|

시장보고서

상품코드

1851505

에너지 수확 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Energy Harvesting Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

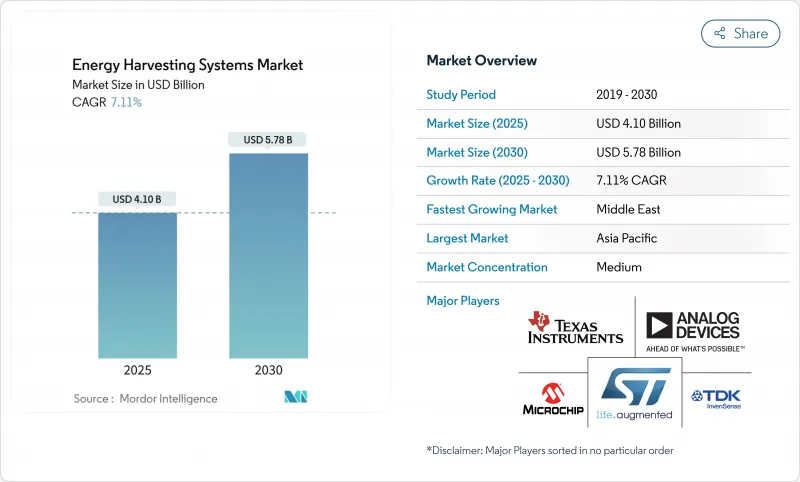

에너지 수확 시스템 시장 규모는 2025년에 41억 달러, 2030년에는 57억 8,000만 달러에 이르고, CAGR 7.11%를 나타낼 것으로 예상됩니다.

배터리가 필요없는 IoT(Internet-of-Things) 장치에 대한 수요가 증가하고 산업 및 소비자 환경에서 초저전력 전자 제품의 보급이 이러한 성장을 뒷받침하고 있습니다. 그 기세는 정교한 레귤레이션 기능을 서브 mm의 풋 프린트에 밀어 넣을 수있는 파워 매니지먼트 집적 회로의 급속한 소형화에 기인하고 있으며, 한편 일회용 배터리의 낭비를 줄이는 정책 압력은 에너지 수확 솔루션의 가치 제안을 강화하고 있습니다. 시장 개척은 또한 턴키 모듈과 레퍼런스 디자인 시장 출시까지의 시간을 단축하는 생태계 파트너십의 혜택을 받아 스마트 빌딩, 공장, 웨어러블에서의 채용을 더욱 촉진합니다. 이러한 힘이 결합되어 에너지 수확 시스템 시장의 현재 10년간의 전망이 강화됩니다.

세계의 에너지 수확 시스템 시장 동향과 인사이트

스마트 빌딩에서 배터리 없는 IoT 센서 노드의 보급

유럽연합(EU)의 에코디자인규칙 2024/1781은 상업시설에 에너지 효율적인 제어시스템의 사용을 의무화하고 빌 관리자를 배터리리스 무선 센서로 밀어 올리고 있습니다. 파리와 오비에도의 실증 실험에서는 거주 데이터와 환경 데이터를 통신하는 태양 센서와 RF 전원 센서를 통합한 결과 평균 36.8kW의 전력 절감을 기록했습니다. RF 수확기는 주변 에너지의 10-50%, 조정된 실내 구역에서는 70% 이상을 변환하여 건물의 라이프사이클에 걸쳐 센서를 계속 작동시킵니다. 시설 소유자는 총 소유 비용을 중시하고 있으며, 세 번의 배터리 교체 사이클이 센서의 초기 하드웨어 비용을 초과한다는 것을 알게 되어 수확 솔루션으로의 전환을 가속화하고 있습니다. 조달 팀이 예산을 유지보수에서 분석 지원 하드웨어로 돌리면서 에너지 수확 시스템 시장은 상업 부동산 부문에서 지속적인 수요를 얻고 있습니다.

아시아태평양 공장에서 지속 가능한 저전력 자동화 요구

중국, 일본, 한국의 산업그룹이 기업의 탄소 삭감 서약을 충족하고 배터리 교환에 수반되는 예정외의 다운타임을 삭감하기 위해 하베스타를 도입. 텔레포니카 테크는 배터리에 대한 액세스가 엄격히 제한된 석유 및 가스 정화소의 진동 노드에 전력을 공급하는 ATEX 인증 열전 발전기를 전개했습니다. 한국과학기술연구원(Korea Institute of Science and Technology)의 조사팀은 열전효과와 압전효과를 조합한 하이브리드 수확기를 개발하여 중기계 모니터링을 위해 출력을 50% 이상 향상시켰습니다. 조밀한 제조 에코시스템은 테스트 도입과 부품 공급업체 간의 빠른 피드백 루프를 가능하게 하여 부품 비용을 더욱 절감합니다. 규제 감사가 생산 공장의 에너지 기준선을 강조함에 따라 경영진은 점점 더 많은 공장에서 수확 플랫폼을 표준화하고 지역적인 기세를 강화하고 있습니다.

농촌 지역에서 앰비언트 RF의 저에너지 밀도

현장 평가판에 따르면 생산자의 70%가 무선 센서 파일럿을 포기합니다. Aggritec Integrator는 현재 관개 펌프에 소형 태양 타일과 진동 스트립을 결합하여 흐린 계절과 RF 신호의 약점을 헤지하고 있습니다. 그럼에도 불구하고 하이브리드 디자인은 비용을 높이고 유지 보수 일정을 복잡하게하기 때문에 비용에 민감한 농장에 대한 광범위한 도입을 늦추고 있습니다. 농촌의 접속 인프라가 확대될 때까지는 이 억제요인이 농업·환경 모니터링의 에너지 수확 시스템 시장의 당면의 상승 요인이 됩니다.

부문 분석

2024년 에너지 수확 시스템 시장 점유율은 빛 기반 태양광 발전 수확기가 42%를 차지했습니다. 뛰어난 성숙도, 와트당 저비용, 예측 가능한 일주 에너지 프로파일로 태양광 발전은 건물과 야외 설치의 극 위치를 유지하고 있습니다. 그러나 RF 하베스팅은 고밀도 5G 배치가 센서의 전력으로 사용할 수 있는 주변의 전자파 레벨을 상승시키기 때문에 2030년까지의 CAGR은 11%를 나타낼 전망입니다. 진동 수확기와 전자파 수확기는 회전 에너지가 풍부한 기계에 도움이 되는 반면, 열 제벡 장치는 자동차의 배기 가스나 산업로에 틈새를 발견합니다. 다수의 모달리티를 융합시킨 하이브리드 아키텍처는 빛이나 움직임의 정체시에 연속성을 제공해, 미션 크리티컬한 이용 사례에 어필합니다. 에너지 수확 시스템 시장은 통합자가 지능형 최대 전력 점 추적과 적응형 스토리지를 결합하여 변동하는 소스 전체에서 수율을 최적화함으로써 탄력성을 높입니다.

하이브리드 실증 예도 풍부합니다. 앰비언트 포토닉스(Ambient Photonics)는 200룩스로 기존 셀의 3배의 출력을 기록해 실내 리모컨과 키보드의 잠금을 해제했습니다. 한편 한국과학기술연구원은 캔틸레버 플랫폼에 열전 채널과 압전 채널을 융합시킴으로써 50%의 출력 향상을 보고하고 있습니다. 이러한 발전으로 인해 투자 회수 기간이 단축되고 가동 시간 보장이 연장되므로 상대방 상표 제품 제조업체가 제안 요청서에 다중 소스 설계를 명시하도록 촉구하고 있습니다. RF 수확 효율이 증가하고 부품 가격이 감소함에 따라 에너지 수확 시스템 시장은 부하 수요를 유지하기 위해 수 밀리 초마다 가장 생산성이 높은 소스를 자동으로 선택하는 수렴 모듈을 보게됩니다.

파워 매니지먼트 IC는 2024년 에너지 수확 시스템 시장 규모의 38%를 차지했습니다. 에너지 수확 트랜스듀서는 설계자가 단일 소스 아키텍처를 넘어 다양화하고 특수 변환 레이어를 필요로 하기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 9.5%를 나타낼 전망입니다. 박막 배터리와 슈퍼커패시터는 간헐적인 에너지 스트림을 완충하고 초저전력 마이크로컨트롤러는 센서 배치를 정당화하는 분석을 수행합니다. ST 마이크로 일렉트로닉스의 SPV1050은 태양광 발전과 열전기 입력에 대해 최대 99%의 변환 효율을 달성하고 정교한 레귤레이션이 노드 수명을 연장하는 방법을 강조합니다. 아사히카세이의 AP4413 시리즈는 셀 밸런싱과 트리클 충전 제어를 1.43mm2의 다이에 집적하여 비용 중심의 소비자용 가젯에 하베스팅 솔루션을 제공합니다.

업계 로드맵은 하베스팅 프론트엔드, 벅 컨버터 및 마이크로컨트롤러를 단일 라미네이트에 통합한 시스템 온칩 패키지로 수렴합니다. 이 통합은 보드 레벨 상호 연결 손실을 없애고 인증을 단순화하므로 산업 자동화에서 스마트 장난감에 이르기까지 사용 가능한 사례를 확대합니다. 예측 기간 동안 집적화 대응 PMIC의 ASP는 감소하고 에너지 수확 시스템 시장은 더욱 강화됩니다.

에너지 수확 시스템 시장은 기술별(광에너지 수확, 진동 에너지 수확, 기타), 구성 요소별(에너지 수확 컨버터, 파워 매니지먼트 IC, 기타), 전력 범위별(10MW 미만, 10-100MW, 기타), 용도별(컨슈머 일렉트로닉스, 빌딩 및 홈 오토메이션, 산업용 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

아시아는 2024년 세계 매출의 35%를 차지하며 중국의 방대한 IoT 전개와 TDK Corporation tdk.com과 같은 기업에 의한 압전 재료에 있어서 일본의 리더십의 혜택을 받았습니다. 서울에서 심천에 이르기까지 정부가 지원하는 스마트시티 프로그램이 센서 인프라를 조성하고 대만과 말레이시아의 수탁 제조업자가 제품 사이클을 단축하는 비용 효율적인 조립 경로를 제공합니다. 한국 반도체 에코시스템은 맞춤형 PMIC 제조를 확대하고 싱가포르의 물류공원은 대규모 앰비언트 IoT 어레이를 테스트하여 현실 세계 수확기의 견고성을 보여줍니다.

중동은 2030년까지 연평균 복합 성장률(CAGR)이 9.2%로 가장 빠른 궤도를 기록합니다. 사우디아라비아의 비전 2030에서는 재생에너지가 거대한 도시 계획의 중심에 위치하고 있으며, 알 하람 모스크의 실내 내비게이션 비콘에서는 순례자의 발소리를 그리드 전력으로 변환하는 피에조 타일 바닥재를 시험하고 있습니다. 걸프 협력 회의 회원국의 전력 회사는 스마트 미터의 하우징에 태양광 발전 장치를 통합하여 배터리 서비스를 위해 트럭을 달리는 것을 피하고 있습니다. 이스라엘과 아랍에미리트(UAE)은 나노 재료 연구소와 벤처 펀드를 결합한 지역의 연구 개발 클러스터를 형성하여 고효율 수확기의 상업화 일정을 가속화하고 있습니다.

북미와 유럽은 라이프사이클의 지속가능성을 중시하는 규제 프레임워크과 결합된 성숙하면서도 견조한 수요를 보여주고 있습니다. 미국 에너지부는 충전기의 대기 전력 제한을 보다 엄격하게 하는 것을 제안해, 가전 제조업체를 환경 전력 경로로 유도하고 있습니다. 독일과 영국은 3년에서 5년 사이 순 현재 가치로 이익을 얻을 수 있도록 회전 기계에 진동 수확기를 공장에 장비하고 있습니다. 이러한 경제권에서는 센서 플랫폼을 선택할 때 엔지니어링 팀이 이산화탄소 삭감량을 정량화하게 되어 있어 초기 투자액이 높아도 에너지 수확 시스템 시장에 안정된 주문이 들어가는 동향이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스마트 빌딩에 있어서 배터리리스 IoT 센서 노드의 보급(유럽, 북미)

- APAC 공장에서 지속 가능한 저전력 자동화 의무화

- 서브 W threshold를 가능하게 하는 초저소비 전력 MCU의 급속한 소형화

- 철도와 항공 OEM에 무선 상태 모니터링 도입 확대

- 웨어러블과 의료용 패치에 태양광 발전 수확기의 통합

- 시장 성장 억제요인

- 농촌에서의 앰비언트 RF의 저에너지 밀도

- 보편적인 전력 관리 규격의 부재

- 경쟁하는 LPWAN 배터리에 의해 온보드 수확기의 필요성이 감소

- 교통기관의 개수에 걸리는 초기 설계·통합 비용의 높이

- 가치/공급망 분석

- 규제와 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 기술별

- 광(태양광/광전지) 에너지 수확

- 진동(압전 및 전자기) 에너지 수확

- 열(제벡/열전) 에너지 수확

- RF(무선 주파수) 에너지 수확

- 하이브리드/다중 소스 에너지 수확

- 구성 요소별

- 에너지 수확 변환기

- 전력 관리 IC

- 에너지 저장 장치(박막 전지, 슈퍼커패시터)

- 초저전력 센서 및 MCU

- 출력 범위별

- 10마이크로와트 미만

- 10-100마이크로와트

- 100마이크로와트-1mW

- 1-10mW

- 10mW 이상

- 용도별

- 소비자 일렉트로닉스

- 빌딩 및 홈 오토메이션

- 산업용 IoT 및 자동화

- 운송

- 자동차

- 철도

- 항공

- 헬스케어 및 웨어러블

- 국방 및 보안

- 농업 및 환경 모니터링

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽(스웨덴, 노르웨이, 덴마크, 핀란드)

- 베네룩스(벨기에, 네덜란드, 룩셈부르크)

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN(싱가포르, 말레이시아, 태국, 인도네시아, 필리핀, 베트남)

- 남미

- 브라질

- 아르헨티나

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 이스라엘

- 튀르키예

- 아프리카

- 남아프리카

- 나이지리아

- 케냐

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Microchip Technology Inc.

- STMicroelectronics NV

- Texas Instruments Incorporated

- Analog Devices Inc.

- Renesas Electronics Corporation

- NXP Semiconductors NV

- onsemi(ON Semiconductor Corp.)

- TDK Corporation(InvenSense)

- Powercast Corporation

- Cymbet Corporation

- EnOcean GmbH

- e-peas SA

- ABB Ltd.

- Advanced Linear Devices Inc.

- Cap-XX Limited

- Fujitsu Components America Inc.

- G24 Power Ltd.

- Drayson Technologies Ltd.

- Piezo.com(Mide Technology)

- LORD MicroStrain(Parker Hannifin)

제7장 시장 기회와 향후 전망

KTH 25.11.21The energy harvesting systems market size is USD 4.10 billion in 2025 and is forecast to climb to USD 5.78 billion by 2030, advancing at a 7.11% CAGR.

Rising demand for battery-free Internet-of-Things (IoT) devices and the spread of ultra-low-power electronics across industrial and consumer environments underpin this growth. Momentum stems from rapid miniaturization in power-management integrated circuits that now squeeze sophisticated regulation functions into sub-millimeter footprints, while policy pressure to cut disposable battery waste reinforces the value proposition for energy harvesting solutions. Developers also benefit from ecosystem partnerships that speed time-to-market for turnkey modules and reference designs, further lifting adoption in smart buildings, factories, and wearables. Together, these forces strengthen the energy harvesting systems market outlook during the current decade.

Global Energy Harvesting Systems Market Trends and Insights

Proliferation of Battery-less IoT Sensor Nodes in Smart Buildings

The European Union Ecodesign Regulation 2024/1781 obliges commercial properties to use energy-efficient control systems, which pushes building managers toward battery-free wireless sensors Demonstrations in Paris and Oviedo logged 36.8 kW average power savings after integrating solar and RF-powered sensors that communicate occupancy and environmental data. RF harvesters convert 10-50% of ambient energy and more than 70% in tuned indoor zones, keeping sensors operational for the entire building life cycle. Facility owners increasingly weigh total cost of ownership and find that three battery replacement cycles eclipse initial sensor hardware costs, accelerating migration to harvesting solutions. As procurement teams pivot budgets from maintenance to analytics-ready hardware, the energy harvesting systems market gains sustained demand from the commercial real-estate sector.

Mandates for Sustainable Low-Power Automation in APAC Factories

Industrial groups across China, Japan, and South Korea install harvesters to satisfy corporate carbon pledges and cut unscheduled downtime tied to battery swaps. Telefonica Tech rolled out ATEX-certified thermoelectric generators that power vibration nodes in oil and gas refineries where battery access is tightly restricted. Researchers at the Korea Institute of Science and Technology combined thermoelectric and piezoelectric effects in a hybrid harvester that boosts power output by more than 50% for heavy-machinery monitoring. Dense manufacturing ecosystems allow quick feedback loops between pilot deployments and component suppliers, further trimming bill-of-materials cost. As regulatory audits emphasize energy baselines in production plants, executives increasingly standardize harvesting platforms across multiple factory sites, reinforcing regional momentum.

Low Energy Density of Ambient RF in Rural Installations

Field trials show that 70% of growers abandon wireless sensor pilots because nodes exhaust batteries faster than expected, a gap magnified where RF density dips below harvestable levels. Agritech integrators now blend small solar tiles with vibration strips on irrigation pumps to hedge against cloudy seasons and weak RF signals. Even so, hybrid designs raise costs and complicate maintenance schedules, delaying wide deployment in cost-sensitive farms. Until rural connectivity infrastructure expands, this restraint caps immediate upside for the energy harvesting systems market in agriculture and environmental monitoring.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Miniaturization of Ultra-Low-Power MCUs Enabling Sub-µW Thresholds

- Growing Deployment of Wireless Condition-Monitoring in Rail & Aviation OEMs

- Absence of Universal Power-Management Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Light-based photovoltaic harvesters controlled 42% of the energy harvesting systems market share in 2024. Superior maturity, low cost per watt, and predictable diurnal energy profiles keep photovoltaics in pole position for building and outdoor installations. RF harvesting, however, posts an 11% CAGR to 2030 as dense 5G deployments raise ambient electromagnetic levels that can be scavenged for sensor power. Vibration and electromagnetic harvesters serve machinery where rotational energy is plentiful, while thermal Seebeck devices find niches in automotive exhaust and industrial furnaces. Hybrid architectures that blend multiple modalities deliver continuity during light or motion lulls, appealing to mission-critical use cases. The energy harvesting systems market gains resilience as integrators pair intelligent maximum-power-point tracking with adaptive storage to optimize yield across variable sources.

Hybrid proof points abound. Ambient Photonics records triple the power output in 200 lux compared with legacy cells, unlocking indoor remote controls and keyboards. Meanwhile, the Korea Institute of Science and Technology reports a 50% power bump by merging thermoelectric and piezoelectric channels in a cantilever platform. These advances compress payback periods and extend uptime guarantees, encouraging original-equipment manufacturers to specify multi-source designs in request-for-proposal documents. As RF harvesting efficiency rises and component prices drop, the energy harvesting systems market will witness converged modules that auto-select the most productive source every few milliseconds to sustain load demands.

Power-management ICs captured 38% of the energy harvesting systems market size in 2024 by value because every harvester topology requires accurate voltage regulation and storage orchestration. Energy-harvesting transducers exhibit a 9.5% CAGR to 2030 as designers diversify beyond single-source architectures and need specialized conversion layers. Thin-film batteries and supercapacitors buffer intermittent energy streams, while ultra-low-power microcontrollers perform the analytics that justify sensor deployments. STMicroelectronics' SPV1050 achieves up to 99% conversion efficiency for photovoltaic and thermoelectric inputs, highlighting how sophisticated regulation extends node lifetimes. Asahi Kasei's AP4413 series integrates cell-balancing and trickle-charge control in a 1.43 mm2 die, bringing harvesting solutions to cost-sensitive consumer gadgets.

Industry roadmaps converge on system-on-chip packages that embed harvesting front ends, buck-boost converters, and microcontrollers within a single laminate. This consolidation removes board-level interconnect losses and simplifies certification, expanding addressable use cases from industrial automation to smart toys. Over the forecast window, falling ASPs for integration-ready PMICs will spur volume shipments, further fortifying the energy harvesting systems market.

Energy Harvesting Systems Market is Segmented by Technology (Light Energy Harvesting, Vibration Energy Harvesting, and More), Component (Energy-Harvesting Transducers, Power-Management ICs, and More), Power Range (Less Than 10 MW, 10-100 MW, and More), Application (Consumer Electronics, Building and Home Automation, Industrial IoT and Automation, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia held 35% of 2024 global revenue, benefiting from China's immense IoT roll-outs and Japan's leadership in piezoelectric materials through firms such as TDK Corporation tdk.com. Government-backed smart-city programs from Seoul to Shenzhen subsidize sensor infrastructure, while contract manufacturers in Taiwan and Malaysia offer cost-efficient assembly paths that shorten product cycles. South Korea's semiconductor ecosystem extends bespoke PMIC fabrication, and Singapore's logistics parks test large-scale ambient IoT arrays that showcase real-world harvester robustness.

The Middle East records the fastest trajectory at a 9.2% CAGR to 2030. Saudi Arabia's Vision 2030 positions renewable energy at the center of megacity planning, and indoor navigation beacons at the Al-Haram mosque now trial piezo tile flooring that converts pilgrim footsteps into grid power doi.org. Gulf Cooperation Council utilities integrate photovoltaic harvesters into smart-meter housings to avoid truck rolls for battery service. Israel and the United Arab Emirates anchor regional R&D clusters that pair nano-material labs with venture funds, accelerating commercialization timelines for high-efficiency harvesters.

North America and Europe show mature yet solid demand tied to regulatory frameworks that emphasize lifecycle sustainability. The United States Department of Energy proposes stricter standby limits for chargers, nudging appliance makers toward ambient power paths. Germany and the United Kingdom equip factories with vibration harvesters for rotating machinery, citing net present value gains over three to five years. Across these economies, engineering teams now quantify carbon abatement when selecting sensor platforms, a trend that channels steady orders into the energy harvesting systems market even where initial capital outlay is higher.

- Microchip Technology Inc.

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Analog Devices Inc.

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- onsemi (ON Semiconductor Corp.)

- TDK Corporation (InvenSense)

- Powercast Corporation

- Cymbet Corporation

- EnOcean GmbH

- e-peas S.A.

- ABB Ltd.

- Advanced Linear Devices Inc.

- Cap-XX Limited

- Fujitsu Components America Inc.

- G24 Power Ltd.

- Drayson Technologies Ltd.

- Piezo.com (Mide Technology)

- LORD MicroStrain (Parker Hannifin)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Battery-less IoT Sensor Nodes in Smart Buildings (Europe and North America)

- 4.2.2 Mandates for Sustainable Low-Power Automation in APAC Factories

- 4.2.3 Rapid Miniaturization of Ultra-Low-Power MCUs Enabling Sub-W Thresholds

- 4.2.4 Growing Deployment of Wireless Condition-Monitoring in Rail and Aviation OEMs

- 4.2.5 Integration of Photovoltaic Harvesters into Wearables and Medical Patches

- 4.3 Market Restraints

- 4.3.1 Low Energy Density of Ambient RF in Rural Installations

- 4.3.2 Absence of Universal Power-Management Standards

- 4.3.3 Competing LPWAN Batteries Reducing Need for On-Board Harvesters

- 4.3.4 High Up-front Design-Integration Costs for Transportation Retrofits

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Light (Solar/Photovoltaic) Energy Harvesting

- 5.1.2 Vibration (Piezoelectric and Electromagnetic) Energy Harvesting

- 5.1.3 Thermal (Seebeck / Thermoelectric) Energy Harvesting

- 5.1.4 RF (Radio-Frequency) Energy Harvesting

- 5.1.5 Hybrid / Multi-Source Energy Harvesting

- 5.2 By Component

- 5.2.1 Energy-Harvesting Transducers

- 5.2.2 Power-Management ICs

- 5.2.3 Energy-Storage Units (Thin-Film Batteries, Supercapacitors)

- 5.2.4 Ultra-Low-Power Sensors and MCUs

- 5.3 By Power Range

- 5.3.1 Less than 10 micro W

- 5.3.2 10-100 micro W

- 5.3.3 100 micro W-1 mW

- 5.3.4 1-10 mW

- 5.3.5 Greater than 10 mW

- 5.4 By Application

- 5.4.1 Consumer Electronics

- 5.4.2 Building and Home Automation

- 5.4.3 Industrial IoT and Automation

- 5.4.4 Transportation

- 5.4.4.1 Automotive

- 5.4.4.2 Rail

- 5.4.4.3 Aviation

- 5.4.5 Healthcare and Wearables

- 5.4.6 Defense and Security

- 5.4.7 Agriculture and Environmental Monitoring

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordics (Sweden, Norway, Denmark, Finland)

- 5.5.2.7 Benelux (Belgium, Netherlands, Luxembourg)

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN (Singapore, Malaysia, Thailand, Indonesia, Philippines, Vietnam)

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Israel

- 5.5.5.4 Turkey

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Microchip Technology Inc.

- 6.4.2 STMicroelectronics N.V.

- 6.4.3 Texas Instruments Incorporated

- 6.4.4 Analog Devices Inc.

- 6.4.5 Renesas Electronics Corporation

- 6.4.6 NXP Semiconductors N.V.

- 6.4.7 onsemi (ON Semiconductor Corp.)

- 6.4.8 TDK Corporation (InvenSense)

- 6.4.9 Powercast Corporation

- 6.4.10 Cymbet Corporation

- 6.4.11 EnOcean GmbH

- 6.4.12 e-peas S.A.

- 6.4.13 ABB Ltd.

- 6.4.14 Advanced Linear Devices Inc.

- 6.4.15 Cap-XX Limited

- 6.4.16 Fujitsu Components America Inc.

- 6.4.17 G24 Power Ltd.

- 6.4.18 Drayson Technologies Ltd.

- 6.4.19 Piezo.com (Mide Technology)

- 6.4.20 LORD MicroStrain (Parker Hannifin)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment