|

시장보고서

상품코드

1851457

자동차용 타이어 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Tires - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

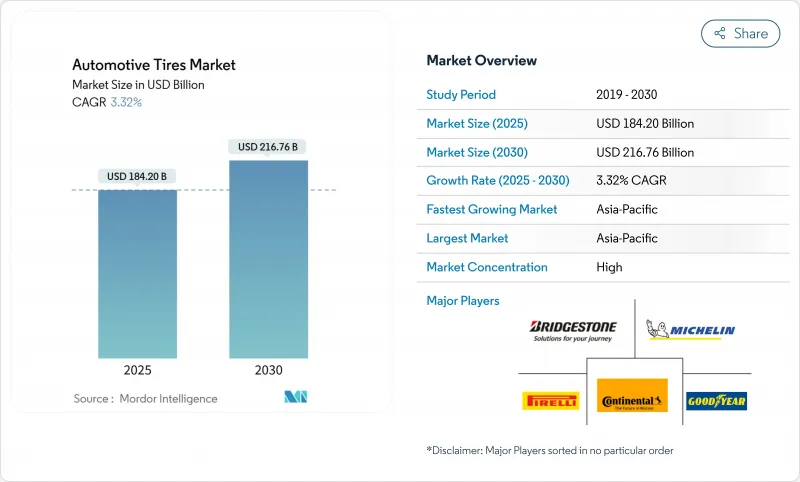

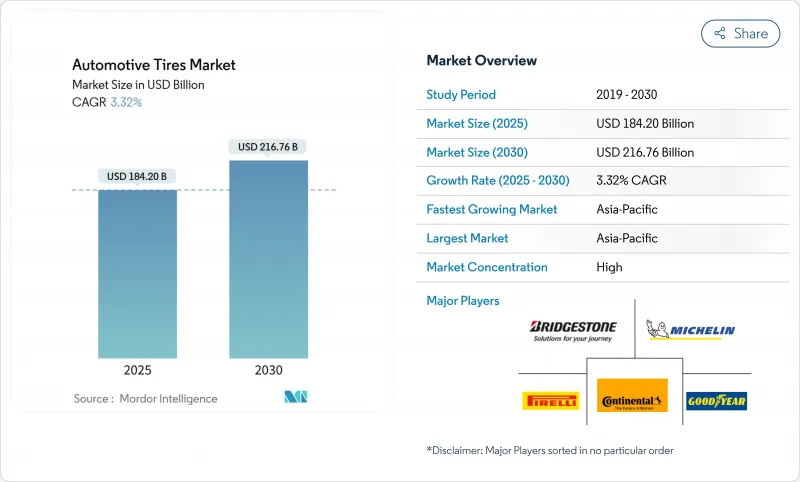

세계의 자동차용 타이어 시장은 2025년에 1,842억 달러, 2030년에는 2,167억 6,000만 달러에 이르고, CAGR 3.32%로 확대될 것으로 예측됩니다.

전기차의 보급이 초저소음 및 저회전 저항제품 수요를 높여 지속가능성 정책이 국내 합성고무에 대한 투자를 촉구하고 소비자의 대경림 지향이 평균 판매가격을 인상하고 있습니다. 북미와 유럽이 연결성과 프리미엄 성능을 중심으로 혁신을 진행하는 한편, 아시아 제조업의 두께와 자동차 보유 대수 증가가 지리적 축을 유지합니다. 동남아시아의 고무 잎병과 유럽의 카본블랙 물류로 인한 공급 측면의 압력은 공급망의 탄력성의 필요성을 강조합니다. 그러나 자동차용 타이어 시장 전체는 플릿이 근대화되고 데이터가 풍부한 스마트 타이어 계약이 새로운 수익원을 해방함에 따라 확대를 계속하고 있습니다.

세계 자동차 타이어 시장 동향과 통찰

전동화로 인한 초저소음 타이어 수요

전동 드라이브 트레인은 엔진의 마스킹 노이즈를 제거하고 타이어와 노면의 상호 작용을 음향의 최전선에 위치시킵니다. 유럽 연합(EU)의 차량 외부 소음 규제의 엄격화는 이러한 추세를 더욱 강화하고, 자동차 타이어 시장의 주류층도 컴플라이언스와 편안함을 위해 유사한 기술을 요구하고 있습니다. 공급업체는 성능과 규제를 충족하고, 갈망하는 OE 적합성을 보장하며, 원재료 비용 상승에도 불구하고 가격 규율을 유지할 수 있습니다.

중국에서 낮은 RR 타이어 채용의 의무화

Phase-6의 연비 규제에서는 소비량의 15% 개선이 의무화되어 있어 구름 저항에 스폿이 맞추어져 있습니다. 국내 및 세계 브랜드는 R&D 사이클을 18개월로 단축하고 연비를 8% 향상시킬 수 있는 실리카 리치 컴파운드를 제공합니다. 중국의 승인으로 달성된 이익은 아시아의 폭넓은 생산에 신속하게 연쇄되어 연구개발비를 중복하지 않고 자동차 타이어 시장 전체의 베이스라인 기술을 향상시킵니다.

동남아시아 고무엽병의 영향

페스탈로티옵시스의 만연에 의해 인도네시아에서는 라텍스 수율이 감소하고, 천연 고무의 스팟 가격이 전년 대비 33% 상승해, 세계의 타이어 공장의 마진이 압박되고 있습니다. 앓고있는 나무는 태핑 성숙에 도달하는 데 10 년이 걸리므로 회복하는 데는 시간이 걸립니다. 생산자는 과유와 러시아 민들레의 원산지로 다양화하고 있지만, 상업적 규모는 아직 몇 시즌 앞에 있으며, 중기적으로는 비용 압력이 계속됩니다.

부문 분석

2024년 자동차용 타이어 시장 점유율은 올 시즌용이 62.28%를 차지해 선두를 유지했습니다. 겨울용 타이어는 소형이지만 유럽의 안전 의무화로 채용이 확대되고 2025-2030년 CAGR은 가장 빠른 4.24%를 보일 것으로 예측됩니다. 여름용 라인은 항상 기온이 높은 지역에서 계속 인기가 있으며, 올 터레인 및 매드 터레인 패턴은 오프로드 성능을 중시하는 SUV 소유자를 캡처하고 있습니다. 제조업체는 현재 높은 실리카 컴파운드와 적응형 사이프를 혼합하여 단일 트레드로 열과 작은 눈을 모두 수용할 수 있게 하여 대리점 재고의 복잡성을 줄일 수 있습니다.

연구개발비는 전기자동차의 요구도 목표로 하고 있습니다. 발포 인서트는 캐빈 노이즈를 줄이고 고무 화학 물질은 빙점 하에서도 유연성을 유지하기 때문에 프리미엄 겨울 SKU는 EV 구매자에게 매력적입니다. 배송 밴에 쓰리피크 마운틴 스노우 플레이크 인증을 지정하는 플릿도 늘어나고 있으며, 규제의 범위가 확대되고 있음을 이야기하고 있습니다. 반면에 데이터 중심의 타이어 회전 서비스는 트레드의 수명을 연장하고 수익을 부가가치가 높은 겨울용 교환 패키지로 전환합니다. 이러한 상호작용의 동향에 의해 시즌 라인은 단순한 온도대를 넘은 진화를 이루고 있습니다.

레이디얼 구조는 연비 효율, 안정적인 핸들링, 긴 트레드 수명으로 2024년 자동차 타이어 시장 점유율의 86.24%를 차지했습니다. 바이어스 플라이는 저속 및 고하중의 틈새 분야에서 존속하고 있지만, 그 영향력은 축소의 길을 따르고 있습니다. 가장 파괴적인 진보는 비뉴마틱 및 에어리스 부문으로 건설, 군사, 그랜드 유지 보수 차량이 펑크에 강한 가동 시간을 요구하고 있기 때문에 2030년까지 연률 5.67%의 성장이 예측되고 있습니다. 열가소성 스포크와 복합 웹은 기존의 방사형 타이어와의 구름 저항의 차이를 줄입니다.

파일럿 프로그램은 펑크 수리 및 다운타임을 고려하면 에어리스 타이어가 라이프사이클 비용을 절감할 수 있음을 보여주고 있으며, OEM은 다음 개발 사이클에서 승용차 테스트를 수행하도록 설득되었습니다. 레이디얼 타이어공급업체는 강도를 희생하지 않고 질량을 줄이는 강화 비드 필러와 슬림한 스틸 벨트를 사용하여 EV의 커브 웨이트가 상승하는 한편 점유율을 지키는 것을 목표로 하고 있습니다. 재활용성에 관한 규제는 사용 후 처리를 단순화하는 단일 소재의 에어리스 설계에 대한 관심을 더욱 높여줍니다. 그 결과는 완전한 대안이 아니라 2개 세워 기술 혁신 경쟁입니다.

승용차는 2024년 판매 대수의 57.18%를 차지해 자동차용 타이어 시장 규모의 핵심을 굳혔습니다. SUV와 크로스오버가 계속 상승하고 타이어 제조업체를 고하중 지수와 고경화로 향하고 있습니다. 현저한 성장 스토리는 BEV 전용 타이어로 세계 전기자동차 등록 대수의 급증에 따라 CAGR 10.92%의 강력한 성장이 전망되고 있습니다. 배터리의 질량이 증가하고, 순간적인 토크가 가해짐으로써, 보다 강도가 높은 케이싱, 실리카를 많이 포함하는 트레드, 어쿠스틱 댐퍼 등 수요가 높아집니다.

초기 플랫폼 엔지니어링 단계에서 프리미엄 자동차 제조업체는 맞춤형 BEV 타이어를 공동 개발하는 것이 늘어나고 있으며, 브랜드 독자적인 치수를 내장하여 교환 수요를 확보하고 있습니다. 교체 채널에서는 항속거리 최적화 마케팅을 통해 비용에 민감한 구매층이 충전당 주행거리가 늘어나면 15-30%의 가격 프리미엄을 받아들이도록 설득하고 있습니다. 한편, 소형 상용차의 전동화는 택배용 강화 측벽을 갖춘 새로운 SKU에 불을 붙입니다. 이러한 차량 믹스의 진화는 공급 체인 전반에 걸쳐 제품의 복잡성을 가속화합니다.

지역 분석

아시아는 2024년에 자동차용 타이어 시장의 54.66%를 차지하고, 2030년까지의 CAGR은 6.51%로 가장 높습니다. 중국이 광대한 OEM 기반을 통해 지역 우위를 유지하고 인도 SUV 붐이 18-20인치 크기와 프리미엄 수입품 수요를 촉진하고 있습니다. 동남아시아의 고무엽병이 천연고무공급을 제약하고 있기 때문에 합성고무의 다양화와 과유 등의 대체작물이 장려되고 있습니다.

북미는 성숙한 수리용 타이어 판매와 상용차에 대한 스마트 타이어 플랫폼의 급속한 도입에 힘입어 2위를 차지하고 있습니다. 미국 IRA가 육성한 국산 합성 고무의 생산 능력은 공급망의 리스크를 저감하고, EV의 보급률은 항속 거리와 소음 저감을 우선하는 특수 타이어 라인에 박차를 가하고 있습니다.

유럽은 여전히 프리미엄으로 지속 가능한 제품을 선호합니다. 2024년 라벨의 검토는 소비자를 고품질의 대체품으로 유도하고, 기술이 풍부한 포트폴리오를 가지는 브랜드는 보상됩니다. 그러나 카본블랙의 물류 과제는 리드 타임을 늘리고 재고 비용을 밀어 올리기 때문에 회수 카본블랙에 대한 관심과 공급업체와의 긴밀한 협력을 촉진하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 성장 촉진요인

- EU 승용차에서 전동화 주도의 초저소음 타이어 수요

- 중국 Phase-6 연료 기준 달성을 위한 저RR 타이어 채용 의무화

- 북미의 라스트 마일 플릿에서 IoT 대응 스마트 타이어 계약

- 미국 IRA 산하의 합성 고무 생산 능력으로 현지 공급 안정성 상승

- 인도 SUV의 18인치 이상 림 붐이 대당 ASP 견인

- EU-2024년의 타이어 라벨링 개정이 A랭크의 교체 수요를 견인

- 시장 성장 억제요인

- 원재료비용을 높이는 동남아시아의 고무잎병

- 보증 클레임을 가속시키는 EV의 과도한 연석 중량

- 유럽에서의 카본블랙 수송의 병목

- 임박한 미국 PFAS의 불소계 이형제 금지

- 가치/공급망 분석

- 규제 및 기술적 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액 및 수량)

- 타이어 유형별

- 여름

- 겨울

- 올 시즌

- 올 터레인 및 매드 터레인

- 타이어 디자인별

- 레이디얼

- 바이어스

- 비뉴마틱 및 에어리스

- 차량 유형별

- 승용차

- SUV 및 크로스오버

- 소형 상용차

- 대형 상용 트럭 및 버스

- 이륜차

- 오프 더 로드 및 스페셜리티(OTR, 농업, 광업, 레이스)

- 용도별

- 온로드

- 오프로드(건설, 광업, 농업)

- 최종 사용자별

- OEM

- 애프터마켓(리플레이스 및 리트레드)

- 림 사이즈별

- 15인치 이하

- 15-20인치

- 20인치 이상

- 추진력별

- 내연자동차

- 배터리 전기자동차

- 하이브리드차 및 연료전지차

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Bridgestone Corporation

- Michelin Group

- Goodyear Tire & Rubber Company

- Continental AG

- Pirelli & C. SpA

- Hankook Tire & Technology

- Yokohama Rubber Co., Ltd.

- Sumitomo Rubber Industries

- MRF Ltd.

- Apollo Tyres

- JK Tyre & Industries

- Kumho Tire

- Toyo Tire Corporation

- Nexen Tire

- Zhongce Rubber Group

- Linglong Tire

- CEAT Ltd.

- Sailun Group

- Nokian Tyres

- Triangle Tire

제7장 시장 기회와 장래의 전망

JHS 25.11.13The Automotive Tire Market stands at USD 184.20 billion in 2025 and is forecast to reach USD 216.76 billion by 2030, expanding at a 3.32% CAGR.

Multiple dynamics shape this trajectory: electric-vehicle adoption raises demand for ultra-low-noise and low-rolling-resistance products; sustainability policies encourage domestic synthetic-rubber investment; and consumer preference for larger rim diameters lifts average selling prices. Asia's manufacturing depth and rising vehicle ownership keep it the geographic anchor, while North America and Europe innovate around connectivity and premium performance. Supply-side pressures from Southeast-Asian rubber-leaf disease and European carbon-black logistics highlight the need for supply-chain resilience. Yet, the overall automotive tire market continues to expand as fleets modernize and data-rich smart-tire contracts unlock new revenue streams.

Global Automotive Tires Market Trends and Insights

Electrification-Led Demand for Ultra-Low-Noise Tires

Electric drivetrains remove engine masking noise, placing tire-road interaction at the acoustic forefront. Premium EV makers pay more premiums for noise-canceling foam products and tuned tread patterns that cut in-cabin decibels by up to 20%.The European Union's stricter exterior-noise limits reinforce this trend, and the automotive tire market now sees mainstream segments requesting similar technology for compliance and comfort. Suppliers can meet performance and regulation, secure coveted OE fitments, and maintain price discipline despite higher raw-material costs.

Mandatory low-RRR Rire Adoption in China

Phase-6 fuel-efficiency rules mandate a 15% consumption improvement, spotlighting rolling resistance. Domestic and global brands are compressing R&D cycles to 18 months to deliver silica-rich compounds capable of 8% fuel-economy gains. Gains achieved for Chinese homologation rapidly cascade into broader Asian production, elevating baseline technology across the automotive tire market without duplicative R&D spend.

Southeast-Asian Rubber-Leaf Disease Impact

Pestalotiopsis infestation has cut latex yields in Indonesia, pushing natural-rubber spot prices up 33% year-on-year and squeezing margins for tire plants worldwide. Recovery is slow because affected trees need up to 10 years to reach tapping maturity. Producers diversify toward guayule and Russian dandelion sources, yet commercial scale remains several seasons away, sustaining cost pressure through the medium term.

Other drivers and restraints analyzed in the detailed report include:

- 18-inch-plus Rim Boom in Indian SUVs

- EU-2024 Tire-Label Revamp

- Excess EV Curb-Weight Accelerating Warranty Claims

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

All-season products maintained leadership in 2024 with 62.28% of the automotive tire market share, helped by their year-round convenience in varied climates. Winter tires, although smaller, are projected to post the fastest 4.24% CAGR between 2025 and 2030 as safety mandates in Europe widen adoption. Summer lines remain popular in regions with consistently high temperatures, while all-terrain/mud-terrain patterns capture SUV owners who value off-road capability. Manufacturers now blend high-silica compounds with adaptive sipes so a single tread can tolerate both heat and light snow, lowering inventory complexity for dealers.

R&D spending also targets electric-vehicle needs: foam inserts reduce cabin noise and rubber chemistries hold flexibility below freezing, making premium winter SKUs attractive to EV buyers. More fleets specify three-peak-mountain-snowflake certification on delivery vans, underscoring growing regulatory reach. Meanwhile, data-driven tire rotation services lengthen tread life, shifting revenue toward value-added winter-changeover packages. These interplay trends ensure seasonal lines evolve well beyond simple temperature bands.

Radial construction captured 86.24% of the automotive tire market share in 2024, due to fuel efficiency, stable handling, and long tread life. Bias ply endures in low-speed, heavy-load niches, yet its influence keeps shrinking. The most disruptive advance is the non-pneumatic/airless segment, which is forecast to grow 5.67% annually through 2030 as construction, military, and grounds-maintenance fleets seek puncture-proof uptime. Thermoplastic spokes and composite webs are narrowing the rolling-resistance gap with conventional radials.

Pilot programs show airless tires delivering lifecycle cost savings once puncture repairs and downtime are factored in, persuading OEMs to schedule passenger-car trials in the next development cycle. Radial suppliers answer with reinforced bead fillers and slimmer steel belts that trim mass without sacrificing strength, aiming to defend share while EV curb weights climb. Regulations on recyclability further elevate interest in single-material airless designs that simplify end-of-life processing. The outcome is a two-track innovation race rather than an outright substitution.

Passenger cars accounted for 57.18% of the 2024 volume, cementing their place at the core of automotive tire market size. SUVs and crossovers continue encroaching, nudging tire makers toward higher load indices and taller diameters. The standout growth story is BEV-specific tires, slated for a robust 10.92% CAGR as global electric-vehicle registrations soar. Added battery mass and instant torque drive demand for stronger casings, silica-rich treads, and acoustic dampers.

During early platform engineering, premium automakers increasingly co-develop bespoke BEV tires, embedding brand-exclusive dimensions that lock in replacement revenue. In the replacement channel, range-optimization marketing persuades cost-sensitive buyers to accept 15-30% price premiums when they can verify extra miles per charge. Meanwhile, light-commercial-vehicle electrification sparks new SKUs with reinforced sidewalls for parcel-delivery duty. This vehicle-mix evolution accelerates product complexity throughout the supply chain.

The Automotive Tire Market Report is Segmented by Tire Type (Summer, Winter, and More), Tire Design (Radial, Bias, and More), Vehicle Type (Passenger Cars and More), Application (On-Road and Off-Road), End User (OEM and Aftermarket) Rim-Size (Less Than 15 Inches and More), Propulsion (ICE, BEV, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia held 54.66% of the automotive tire market in 2024 and sustained the highest 6.51% CAGR to 2030. China anchors regional dominance through its vast OEM base, while India's SUV boom fuels demand for 18-20-inch sizes and premium imports. Rubber-leaf disease in Southeast Asia constrains natural rubber supply, encouraging synthetic rubber diversification and alternative crops such as guayule.

North America ranks second, supported by mature replacement sales and rapid adoption of smart-tire platforms in commercial fleets. Domestic synthetic-rubber capacity fostered by the U.S. IRA reduces supply-chain risk, while rising EV penetration spurs specialized tire lines that prioritize range and noise reduction.

Europe continues to prioritize premium and sustainable products. The 2024 label overhaul guides consumers toward high-grade replacements, rewarding brands with technology-rich portfolios. Carbon-black logistics challenges, however, lengthen lead times and boost inventory costs, prompting interest in recovered carbon black and tighter supplier collaboration.

- Bridgestone Corporation

- Michelin Group

- Goodyear Tire & Rubber Company

- Continental AG

- Pirelli & C. SpA

- Hankook Tire & Technology

- Yokohama Rubber Co., Ltd.

- Sumitomo Rubber Industries

- MRF Ltd.

- Apollo Tyres

- JK Tyre & Industries

- Kumho Tire

- Toyo Tire Corporation

- Nexen Tire

- Zhongce Rubber Group

- Linglong Tire

- CEAT Ltd.

- Sailun Group

- Nokian Tyres

- Triangle Tire

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Electrification-led demand for ultra-low-noise tires in EU passenger cars

- 4.1.2 Mandatory low-RRR tire adoption to meet China Phase-6 fuel norms

- 4.1.3 IoT-enabled smart-tire contracts in North-American last-mile fleets

- 4.1.4 On-shored synthetic-rubber capacity under U.S. IRA boosting local supply security

- 4.1.5 18-inch-plus rim boom in Indian SUVs lifting ASP per unit

- 4.1.6 EU-2024 tyre-labelling revamp pushing A-rated replacement demand

- 4.2 Market Restraints

- 4.2.1 Southeast-Asian rubber-leaf disease inflating raw-material costs

- 4.2.2 Excess EV curb-weight accelerating warranty claims

- 4.2.3 Carbon-black shipping bottlenecks in Europe

- 4.2.4 Impending US PFAS ban on fluorinated mould-release agents

- 4.3 Value / Supply-Chain Analysis

- 4.4 Regulatory or Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers / Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Tire Type

- 5.1.1 Summer

- 5.1.2 Winter

- 5.1.3 All-Season

- 5.1.4 All-Terrain / Mud-Terrain

- 5.2 By Tire Design

- 5.2.1 Radial

- 5.2.2 Bias

- 5.2.3 Non-pneumatic / Airless

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 SUVs & Crossovers

- 5.3.3 Light Commercial Vehicles

- 5.3.4 Heavy Commercial Trucks & Buses

- 5.3.5 Two-Wheelers

- 5.3.6 Off-the-Road & Specialty (OTR, Agriculture, Mining, Racing)

- 5.4 By Application

- 5.4.1 On-Road

- 5.4.2 Off-Road (Construction, Mining, Agriculture)

- 5.5 By End User

- 5.5.1 OEM

- 5.5.2 Aftermarket (Replacement & Retread)

- 5.6 By Rim Size

- 5.6.1 Below 15 inches

- 5.6.2 15 - 20 inches

- 5.6.3 Above 20 inches

- 5.7 By Propulsion

- 5.7.1 Internal-Combustion Vehicles

- 5.7.2 Battery-Electric Vehicles

- 5.7.3 Hybrid & Fuel-Cell Vehicles

- 5.8 Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Rest of Europe

- 5.8.3 Asia-pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 South Korea

- 5.8.3.5 Rest of Asia-Pacific

- 5.8.4 South America

- 5.8.4.1 Brazil

- 5.8.4.2 Argentina

- 5.8.4.3 Rest of South America

- 5.8.5 Middle East

- 5.8.5.1 GCC

- 5.8.5.2 Turkey

- 5.8.5.3 Rest of Middle East

- 5.8.6 Africa

- 5.8.6.1 South Africa

- 5.8.6.2 Nigeria

- 5.8.6.3 Rest of Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Bridgestone Corporation

- 6.3.2 Michelin Group

- 6.3.3 Goodyear Tire & Rubber Company

- 6.3.4 Continental AG

- 6.3.5 Pirelli & C. SpA

- 6.3.6 Hankook Tire & Technology

- 6.3.7 Yokohama Rubber Co., Ltd.

- 6.3.8 Sumitomo Rubber Industries

- 6.3.9 MRF Ltd.

- 6.3.10 Apollo Tyres

- 6.3.11 JK Tyre & Industries

- 6.3.12 Kumho Tire

- 6.3.13 Toyo Tire Corporation

- 6.3.14 Nexen Tire

- 6.3.15 Zhongce Rubber Group

- 6.3.16 Linglong Tire

- 6.3.17 CEAT Ltd.

- 6.3.18 Sailun Group

- 6.3.19 Nokian Tyres

- 6.3.20 Triangle Tire

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment