|

시장보고서

상품코드

1851473

신장 바이오마커 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Renal Biomarkers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

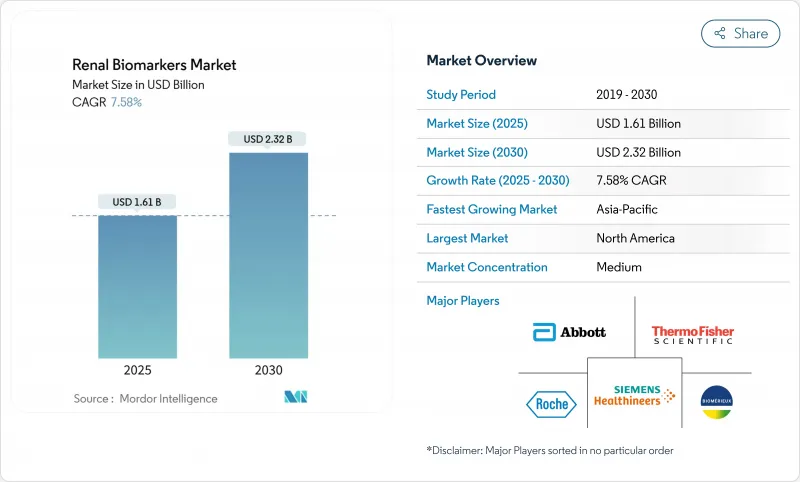

신장 바이오마커 시장은 2025년에 16억 1,000만 달러, 2030년에는 23억 2,000만 달러에 이르고, 예측 기간 동안 7.58%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다.

이 확장은 크레아티닌 중심의 단일 분석으로부터 기능적, 구조적, 염증성 신장 장애 신호를 한 번에 추적하는 고함유 멀티플렉스 패널에 꾸준한 전환을 반영합니다. 고소득 국가의 실험실에서는 이러한 패널을 AI 지원 플랫폼에서 자동화하고 실시간으로 분석 드리프트에 플래그를 지정하여 보다 신속한 임상 판단과 재검사율을 줄일 수 있습니다. 또한 실시간으로 eGFR을 추정할 수 있는 디지털 웨어러블은 지역 스크리닝 프로그램과 재택 모니터링을 위한 길을 열고 있습니다. 기술적인 진보에도 불구하고, 새롭게 인가된 바이오마커에 대한 상환은 여전히 일관되지 않고, 또한 통일된 기준 표준이 없기 때문에 실험실 간 결과의 비교가 늦어지고, 진단 프로토콜에서 측정되었지만 확실한 진화를 이루게 됩니다.

세계 신장 바이오마커 시장 동향과 통찰

만성 신장 질환(CKD)과 급성 신장 장애(AKI)의 유병률 상승

CKD는 미국의 성인 3,700만 명이 앓고 있으며, 그 유병률은 2030년까지 30세 이상의 17%를 보일 것으로 예측되고 있습니다. 의료 시스템이 스크리닝을 신장 내과 클리닉에서 1차 진료 워크플로우로 전환함에 따라 검사량은 구조적으로 급증합니다. CKD 환자의 최대 90%는 진행될 때까지 진단되지 않은 채로 남아 있어 치료비와 투석 의존도를 높이고 있습니다. 따라서 지불자는 eGFR이 떨어지기 전에 부상을 인지하는 종합적인 바이오마커 패널을 권장합니다. 현재는 크레아티닌과 시스타틴 C, NGAL, 요중 알부민을 조합하여 위험을 층별화하고, 치료 강도를 도모하고, 기능적이고 발현량이 높은 단백질에 대한 지속적인 수요를 지지하고 있습니다. 미국과 독일의 포퓰레이션 헬스 계약은 입원 감소로 인한 비용 상쇄를 증명하는 여러 분석 패널에 환불을 실시하는 것으로, 신장 바이오마커 검사는 확정적인 것이 아니라 예방적인 툴이 되고 있습니다. 신흥 시장의 정부는 이러한 성과를 주시하고 있으며, 세계적인 보급의 기세에는 긴 길이 있다는 것을 시사하고 있습니다.

당뇨병·고혈압 인구 증가

당뇨병과 고혈압은 세계 말기 신장병 환자 소개의 60% 이상을 차지하고 있으며, KDIGO의 2024년 가이드라인에서는 고위험 당뇨병 환자에게는 연 1회 신장 바이오마커 검사가 아니라 분기에 1회 신장 바이오마커 검사를 지시하고 있습니다. 임상 실험실은 알부민/크레아티닌 비율, 혈청 크레아티닌, 시스타틴 C, NGAL을 가치 기반 지불 지표에 적합한 하나의 주문 가능한 코드로 번들로 지원합니다. SGLT2 억제제는 복용량 조절이 조기 eGFR의 변화에 의존하기 때문에 치료적 인센티브를 추가하여 정확하고 빈번한 바이오마커 측정에 대한 임상의의 신뢰를 높입니다. 아시아태평양은 2형 당뇨병의 이환율이 가장 급상승하고 있기 때문에 중국과 인도의 부처는 손가락을 찌르는 크레아티닌과 포인트 오브 케어의 NGAL 카트리지를 사용하는 지역 스크리닝 차량에 자금을 제공하고 있으며 신장 바이오마커 시장이 만성 질환 관리 경로에 통합됨을 보여줍니다.

실험실 간에 통일된 기준 표준의 부족

NGAL, KIM-1, penKid는 아직 통일된 검량선이 없기 때문에 검사실 간의 변동 계수가 18%를 초과할 수 있으며 의사의 신뢰를 손상시키지 않고 가이드라인의 승인을 지연시킵니다. 국제임상화학연합은 시스타틴 C에 대해서는 세계적인 기준계를 소집하고 있지만, 요세관 장애 단백질에 대해서는 동등한 워크스트림은 자금 부족으로 기술적으로도 복잡하게 남아 있습니다. 브라질과 나이지리아의 조달 팀은 플랫폼이 다른 절대값을 보고하기 때문에 분석 선택이 마비되었다고 보고합니다. 일본과 캐나다의 학술 컨소시엄은 바이오뱅크를 풀어 민족 고유의 기준 간격을 확립하려고 하고 있지만, IDMS 트레이서블인 크레아티닌의 성공과 같은 인증 체계가 생길 때까지 신규 바이오마커의 전개는 아직 단편적인 것에 그치는 것으로 보입니다.

부문 분석

기능성 바이오마커는 2024년 8억 4,000만 달러를 창출해 신장 바이오마커 시장의 52.32%에 해당합니다. 크레아티닌은 여전히 eGFR 산출을 위한 유비쿼터스한 바이오마커이지만, 조기 상해에 있어서의 맹점이기 때문에 임상의사는 소아나 노인에게 있어서 보다 넓은 다이나믹 레인지로 정밀도를 향상시키는 혈청 시스타틴 C와 페어로 사용하는 경우가 많습니다. 알부민 소변의 스크리닝 양은 기능 블록에서 가장 빠르게 증가하고 있는데, 이는 당뇨병 치료 경로가 마이크로 알부민의 결과를 치료 강화에 연결하기 때문입니다. 이 부문은 비색 알부민의 변화를 촬영하고 클라우드 대시보드에 데이터를 중계하는 스마트폰 대응의 딥틱에 의해 아시아와 아프리카의 농촌에서의 액세스가 확대되고 더욱 증가하고 있습니다.

상향조절 단백질은 CAGR 8.31%로 상승하고 다른 모든 카테고리를 초과할 것으로 예측됩니다. NGAL은 이환 후 2시간 후에 검출할 수 있기 때문에 각광을 받고 있습니다. 독일의 응급실에서는 혈장 NGAL을 패혈증 패널에 추가하여 크레아티닌보다 빨리 임박한 신장 장애에 플래그를 지정합니다. 2025년에 승인된 KIM-1 분석은 암 임상시험에서 약물유발성 신독성 감시를 위해 CRO로부터의 추가 주문이 기대됩니다. 가이드라인 위원회가 예상대로 적응을 확대할 경우, 2030년까지 상향조절 단백질 시장 규모는 4억 9,000만 달러에 달할 수 있으며, 이 분야가 시장 전체의 성장에 있어서 가속기의 역할을 한다는 것을 뒷받침합니다.

지역 분석

북미는 2024년 매출의 42.23%를 차지했으며 신장 바이오마커 시장 규모의 6억 8,000만 달러에 해당합니다. 이는 견고한 실험실 자동화, FDA의 명확한 패스웨이, 증거가 되는 임계값을 충족하는 신규 검사에 대한 보험사의 상환 의욕에 뒷받침됩니다. 메디케어의 Merit-based Incentive Payment System은 신장 내과의 진료 점수와 연간 알부민 요율을 연결하여 프로토콜의 갱신과 검사 주문 빈도의 향상을 촉진하고 있습니다. 미국 벤더는 신속한 임상시험 등록을 위해 대학의료센터에 대한 근접성을 활용하여 바이오마커의 검증주기를 단축하고, 이 지역을 시장 출시의 최전선에 자리잡고 있습니다.

아시아태평양은 CAGR 8.64%의 성장 엔진이며, 중국, 인도, 한국은 CKD 조기 발견을 조성하기 위해 공적 의료 의무와 현금백 보험 제도를 조합하고 있습니다. 중국의 지방정부는 주요 체외 진단용 의약품 제조업체와 제휴해, 혈청 크레아티닌과 NGAL를 검사하는 이동 실험실을 공장의 진료소에 배치하고 있어, 이 모델은 2027년까지 100 유닛까지 확대할 것으로 예상되고 있습니다. 인도에서는 Ayushman Bharat 보험 패키지가 당뇨병 계약자에 대해 연 2회의 알부민 크레아티닌 비율 검사를 보상해 2급 도시에서 검사 건수의 급증을 견인하고 있습니다. 이러한 정책은 검사 단가를 낮추는 시약의 현지 생산과 함께 이 지역 신장 바이오마커 시장의 지속적인 확대를 확보하고 있습니다.

유럽은 증거 기반 정책 틀에 힘입어 한 자리 대 중반의 안정적인 수익 성장을 보여줍니다. 독일 IQWiG는 크레아티닌 단독보다 CKD 병기 분류 재분류가 12% 개선된다는 메타 분석 결과를 받았으며 2025년 시스타틴 C 상환을 승인했습니다. 영국의 NICE는 6개의 NHS 트러스트로 NGAL과 KIM-1을 결합한 패널을 시험적으로 도입하고 있으며, 초기 의료 경제 모델링에서는 투석 연기로 인한 절약이 24개월 이내에 검사 비용을 상쇄할 것을 시사하고 있습니다. 스웨덴의 신흥 기업은 현재 스마트 링의 eGFR 측정을 전자 의료 기록에 통합하여 바이오 마커 데이터가 소비자 장비와 임상 의사 결정 지원 간에 원활하게 반복되도록합니다. 전반적으로, 비용 효과에 대한 유럽의 경계심은 큰 프레임의 성장을 억제하고, 검증된 분석의 장기적인 채택을 확고하게 하고, 신장 바이오마커 시장의 27%의 점유율을 유지하고 있습니다..

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 신장 질환(CKD)과 급성 신장 장애(AKI)의 유병률 상승

- 당뇨병 및 고혈압 인구 증가

- 신장병 실험실에서 높은 처리량 다중 분석의 급속한 보급

- 정부의 CKD 스크리닝 의무

- 초조기 발견을 위한 AI 대응 요중 단백질체학

- 실시간 eGFR을 생성하는 디지털 웨어러블의 통합

- 시장 성장 억제요인

- 검사실간의 보편적인 표준물질의 부족

- 신규 바이오마커에 대한 엄격한 상환 장애물

- 포인트 오브 케어 설정에서의 분석 전 검체의 편차

- 소수 민족 집단의 제한된 검증 데이터

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 바이오마커 유형별

- 기능적 바이오마커

- 혈청 크레아티닌

- 혈청 시스타틴 C

- 소변 알부민

- 상향 조절 단백질

- NGAL

- 신장 장애 분자-1

- Interleukin-18

- 기타 바이오마커

- 기능적 바이오마커

- 진단 기술별

- 효소 결합 면역흡착 측정법(ELISA)

- 입자 증강 비탁 면역 측정법(PETIA)

- 비색 측정

- 화학발광 면역측정법(CLIA)

- 액체 크로마토그래피 질량분석(LC-MS)

- 기타

- 최종 사용자별

- 병원

- 진단 실험실

- 학술기관 및 연구기관

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- F.-Hoffmann-La Roche AG

- Thermo Fisher Scientific Inc.

- Siemens Healthineers AG

- BioPorto Diagnostics A/S

- SEKISUI Medical Co., Ltd.

- BioMerieux SA

- SphingoTec GmbH

- Randox Laboratories Ltd

- Enzo Life Sciences Inc.

- Beckman Coulter Inc.

- QIAGEN NV

- DiaSorin SpA

- Becton, Dickinson & Co.

- Bio-Rad Laboratories Inc.

- EKF Diagnostics Holdings plc

- Proteomics International Labs Ltd

- Arkray Inc.

- Sysmex Corporation

- Danaher Corp.(Cepheid)

제7장 시장 기회와 장래의 전망

SHW 25.11.13The renal biomarkers market is valued at USD 1.61 billion in 2025 and is forecast to climb to USD 2.32 billion by 2030, registering a 7.58% CAGR through the period.

This expansion reflects a steady pivot from single-analyte, creatinine-centric testing toward high-content multiplex panels that track functional, structural and inflammatory kidney injury signals in one run. Laboratories in high-income countries are automating these panels on AI-enabled platforms that flag assay drift in real time, allowing faster clinical decisions and lower repeat-test rates. Broader adoption is further propelled by value-based reimbursement schemes that reward early CKD detection, while digital wearables capable of estimating real-time eGFR are opening a path for community screening programs and home-based monitoring. Despite technical advances, reimbursement for newly cleared biomarkers remains inconsistent and a lack of harmonized reference standards slows cross-lab result comparability, creating a measured but unmistakable evolution in diagnostic protocols.

Global Renal Biomarkers Market Trends and Insights

Rising Prevalence of Chronic Kidney Disease (CKD) & Acute Kidney Injury (AKI)

CKD affects 37 million U.S. adults and prevalence is projected to reach 17% among people aged 30 and older by 2030, driving a structural jump in test volumes as health systems move screening from nephrology clinics into primary care workflows . Up to 90% of CKD cases remain undiagnosed until advanced stages, inflating treatment costs and dialysis dependence; payers therefore endorse comprehensive biomarker panels that flag injury before eGFR declines. Clinical pathways now combine creatinine with cystatin C, NGAL and urinary albumin to stratify risk and chart therapy intensity, supporting sustained demand for functional and up-regulated proteins. Population health contracts in the United States and Germany reimburse multi-analyte panels that demonstrate cost offsets from reduced hospitalization, turning renal biomarker testing into a preventive rather than confirmatory tool. Emerging-market governments are watching these outcomes closely, suggesting a long runway for global adoption momentum.

Growing Diabetic & Hypertensive Population Base

Diabetes and hypertension account for more than 60% of end-stage kidney disease referrals worldwide, and KDIGO's 2024 guideline now directs quarterly renal biomarker testing for high-risk diabetics, not yearly reviews. Clinical laboratories are responding by bundling albumin-to-creatinine ratio, serum creatinine, cystatin C and NGAL in one orderable code that suits value-based payment metrics. SGLT2 inhibitors have added a therapeutic incentive because their dose adjustments hinge on early eGFR changes, raising clinician reliance on precise, high-frequency biomarker readings. Asia-Pacific faces the steepest uptick in type 2 diabetes incidence, so ministries in China and India are funding community screening vans that use finger-stick creatinine plus point-of-care NGAL cartridges, signaling the renal biomarkers market will embed itself in chronic-disease management pathways.

Lack of Universal Reference Standards Across Laboratories

NGAL, KIM-1 and penKid still lack harmonized calibrators, so inter-laboratory coefficient of variation can exceed 18%, undermining physician confidence and delaying guideline endorsement. While the International Federation of Clinical Chemistry has convened a global reference system for cystatin C, comparable workstreams for tubular injury proteins remain underfunded and technically complex. Emerging markets feel the impact most: procurement teams in Brazil and Nigeria report assay selection paralysis because platforms report different absolute values. Academic consortia in Japan and Canada are pooling biobanks to establish ethnicity-specific reference intervals, but until a certification scheme mirrors the success of IDMS-traceable creatinine, novel biomarker roll-outs will stay patchy.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of High-Throughput Multiplex Assays in Nephrology Labs

- Government CKD Screening Mandates

- Stringent Reimbursement Hurdles for Novel Biomarkers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Functional biomarkers generated USD 0.84 billion in 2024, equal to 52.32% of the renal biomarkers market. Creatinine remains ubiquitous for eGFR calculation, yet its blind spot in early injury means clinicians frequently pair it with serum cystatin C, whose broader dynamic range improves accuracy in pediatrics and the elderly. Albuminuria screening volumes are rising fastest within the functional block because diabetic care pathways link microalbumin results to therapy intensification. The segment is gaining incremental lift from smartphone-enabled dipsticks that photograph colorimetric albumin changes and relay data to cloud dashboards, widening access in rural Asia and Africa.

Up-regulated proteins are forecasted to climb at an 8.31% CAGR, outpacing all other categories. NGAL grabs the spotlight owing to its 2-hour post-insult detection window; emergency departments in Germany now add plasma NGAL to their sepsis panels to flag impending renal injury earlier than creatinine . KIM-1 assays approved in 2025 for drug-induced nephrotoxicity surveillance in oncology trials are expected to pull incremental orders from CROs. The renal biomarkers market size for up-regulated proteins could hit USD 0.49 billion by 2030 if guideline committees broaden indications as anticipated, underlining the segment's accelerator role in overall market growth.

The Renal Biomarkers Market is Segmented by Biomarker Type (Functional Biomarker [Serum Creatinine and More], Up-Regulated Protein, Other Biomarker Types), Diagnostic Technique (Enzyme-Linked Immunosorbent Assay (ELISA), and More), End User (Hospitals, Diagnostic Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 42.23% revenue in 2024, equal to USD 0.68 billion of the renal biomarkers market size, underpinned by robust laboratory automation, clear FDA pathways and insurer willingness to reimburse novel tests that meet evidentiary thresholds. Medicare's Merit-based Incentive Payment System links nephrology practice scores to annual albuminuria rates, sparking protocol updates and higher test ordering frequency. U.S. vendors leverage proximity to academic medical centers for rapid clinical trial enrollment, shortening biomarker validation cycles and keeping the region at the forefront of first-to-market launches.

Asia-Pacific is the growth engine at 8.64% CAGR, with China, India and South Korea combining public health mandates and cashback insurance schemes to subsidize early CKD detection. Provincial governments in China partnered with leading IVD firms to deploy mobile labs testing serum creatinine and NGAL in factory clinics, a model expected to scale to 100 units by 2027. In India, Ayushman Bharat insurance packages now remunerate albumin-to-creatinine ratio tests twice yearly for diabetic policyholders, driving steep volume increases in tier-2 cities. This policy pull, coupled with local reagent manufacturing that trims cost per test, secures enduring lift for the renal biomarkers market in the region.

Europe contributes stable, mid-single-digit revenue growth anchored in evidence-based policy frameworks. Germany's IQWiG approved cystatin C reimbursement in 2025 following a meta-analysis that demonstrated 12% reclassification improvement in CKD staging over creatinine alone. The United Kingdom's NICE is piloting a combined NGAL and KIM-1 panel in six NHS trusts, with early health-economic modeling suggesting dialysis deferral savings offset assay costs within 24 months. Scandinavian countries remain early adopters of digital health; Swedish startups now integrate eGFR readings from smart rings into electronic medical records, ensuring biomarker data loop seamlessly between consumer devices and clinical decision support. Collectively, European vigilance for cost-effectiveness tempers headline growth but cements long-term adoption of validated assays, maintaining a 27% slice of the renal biomarkers market.

- Abbott Laboratories

- F.-Hoffmann-La Roche AG

- Thermo Fisher Scientific

- Siemens Healthineers

- BioPorto Diagnostics A/S

- SEKISUI Medical Co., Ltd.

- bioMerieux

- SphingoTec GmbH

- Randox Laboratories

- Enzo Biochem

- Beckton Dickinson

- QIAGEN

- DiaSorin

- Beckton Dickinson

- Bio-Rad Laboratories

- EKF Diagnostics Holdings plc

- Proteomics International Labs Ltd

- Arkray

- Sysmex

- Danaher Corp. (Cepheid)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Kidney Disease (CKD) & Acute Kidney Injury (AKI)

- 4.2.2 Growing Diabetic & Hypertensive Population Base

- 4.2.3 Rapid Adoption of High-Throughput Multiplex Assays in Nephrology Labs

- 4.2.4 Government CKD Screening Mandates

- 4.2.5 AI-Enabled Urinary Proteomics for Ultra-Early Detection

- 4.2.6 Integration of Digital Wearables Generating Real-Time eGFR

- 4.3 Market Restraints

- 4.3.1 Lack Of Universal Reference Standards Across Laboratories

- 4.3.2 Stringent Reimbursement Hurdles for Novel Biomarkers

- 4.3.3 Pre-Analytical Sample Variability in Point-Of-Care Settings

- 4.3.4 Limited Validation Data in Minority Ethnic Populations

- 4.4 Regulatory Landscape

- 4.5 Porters Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Biomarker Type

- 5.1.1 Functional Biomarkers

- 5.1.1.1 Serum Creatinine

- 5.1.1.2 Serum Cystatin C

- 5.1.1.3 Urine Albumin

- 5.1.2 Up-regulated Proteins

- 5.1.2.1 NGAL

- 5.1.2.2 Kidney Injury Molecule-1

- 5.1.2.3 Interleukin-18

- 5.1.3 Other Biomarker Types

- 5.1.1 Functional Biomarkers

- 5.2 By Diagnostic Technique

- 5.2.1 Enzyme-Linked Immunosorbent Assay (ELISA)

- 5.2.2 Particle-Enhanced Turbidimetric Immunoassay (PETIA)

- 5.2.3 Colorimetric Assay

- 5.2.4 Chemiluminescent Immunoassay (CLIA)

- 5.2.5 Liquid Chromatography-Mass Spectrometry (LC-MS)

- 5.2.6 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Laboratories

- 5.3.3 Academic & Research Institutes

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F.-Hoffmann-La Roche AG

- 6.3.3 Thermo Fisher Scientific Inc.

- 6.3.4 Siemens Healthineers AG

- 6.3.5 BioPorto Diagnostics A/S

- 6.3.6 SEKISUI Medical Co., Ltd.

- 6.3.7 BioMerieux SA

- 6.3.8 SphingoTec GmbH

- 6.3.9 Randox Laboratories Ltd

- 6.3.10 Enzo Life Sciences Inc.

- 6.3.11 Beckman Coulter Inc.

- 6.3.12 QIAGEN N.V.

- 6.3.13 DiaSorin S.p.A.

- 6.3.14 Becton, Dickinson & Co.

- 6.3.15 Bio-Rad Laboratories Inc.

- 6.3.16 EKF Diagnostics Holdings plc

- 6.3.17 Proteomics International Labs Ltd

- 6.3.18 Arkray Inc.

- 6.3.19 Sysmex Corporation

- 6.3.20 Danaher Corp. (Cepheid)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment