|

시장보고서

상품코드

1851502

광학 이미징 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Optical Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

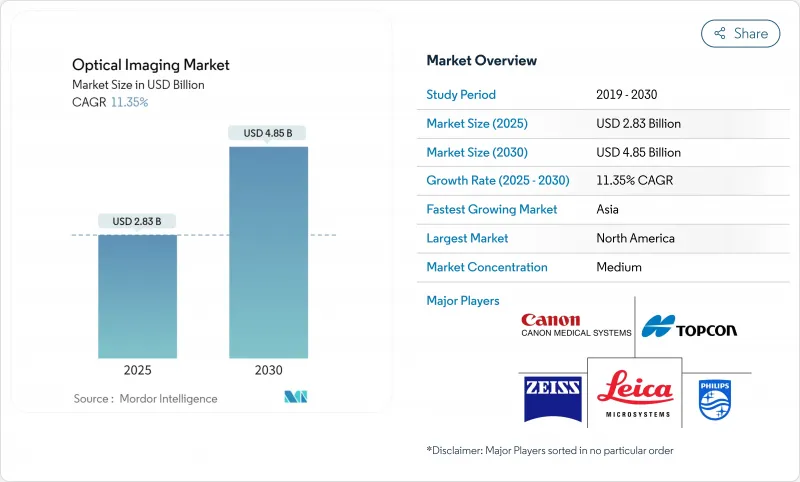

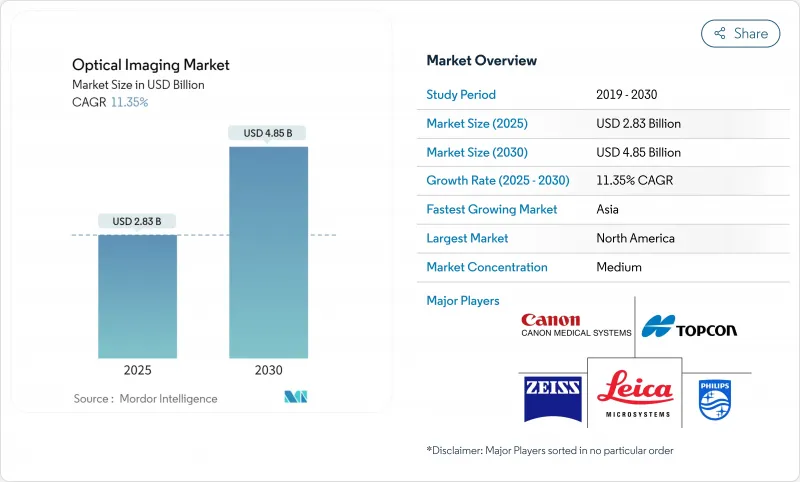

광학 이미징 시장은 2025년에 28억 3,000만 달러, 2030년에는 48억 5,000만 달러에 이르고, CAGR 11.35%를 나타낼 전망입니다.

고해상도 영상 시스템의 꾸준한 돌파구, 비침습적 진단으로의 이동, 안과, 순환기과, 종양과, 피부과, 신경과에서 사용 확대가 성장을 추진하고 있습니다. 인공지능과의 통합은 검출 정밀도와 워크플로우 속도를 향상시키고 광간섭 단층계(OCT)와 광음향 또는 하이퍼스펙트럼 툴을 통합한 멀티모달 플랫폼은 임상적 가치를 확대하고 있습니다. 반도체 공급 부족은 공급업체에 검출기 재설계 및 수직 통합 추구를 촉구하고 있지만, 업계별 시장은 병원, 외래 수술 센터(ASC), 연구소에서 탄력적인 조달 예산의 혜택을 계속 받고 있습니다. 아시아태평양에서는 당뇨병 안과 검진용 핸드헬드 OCT가 급속히 보급되고 있으며, 북미에서는 OCT 가이드 하관동맥 인터벤션에 대한 상환이 호의적으로 이루어지고 있기 때문에 확대 노선이 더욱 강화되고 있습니다.

세계의 광학 이미징 시장 동향과 인사이트

외래 수술 센터(ASC)에서 수술 중 광학 이미징 시스템 도입 가속

외래 수술 센터(ASC)는 2024년 미국에서 2,300만건 이상의 수술을 실시해 전년대비 15% 증가했습니다. UCLA Health의 Dynamic Optical Contrast Imaging 장비로 대표되는 컴팩트한 수술 중 광학 플랫폼은 실시간으로 종양 단단을 묘사하고, 처리 시간을 20% 단축하여 ASC의 처리량을 향상시키기 위해 인기를 끌고 있습니다. 이러한 시스템에 대한 설비 투자는 병원 수술에 비해 35-50%의 비용 절감이 가능하고 외래 환자 경로에 대한 보험사의 지원이 높아지고 있기 때문에 정당화되고 있습니다. 보험 상환의 변화에 의해 2030년까지 전 수술에 차지하는 ASC의 점유율은 68%가 될 것으로 예상되어, 휴대용으로 네트워크 대응의 광학 리그에 수요가 높아져, 광학 이미징 시장의 밑단이 넓어집니다.

미국과 일본의 OCT 가이드 하 PCI 상환 범위 확대

OCCUPI시험은 1년 후 OCT가이드하 PCI에서 복합 이벤트 발생률이 4.9%인 반면 혈관조영 단독에서는 9.5%였음을 보고하고 미국에서는 상환을 12% 끌어올려 일본에서는 적용 범위를 확대하는 정책 변경을 불러일으켰습니다. 프로바이더는 재수술이 22% 감소하고, 수술당 비용 증가를 상쇄하고, 고위험 관상동맥 병변에서 채용에 박차를 가했습니다. 관상동맥 인터벤션에서 OCT 이용률은 2024년 15%에서 2028년 약 35%로 상승하여 인터벤셔널 카디올로지 워크플로우에 광학 이미징이 깊게 통합될 것으로 예측됩니다.

벤치탑에서 수술실 통합형 이미징 스위트로 자본 집약적 변화

OCT, 형광 및 네비게이션을 번들로 제공하는 완벽하게 통합된 광학 제품군은 극장당 150만-250만 달러가 소요되며 벤치탑 설치의 3배에서 4배가 되며 대규모 인프라 재배선이 필요합니다. 병원은 또한 서비스 계약 및 전문가 교육을 위해 5년 동안 15-20%의 추가 소유 비용을 부담합니다. 그 결과, 2024년에 완전한 통합을 완료한 병원은 대상 병원의 23%에 불과하며, 많은 병원이 업그레이드를 지연시키고 있거나 여러 예산 주기에 걸쳐 단계적으로 모듈을 도입했습니다. 신흥국은 보다 엄격한 제약에 직면하고 있으며, 임상상의 이점은 분명하지만, 보급이 늦어지고 있습니다.

부문 분석

이미징 시스템은 안과, 순환기과, 연구 분야에서 사용되는 턴키 콘솔이 호조로 2024년 매출의 37%를 차지했습니다. 이 부문 시장 세분화는 공급업체가 콘솔에 AI 소프트웨어 및 멀티모달 애드온을 추가하여 꾸준히 확대될 것으로 예측됩니다. 낮은 침습 수술에서 실시간 지침에 대한 수요가 증가함에 따라 반도체 부족으로 인한 검출기 비용 상승으로 인해 병원 투자가 계속 유지되고 있습니다. 반면에 고속 카메라는 성능 임계값을 재정의합니다. Phantom High-Speed의 S710 카메라는 홀로그램 망막 혈류 영상으로 4,000fps를 달성하고 혈관 진단을 강화하는 정확한 도플러 계산을 가능하게 합니다. 이 기술적인 도약은 2030년까지의 CAGR이 12.5%로 예측되는 것과 일치합니다.

좁은 밴드 LED와 슈퍼 연속 레이저를 사용하는 차세대 일루미네이션 엔진은 외과 의사가 조직 특이적인 대비를 요구하는 동안 일루미네이션 시스템 분야에서 관심을 지속하고 있습니다. 한때 주변기기였던 소프트웨어 솔루션은 AI 알고리즘이 자동 세분화, 혈관 정량화, 비정상적인 플래그를 지정하기 때문에 이제 차별화의 축이 되고 있습니다. 렌즈는 여전히 필수적입니다. 비구면 광학계와 그래디언트 인덱스 광학계의 진보로 깊이 방향으로의 투과성이 향상되고, 색수차가 감소하고, 화상의 선명도가 향상되고 있습니다. TDK의 스핀 포토 검출기는 자성 소자를 사용하여 초고속으로 빛을 감지하고 기존 반도체 병목 현상을 제거하여 부품 공급망을 안정화합니다.

안과는 망막질환 관리를 위한 OCT 사용이 정착되어 있기 때문에 2024년 34.8%로 최대 슬라이스를 유지했습니다. 적응 광학 기술은 현재 광 수용체 모자이크와 융모 모세 혈관 흐름을 밝혀 황반 장애의 증상 전 감지를 가능하게 합니다. 이와 병행하여 종양학은 15.1%의 연평균 복합 성장률(CAGR)로 기세를 늘리고 있습니다. 이는 광학 이미징이 종양 절제시 마진 평가를 유도하고 치료 중 혈관 반응을 추적하기 때문입니다. 저산소 구역을 타겟으로 하는 광음향 조영제는 종양의 미세 환경을 센티미터 깊이까지 실시간으로 시각화할 수 있게 되었습니다. 그 결과, 3차 병원이 수술 중 광학 지침을 표준화함에 따라, 종양학 응용 분야의 광학 이미징 시장 점유율은 상승합니다.

심장병학이 이어집니다. : OCT 가이드에 의한 경피적 관상동맥 인터벤션은 복잡한 병변 관리에서 혈관 조영만 보다 우수하다는 것이 증명되고 있습니다. 순환기과의 광학 이미징 시장 규모는 더 많은 지불자가 보험 적용을 승인함에 따라 가속화될 것으로 예측됩니다. 피부과는 생검을 줄이고 의심스러운 병변의 치료를 개선하는 AI 대응 스펙트럼 스캐너의 혜택을 받습니다. 신경학과 치과 과학의 틈새는 작지만 혁신적입니다. 수술 중 뇌 OCT는 조직 역학을 추적하고 치과 OCT는 전리 방사선을 사용하지 않고 우식의 조기 발견에 도움이 됩니다. 제약 연구 그룹은 약물-세포 상호작용을 시각화하기 위해 라벨이 없는 절편을 채택하여 종양학의 신약 개발주기를 단축하고 있습니다.

지역 분석

북미는 2024년에 40%의 점유율을 차지하고 강력한 상환과 대학, 신흥기업, 선도기기 제조업체를 잇는 혁신 에코시스템이 그 기반이 되었습니다. 2024년 FDA가 AI 지원형 피부암 광학식 독영장치에 그린라이트를 내놓은 것으로, 전문 분야를 넘은 도입이 가속화되고, 듀크 대학의 핸드헬드 OCT 프로토타입이 POC(Point-of-Care) 안과 검사를 전진시킵니다. 이 지역의 광학 이미징 시장 규모는 보험 회사가 AI 통합 진단의 적용 범위를 확대하고 자본 예산이 하이브리드 OR 업그레이드를 타겟팅함에 따라 계속 확대될 것으로 보입니다.

아시아태평양은 가장 빠르게 성장하는 클러스터이며 CAGR은 12.4%를 나타낼 전망입니다. 중국, 인도, 일본 정부는 국내 제조에 자금을 공급하고 수입 의존도를 낮추고 지방 클리닉 업그레이드에 보조금을 내고 있습니다. 당뇨병 망막증 스크리닝에서 핸드헬드 OCT의 확산은 접근 격차를 메우고 있습니다. 하지만 초분광 영상 전문가가 부족하기 때문에 특히 인도나 동남아시아에서는 임상시험이 늦어지고 있습니다. 국경을 넘어서는 교육 파트너십은 장기적인 채용을 유지하는 인재 파이프라인을 구축하는 것을 목표로 합니다. 이러한 장애물에도 불구하고, 아시아태평양의 광학 이미징 시장은 망막 스크리닝 수요를 촉진하는 건강 관리 투자 증가와 당뇨병 유병률의 높이로부터 혜택을 받고 있습니다.

유럽은 강력한 연구 보조금과 학술 병원 네트워크에 의해 지원되는 대규모 기반을 유지하고 있습니다. 독일, 프랑스, 영국의 센터가 피부과와 신경과의 임상 검증을 이끌고 있지만, 치과용도는 단편적인 상환하에 시달리고 있습니다. 치과 진료소의 8%만 광학 이미징을 사용하고 있습니다. 한편, 동유럽의 의료 시스템은 채워지지 않은 종양 영상 요구를 충족시키기 위해 저비용 플랫폼을 찾고 있습니다. 중동 및 아프리카에서는 규모가 작고 UAE와 사우디아라비아의 전문 병원에서 꾸준한 도입이 기록되어 있으며 정부의 지원으로 인프라 지출과 외상 이미지에 대한 군의 관심이 뒷받침되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 외래 수술 센터(ASC)에서 수술 중 광학 이미징 시스템의 도입 가속(북미 및 EU)

- 미국과 일본에 있어서 OCT 가이드하 PCI의 상환 범위 확대

- 1차 케어에서 당뇨병 망막증 스크리닝을 위한 핸드헬드 OCT의 급속한 보급(아시아)

- 피부과 진단 워크플로우에 있어서 AI 기반의 스펙트럼 알고리즘의 통합(EU 주요 클리닉)

- 암 영역의 신약 개발을 가속하는 라벨 프리 광 절단에 대한 제약 기업 수요 급증

- 외상 트리아지에 있어서 광음향 토모그래피에 대한 군으로부터의 자금 원조(중동·이스라엘)

- 시장 성장 억제요인

- 벤치탑에서 수술실 일체형 이미징 스위트로의 자본 집약적 변화

- 유럽에서 치과용 광학 이미징 처치의 상환은 한정적

- 초분광 영상 전문가의 부족이 신흥 아시아에서 임상 검증을 지연

- 광독성의 우려가 소아 신경학에서 재촬영을 제한

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 이미징 시스템

- 광학 이미징 시스템

- 스펙트럼 이미징 시스템

- 카메라

- 조명 시스템

- 렌즈

- 소프트웨어

- 이미징 시스템

- 용도별

- 안과

- 치과

- 피부과

- 심장학

- 신경학

- 종양학

- 생명공학 및 연구

- 기타 용도

- 기술별

- 광간섭 단층 촬영법

- 근적외선 분광법

- 하이퍼스펙트럼 이미징

- 광음향 단층 촬영법

- 최종 사용자별

- 병원 및 클리닉

- 진단 영상 센터

- 연구 및 진단 실험실

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 페루

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 전략적 발전

- 공급업체 포지셔닝 분석

- 기업 프로파일

- Carl Zeiss AG

- Leica Microsystems(Danaher)

- Topcon Corporation

- Canon Medical Systems(Canon Inc.)

- Koninklijke Philips NV

- PerkinElmer Inc.

- Nikon Metrology NV(Nikon Corp.)

- Olympus Corporation

- Teledyne Princeton Instruments

- Prior Scientific

- Thorlabs Inc.

- Abbott Laboratories

- Headwall Photonics Inc.

- Optovue Inc.

- Cytoviva Inc.

- Michelson Diagnostics Ltd.

- Damae Medical

- Wasatch Photonics Inc.

- Santec Corporation

- BaySpec Inc.

- Optovue Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.13The optical imaging market stands at USD 2.83 billion in 2025 and is on track to reach USD 4.85 billion by 2030, advancing at an 11.35% CAGR.

Growth is being propelled by steady breakthroughs in high-resolution imaging systems, the shift toward non-invasive diagnostics, and widening use in ophthalmology, cardiology, oncology, dermatology, and neurology. Integration with artificial intelligence is improving detection accuracy and workflow speed, while multi-modal platforms that merge optical coherence tomography (OCT) with photoacoustic or hyperspectral tools are expanding clinical value. Semiconductor shortages are nudging suppliers to redesign detectors and pursue vertical integration, yet the optical imaging market continues to benefit from resilient procurement budgets in hospitals, ambulatory surgery centers, and research labs. Asia-Pacific's rapid uptake of handheld OCT for diabetic eye screening and North America's favorable reimbursement for OCT-guided coronary interventions further reinforce the expansion path.

Global Optical Imaging Market Trends and Insights

Accelerated deployment of intra-operative optical imaging systems in ambulatory surgery centers

Ambulatory surgery centers (ASCs) performed more than 23 million procedures in the United States in 2024, a 15% year-on-year rise as payers reposition surgeries to outpatient settings. Compact intra-operative optical platforms, exemplified by UCLA Health's Dynamic Optical Contrast Imaging device, are gaining traction because they delineate tumor margins in real time and trim procedure time by 20%, boosting ASC throughput. Capital spending on these systems is justified by 35-50% cost savings relative to hospital surgeries and by growing insurer support for outpatient pathways. Reimbursement shifts are expected to drive ASC share of all surgeries to 68% by 2030, feeding demand for portable, network-ready optical rigs and widening the optical imaging market base.

Expanding reimbursement coverage for OCT-guided PCI in the United States & Japan

The OCCUPI trial reported a 4.9% composite event rate for OCT-guided PCI at one year compared with 9.5% for angiography alone, sparking policy changes that lift reimbursement by 12% in the United States and broaden coverage in Japan. Providers gain a 22% drop in repeat procedures, offsetting higher per-procedure costs and spurring adoption across high-risk coronary lesions. Utilization of OCT in coronary interventions is forecast to climb from 15% in 2024 to about 35% by 2028, embedding optical imaging deeper into interventional cardiology workflows.

Capital-intensive shift from benchtop to integrated operating-room imaging suites

Fully integrated optical suites bundling OCT, fluorescence, and navigation cost USD 1.5-2.5 million per theater, triple to quadruple benchtop setups, and require extensive infrastructure rewiring. Hospitals also carry 15-20% extra ownership costs over five years for service contracts and specialist training. Consequently, only 23% of eligible hospitals had completed full integration in 2024, with many deferring upgrades or phasing modules over multiple budget cycles. Emerging economies face sharper constraints, slowing penetration despite clear clinical benefits.

Other drivers and restraints analyzed in the detailed report include:

- Rapid adoption of handheld OCT for diabetic retinopathy screening in primary care settings

- Integration of AI-based spectral algorithms in dermatology diagnostic workflows

- Limited reimbursement for dental optical imaging procedures in Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Imaging Systems held 37% of revenue in 2024 on the strength of turnkey consoles used across ophthalmology, cardiology, and research settings. The optical imaging market size for this segment is forecast to expand steadily as vendors augment consoles with AI software and multi-modal add-ons. Rising demand for real-time guidance in minimally invasive surgery maintains hospital investment, even as procurement teams grapple with semiconductor shortages that inflate detector costs. Meanwhile, high-speed Cameras are redefining performance thresholds. Phantom High-Speed's S710 camera achieves 4,000 fps in holographic retinal blood-flow imaging, enabling precise Doppler calculations that enhance vascular diagnostics. This technical leap aligns with a projected 12.5% CAGR through 2030, the fastest within the product spectrum.

Next-generation illumination engines using narrow-band LEDs and super-continuum lasers sustain interest in the Illumination Systems segment as surgeons seek tissue-specific contrast. Software solutions, once peripheral, now anchor differentiation because AI algorithms deliver automated segmentation, vessel quantification, and anomaly flagging. Lenses remain indispensable: advances in aspheric and gradient-index optics boost depth penetration and reduce chromatic aberration, elevating image clarity. To mitigate chip shortages, TDK's Spin Photo Detector leverages magnetic elements to detect light at ultra-high speeds, opening a path to sidestep conventional semiconductor bottlenecks and stabilize component supply chains.

Ophthalmology retained the largest slice at 34.8% in 2024 due to entrenched OCT use for retinal disease management. Adaptive optics technologies are now revealing photoreceptor mosaics and choriocapillaris flow, allowing pre-symptomatic detection of macular disorders. In parallel, Oncology is gaining momentum with a 15.1% CAGR because optical imaging guides margin assessment during tumor resection and tracks vascular response during therapy. Photoacoustic contrast agents targeting hypoxic zones are enabling centimeter-deep visualization of tumor microenvironments in real time. Consequently, the optical imaging market share for oncology applications is set to rise as tertiary hospitals standardize intraoperative optical guidance.

Cardiology follows closely: OCT-guided percutaneous coronary intervention is proving superior to angiography alone in complex lesion management. The optical imaging market size for cardiology is projected to accelerate as more payers authorize coverage. Dermatology benefits from AI-enabled spectral scanners that cut biopsies and improve triage of suspicious lesions. Neurology and Dentistry niches are smaller yet innovative: intraoperative brain OCT tracks tissue mechanics, while dental OCT aids early caries detection without ionizing radiation. Pharmaceutical research groups employ label-free sectioning to visualize drug-cell interactions, shortening oncology drug discovery cycles.

The Optical Imaging Market Report is Segmented by Product (Imaging Systems, Cameras, Illumination Systems, Lenses, and Software), Application (Ophthalmology, Dentistry, Dermatology, Cardiology, Neurology, and Oncology), Technique (OCT, NIRS, Hyperspectral Imaging, and Photoacoustic Tomography), End-User (Hospitals, Diagnostic Centers, and Research Labs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 40% share in 2024, anchored by strong reimbursement and an innovation ecosystem linking universities, startups, and large device makers. The FDA's green light for AI-assisted skin-cancer optical readers in 2024 accelerated cross-specialty adoption, while Duke University's handheld OCT prototypes advance point-of-care eye exams. The optical imaging market size in the region will keep growing as insurers widen coverage for AI-integrated diagnostics and as capital budgets target hybrid OR upgrades.

Asia-Pacific is the fastest-growing cluster, projected at a 12.4% CAGR. Governments in China, India, and Japan are funding domestic manufacturing, lowering import reliance, and subsidizing upgrades for rural clinics. Widespread use of handheld OCT in diabetic retinopathy screening is closing access gaps. Nevertheless, the lack of hyperspectral imaging specialists slows clinical trials, particularly in India and Southeast Asia. Cross-border training partnerships aim to build a talent pipeline that sustains longer-term adoption. Despite these hurdles, the optical imaging market in Asia-Pacific benefits from rising healthcare investment and high diabetes prevalence that drives retinal screening demand.

Europe maintains a sizeable base supported by robust research grants and academic hospital networks. German, French, and UK centers lead clinical validation in dermatology and neurology, yet dental applications suffer under fragmented reimbursement. Only 8% of dental practices use optical imaging because private pay models limit patient uptake. Eastern European health systems, meanwhile, seek lower-cost platforms to address unmet oncology imaging needs. The Middle East and Africa, while smaller, record steady uptake in specialist hospitals across the UAE and Saudi Arabia, buoyed by government-backed infrastructure spending and military interest in trauma imaging.

- Carl Zeiss AG

- Leica Microsystems (Danaher)

- Topcon Corporation

- Canon Medical Systems (Canon Inc.)

- Koninklijke Philips NV

- PerkinElmer Inc.

- Nikon Metrology NV (Nikon Corp.)

- Olympus Corporation

- Teledyne Princeton Instruments

- Prior Scientific

- Thorlabs Inc.

- Abbott Laboratories

- Headwall Photonics Inc.

- Optovue Inc.

- Cytoviva Inc.

- Michelson Diagnostics Ltd.

- Damae Medical

- Wasatch Photonics Inc.

- Santec Corporation

- BaySpec Inc.

- Optovue Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated deployment of intra-operative optical imaging systems in ambulatory surgery centres (North America and EU)

- 4.2.2 Expanding reimbursement coverage for OCT-guided PCI in the United States and Japan

- 4.2.3 Rapid adoption of handheld OCT for diabetic retinopathy screening in primary-care settings (Asia)

- 4.2.4 Integration of AI-based spectral algorithms in dermatology diagnostic workflows (EU major clinics)

- 4.2.5 Surge in pharma demand for label-free optical sectioning to accelerate oncology drug discovery

- 4.2.6 Military funding for photoacoustic tomography in trauma triage (Middle-East and Israel)

- 4.3 Market Restraints

- 4.3.1 Capital-intensive shift from benchtop to integrated operating-room imaging suites

- 4.3.2 Limited reimbursement for dental optical imaging procedures in Europe

- 4.3.3 Scarcity of hyperspectral imaging experts slows clinical validation in emerging Asia

- 4.3.4 Phototoxicity concerns restricting repeat imaging in paediatric neurology

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Imaging Systems

- 5.1.1.1 Optical Imaging Systems

- 5.1.1.2 Spectral Imaging Systems

- 5.1.2 Cameras

- 5.1.3 Illumination Systems

- 5.1.4 Lenses

- 5.1.5 Software

- 5.1.1 Imaging Systems

- 5.2 By Application

- 5.2.1 Ophthalmology

- 5.2.2 Dentistry

- 5.2.3 Dermatology

- 5.2.4 Cardiology

- 5.2.5 Neurology

- 5.2.6 Oncology

- 5.2.7 Biotechnology and Research

- 5.2.8 Other Applications

- 5.3 By Technique

- 5.3.1 Optical Coherence Tomography

- 5.3.2 Near-Infrared Spectroscopy

- 5.3.3 Hyperspectral Imaging

- 5.3.4 Photoacoustic Tomography

- 5.4 By End-User

- 5.4.1 Hospitals and Clinics

- 5.4.2 Diagnostic Imaging Centres

- 5.4.3 Research and Diagnostic Laboratories

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Peru

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Carl Zeiss AG

- 6.3.2 Leica Microsystems (Danaher)

- 6.3.3 Topcon Corporation

- 6.3.4 Canon Medical Systems (Canon Inc.)

- 6.3.5 Koninklijke Philips NV

- 6.3.6 PerkinElmer Inc.

- 6.3.7 Nikon Metrology NV (Nikon Corp.)

- 6.3.8 Olympus Corporation

- 6.3.9 Teledyne Princeton Instruments

- 6.3.10 Prior Scientific

- 6.3.11 Thorlabs Inc.

- 6.3.12 Abbott Laboratories

- 6.3.13 Headwall Photonics Inc.

- 6.3.14 Optovue Inc.

- 6.3.15 Cytoviva Inc.

- 6.3.16 Michelson Diagnostics Ltd.

- 6.3.17 Damae Medical

- 6.3.18 Wasatch Photonics Inc.

- 6.3.19 Santec Corporation

- 6.3.20 BaySpec Inc.

- 6.3.21 Optovue Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment