|

시장보고서

상품코드

1851472

연기 감지기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Smoke Detector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

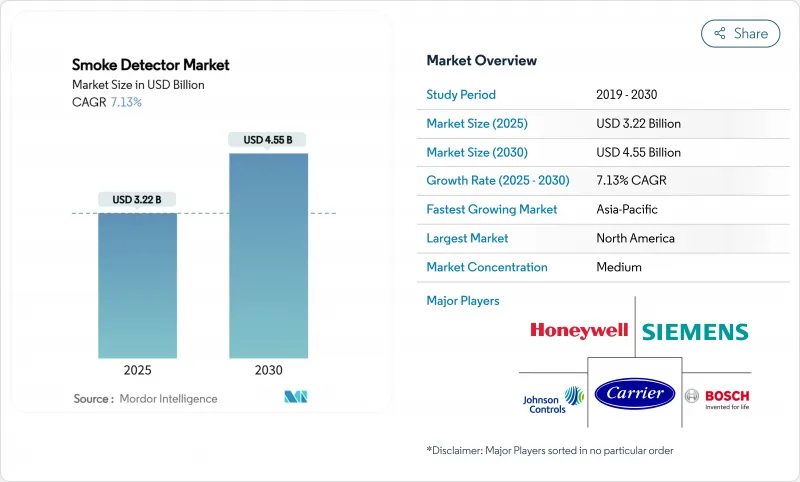

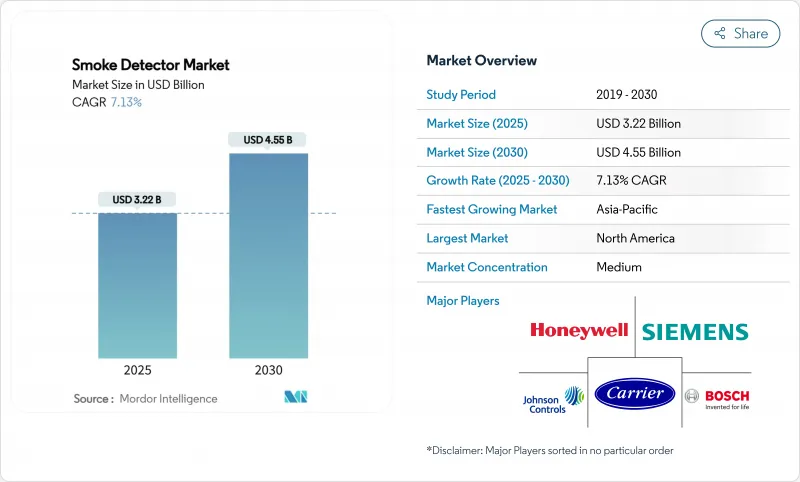

연기 감지기 시장 규모는 2025년에 32억 2,000만 달러, CAGR 7.13%로 성장하여 2030년에는 45억 5,000만 달러까지 확대될 전망입니다.

성장을 뒷받침하는 것은 화재 안전 기준의 엄격화, 진행 중인 도시 건설, 오보를 줄여 보험료를 인하하는 스마트한 보험 대상 기기로의 급속한 전환입니다. 북미 건설 규정, 유럽 EN 54 프레임워크, 중국 GB 55037-2022의 복고풍 의무화로 인터커넥트형 알람의 설치 기준이 계속 확대되고 있으며, 듀얼 센서와 흡입 기술은 복잡한 현장 오보 문제를 해결하고 있습니다. 광전 제품은 낮은 스몰더리스크 주택에서 리드를 유지하고 있지만, 멀티센서 시스템은 현재 법령과 보험사의 면밀한 조사에 직면하고 있는 사무실, 쇼핑몰, 창고에서 큰 승리를 거두고 있습니다. 제조업체는 밀폐형 리튬 배터리와 주소 지정이 가능한 IoT 모듈에 주력하여 유지 보수를 줄이고 빌딩 관리 플랫폼에 실시간 데이터를 전달하고 있습니다. 경쟁 분야는 세계 리더가 틈새 시장의 혁신자를 인수하는 한편, 신규 진출기업이 신흥 시장을 위해 저가격으로 앱 대응 설계를 추진하기 위해 적당히 세분화되고 있습니다.

세계 연기 감지기 시장 동향과 통찰

미국과 캐나다에서 주택용 화재 경보기의 상호 연결 의무화

24CFR § 3280.209의 업데이트로 미국 제조 주택에서는 신규 또는 교체 경보가 모두 하드 배선으로 상호 연결되어야 하며, 하나가 연기를 감지하면 모든 유닛이 작동하게 되었습니다. 국제코드 평의회의 R314 조항은 부지 내에 건설된 주택에 대한 이 요건을 반영하고 있으며, 소유자가 노후화된 독립형 장비를 교체할 때 대규모 리노베이션의 물결이 밀려들고 있습니다. 캐나다는 국가 소방법(National Fire Code)에서 유사한 규칙을 수립하고 있으며, 온타리오주 소방법(Ontario's Fire Code)에서는 주택과 게스트 스위트 모두에서 상호 연결을 의무화하고 있습니다. 건설업자가 이에 따라 멀티링크 대응 기기의 출하대수가 증가하고 보험사는 보험료를 인하하기 때문에 더욱 보급이 진행됩니다. 공급업체는 기존 주택 스톡 업그레이드를 간소화하는 유선-무선 메쉬 콤보 솔루션을 지원합니다.

EN 54-29 다중 센서 요구사항이 유럽 상업시설 개조를 가속화

EN 54-29는 연기, 열 및 CO 감지를 하나의 인증된 멀티 센서 헤드로 통합하여 바쁜 상업 공간에서 원치 않는 트리거를 줄입니다. 독일과 벨기에는 현재 EN 54-13 시스템 전체의 호환성을 요구하고 있으며, 호텔, 쇼핑몰, 사무실은 기존의 단일 기술 감지기를 형식 인증된 하이브리드로 교체해야 합니다. 소방서는 유효한 다중 센서 신호를 화재 확인 신호로 취급하여 비용이 많이 드는 출동 및 보험 인수의 위험을 줄입니다. 시스템 통합자는 감지기, 어드레서블 패널 및 클라우드 분석을 번들로 프로젝트의 이점을 확대하고 있습니다. 영국, 프랑스, 북유럽에서는 에너지 효율적인 리노베이션이 진행되고 있습니다.

전리 상자에 Am-241 동위 원소 공급 제약

로스알라모스 국립연구소가 Am-241의 국내 생산을 재개했으나 여전히 생산량이 급박하고 출시가 복잡합니다. 지정학적 갈등은 전통적인 대체 공급원인 러시아의 수출을 제한합니다. 제조업체는 광전식 또는 듀얼 센서 헤드를 중심으로 라인을 재설계하여 헤지하고 있지만, 비용에 민감한 구매자는 여전히 빠른 화염 감지를 위해 이온화를 선호합니다. 스팟 부족은 부품 가격을 인상하고, 이폭을 압박하고, 라틴아메리카와 아프리카 전역에서 광전 모델과의 가격차를 넓히고 있습니다.

부문 분석

광전 모델은 2024년 연기 감지기 시장에서 34%의 점유율을 차지했으며, 가정 내 화재 위험을 대상으로 하는 규제 덕분에 선호되었습니다. 이온화 원리와 광전원리를 융합한 듀얼 센서 유닛은 상업규범이 보다 넓은 범위를 커버할 것을 요구하고 있기 때문에 가장 빠른 9.5%의 CAGR을 기록합니다. 이온화 헤드는 여전히 저소득자 주택에서 판매되고 있지만 Am-241 제약에 직면하고 있습니다. 한편, 빔 검출기는 장거리의 전망선을 필요로 하는 아트리움이나 경기장에서 스폿을 확보하고 있습니다. 흡입식 시스템은 하니웰의 FAAST FLEX가 오보가 다운타임의 위험이 되는 먼지가 많은 산업지역에서 점유율을 늘리고 프리미엄층을 차지하고 있습니다.

멀티센서 채택에 대한 규제의 기울기는 연구개발 예산을 재조합하고 있습니다. 네이처 잡지의 연구는 정전용량 입자 분석이 ppm 수준에서 연기와 증기를 식별할 수 있음을 입증하여 보다 스마트한 알고리즘을 가능하게 했습니다. EN 54의 통일성은 공급업체가 혼합된 센서를 일반 패널에 연결할 수 있어 통합자의 위험을 줄여줍니다. 이미 석유 및 가스 플랜트에서 시험적으로 도입된 비디오 연기 감지는 몇 초 안에 연기를 식별하여 포인트 센서를 혼란시킬 수 있지만 대역폭이 높기 때문에 비용이 낮을 때까지 주류 사용이 제한됩니다.

2024년 연기 감지기 시장에서는 배터리 구동 장비가 44%의 점유율을 차지했습니다. 그러나 배터리 백업이 포함된 유선형 장치는 정전 시에도 경보가 작동하도록 규제가 요구됨에 따라 8.8%라는 가장 높은 연평균 성장률(CAGR)을 보였습니다. 유럽에서는 밀폐식 10년 리튬팩이 지지를 모으고 있으며, 연간 유지보수를 절약하고 사용자에 의한 변조를 막고 있습니다. 솔라 어시스트 헤드와 에너지 수확 마이크로 발전기는 여전히 틈새 시장으로 원격지 채광소 및 통신 대피소로 제한됩니다.

총 소유 비용(Total Cost of Ownership)은 가격보다 구매자의 선택에 대한 지침입니다. 덴버시 소방국은 배터리 잔량 부족을 알리는 호출음에 의한 출동 요청을 줄이기 위해 리튬 배터리 알람을 추진하고 있습니다. OEM 대시보드는 현재 배터리 상태를 신고하여 부동산 관리자가 적극적으로 장치를 교체할 수 있도록 합니다. 연구 프로젝트는 건물의 HVAC 진동에서 에너지를 절약하는 것을 찾고 있지만, 상업적 준비는 적어도 5년 이상이 걸립니다.

지역 분석

북미는 연기 감지기 시장이 2024년 매출액의 40%를 차지했으며 엄격한 건축 기준법과 보험 회사의 인센티브에 의해 활성화되고 있습니다. 미국의 제조 주택에 관한 규칙은 하드 와이어로 상호 연결된 경보를 의무화하고 있으며 캐나다 소방법도 그 조항을 반영합니다. 스테이트 팜이 200만 개의 Ting 센서를 배포하는 것은 보험 회사 주도의 스마트 피벗의 예이며, 리버티 뮤추얼은 구글 브랜드의 감지기에 단계적인 보험료를 제공합니다. 멕시코의 산업 회랑에서는 니어 쇼어링 브랜드에 서비스를 제공하는 수출 창고를 보호하기 위해 흡입 시스템을 채택하고 있습니다.

아시아태평양은 2025-2030년 CAGR이 가장 빠른 8.4%를 나타낼 전망입니다. 중국의 GB 55037-2022는 모든 고층 주택에 감지기 네트워크를 설치하고 부동산 관리 대시보드와의 IoT 통합을 추진하도록 규정하고 있으며, 2030년까지 이 지역의 연기 감지기 시장 규모를 획기적으로 확대합니다. 일본은 밀집한 도시 빌딩의 과제를 해결하기 위해 멀티 센서 제품을 채택하고, 인도의 스마트 시티 프로젝트는 예산 관계로 LoRaWAN을 정중하게 건너뛰지만, 지하철역 구내의 어드레서블 회선이 선호됩니다. ASEAN 국가들은 설치업체 부족으로 고통받고 있으며 인지도가 높아졌음에도 불구하고 일부 프로젝트가 지연되고 있습니다.

유럽은 EN 54의 정합화가 레트로핏을 지지하고, 한 자리수 중반의 성장을 유지하고 있습니다. 독일과 벨기에는 EN 54-13 호환성 증명을 시행하고 전체 시스템 업그레이드 수요를 증가시키고 있습니다. 영국의 오보 과금 제도는 장애물을 높이는 것과 동시에, 오너에 대해서, 도입 후의 리스크가 지나가면, 보다 뛰어난 기술에 투자하도록 압력을 가하는 것입니다. 북유럽 국가들은 유지 보수 노력을 줄이기 위해 밀폐형 리튬 설계를 지원합니다. 남유럽 국가에서는 호스피탈리티를 중시하고 관광업이 회복되고 소유자가 1990년대의 이온화 헤드를 듀얼 센서 유닛으로 교환함으로써 새로운 보험 조항을 충족하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 미국과 캐나다에 있어서의 주택용 화재 경보기의 상호 접속 의무화

- EN 54-29 멀티 센서 요구사항이 유럽에서 상업적 개조 가속화

- 중국의 2024년 고층 빌딩 GB50116 코드 업그레이드

- 유럽에서 유지 보수 비용을 절감하는 10년 밀봉 리튬 배터리 개조

- IoT 접속형 감지기의 보험료 할인

- 전자상거래 창고 붐이 흡입식 검출기를 견인한다

- 시장 성장 억제요인

- 전리 상자에의 Am-241 아이소토프공급 제약

- ASEAN에 있어서의 코드 준거의 설치 기술 격차

- 영국의 다중 센서 채택을 늦추는 잘못된 경보 책임

- 인도와 브라질의 LoRaWAN/BLE 스마트 검출기의 높은 초기 비용

- 가치/공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 센서 유형별

- 광전

- 이온화

- 듀얼 센서(이온화+광전식)

- 빔

- 흡입/에어 샘플링

- 전원별

- 배터리 구동

- 하드 와이어

- 배터리 백업이있는 하드 와이어

- 태양과 에너지 수확

- 접속성별

- 독립형/전통형

- 어드레서블

- 스마트/IoT 대응

- 최종 사용자별

- 주택용

- 상업용

- 기업 오피스

- 접객 & 레저

- 교육시설

- 의료시설

- 소매와 쇼핑몰

- 산업

- 석유 및 가스

- 제조공장

- 데이터센터

- 운송 및 물류

- 항공

- 마린

- 철도·지하철

- 유통 채널별

- 직접/시스템 인티그레이터

- 간접적

- 오프라인 소매/도매

- 온라인(전자상거래)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Honeywell International Inc.

- Siemens AG

- Johnson Controls International plc

- Robert Bosch GmbH

- Hochiki Corporation

- ABB Ltd

- Carrier Global(Kidde)

- Resideo Technologies(First Alert/BRK)

- Google LLC(Nest Labs)

- Schneider Electric SE

- Panasonic Corporation

- Apollo Fire Detectors Ltd(Halma plc)

- X-Sense(Shenzhen Huidu)

- Hekatron Brandschutz

- Fike Corporation

- Nittan Co., Ltd.

- Mircom Group of Companies

- Tyco(Johnson Controls Fire Protection)

- Ei Electronics

- Hochiki America

- Bosch Security Systems

제7장 시장 기회와 장래의 전망

SHW 25.11.13The smoke detector market size is estimated at USD 3.22 billion in 2025 and is on track to register a 7.13% CAGR, lifting revenues to USD 4.55 billion by 2030.

Growth is propelled by stricter fire-safety codes, ongoing urban construction, and a rapid swing toward smart, insured-incentivized devices that cut false alarms and lower premiums. Construction rules in North America, the EN 54 framework in Europe, and China's GB 55037-2022 retrofit mandate continue to widen the installed base of interconnected alarms, while dual-sensor and aspirating technologies address the false-alarm problem in complex sites. Photoelectric products keep their lead in low-smolder risk dwellings, yet multi-sensor systems are winning big in offices, malls, and warehouses that now face both code and insurer scrutiny. Manufacturers concentrate on sealed lithium batteries and addressable IoT modules to reduce maintenance and deliver real-time data to building management platforms. The competitive field stays moderately fragmented as global leaders acquire niche innovators, while new entrants push low-cost, app-ready designs for emerging markets.

Global Smoke Detector Market Trends and Insights

Mandatory Interconnection of Residential Smoke Alarms in US & Canada

The 24 CFR § 3280.209 update obliges every new or replacement alarm in US manufactured housing to be hard-wired and interconnected, triggering all units when one senses smoke. The International Code Council's R314 clause mirrors this requirement for site-built dwellings, creating a large retrofit wave as owners replace aging stand-alone devices. Canada follows with similar rules in its National Fire Code, and Ontario's Fire Code enforces interconnection in both dwelling units and guest suites. As builders comply, shipment volumes of multi-linkable devices increase, and insurers lower premiums, further pushing adoption. Vendors respond with combo wired-wireless mesh solutions that simplify upgrades in existing housing stock.

EN 54-29 Multi-Sensor Requirement Accelerating Commercial Retrofits in Europe

EN 54-29 aligns smoke, heat, and CO sensing under one certified multi-sensor head, reducing nuisance triggers in busy commercial spaces. Germany and Belgium now demand EN 54-13 system-wide compatibility, compelling hotels, malls, and offices to swap legacy single-technology detectors for type-approved hybrids. Fire services treat validated multi-sensor signals as confirmed fires, trimming costly call-outs and underwriting risk, a perk amplified by some insurers offering premium credits. Systems integrators see higher project margins as they bundle detectors with addressable panels and cloud analytics. Retrofits gather pace in the UK, France, and Nordics where energy-efficient refurbishments are underway.

Am-241 Isotope Supply Constraints for Ionization Chambers

Los Alamos National Laboratory resumed domestic Am-241 production, yet volumes remain tight and ramp-up is complex. Geopolitical frictions limit Russian exports, the traditional fallback source. Manufacturers hedge by redesigning lines around photoelectric or dual-sensor heads, but cost-sensitive buyers still prefer ionization for fast-flame detection. Spot shortages lift component prices, pressuring margins and widening the price gap to photoelectric models across Latin America and Africa.

Other drivers and restraints analyzed in the detailed report include:

- China's 2024 GB50116 Code Upgrade for High-Rise Buildings

- 10-Year Sealed Lithium-Battery Retrofits Reducing Maintenance Costs in Europe

- Installation Skill Gap in ASEAN Code-Compliant Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Photoelectric models held 34% share of the smoke detector market in 2024, favored by codes targeting smoldering-fire risk in homes. Dual-sensor units, blending ionization and photoelectric principles, post the fastest 9.5% CAGR as commercial codes demand broader coverage. Ionization heads still sell into low-income housing but face Am-241 constraints, while beam detectors secure spots in atria and stadiums that require long-range line-of-sight. Aspirating systems occupy the premium tier, with Honeywell's FAAST FLEX gaining mindshare in dusty industrial zones where false alarms risk downtime.

The regulatory tilt toward multi-sensor adoption is reshaping R&D budgets. A Nature study proves capacitive particle analysis can recognize smoke versus steam at ppm levels, enabling smarter algorithms. EN 54 uniformity allows mixed-vendor sensors to plug into common panels, cutting integrator risk. Video smoke detection, already piloted in oil-gas plants, may disrupt point sensors by identifying smoke in seconds, though high bandwidth limits mainstream use until costs fall.

Battery-powered devices retained 44% share of the smoke detector market in 2024 because retrofits seldom add wiring. Yet hard-wired units with battery backup display the strongest 8.8% CAGR as codes insist alarms keep working during outages. Sealed 10-year lithium packs gain favor in Europe, saving annual maintenance and preventing user tampering. Solar-assisted heads and energy-harvesting micro-generators remain niche, restricted to remote mining or telecom shelters.

Total cost of ownership guides buyer choice more than sticker price. Denver Fire Department promotes lithium-battery alarms to reduce callouts for chirping low-battery alerts. OEM dashboards now flag battery health, letting property managers replace units proactively. Research projects explore energy-scavenging from building HVAC vibration, but commercial readiness is at least five years out.

The Smoke Detector Market Report is Segmented by Sensor Type (Photoelectric, Ionization, Dual-Sensor, Beam, and More), Power Source (Battery-Powered, Hard-Wired, and More), Connectivity (Stand-Alone/Conventional, Addressable, Smart/IoT-Enabled), End-User (Residential, Commercial, Industrial, and More), Distribution Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 40% of 2024 revenue for the smoke detector market, energized by tight building codes and widespread insurer incentives. US manufactured housing rules require hard-wired interconnected alarms, while Canada's Fire Code mirrors those clauses. State Farm's distribution of 2 million Ting sensors exemplifies the insurer-driven smart pivot, and Liberty Mutual offers tiered premiums for Google-branded detectors. Mexico's industrial corridors adopt aspirating systems to safeguard export warehouses serving near-shoring brands.

Asia Pacific records the fastest 8.4% CAGR for 2025-2030. China's GB 55037-2022 dictates detector networks in all high-rise residences and pushes IoT integration with property-management dashboards, lifting the smoke detector market size for the region dramatically through 2030. Japan adopts multi-sensor products to solve dense urban building challenges, while India's smart-city projects politely skip LoRaWAN owing to budget but favor addressable lines in metro stations. ASEAN nations struggle with installer shortages, delaying some projects despite rising awareness.

Europe maintains mid-single-digit growth as EN 54 harmonization underpins retrofits. Germany and Belgium enforce EN 54-13 compatibility proof, boosting demand for full-system upgrades. The UK's false-alarm charging adds an extra hurdle yet simultaneously pressures owners to invest in better technology once bedding-in risks pass. Nordic countries champion sealed lithium designs to cut maintenance. Southern Europe leans on hospitality builds, where tourism rebounds and owners replace 1990s-era ionization heads with dual-sensor units to meet new insurance clauses.

- Honeywell International Inc.

- Siemens AG

- Johnson Controls International plc

- Robert Bosch GmbH

- Hochiki Corporation

- ABB Ltd

- Carrier Global (Kidde)

- Resideo Technologies (First Alert/BRK)

- Google LLC (Nest Labs)

- Schneider Electric SE

- Panasonic Corporation

- Apollo Fire Detectors Ltd (Halma plc)

- X-Sense (Shenzhen Huidu)

- Hekatron Brandschutz

- Fike Corporation

- Nittan Co., Ltd.

- Mircom Group of Companies

- Tyco (Johnson Controls Fire Protection)

- Ei Electronics

- Hochiki America

- Bosch Security Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory Interconnection of Residential Smoke Alarms in US and Canada

- 4.2.2 EN 54-29 Multi-Sensor Requirement Accelerating Commercial Retrofits in Europe

- 4.2.3 China's 2024 GB50116 Code Upgrade for High-Rise Buildings

- 4.2.4 10-Year Sealed Lithium-Battery Retrofits Reducing Maintenance Costs in Europe

- 4.2.5 Insurance Premium Discounts for IoT-Connected Detectors

- 4.2.6 E-Commerce Warehousing Boom Driving Aspirating Detectors

- 4.3 Market Restraints

- 4.3.1 Am-241 Isotope Supply Constraints for Ionization Chambers

- 4.3.2 Installation Skill Gap in ASEAN Code-Compliant Deployment

- 4.3.3 False-Alarm Liability Slowing UK Multi-Sensor Adoption

- 4.3.4 High Up-Front Cost of LoRaWAN/BLE Smart Detectors in India and Brazil

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Photoelectric

- 5.1.2 Ionization

- 5.1.3 Dual-Sensor (Ionization + Photoelectric)

- 5.1.4 Beam

- 5.1.5 Aspirating / Air-Sampling

- 5.2 By Power Source

- 5.2.1 Battery-Powered

- 5.2.2 Hard-Wired

- 5.2.3 Hard-Wired with Battery Backup

- 5.2.4 Solar and Energy-Harvesting

- 5.3 By Connectivity

- 5.3.1 Stand-Alone / Conventional

- 5.3.2 Addressable

- 5.3.3 Smart / IoT-Enabled

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.2.1 Corporate Offices

- 5.4.2.2 Hospitality and Leisure

- 5.4.2.3 Education Facilities

- 5.4.2.4 Healthcare Facilities

- 5.4.2.5 Retail and Malls

- 5.4.3 Industrial

- 5.4.3.1 Oil and Gas

- 5.4.3.2 Manufacturing Plants

- 5.4.3.3 Data Centers

- 5.4.4 Transportation and Logistics

- 5.4.4.1 Aviation

- 5.4.4.2 Marine

- 5.4.4.3 Rail and Metro

- 5.5 By Distribution Channel

- 5.5.1 Direct / System Integrators

- 5.5.2 Indirect

- 5.5.2.1 Offline Retail / Wholesale

- 5.5.2.2 Online (E-commerce)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Siemens AG

- 6.4.3 Johnson Controls International plc

- 6.4.4 Robert Bosch GmbH

- 6.4.5 Hochiki Corporation

- 6.4.6 ABB Ltd

- 6.4.7 Carrier Global (Kidde)

- 6.4.8 Resideo Technologies (First Alert/BRK)

- 6.4.9 Google LLC (Nest Labs)

- 6.4.10 Schneider Electric SE

- 6.4.11 Panasonic Corporation

- 6.4.12 Apollo Fire Detectors Ltd (Halma plc)

- 6.4.13 X-Sense (Shenzhen Huidu)

- 6.4.14 Hekatron Brandschutz

- 6.4.15 Fike Corporation

- 6.4.16 Nittan Co., Ltd.

- 6.4.17 Mircom Group of Companies

- 6.4.18 Tyco (Johnson Controls Fire Protection)

- 6.4.19 Ei Electronics

- 6.4.20 Hochiki America

- 6.4.21 Bosch Security Systems

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment