatings Market Trends and Insights

Modular & RTA Furniture Boom in Asia-Pacific

Rapid urbanization and shrinking apartment sizes have spurred a surge in modular and ready-to-assemble furniture across China, India, and Indonesia. These high-volume furniture lines require scratch-resistant finishes that cure quickly, pushing formulators to optimize penetration on engineered substrates such as MDF. Indonesian factories alone produced 1.004 million tons of coatings by October 2024, with wood coatings representing 7%, highlighting the scale of regional demand. Suppliers responding with fast-drying polyurethane-acrylic hybrids are capturing new contracts, reinforcing Asia-Pacific's central role in the wood coatings market.

EU-Led Shift to Low-VOC Waterborne Formulations

The European Union's tightening VOC caps have accelerated migration away from solvent-borne systems. Recent aqueous polyurethane dispersions now match solvent-borne durability, closing the historical performance gap. European formulators exporting these compliant chemistries to North America and Asia achieve cost synergies by running global production lines on a single recipe, gaining first-mover advantages as other regions move toward similar rules. This alignment is a leading structural driver for the wood coatings market, stimulating R&D focused on bio-based co-binders that further cut emissions.

Resin & Solvent Price Volatility

Anti-dumping duties of 11.4%-32.3% on Chinese titanium dioxide entering the EU, effective January 2025, have pushed raw-material costs sharply higher. Smaller manufacturers in the wood coatings market face margin compression, leading some to reformulate with lower pigment volumes or alternative extenders, while multinationals hedge exposure through long-term supply contracts.

Other drivers and restraints analyzed in the detailed report include:

- Premium Interior Decor Trend in North America

- Timber-Rich Multi-Family Housing in Europe

- Stricter Formaldehyde / VOC Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane dominated the wood coatings market with a 60% share in 2024 and is set to grow at 3.79% CAGR through 2030. Its cross-linking density delivers chemical resistance that furniture exporters demand to meet stringent durability tests. In 2024 polyurethane already represented the largest slice of wood coatings market size for resins and continues widening its lead with introductions of bio-polyol grades that cut fossil content without sacrificing hardness. Acrylic resins remain the exterior workhorse thanks to UV stability, while nitrocellulose still services classic furniture in regions with lenient safety codes. Solus-enabled biobased systems are nudging buyers toward safer drop-in options. Polyester's niche in high-build gloss finishes for pianos and boutique cabinetry signals its specialty positioning. Emerging lignin-based binders are poised to capture sustainability-driven pilot projects but remain under 1% of total demand today. Polyurethane's entrenched position therefore anchors competitive formulation roadmaps across every major producer participating in the wood coatings market.

Advancements in moisture-curing aliphatic polyurethanes now offer <50 g/L VOC content, surpassing legacy specifications without sacrificing open time. Major OEM furniture lines in Vietnam and Poland have validated these systems for flat-line spray and vacuum coaters, demonstrating that polyurethane will continue shaping premium performance tiers. As environmental scrutiny tightens, suppliers integrating recycled PET polyols further extend the resin's lifecycle credentials, keeping this chemistry at the center of investment decisions across the global wood coatings industry.

The Wood Coatings Market Report Segments the Industry by Resin Type (Polyurethane, Acrylic, Nitrocellulose, and More), Technology (Water-Borne, Solvent-Borne, UV-Cured, and More), Application (Furniture and Fixtures, Doors and Windows, Cabinets, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific dominated the wood coatings market with 57% share in 2024 and posted the quickest regional CAGR at 3.9%. China remains the cornerstone, supported by domestic consumption and export-oriented furniture clusters, while India's rising middle class powers local premium segments. Water-borne adoption is accelerating as regional governments tighten emission ceilings, making Asia-Pacific the pivotal arena for scale-driven innovation.

North America holds significant share in the wood coatings market and leads in technology upgrades. DIY participation and premium decor formats shape buying patterns, and big-box retailers' private-label programs now demand third-party sustainability certifications. HIRI forecasts a 3.9% rebound in 2025 home-improvement expenditures, reinforcing short-cycle demand resilience. Climatic events have also heightened demand for exterior stains with flexible membranes that tolerate moisture swings across siding substrates, further diversifying SKU count in the region's wood coatings market.

Europe combines stringent regulations with architectural timber adoption. The EU's Green Deal incentives favor low-carbon building materials, propelling demand for high-performance coatings that shield CLT elements in multi-family structures. Enforcement of formaldehyde and VOC thresholds has shifted nearly half of regional furniture finishing lines to water-borne or UV-cure chemistries since 2022, compressing the solvent-borne base faster than in any other geography. These dynamics position Europe as both a regulatory benchmark and an export hub for formulation technology destined for developing markets.

- Akzo Nobel N.V.

- Asian Paints

- Axalta Coating Systems

- Benjamin Moore & Co.

- Ceramic Industrial Coatings

- Hempel A/S

- Jotun

- Kansai Nerolac Paints Limited

- KAPCI Coating

- MAS Paints

- National Paints Factories Co. Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- Ritver

- RPM International Inc.

- Teknos Group

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Modular and RTA Furniture Boom in Asia-Pacific

- 4.2.2 EU-Led Shift to Low-VOC Waterborne Formulations

- 4.2.3 Premium Interior Decor Trend in North America

- 4.2.4 Expansion of DIY Home-Improvement Retail

- 4.2.5 Timber-Rich Multi-Family Housing in Europe

- 4.3 Market Restraints

- 4.3.1 Resin and Solvent Price Volatility

- 4.3.2 Stricter Formaldehyde / VOC Caps

- 4.3.3 Substitution by Laminates and Plastics in Furniture

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Resin Type

- 5.1.1 Polyurethane

- 5.1.2 Acrylic

- 5.1.3 Nitrocellulose

- 5.1.4 Polyester

- 5.1.5 Others

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 UV-Cured

- 5.2.4 Powder Coatings

- 5.3 By Application

- 5.3.1 Furniture and Fixtures

- 5.3.2 Doors and Windows

- 5.3.3 Cabinets

- 5.3.4 Other Applications (including Floors, Decks, and Molding Products)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Asian Paints

- 6.4.3 Axalta Coating Systems

- 6.4.4 Benjamin Moore & Co.

- 6.4.5 Ceramic Industrial Coatings

- 6.4.6 Hempel A/S

- 6.4.7 Jotun

- 6.4.8 Kansai Nerolac Paints Limited

- 6.4.9 KAPCI Coating

- 6.4.10 MAS Paints

- 6.4.11 National Paints Factories Co. Ltd.

- 6.4.12 Nippon Paint Holdings Co., Ltd.

- 6.4.13 PPG Industries Inc.

- 6.4.14 Ritver

- 6.4.15 RPM International Inc.

- 6.4.16 Teknos Group

- 6.4.17 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Demand for UV-cured Coatings