|

시장보고서

상품코드

1851506

이유식 포장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Baby Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

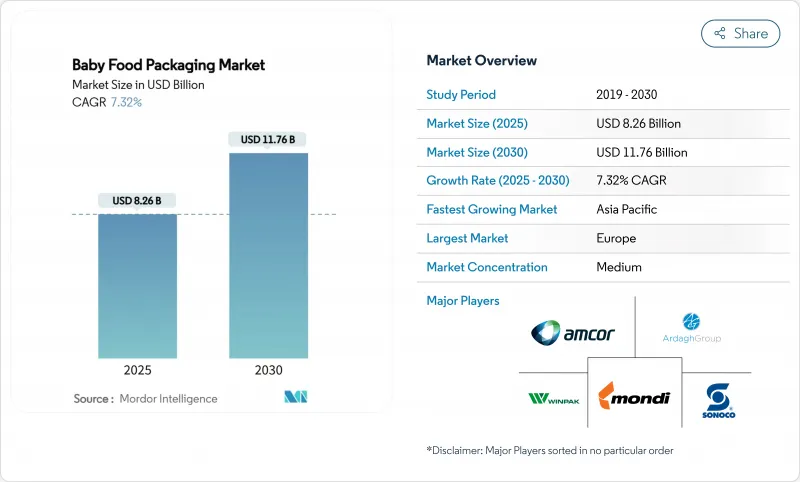

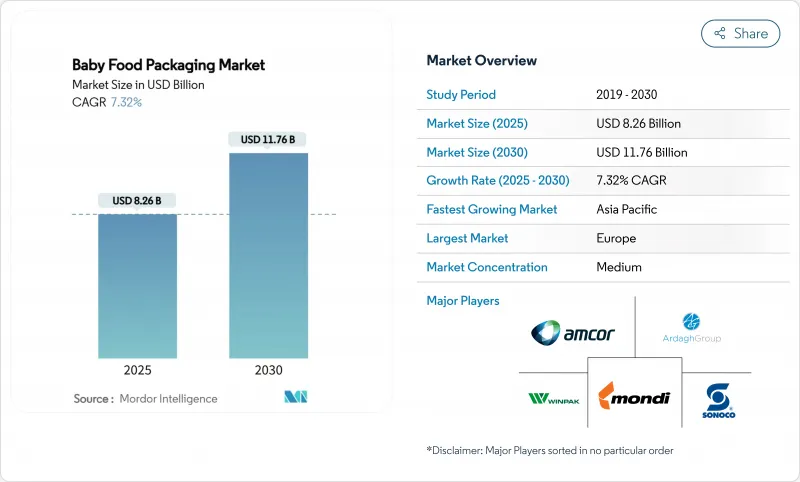

이유식 포장 시장 규모는 2025년에 82억 6,000만 달러, 2030년에는 117억 6,000만 달러에 이르고, CAGR 7.32%를 나타낼 것으로 예상됩니다.

이 성장률은 도시의 가정이 빨리 먹을 수 있는 형식을 요구하고, 규제 당국이 유아의 안전에 관한 엄격한 규칙을 부과하고, 컨버터가 소비자와의 대화를 가능하게 하면서 유통 기한을 연장하는 스마트 소재를 전개함에 따라, 보다 광범위한 식품 포장 카테고리를 상회하고 있습니다. 유아용 수지의 프리미엄 가격 내성은 안정적이며 공급업체는 컴플라이언스 비용을 가격으로 전가할 수 있는 반면, 확대 생산자 책임(EPR) 프로그램은 재활용 가능한 라미네이트 및 바이오 라미네이트 수요를 촉진하고 있습니다. 2025년부터 2030년까지도 파우치, 무균 충전 라인, AI를 활용한 추적 가능성는 이유식 포장 시장에서 고성능 벤더와 코모디티 경쟁사를 나누는 매우 중요한 혁신의 최전선이 될 것으로 예측됩니다. 세계적인 수지 변동과 DIY 퓌레의 동향이 카테고리의 기세를 약화시키는 가운데, 의약품 등급의 스파우트 및 배리어 필름에 대한 공급망의 규율 강화는 계속 필수적입니다.

세계의 이유식 포장 시장 동향과 인사이트

편리함이 이유식용 파우치의 보급을 견인

가루가 달린 파우치는 가벼운 무게, 운반 용이성, 흩어지지 않은 분주로 유리 병을 대체하여 이유식 포장 시장에서 30% 이상의 점유율을 보장합니다. 밀레니얼 세대의 부모는 리실러빌리티와 파손 위험의 감소를 결정적인 이점으로 간주하고 가격 프리미엄 및 반복 구매를 지원합니다. 내열성 라미네이트는 핫 필, 레토르트, 고압 저온 살균을 가능하게 해, 보존료 프리의 보존 안정성을 실현합니다. 브랜드 사례 연구는 특히 유기농 퓌레에서 파우치 형식으로 전환한 후 매출이 두 자리 상승한 것으로 나타났습니다. 이러한 요인들이 결합되어, 이 부문은 이유식 포장 시장의 가장 크고 가장 빠른 성장 엔진임을 뒷받침합니다.

도시 지역의 공동 가구는 시간 절약 형식을 요구합니다.

밀집한 대도시에서는 공동 작업의 부모가, 밑바닥 세척의 수고를 생략하는 곧바로 먹을 수 있는 포장에 바꿔 넣습니다. 원스 어폰 어 팜은 이 수요에 부응하기 위해 자동화 라인을 2020년의 3배 주 120만 팩으로 확장했습니다. 전자상거래의 보급은 파우치나 강화 카톤이 유리보다 소포를 취급할 때의 충격에 강하기 때문에 이 동향을 증폭시킵니다. 가격 프리미엄은 20-30%에 달하는 것, 탄력성은 여전히 양호하고, 가정은 포장의 편리성을 무형의 시간 절약과 동일시하기 때문에 이유식 포장 시장에는 지속적인 추풍이 됩니다.

플라스틱의 지속가능성에 대한 반발과 법규

캘리포니아, 메인, 오레곤, 콜로라도의 EPR 법은 생산자에게 재활용 시스템을 지원하고 회수를 위한 설계 기준을 충족해야 합니다. EU의 포장·포장 폐기물 규제는 2030년까지 재활용률 30%를 의무화하고 있습니다. 식품 재활용 PP의 생산 능력은 재활용 폴리머 총 생산량의 10% 가까이에 머물러 있으며, 공급은 급박하고 비용은 상승하고 있습니다. 재활용성과 퇴비화 가능성을 입증할 수 있는 브랜드는 소비자의 신뢰를 얻지만, 기존의 다층 포맷은 진부화의 가속에 직면해, 이유식 포장 시장 전체의 당면의 이폭을 압박하고 있습니다.

부문 분석

플라스틱은 광범위한 가공 인프라를 반영하여 2024년에는 26.7%의 판매 점유율을 유지했지만 규제 당국과 브랜드가 탄소 감축 목표를 강화함에 따라 바이오플라스틱이 가장 빠른 9.7%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 브라스켐의 사용된 식용유 유래의 바이오서큘러 폴리프로필렌은 라인 전환을 용이하게 하는 드롭 인 대체품을 제공합니다. ADBioplastics는 습식 유아용 퓌레에 적합한 100% 퇴비화 가능한 수지를 상용화했습니다. 바이오폴리머를 조기에 채택한 기업은 EPR 크레딧과 마케팅 우위를 확보하고 기존의 플라스틱이 규모와 비용의 우위를 유지하는 한편 바이오폴리머를 전략적 헤지로 자리매김하고 있습니다.

컨버터는 바이오폴리머 공급업체와 장기적인 인수 협상을 수행하며, CPG는 라벨의 디자인을 변경하여 사용되었음을 강조합니다. 수량이 증가함에 따라 규모의 경제가 비용 차이를 줄이고 바이오플라스틱이 이유식 포장 시장에 더 정착할 것으로 예측됩니다.

지역 분석

유럽은 재활용 가능한 설계에 보답하고 화학적 위험성을 처벌하는 진보적인 규제에 힘입어 2024년 매출에서 25.8%의 리드를 유지했습니다. 2025년 1월 BPA 금지령은 신속한 개선을 촉구하고 자격을 갖춘 재료 및 규정 준수 문서가 있는 공급업체로 비즈니스를 유도합니다. 독일과 프랑스는 지속가능한 포장의 연구개발 거점이 있으며, 영국에서는 추적 가능성 칩을 포함한 스마트 파우치가 포함된 프리미엄 유기농 퓌레에 대한 수요가 지속되고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 7.8%를 나타냅니다. 중간층의 소득 증가와 도시의 라이프 스타일이 편리성 중시의 SKU를 가속시켜, 이 지역을 이유식 포장 시장에 있어서 최대의 수량 증가원으로 위치시킵니다. 중국의 유아용 준비 분유 리바운드 H&H Group은 2025년 1분기에 44.3%의 증수를 기록해 이전의 안전성 불안 이후 브랜드 영양에 대한 신뢰가 다시 높아지고 있음을 나타냅니다. 인도의 BPA 프리 의무화는 Amcor에 의한 Phoenix Flexibles의 2,000만 달러의 인수와 일치. 일본과 한국은 소비자의 안전성 확인 지향을 반영하여 듀얼 QR 추적 가능성의 선구자가 됩니다.

북미는 FDA 규칙이 엄격하고 전자상거래가 널리 보급되어 있기 때문에 여전히 고가치의 무대입니다. 4개 주에서 EPR법이 제정되고, 브랜드는 재활용 자금을 조달하는 것이 의무화되고, 단일 소재 라미네이트의 신속한 채용이 추진됩니다. 2022년 분유 부족은 국내 생산 능력 투자를 촉진했습니다. Bobby의 오하이오 공장은 현재 9만 평방피트의 크기로 엄격한 미생물 학적 관리하에 통조림 우유와 분말 분유를 생산하고 있습니다. 캐나다의 각 주 EPR 네트워크는 유연한 포맷과 리지드 포맷에 관계없이 재활용을 고려한 설계를 장려하고 꾸준한 기술 혁신을 지원합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 편리성 주도의 이유식 파우치 채용

- 도시의 공동 세대가 요구하는 시간 절약 포맷

- 영유아 안전규제의 강화가 고급 포장을 확대

- 대두하는 무균 스파우트 파우치 충전 라인

- 재활용 가능성에 대한 확대 생산자 책임 인센티브

- AI에 의한 퍼스널라이즈드 영양 팩의 디자인 혁신

- 시장 성장 억제요인

- 플라스틱의 지속가능성에 대한 반발과 법규제

- BPA/화학물질 컴플라이언스 비용 압력

- 제약 등급 스파우트 수지 공급 병목

- 이유식의 DIY 동향이 포장 수요를 감소

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시경제 요인 평가

제5장 시장 규모와 성장 예측

- 재료별

- 플라스틱

- 판지

- 금속

- 유리

- 바이오플라스틱

- 포장 유형별

- 병

- 판지

- 항아리

- 파우치

- 백 인 박스

- 제품별

- 액체 분유

- 건조 이유식

- 분유

- 조리 이유식

- 유아 간식

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor PLC

- Tetra Laval Group

- Mondi Group

- Berry Global Inc.(incl. former RPC)

- Silgan Holdings Inc.

- Sonoco Products Company

- Ardagh Group

- Winpak Ltd

- DS Smith PLC

- SIG Combibloc Group

- Cheer Pack North America

- Gualapack Group

- Scholle IPN

- UFlex Ltd

- ProAmpac LLC

- Huhtamaki Oyj

- AptarGroup Inc.

- Plastipak Packaging Inc.

- Crown Holdings Inc.

- Sealed Air Corp.

제7장 시장 기회와 향후 전망

KTH 25.11.21The baby food packaging market size stands at USD 8.26 billion in 2025 and is forecast to reach USD 11.76 billion by 2030, advancing at a 7.32% CAGR.

This growth rate exceeds the broader food-packaging category as urban families seek ready-to-serve formats, regulators impose strict infant-safety rules, and converters deploy smart materials that lengthen shelf life while enabling consumer interaction. Steady premium-price tolerance for infant-grade resins allows suppliers to pass through compliance costs, while extended-producer-responsibility (EPR) programs propel demand for recyclable or bio-based laminates. During 2025-2030, spouted pouches, aseptic filling lines, and AI-enabled traceability are expected to remain the pivotal innovation fronts that separate high-performing vendors from commodity competitors in the baby food packaging market. Heightened supply-chain discipline around pharmaceutical-grade spouts and barrier films will remain essential as global resin volatility and DIY puree trends periodically temper category momentum.

Global Baby Food Packaging Market Trends and Insights

Convenience-Driven Adoption of Baby Food Pouches

Spouted pouches have secured more than 30% share of the baby food packaging market by displacing glass jars through lighter weight, portability, and mess-free dispensing. Millennial parents view resealability and reduced breakage risk as decisive benefits, supporting price premiums and repeat purchases. Heat-resistant laminates enable hot-fill, retort, and high-pressure pasteurization, delivering preservative-free shelf stability. Brand case studies show double-digit sales lifts after switching to pouch formats, particularly in organic purees. Together, these factors underpin the segment's dual status as both largest and fastest growth engine of the baby food packaging market.

Urban Dual-Income Households Demanding Time-Saving Formats

In dense metros, working parents trade up to ready-to-consume packages that cut prep time and washing. Once Upon a Farm scaled automated lines to 1.2 million packs per week triple 2020 throughput-to meet this demand.Asia Pacific megacities show the sharpest volume increases as extended-family childcare support wanes. E-commerce penetration amplifies the trend because pouches and reinforced cartons tolerate parcel-handling shocks better than glass. Despite 20-30% price premiums, elasticity remains favorable as households equate packaging convenience with intangible time savings, providing sustained tailwinds for the baby food packaging market.

Plastics Sustainability Backlash & Legislation

EPR statutes in California, Maine, Oregon, and Colorado obligate producers to bankroll recycling systems and meet design-for-recovery criteria.The EU's Packaging and Packaging Waste Regulation further mandates 30% recycled content by 2030. Food-grade recycled PP capacity sits near 10% of total recycled polymer output, tightening supply and inflating costs. Brands able to validate recyclability or compostability gain consumer trust, whereas legacy multilayer formats face accelerating obsolescence, weighing on near-term margins across the baby food packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Infant-Safety Regulations Expanding Premium Packaging

- Aseptic Spouted-Pouch Filling Lines Gaining Ground

- Supply Bottlenecks of Pharma-Grade Spout Resins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic maintained 26.7% revenue share in 2024, reflecting extensive processing infrastructure, but bioplastics now post the quickest 9.7% CAGR as regulators and brands escalate carbon-reduction targets. Braskem's bio-circular polypropylene derived from used cooking oil offers a drop-in alternative that eases line changeovers. ADBioplastics commercialized a 100% compostable resin tailored for wet baby purees. Early adopters secure EPR credits and marketing lift, positioning biopolymers as a strategic hedge even while traditional plastics keep scale and cost advantages.

The material shift galvanizes supply-chain reengineering: converters negotiate long-term offtake with bio-polymer suppliers, and CPGs redesign labels to highlight end-of-life credentials. As volumes rise, economies of scale are expected to narrow the cost delta, further embedding bioplastics within the baby food packaging market.

Baby Food Packaging Market Report is Segmented by Material (Plastic, Paperboard, Metal, Glass, Bioplastics), Package Type (Bottles, Cartons, Jars, Pouches, Bag-In-Box), Product (Liquid Milk Formula, Dried Baby Food, Powder Milk Formula, Prepared Baby Food, Baby Snacks), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe maintained a 25.8% revenue lead in 2024, propelled by progressive regulation that rewards recyclable designs and punishes chemical hazards. The January 2025 BPA prohibition forces immediate reformulations, channeling business toward suppliers with qualifying materials and compliance documentation. Germany and France house active clusters of sustainable-packaging R&D, while the UK displays sustained demand for premium organic purees sold in smart pouches that embed traceability chips.

Asia Pacific shows the fastest 7.8% CAGR through 2030. Rising middle-class incomes and urban lifestyles accelerate convenience-focused SKUs, positioning the region as the largest incremental volume source for the baby food packaging market. China's infant-formula rebound H&H Group recorded 44.3% Q1 2025 revenue growth signals renewed confidence in branded nutrition after earlier safety scares. India's BPA-free mandate aligns with Amcor's USD 20 million purchase of Phoenix Flexibles, which boosts local flexible-film capacity in Gujarat. Japan and South Korea pioneer dual-QR traceability, reflecting consumer penchant for safety verification.

North America remains a high-value arena given stringent FDA rules and wide e-commerce penetration. EPR laws in four states obligate brands to finance recycling, pushing quick adoption of mono-material laminates. The 2022 formula shortage catalyzed domestic capacity investments: Bobbie's 90,000 sq ft Ohio plant now produces canned and powdered formula under strict microbiological controls. Canada's harmonized provincial EPR network incentivizes design-for-recycling across flexible and rigid formats alike, sustaining steady innovation.

- Amcor PLC

- Tetra Laval Group

- Mondi Group

- Berry Global Inc. (incl. former RPC)

- Silgan Holdings Inc.

- Sonoco Products Company

- Ardagh Group

- Winpak Ltd

- DS Smith PLC

- SIG Combibloc Group

- Cheer Pack North America

- Gualapack Group

- Scholle IPN

- UFlex Ltd

- ProAmpac LLC

- Huhtamaki Oyj

- AptarGroup Inc.

- Plastipak Packaging Inc.

- Crown Holdings Inc.

- Sealed Air Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Convenience-driven adoption of baby food pouches

- 4.2.2 Urban dual-income households demanding time-saving formats

- 4.2.3 Stricter infant-safety regulations expanding premium packaging

- 4.2.4 Aseptic spouted-pouch filling lines gaining ground

- 4.2.5 Extended-producer-responsibility incentives for recyclability

- 4.2.6 AI-led personalised-nutrition pack design innovations

- 4.3 Market Restraints

- 4.3.1 Plastics sustainability backlash and legislation

- 4.3.2 BPA/chemicals compliance cost pressures

- 4.3.3 Supply bottlenecks of pharma-grade spout resins

- 4.3.4 DIY baby-food trend reducing packaged demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Paperboard

- 5.1.3 Metal

- 5.1.4 Glass

- 5.1.5 Bioplastics

- 5.2 By Package Type

- 5.2.1 Bottles

- 5.2.2 Cartons

- 5.2.3 Jars

- 5.2.4 Pouches

- 5.2.5 Bag-in-Box

- 5.3 By Product

- 5.3.1 Liquid Milk Formula

- 5.3.2 Dried Baby Food

- 5.3.3 Powder Milk Formula

- 5.3.4 Prepared Baby Food

- 5.3.5 Baby Snacks

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Southeast Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Egypt

- 5.4.5.2.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Tetra Laval Group

- 6.4.3 Mondi Group

- 6.4.4 Berry Global Inc. (incl. former RPC)

- 6.4.5 Silgan Holdings Inc.

- 6.4.6 Sonoco Products Company

- 6.4.7 Ardagh Group

- 6.4.8 Winpak Ltd

- 6.4.9 DS Smith PLC

- 6.4.10 SIG Combibloc Group

- 6.4.11 Cheer Pack North America

- 6.4.12 Gualapack Group

- 6.4.13 Scholle IPN

- 6.4.14 UFlex Ltd

- 6.4.15 ProAmpac LLC

- 6.4.16 Huhtamaki Oyj

- 6.4.17 AptarGroup Inc.

- 6.4.18 Plastipak Packaging Inc.

- 6.4.19 Crown Holdings Inc.

- 6.4.20 Sealed Air Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment