|

시장보고서

상품코드

1851484

보안 분석 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Security Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

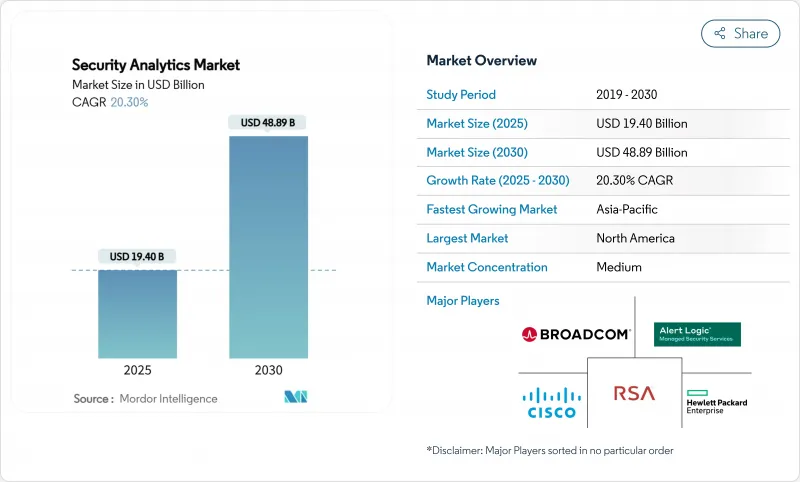

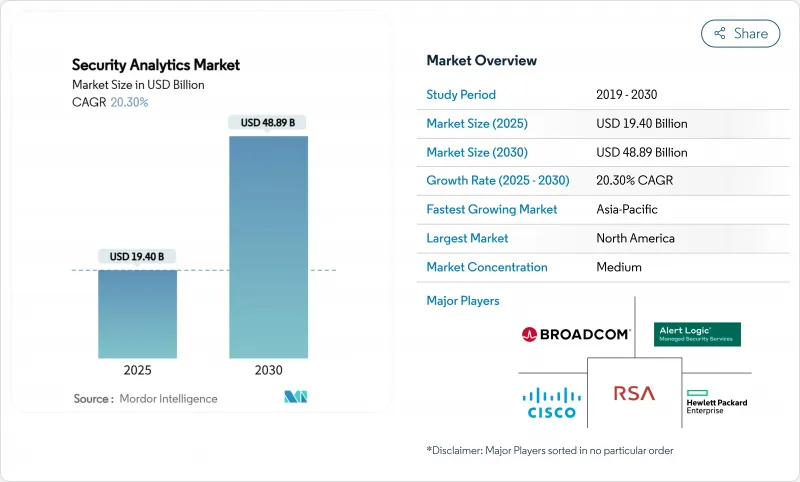

보안 분석 시장의 2025년 시장 규모는 194억 달러, 2030년에는 488억 9,000만 달러에 이르고, CAGR 20.30%를 보일 것으로 예측됩니다.

이 급성장은 수십억 개의 이벤트를 실시간으로 분석하는 AI 주도 플랫폼을 통해 고급 사이버 공격을 무력화하려는 기업의 움직임을 반영합니다. 성장의 배경으로는 IoT 엔드포인트의 폭발적 증가, 클라우드 우선 변혁 프로젝트, 자동 분석이 필요한 컴플라이언스 규제 강화가 포함됩니다. 선도적인 공급업체는 현재 SIEM, SOAR, UEBA, 위협 인텔리전스를 단일 제품군으로 통합하여 운영을 간소화하고 도구 난립에 대처하고 있습니다. CrowdStrike, Palo Alto Networks, Microsoft, IBM, Cisco는 애널리틱스의 폭, 속도, 네이티브 자동화로 적극적으로 경쟁하며, 틈새 전문 기업은 차별화된 AI 모델과 클라우드 네이티브 아키텍처에서 견인력을 유지하고 있습니다.

세계 보안 분석 시장 동향과 통찰

사이버 위협의 고도화

국가 주체는 현재 서명 기반 방어를 피하는 자동화된 툴체인을 개발하고 있으며, 기업은 수평 움직임과 제로 데이 익스플로잇을 감지하는 행동 분석으로 향하고 있습니다. FBI는 감시와 데이터 유출을 목적으로 하는 통신사업자에 대한 국가 주도의 공격이 급증하고 있음을 꼽고 있습니다. 따라서 보안 팀은 네트워크 기준선을 자체 학습하고 밀리초 단위로 비정상적인 경로를 표시하는 머신러닝 모델을 갖춘 플랫폼을 선호하고 사용합니다. 공급업체는 UEBA와 위협 인텔의 피드를 SIEM 엔진에 직접 통합하여 체류 시간을 단축하고 평균 감지 시간을 향상시킵니다. 이 군 경쟁은 수작업으로 피처 엔지니어링 없이 모델을 지속적으로 재교육할 수 있는 공급업체에게 보상을 받고 있습니다.

IoT 및 BYOD 엔드포인트의 폭발적 증가

산업용 센서, 의료기기, 리모트 워크용 노트북이 공격 대상 영역을 확대하여 경계 제어가 효과가 없어지고 있습니다. Scientific Reports 잡지의 조사에 따르면 60% 이상의 조직이 관리되지 않는 장치와 관련된 내부 위협을 받고 있음을 알 수 있습니다. 최신 분석에서는 OT 게이트웨이, 모바일 EDR 에이전트 및 에지 노드에서 원격 측정을 수집하고 교사 없는 학습을 적용하여 장치의 동작을 분류합니다. 에지 처리는 대기 시간을 줄이고 연결성이 떨어지더라도 작동을 계속합니다. 공급업체는 현재 경량 에이전트를 펌웨어에 통합하고 클라우드 측 그래프 분석과 결합하여 수백만 대의 엔드포인트의 전체 함대 이상을 상관시키고 있습니다.

데이터 통합 및 도구 난립 문제

대부분의 기업은 25-50개의 보안 도구를 다루고 있으며, 이로 인해 사용자 정의 파서를 사용하지 않아도 상관관계가 느려지고 있습니다. CSO Online은 통합 오버헤드가 분석가의 능력을 소모하고 크로스 벡터 공격을 보이지 않는다고 보고합니다. 구매자는 포인트 솔루션을 통합 애널리틱스 제품군으로 대체하고 있지만, 공급업체의 잠금을 두려워하고 대체 프로젝트가 지연되고 있습니다. 클라우드로의 전환이 복잡해짐에 따라 플랫폼은 On-Premise Syslog, 클라우드 API 메타데이터, SaaS 감사 추적을 단일 데이터 레이크 내에서 정규화해야 하며, 그렇지 않으면 사일로화를 지속할 위험이 있습니다.

부문 분석

네트워크 보안 분석은 2024년 수익의 38%를 차지했으며 보안 분석 시장에서 딥 패킷 검사와 NetFlow 분석의 지속적인 역할을 명확히 했습니다. 클라우드의 보안 분석은 기업이 워크로드를 오프프레미스로 전환하고 크로스 클라우드 가시성을 요구하기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 17.6%로 성장할 것으로 예상됩니다. 용도, 웹 및 엔드포인트 분석이 통합되어 감지 범위를 확장하는 반면, 내부 위협 모듈은 UEBA를 사용하여 사용자 행동을 프로파일링합니다.

이러한 하위 부문이 융합되면 공급업체는 다양한 원격 측정을 통합 데이터 패브릭에 통합하는 마이크로서비스 기반 컬렉터를 통합해야 합니다. AI 주도 정책 권고와 자동 복구를 제공하는 플랫폼은 레거시 규칙 엔진과 비교하여 오감지를 59% 줄일 수 있습니다. 따라서 통합 제품군은 하나의 콘솔에서 네트워크, 용도 및 신원 레이어를 보호하면서 경보 노이즈를 줄이려는 보안 리더에게 매력적입니다.

On-Premise 구현은 2024년 매출의 54.5%를 차지하며 방화벽 내에 기밀 로그를 유지하기 위한 투자 및 소블린 데이터 규칙을 반영합니다. 하지만 클라우드 구축의 보안 분석 시장 규모는 기업이 SASE와 제로 트러스트 지침을 채택함에 따라 2030년까지 21%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 하이브리드 모델은 보안 클라우드에서 버스트 분석을 수행하면서 중요한 로그가 로컬에 남아 있다는 실용적인 교량 역할로 부상하고 있습니다.

미국 국방부의 제로 트러스트 아키텍처 2.0은 2027년까지 완전히 커버하는 것을 목표로 하며 확장성을 위해 상용 클라우드 분석을 활용합니다. 소비 기반 라이선싱과 관리되는 캡처 파이프라인은 자본 지출 장애물을 제거하고 규제 산업조차도 계산 집약적인 상관 작업을 오프로드하도록 유도합니다. 업체들은 분석 깊이를 유지하면서도 데이터 거주 규제를 준수하기 위해 지역별 클라우드 ‘셀’을 배치합니다.

지역별 분석

북미는 2024년 매출액의 42%를 차지했으며 대규모 사이버 예산과 AI 강화형 SIEM의 조기 도입으로 혜택을 누립니다. 대통령령 14028과 같은 연방지령은 지속적인 진단과 정보공시를 강제하고 지출을 더욱 촉진합니다.

아시아태평양의 CAGR은 13.8%를 보일 것으로 예측되며 클라우드로의 이행, 사이버 보험 보급률의 급상승, 정부가 지원하는 디지털 프로그램 등이 뒷받침하고 있습니다. Gallagher Re에 따르면 아시아태평양의 사이버 보험료는 매년 50% 가까이 상승하고 있습니다. 호주, 싱가포르, 일본, 한국이 지출의 선두에 서 있지만, 인도와 중국이 국내 하이테크 챔피언이 세계적인 규모를 확대하는 가운데 신규 도입 건수가 가장 많아지고 있습니다.

라틴아메리카에서는 2025년을 향해 IT 예산이 64% 확대되고, 지역 전체에서 초당 평균 1,600건의 공격을 처리하는 분석을 우선시하고 있습니다. 중동과 북아프리카의 보안 지출은 석유 및 가스 및 정부 부문에서 AI 도입이 박차를 가하고 2025년 보안 예산이 30억 달러 이상에 달할 것으로 보입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 사이버 위협 상황의 고도화

- IoT와 BYOD 엔드포인트의 폭발적 성장

- 클라우드 퍼스트의 디지털 변혁 프로그램

- 세계로 확대하는 사이버 보안 준수 체제

- AI에 의한 폴리모픽 악성코드의 출현

- 관리되지 않는 머신 투 머신 ID의 급증

- 시장 성장 억제요인

- 데이터 통합과 툴 스프롤의 과제

- SOC 분석가의 세계적 부족

- 높은 경계 피로와 위양성률

- 애널리틱스를 제한하는 데이터 주권 규칙

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용도별

- 네트워크 보안 분석

- 용도 보안 분석

- 웹 보안 분석

- 엔드포인트 보안 분석

- 클라우드 보안 분석

- 내부자 위협 분석

- 전개 모드별

- On-Premise

- 클라우드

- 하이브리드

- 조직 규모별

- 대기업

- 중소기업

- 최종 사용자 업계별

- 은행 및 금융 서비스

- 헬스케어

- 방위·안전 보장

- 통신 및 IT

- 소매 및 전자상거래

- 제조업

- 정부기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Alert Logic, Inc.

- Arbor Networks, Inc.(NETSCOUT Systems, Inc.)

- Broadcom Inc.(Symantec Enterprise Division)

- Cisco Systems, Inc.

- RSA Security LLC

- Hewlett Packard Enterprise Company

- International Business Machines Corporation

- LogRhythm, Inc.

- Mandiant, Inc.

- Splunk Inc.

- Fortinet, Inc.

- McAfee, LLC

- Micro Focus International plc

- Securonix, Inc.

- Exabeam, Inc.

- Devo Technology, Inc.

- Microsoft Corporation

- Palo Alto Networks, Inc.

- CrowdStrike Holdings, Inc.

- Elastic NV

제7장 시장 기회와 장래의 전망

SHW 25.11.13The security analytics market is valued at USD 19.40 billion in 2025 and is forecast to touch USD 48.89 billion by 2030, advancing at a CAGR of 20.30%.

The surge reflects enterprises' drive to neutralize sophisticated cyber-attacks with AI-led platforms that analyze billions of events in real time. Growth stems from an explosion of IoT endpoints, cloud-first transformation projects, and tightening compliance regimes that require automated analytics. Demand is further amplified by platform consolidation: large vendors now bundle SIEM, SOAR, UEBA, and threat-intelligence into single suites to simplify operations and counter tool sprawl. CrowdStrike, Palo Alto Networks, Microsoft, IBM, and Cisco compete aggressively on analytics breadth, speed, and native automation while niche specialists maintain traction through differentiated AI models and cloud-native architectures.

Global Security Analytics Market Trends and Insights

Sophistication of cyber-threat landscape

Nation-state actors now deploy automated toolchains that evade signature-based defenses, pushing enterprises toward behavioral analytics that detect lateral movement and zero-day exploits. The FBI cited a spike in state-sponsored attacks on telecom carriers aimed at surveillance and data exfiltration. Security teams therefore favor platforms with machine-learning models that self-learn network baselines and flag anomalous paths in milliseconds. Vendors integrate UEBA and threat-intel feeds directly into SIEM engines, shrinking dwell time and improving mean time to detect. This arms race rewards suppliers able to retrain models continuously without manual feature engineering.

Explosive growth of IoT and BYOD endpoints

Industrial sensors, medical devices, and remote-work laptops have swollen the attack surface, leaving perimeter controls ineffective. Research in Scientific Reports found that more than 60% of organizations suffered insider threats tied to unmanaged devices. Modern analytics ingest telemetry from OT gateways, mobile EDR agents, and edge nodes, applying unsupervised learning to classify device behaviors. Edge processing cuts latency and keeps operations running when connectivity drops. Vendors now embed lightweight agents in firmware and combine them with cloud-side graph analytics to correlate anomalies across fleets of millions of endpoints.

Data-integration and tool-sprawl challenges

Most enterprises juggle 25-50 security tools that emit disjointed log schemas, forcing custom parsers and delaying correlation. CSO Online reports that integration overhead drains analyst capacity and obscures cross-vector attacks. Buyers are replacing point solutions with converged analytics suites, yet fear of vendor lock-in slows rip-and-replace projects. As cloud migration compounds complexity, platforms must normalize on-prem Syslog, cloud API metadata, and SaaS audit trails within a single data lake, or risk perpetuating silos.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-first digital-transformation programs

- Expanding global cybersecurity-compliance regimes

- Global shortage of SOC analysts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Network security analytics generated 38% of 2024 revenue, underscoring the enduring role of deep-packet inspection and NetFlow analysis in the security analytics market. Cloud security analytics is advancing at 17.6% CAGR to 2030 as enterprises shift workloads off-premises and seek cross-cloud visibility. Application, web, and endpoint analytics together broaden detection coverage, while insider-threat modules employ UEBA to profile user behavior.

The convergence of these sub-segments pushes vendors to embed microservices-based collectors that ingest diverse telemetry into unified data fabrics. Platforms offering AI-driven policy recommendations and automated remediation now achieve a 59% drop in false positives versus legacy rule engines. Integrated suites therefore appeal to security leaders aiming to slash alert noise while protecting network, application, and identity layers in one console.

On-premise implementations held 54.5% revenue in 2024, reflecting sunk investments and sovereign-data rules that keep sensitive logs inside firewalls. Yet the security analytics market size for cloud deployments is forecast to expand at a 21% CAGR through 2030 as firms adopt SASE and zero-trust mandates. Hybrid models are emerging as a pragmatic bridge-critical logs remain local while burst analysis occurs in secure clouds.

The U.S. Department of Defense's Zero Trust Architecture 2.0 targets full coverage by 2027, leaning on commercial cloud analytics for scalability. Consumption-based licensing and managed ingestion pipelines erase capital expenditure hurdles, enticing even regulated industries to offload compute-intensive correlation tasks. Vendors also deploy regional cloud "cells" to meet data-residency directives without sacrificing analytic depth.

The Security Analytics Market Report is Segmented by Application (Network Security Analytics, Application Security Analytics, and More), Deployment Mode (On-Premise, Cloud, Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (Banking and Financial Services, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 42% revenue in 2024, benefitting from sizable cyber-budgets and early uptake of AI-enhanced SIEM. Federal directives such as Executive Order 14028 force continuous diagnostics and disclosure, further fueling spend.

Asia-Pacific is projected to grow at 13.8% CAGR, propelled by cloud migrations, cyber-insurance penetration jumps, and government-backed digital programs. Gallagher Re reports Asia-Pacific cyber-insurance premiums climbing nearly 50% annually. Australia, Singapore, Japan, and South Korea spearhead spending, yet India and China add the largest volume of new deployments as domestic tech champions scale globally.

Latin America eyes 64% IT-budget expansion for 2025, prioritizing analytics that handle a region-wide average of 1,600 attacks per second. EMEA growth remains steady; Europe leans on GDPR and the forthcoming Cyber Resilience Act, while Middle East and North Africa security outlays are set to exceed USD 3 billion in 2025, spurred by AI adoption in oil, gas, and government sectors.

- Alert Logic, Inc.

- Arbor Networks, Inc. (NETSCOUT Systems, Inc.)

- Broadcom Inc. (Symantec Enterprise Division)

- Cisco Systems, Inc.

- RSA Security LLC

- Hewlett Packard Enterprise Company

- International Business Machines Corporation

- LogRhythm, Inc.

- Mandiant, Inc.

- Splunk Inc.

- Fortinet, Inc.

- McAfee, LLC

- Micro Focus International plc

- Securonix, Inc.

- Exabeam, Inc.

- Devo Technology, Inc.

- Microsoft Corporation

- Palo Alto Networks, Inc.

- CrowdStrike Holdings, Inc.

- Elastic N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sophistication of cyber-threat landscape

- 4.2.2 Explosive growth of IoT and BYOD endpoints

- 4.2.3 Cloud-first digital-transformation programs

- 4.2.4 Expanding global cybersecurity-compliance regimes

- 4.2.5 AI-driven polymorphic malware emergence

- 4.2.6 Surge in unmanaged machine-to-machine identities

- 4.3 Market Restraints

- 4.3.1 Data-integration and tool-sprawl challenges

- 4.3.2 Global shortage of SOC analysts

- 4.3.3 High alert-fatigue and false-positive rates

- 4.3.4 Data-sovereignty rules restricting analytics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter?s Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Application

- 5.1.1 Network Security Analytics

- 5.1.2 Application Security Analytics

- 5.1.3 Web Security Analytics

- 5.1.4 Endpoint Security Analytics

- 5.1.5 Cloud Security Analytics

- 5.1.6 Insider Threat Analytics

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 Banking and Financial Services

- 5.4.2 Healthcare

- 5.4.3 Defense and Security

- 5.4.4 Telecom and IT

- 5.4.5 Retail and E-Commerce

- 5.4.6 Manufacturing

- 5.4.7 Government

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alert Logic, Inc.

- 6.4.2 Arbor Networks, Inc. (NETSCOUT Systems, Inc.)

- 6.4.3 Broadcom Inc. (Symantec Enterprise Division)

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 RSA Security LLC

- 6.4.6 Hewlett Packard Enterprise Company

- 6.4.7 International Business Machines Corporation

- 6.4.8 LogRhythm, Inc.

- 6.4.9 Mandiant, Inc.

- 6.4.10 Splunk Inc.

- 6.4.11 Fortinet, Inc.

- 6.4.12 McAfee, LLC

- 6.4.13 Micro Focus International plc

- 6.4.14 Securonix, Inc.

- 6.4.15 Exabeam, Inc.

- 6.4.16 Devo Technology, Inc.

- 6.4.17 Microsoft Corporation

- 6.4.18 Palo Alto Networks, Inc.

- 6.4.19 CrowdStrike Holdings, Inc.

- 6.4.20 Elastic N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment