|

시장보고서

상품코드

1851455

합성 다이아몬드 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Synthetic Diamond - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

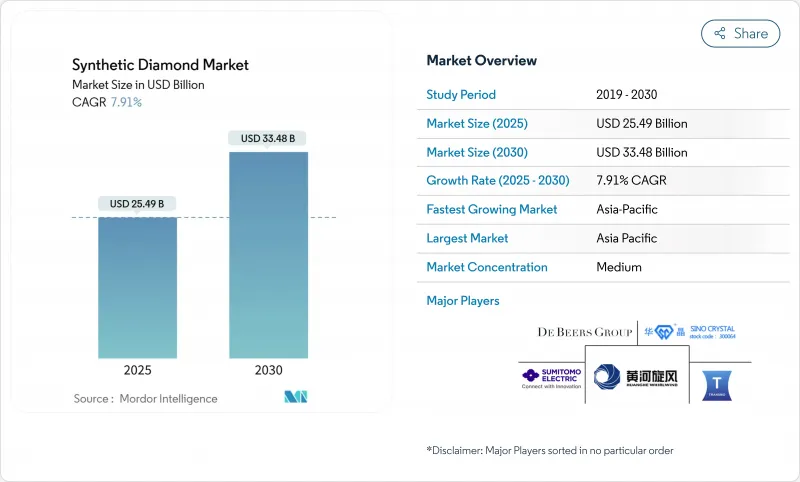

세계의 합성 다이아몬드 시장 규모는 2025년 254억 9,000만 달러로, 2030년에는 334억 8,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 7.91%로 확대될 것으로 보입니다.

통신, 전기자동차, 항공우주, 고정밀 제조업 수요 증가가 수익원을 가속화하는 한편, 지속가능성의 지속적인 의무화를 통해 고객은 채굴석에서 인공 대체품으로 전환하고 있습니다. 아시아태평양은 이미 대부분의 다이아몬드 웨이퍼와 초연마 공구를 공급하고 있으며, 국가의 까다로운 우대 조치와 전자 기기 수출의 급증의 혜택을 받고 있습니다. 기술에 중점을 둔 진입기업이 디바이스급 순도를 달성할 수 있는 화학기상성장법(CVD)의 생산능력을 확대하고 있으며 기존의 고압고온법(HPHT) 모델에 대한 직접적인 과제가 되어 경쟁이 격화되고 있습니다. 한편, 걸프 협력 회의의 고급 브랜드는 환경 의식이 높은 소비자를 만족시키기 위해서 팬시 칼라의 랩 그로운 스톤을 활용해, 기존 브라이들 쥬얼리를 넘어 대응 가능한 범위 넓히고 있습니다. 특히 소매가격 시정이 최종사용자의 재판매가치 인식을 훼손하는 가운데 규제 불확실성과 불균일한 인증기준이 주요 역풍이 되고 있지만, 성능 주도의 하이테크 분야는 계속해서 금리를 확보하고 있습니다.

세계 합성 다이아몬드 시장 동향과 통찰

아시아에서 5G/6G RF 필터용 CVD 다이아몬드 채용 증가

CVD 단결정 웨이퍼는 22W/cm*K로 방열하기 때문에 고밀도의 5G나 미래의 6G 네트워크를 지지하는 고주파 필터의 소형화와 신뢰성의 향상이 가능하게 됩니다. 특히 중국, 한국, 대만에서는 수직 통합형 OEM이 대규모 다입력 다출력(mMIMO) 안테나 내에 다이아몬드 다이 부착층을 내장하고 있습니다. 현지 장비 공급업체에 따르면 전력 소비가 감소하고 기지국 수명이 연장됨에 따라 운영자는 총 소유 비용을 측정할 수 있을 만큼 향상시킬 수 있었다고 보고했습니다.

EV 배터리 기가팩토리로 산업용 다이아몬드 수요 급증

다결정 다이아몬드 코팅이 적용된 정밀 연삭 휠은 실리콘이 풍부한 애노드 절단, 세퍼레이터 필름의 레이저 전사, 알루미늄 케이싱의 표면 처리에 필수적입니다. 미국과 유럽의 기가비트 배터리 공장은 현재 고속 가공 스테이션의 70% 이상에 다이아몬드 공구를 사용하고 있으며 차량 플랫폼당 단위 소비량이 증가하고 있습니다. 다이아몬드 주조의 웨이퍼 기반 인버터는 기존의 설계보다 6배 소형이면서 고성능이며, 열적 및 전기적 특성이 드라이브 트레인의 효율을 어떻게 향상시키는지를 입증하고 있습니다.

규제 및 인증 문제

인도의 중앙 소비자 보호국(Central Consumer Protection Authority)은 소매업체에게 인보이스 및 마케팅 자료에 산지 및 성장 방법을 명시할 것을 의무화하고 있습니다. 미국에서는 보석품 검사위원회(Jewelers Vigilance Committee)의 지침도 마찬가지로 감사 의무를 강화하고 있으며, 기업은 분광 검사 및 자동 스크리닝 장비에 대한 투자를 촉구하고 있습니다. 지역에 따라 규칙이 다르기 때문에 국경을 넘은 거래가 복잡해지고 판매자에게는 법적인 리스크가 발생합니다.

부문 분석

원석은 2024년에 합성 다이아몬드 시장 점유율의 66%를 차지했으며, 이는 건설, 석유 및 가스 굴삭, 정밀 절삭 공구에 많이 채용되었기 때문에 이들은 모두 비교할 수 없는 경도와 열전도성을 활용하고 있습니다. 미국 지질조사소는 국내 생산량 1억 6,000만캐럿, 5,300만 달러를 기록해 전년 대비 5% 증가했습니다.

연마석은 톤수가 적지만 CAGR 9.84%로 예측되는 가장 급성장하고 있는 카테고리입니다. 소비자에게 널리 받아들여져 디자인의 유연성이 높아지고, 플라즈마에 의한 후처리가 진보해 채도가 높아짐으로써, 중견의 보석품 체인으로 취급량이 증가하고 있습니다. 미국 보석학회(Gemological Institute of America)에 따르면 CVD의 샘플 제출량이 HPHT의 샘플 제출량을 상회하고, 팬시 컬러와 3캐럿 이상의 돌이 전년 대비 크게 증가하고 있습니다. 예측 기간 동안 도매 가격이 안정되더라도 광택 마감 보석은 옴니 채널 소매 선반 공간을 늘릴 것으로 예측됩니다.

지역 분석

아시아태평양은 2024년 세계 매출의 56%를 차지하며 2030년까지 연평균 복합 성장률(CAGR) 8.35%에서 가장 빠른 성장을 이어갑니다. 허난성, 산동성, 구자라트의 생산 클러스터는 시드 합성에서 보석 완제품에 이르기까지 수직 통합 사업을 전개하고 있습니다. 중국은 실험용 반응기에서 우위를 차지하기 때문에 비용면에서 유리하며 인도는 다이아몬드 씨앗에 대한 5%의 수입 관세를 철폐했기 때문에 해외 합작투자를 유치하고 있습니다.

고성능 용도, 특히 양자 감지 및 와이드 밴드갭 파워 일렉트로닉스에서는 북미가 여전히 매우 중요합니다. Adamas One Corp.의 사우스 캐롤라이나 공장은 현재 12개의 반응기로 월산 3,000캐럿 원석을 생산하고 있으며 IP로 보호되는 성장 프로토콜을 중시하고 항공우주와 의료 계약을 획득하고 있습니다.

유럽은 안정적이지만 혁신 지향적인 자세를 유지하고 있습니다. 독일 공구 제조업체와 프랑스 포토닉스 신흥 기업은 자동차의 경량화 요구에 부응하기 위해 다이아몬드 인서트를 통합하고 있습니다. 영국의 학술 생태계, 특히 국립 양자 컴퓨팅 센터는 안전한 통신을 위한 질소 공공(NV) 결함 공학을 추진하고 있습니다. 유럽 이외의 중동에서는 두바이가 무역과 생산의 허브로 자리잡고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 5G 및 6G용 RF 필터에 CVD 다이아몬드의 채용이 증가(아시아)

- EV 배터리 및 기가팩토리에 의한 공업용 다이아몬드 수요 급증

- 초연삭재 수요 증가

- 항공우주용 복합재의 자동 CNC 가공에서 초연삭재 이용

- GCC에서 럭셔리 브랜드의 지속가능성이 랩 그로운 및 팬시 컬러 스톤으로 전환

- 시장 성장 억제요인

- 규제와 인증의 과제

- 복잡한 제조 공정

- LGD 가격 하락 대 천연 다이아몬드를 둘러싼 소비자의 혼란

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액 및 수량)

- 제품 유형별

- 광택

- 쥬얼리

- 일렉트로닉스

- 헬스케어

- 기타 연마 유형

- 러프

- 건설

- 광업

- 석유 및 가스

- 기타 러프 유형

- 광택

- 제조 공정별

- 고압 고온(HPHT)

- 화학 증착(CVD)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ADAMAS ONE

- Applied Diamond Inc.

- Coherent Corp.

- De Beers Group(Element Six)

- Diamond Foundry

- Henan Huanghe Whirlwind CO.,Ltd.

- Heyaru Group

- ILJIN DIAMOND CO., LTD.

- John Crane(Advanced Diamond Technologies, Inc.)

- NEW DIAMOND TECHNOLOGY LLC

- PURE LAB DIAMONDS

- Sandvik AB

- Sumitomo Electric Industries, Ltd.

- Swarovski AG

- Tecdia, Inc.

- Washington Diamond

- Zhengzhou Sino-Crystal Diamond Co.,Ltd.

- Zhuhai Zhong Na Diamond Co.,Ltd Inc.

제7장 시장 기회와 장래의 전망

JHS 25.11.13The Synthetic Diamond Market size is estimated at USD 25.49 billion in 2025, and is expected to reach USD 33.48 billion by 2030, at a CAGR of 7.91% during the forecast period (2025-2030).

Escalating demand from telecommunications, electric vehicles, aerospace, and high-precision manufacturing is accelerating revenue streams, while persistent sustainability mandates are steering customers away from mined stones toward engineered alternatives. Asia Pacific, already supplying most diamond wafers and super-abrasive tools, benefits from generous state incentives and surging electronics exports. Competition is intensifying because technology-focused entrants are scaling Chemical Vapor Deposition (CVD) capacity that can achieve device-grade purity, posing a direct challenge to the incumbent High Pressure High Temperature (HPHT) model. Meanwhile, luxury brands in the Gulf Cooperation Council are leveraging fancy-color lab-grown stones to satisfy environmentally conscious consumers, widening the addressable base beyond traditional bridal jewelry. Regulatory uncertainty and uneven certification standards remain the chief headwinds, especially as retail price corrections undermine perceived resale value among end users, but the performance-driven high-tech arena continues to shield margins.

Global Synthetic Diamond Market Trends and Insights

Rising Adoption of CVD Diamonds for 5G/6G RF Filters in Asia

CVD single-crystal wafers dissipate heat at 22 W/cm*K, enabling smaller and more reliable radio-frequency filters that underpin dense 5G and future 6G networks. Large-area substrate work sponsored by DARPA is migrating into commercial foundries, particularly in China, South Korea, and Taiwan, where vertically integrated OEMs are embedding diamond die-attach layers inside massive multiple-input multiple-output (mMIMO) antennas. Local equipment vendors report lower power consumption and longer base-station lifetimes, giving operators measurable total-cost-of-ownership gains.

Industrial Diamond Demand Surge from EV Battery Gigafactories

Precision grinding wheels with polycrystalline diamond coatings are indispensable for cutting silicon-rich anodes, laser-scribing separator films, and surfacing aluminum casings. Giga-scale battery plants in the United States and Europe now specify diamond tooling in over 70% of high-speed machining stations, elevating unit consumption per vehicle platform. Diamond Foundry's wafer-based inverter, six times smaller than the incumbent design yet more powerful, underscores how thermal and electrical properties improve drivetrain efficiency.

Regulatory and Certification Challenges

The Central Consumer Protection Authority in India requires retailers to specify production origin and growth method on invoices and marketing collateral, adding compliance costs and compelling supply-chain transparency. In the United States, Jewelers Vigilance Committee guidelines similarly tighten audit obligations, prompting firms to invest in spectroscopy and automated screening equipment. Divergent rules by region complicate cross-border trading and create legal exposure for distributors.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Super-Abrasives

- Luxury Brands' Sustainability Pivot to Lab-Grown Fancy-Color Stones in the GCC

- Consumer Confusion Over Lab-Grown Diamond Price Depreciation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rough stones captured 66% of the synthetic diamond market share in 2024, owing to heavy uptake in construction, oil-and-gas drilling, and precision cutting tools, all of which leverage unmatched hardness and thermal conductivity. The U.S. Geological Survey recorded domestic output of 160 million carats valued at USD 53 million, a 5% rise on the prior year.

Polished stones, though smaller in tonnage, are the fastest-expanding category at a projected 9.84% CAGR. Wider consumer acceptance, heightened design flexibility, and advances in plasma post-processing that enhance color saturation are boosting volumes across mid-tier jewelry chains. The Gemological Institute of America notes that CVD submissions now exceed HPHT samples, with fancy colors and 3-carat-plus stones up sharply year over year. Over the forecast horizon, polished gems are expected to secure incremental shelf space in omnichannel retail, even as wholesale prices stabilize.

The Synthetic Diamond Market Report Segments the Industry by Product Type (Polished and Rough), Manufacturing Process (High Pressure, High Temperature (HPHT) and Chemical Vapor Deposition (CVD)), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific anchored 56% of global revenue in 2024 and continues to post the fastest regional growth at an 8.35% CAGR through 2030. Production clusters in Henan, Shandong, and Gujarat host vertically integrated operations that span seed synthesis to finished jewelry. China's dominance in lab reactors provides cost advantages, while India's abolition of a 5% import duty on diamond seeds attracts overseas joint ventures.

North America remains pivotal for high-performance applications, particularly in quantum sensing and wide-band-gap power electronics. Adamas One Corp's South Carolina facility, which currently runs 12 reactors producing 3,000 rough carats monthly, emphasizes IP-protected growth protocols to secure aerospace and medical contracts.

Europe maintains a stable but innovation-oriented stance. German toolmakers and French photonics startups incorporate diamond inserts to meet automotive lightweighting mandates. The United Kingdom's academic ecosystem, notably the National Quantum Computing Centre, advances Nitrogen-Vacancy (NV) defect engineering for secure communications. Outside Europe, the Middle East positions Dubai as a trading and production hub.

- ADAMAS ONE

- Applied Diamond Inc.

- Coherent Corp.

- De Beers Group (Element Six)

- Diamond Foundry

- Henan Huanghe Whirlwind CO.,Ltd.

- Heyaru Group

- ILJIN DIAMOND CO., LTD.

- John Crane (Advanced Diamond Technologies, Inc.)

- NEW DIAMOND TECHNOLOGY LLC

- PURE LAB DIAMONDS

- Sandvik AB

- Sumitomo Electric Industries, Ltd.

- Swarovski AG

- Tecdia, Inc.

- Washington Diamond

- Zhengzhou Sino-Crystal Diamond Co.,Ltd.

- Zhuhai Zhong Na Diamond Co.,Ltd Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of CVD Diamonds for 5G/6G RF Filters Asia

- 4.2.2 Industrial Diamond Demand Surge from EV Battery Gigafactories

- 4.2.3 Growing Demand for Super Abrasives

- 4.2.4 Super-abrasive Usage in Automated CNC Machining for Aerospace Composites

- 4.2.5 Luxury Brands' Sustainability Pivot to Lab-Grown Fancy-Color Stones in the GCC

- 4.3 Market Restraints

- 4.3.1 Regulatory and Certification Challenges

- 4.3.2 Complex Manufacturing Process

- 4.3.3 Consumer Confusion Over LGD Price Depreciation vs. Natural Diamonds

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 Polished

- 5.1.1.1 Jewelry

- 5.1.1.2 Electronics

- 5.1.1.3 Healthcare

- 5.1.1.4 Other Polished Types

- 5.1.2 Rough

- 5.1.2.1 Construction

- 5.1.2.2 Mining

- 5.1.2.3 Oil and Gas

- 5.1.2.4 Other Rough Types

- 5.1.1 Polished

- 5.2 By Manufacturing Process

- 5.2.1 High Pressure High Temperature (HPHT)

- 5.2.2 Chemical Vapor Deposition (CVD)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordics

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ADAMAS ONE

- 6.4.2 Applied Diamond Inc.

- 6.4.3 Coherent Corp.

- 6.4.4 De Beers Group (Element Six)

- 6.4.5 Diamond Foundry

- 6.4.6 Henan Huanghe Whirlwind CO.,Ltd.

- 6.4.7 Heyaru Group

- 6.4.8 ILJIN DIAMOND CO., LTD.

- 6.4.9 John Crane (Advanced Diamond Technologies, Inc.)

- 6.4.10 NEW DIAMOND TECHNOLOGY LLC

- 6.4.11 PURE LAB DIAMONDS

- 6.4.12 Sandvik AB

- 6.4.13 Sumitomo Electric Industries, Ltd.

- 6.4.14 Swarovski AG

- 6.4.15 Tecdia, Inc.

- 6.4.16 Washington Diamond

- 6.4.17 Zhengzhou Sino-Crystal Diamond Co.,Ltd.

- 6.4.18 Zhuhai Zhong Na Diamond Co.,Ltd Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Applications in Orthopedic Medical Devices