|

시장보고서

상품코드

1851468

유럽의 접착제 및 실란트 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

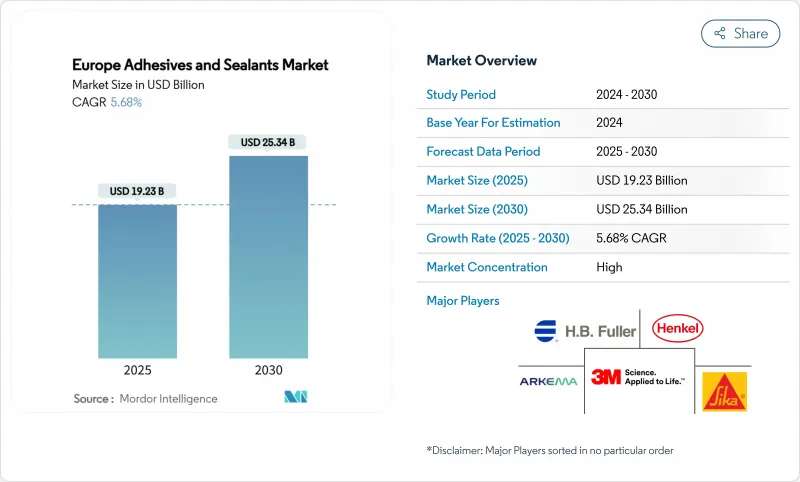

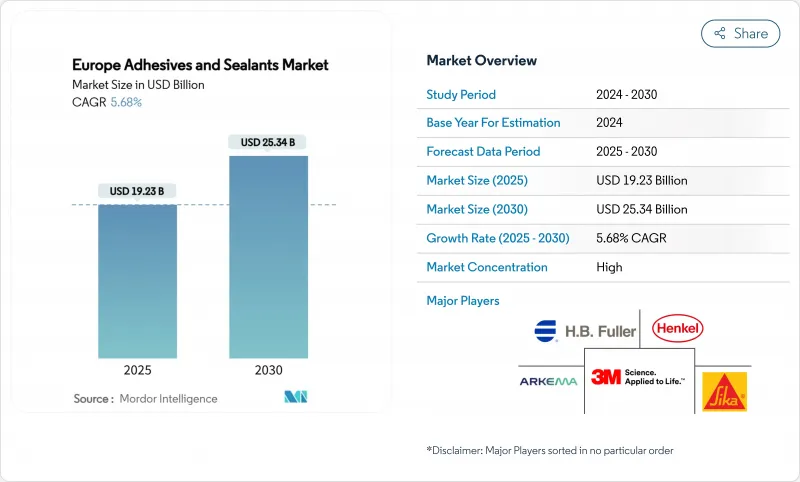

유럽의 접착제 및 실란트 시장 규모는 2025년 192억 3,000만 달러로, 예측기간 중(2025-2030년) CAGR은 5.68%로 확대되어, 2030년에는 253억 4,000만 달러에 달할 것으로 예측됩니다.

이 궤적은 건설업의 회복, 자동차의 경량화 의무, 재생가능 에너지의 확대를 활용하면서 EU의 엄격한 그린딜 규제를 극복하는 이 분야의 능력을 반영하고 있습니다. VOC 규제가 강화됨에 따라 수성 시스템이 견인력을 늘리고 UV 경화형 케미스트리는 전자 및 자동차 공장의 라인 스피드를 가속시킵니다. 독일 인프라 투자는 견조한 수요를 뒷받침하고 스페인의 신재생에너지 건설은 이 지역에서 가장 급성장하는 구조용 접착 솔루션의 구매자가 되었습니다. 경쟁의 심각성은 여전히 완만하며, 대기업의 기존 기업들은 바이오 수지에 포트폴리오를 다시 집중하고 있으며, 원료 가격의 변동과 탄소 절감 비용으로부터 이익을 보호하기 위해 인수 주도로 능력을 확대하고 있습니다.

유럽 접착제 및 실란트 시장 동향 및 통찰

주택 리폼 수요 증가

유럽의 리폼은 에너지 효율의 의무화와 유행 후 라이프 스타일의 변화에 의해 단열재, 바닥재, 창의 개수에 대한 지출이 증가해, 기세를 늘리고 있습니다. EU의 리노베이션 웨이브는 2030년까지 건물의 개수율을 두배로 늘리는 것을 목표로 하고 있으며, 열교 현상을 해소하는 연속 접착 시스템 수요를 뒷받침하고 있습니다. 독일의 연간 500억 유로(-584억 5,000만 달러)의 리노베이션 시장에서 Henkel의 LOCTITE HB S ECO와 같은 바이오 제품의 채용이 증가하고 있습니다. 북유럽 공급업체는 조립식 외관 패널을 위한 공장 도포형 접착제의 선구자이며 엄격한 실내 공기 환경 기준을 충족하면서 현장에서 신속하게 조립할 수 있습니다. 이러한 개수의 추진에 의해 유럽의 접착제 및 실란트 시장은 2028년까지 수량 성장을 유지할 것으로 보입니다.

전자상거래 포장량 급증

소포 출하가 증가함에 따라 컨버터는 FEICA가 발표한 종이 재활용 지침을 준수하는 고속 무용제 접착 솔루션을 채택해야 합니다. 연포장용 접착제는 EU 플라스틱 전략 하에서 재활용을 단순화하는 모노 머티리얼 설계를 지원하면서 접착 강도와 탈잉크성의 균형을 맞추어야 합니다. 독일과 네덜란드에서는 엄격한 점도 관리와 빠른 경화가 필요한 자동화 라인 업그레이드가 진행되고 있습니다. 이러한 동향은 유럽의 접착제 및 실란트 시장, 특히 신속한 처리량을 위해 설계된 핫멜트 및 수성 등급 시장 확대를 지원하는 것입니다.

환경 문제 증가

2023년 8월 발효된 REACH 디이소시아네이트 규제는 폴리우레탄 시스템의 개질 또는 작업자 훈련의 의무를 강요하고, 2026년 8월 발효될 포름알데히드 배출 규제는 초저 배출 등급으로의 이동을 촉진합니다. 옥타메틸트리실록산을 포함한 247개의 SVHC가 추가되어 규제 불확실성이 확대됩니다. 지속가능성에 대한 투자 요구는 유럽의 화학 부문 전반에 걸쳐 연간 자본 지출을 70% 증가시키고 이익을 줄이지만 바이오 원료의 장기적인 혁신에 박차를 가합니다.

부문 분석

아크릴 수지는 범용성과 다양한 기재에 대한 접착성으로 2024년 유럽 접착제 및 실란트 시장에서 37.16%의 매출 점유율을 유지했습니다. 바이오 혁신을 포함한 기타 수지는 탄소 감축 의무화가 강화됨에 따라 2030년까지 연평균 복합 성장률(CAGR)이 6.96% 확대될 것으로 예측됩니다. 유럽 접착제 및 실란트 바이오베이스 등급 시장 규모는 BASF의 재생 가능한 에틸 아크릴레이트가 롤아웃되고 자일란 핫멜트가 재사용 가능한 상태로 30MPa의 랩 시어를 입증함에 따라 확대될 것으로 예측됩니다. 시아노아크릴레이트는 일렉트로닉스의 소형화로 지지를 모으고, 폴리우레탄 성형 제조업체는 디이소시아네이트 트레이닝을 우회하는 습기 경화 시스템을 추구합니다. 실리콘 수지는 고온 분야에서 성장하고, VAE 및 EVA는 비용 중심의 틈새를 유지하고 있습니다.

수성 플랫폼은 2024년 매출 기준 43.19%를 차지하며, 이는 정착된 생산 라인과 VOC 캡의 무결성을 반영합니다. 그러나 UV 경화 시스템은 조립 공장이 인스턴트 본드 가공을 요구하기 때문에 2030년까지 CAGR은 6.54%가 될 것으로 보입니다. Panacol의 흑색 UV 에폭시는 두꺼운 층으로 경화하기 때문에 그림자 영역을 없애고 현재 EV 모터 와이어의 응력 완화 조인트로 지정되어 있습니다.

반응성 핫멜트는 빠른 경화와 강력한 최종 접착을 결합하여 고속 패키징 라인에 유용합니다. 긴 오픈타임이 중요한 항공우주 분야에서는 용제를 사용하는 수요가 지속되고 있지만, 고고형분 버전은 엄격한 배기가스 규제를 충족시키는데 도움이 되고 있습니다. LED-UV 램프로의 설비 업그레이드는 에너지 사용을 줄이고 유럽의 접착제 및 실란트 시장에서 기술 전환을 더욱 촉진합니다.

유럽의 접착제 및 실란트 보고서는 접착제 수지(아크릴, 시아노아크릴레이트, 에폭시 등), 접착 기술(핫멜트, 반응성, 용매 기반 등), 실란트 수지(폴리 우레탄, 폭시, 아크릴, 기타), 최종 사용자 산업(항공우주, 자동차, 건축 및 건설 등), 지역(독일, 영국, 프랑스, 이탈리아, 스페인, 러시아, 북유럽 국가 및 기타 유럽)으로 구분됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 주택 리폼 수요 증가

- 전자상거래 포장량의 급증

- 가속하는 유럽 자동차 산업의 경량화

- 급성장하는 풍력 터빈 블레이드 접착 시장

- 조립식 모듈식 건축의 보급

- 시장 성장 억제요인

- 높아지는 환경 문제

- 불안정한 원료 가격

- 로봇 접착제 도포 노동력에서의 스킬 갭

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 접착 수지별

- 아크릴

- 시아노아크릴레이트

- 에폭시

- 폴리우레탄

- 실리콘

- VAE 및 EVA

- 기타 수지(실란 변성 폴리머(SMP), 바이오 베이스 수지 등)

- 접착 기술별

- 핫멜트

- 반응성

- 용제계

- UV 경화형

- 수성

- 실란트 수지별

- 폴리우레탄

- 에폭시

- 아크릴

- 실리콘

- 기타 수지(폴리설파이드, SMP 하이브리드 등)

- 최종 사용자 업계별

- 항공우주

- 자동차

- 건축 및 건설

- 신발 및 가죽

- 헬스케어

- 포장

- 목공 및 가구

- 기타 최종 사용자 산업(재생에너지, 일렉트로닉스 및 어플라이언스 등)

- 지역별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- Akzo Nobel NV

- Arkema

- Avery Dennison Corporation

- BASF

- Dow

- Dymax

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC.

- Jowat

- Mapei SpA

- Momentive

- Munzing

- PPG Industries, Inc.

- Sika AG

- Soudal Group

- Wacker Chemie AG

제7장 시장 기회와 장래의 전망

JHS 25.11.13The Europe Adhesives And Sealants Market size is estimated at USD 19.23 billion in 2025, and is expected to reach USD 25.34 billion by 2030, at a CAGR of 5.68% during the forecast period (2025-2030).

This trajectory reflects the sector's ability to navigate stringent EU Green Deal regulations while capitalizing on construction recovery, automotive lightweighting mandates, and renewable-energy expansion. Water-borne systems gain traction as VOC limits tighten, and UV-cured chemistries accelerate line speeds in electronics and automotive plants. German infrastructure outlays underpin steady demand, while Spain's renewable build-out positions it as the region's quickest-growing buyer of structural bonding solutions. Competitive intensity remains moderate, with large incumbents refocusing portfolios on bio-based resins and acquisition-driven capability expansion to safeguard margins against feedstock price volatility and carbon-reduction costs.

Europe Adhesives And Sealants Market Trends and Insights

Rising Demand from Residential Renovation

European renovation activity is gathering momentum as energy-efficiency mandates and post-pandemic lifestyle shifts lift spending on insulation, flooring, and window upgrades. The EU Renovation Wave aims to double building refurbishment rates by 2030, bolstering demand for continuous-bonding systems that eliminate thermal bridging. Germany's EUR 50 billion (~USD 58.45 billion) annual renovation market increasingly specifies bio-based products such as Henkel's LOCTITE HB S ECO, which cuts embodied CO2 by more than 60% compared with fossil-based counterparts. Nordic suppliers pioneer factory-applied adhesives for prefabricated facade panels, allowing rapid site assembly while meeting stringent indoor-air-quality norms. This renovation push is set to sustain volume growth for the European adhesives and sealants market through 2028.

Surge in E-Commerce Packaging Volumes

Rising parcel shipments prompt converters to adopt high-speed, solvent-free bonding solutions compatible with paper-recycling guidelines published by FEICA. Flexible-packaging adhesives must balance bond strength and de-inkability while supporting mono-material designs that simplify recycling under the EU Plastics Strategy. Germany and the Netherlands are upgrading automated lines that require tight viscosity control and quick setting. These trends underpin incremental gains for the European adhesives and sealants market, especially in hot-melt and waterborne grades engineered for rapid throughput.

Rising Environmental Concerns

REACH diisocyanate restrictions effective August 2023 force reformulation of polyurethane systems or mandatory worker training, while formaldehyde emission ceilings effective August 2026 drive shifts to ultra-low-emission grades. The addition of 247 SVHCs, including octamethyltrisiloxane, extends regulatory uncertainty. Sustainability investment needs 70% higher annual capital outlays across Europe's chemical sector, compressing margins yet spurring long-run innovation in bio-based feedstocks.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Lightweighting in European Auto Industry

- Fast-Growing Wind-Turbine Blade Bonding Market

- Volatile Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylics retained 37.16% revenue share of the European adhesives and sealants market in 2024, thanks to versatility and adhesion to diverse substrates. Other resins, including bio-based innovations, are forecast to expand 6.96% CAGR to 2030 as carbon-reduction mandates intensify. Europe adhesives and sealants market size for bio-based grades is projected to widen as BASF's renewable ethyl acrylate rolls out and xylan hot-melts demonstrate 30 MPa lap-shear while remaining reusable. Cyanoacrylates gain traction in electronics miniaturization, and polyurethane formulators pursue moisture-curing systems that bypass diisocyanate training. Silicone chemistries grow in high-temperature segments, whereas VAE/EVA retains cost-driven niches.

Waterborne platforms accounted for 43.19% of the 2024 revenue base, reflecting entrenched production lines and alignment with VOC caps. UV-cured systems, however, will post a 6.54% CAGR through 2030 as assembly plants seek instant-bond processing. Panacol's black UV epoxies cure in thicker layers, eliminating shadow areas, and are now specified in EV motor wire stress-relief joints.

Reactive hot melts combine rapid set with strong final bonds, serving high-speed packaging lines. Solvent-borne demand persists in aerospace, where long open time is critical, but higher-solids versions help meet tightening emission norms. Equipment upgrades toward LED-UV lamps cut energy use and further incentivize technology switching in the European adhesives and sealants market.

The Europe Adhesives and Sealants Report is Segmented by Adhesive Resin (Acrylic, Cyanoacrylate, Epoxy, and More), Adhesive Technology (Hot-Melt, Reactive, Solvent-Borne, and More), Sealant Resin (Polyurethane, Epoxy, Acrylic, and More), End-User Industry (Aerospace, Automotive, Building and Construction, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, NORDIC Countries, and Rest of Europe).

List of Companies Covered in this Report:

- 3M

- Akzo Nobel N.V.

- Arkema

- Avery Dennison Corporation

- BASF

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC.

- Jowat

- Mapei S.p.A

- Momentive

- Munzing

- PPG Industries, Inc.

- Sika AG

- Soudal Group

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand from Residential-Renovation

- 4.2.2 Surge in E-Commerce Packaging Volumes

- 4.2.3 Accelerating Lightweighting in European Auto Industry

- 4.2.4 Fast-Growing Wind-Turbine Blade Bonding Market

- 4.2.5 Prefab Modular Construction Uptake

- 4.3 Market Restraints

- 4.3.1 Rising Environmental Concerns

- 4.3.2 Volatile Feedstock Prices

- 4.3.3 Skill Gap in Robotic Adhesive-Dispensing Workforce

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Adhesive Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE / EVA

- 5.1.7 Other Resins (Silane-Modified Polymer (SMP), Bio-based Resins, etc.)

- 5.2 By Adhesive Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-Borne

- 5.2.4 UV-Cured

- 5.2.5 Water-Borne

- 5.3 By Sealant Resin

- 5.3.1 Polyurethane

- 5.3.2 Epoxy

- 5.3.3 Acrylic

- 5.3.4 Silicone

- 5.3.5 Other Resins (Polysulfide, SMP Hybrid, etc.)

- 5.4 By End-User Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Woodworking and Joinery

- 5.4.8 Other End-User Industries (Renewable Energy,Electronics and Appliances, etc.)

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 NORDIC Countries

- 5.5.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 Dow

- 6.4.7 Dymax

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman International LLC.

- 6.4.11 Jowat

- 6.4.12 Mapei S.p.A

- 6.4.13 Momentive

- 6.4.14 Munzing

- 6.4.15 PPG Industries, Inc.

- 6.4.16 Sika AG

- 6.4.17 Soudal Group

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 EU Green Deal push for low-VOC and circular materials

- 7.3 Innovation and Development of Bio-based Adhesives