|

시장보고서

상품코드

1851513

보호 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Protective Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

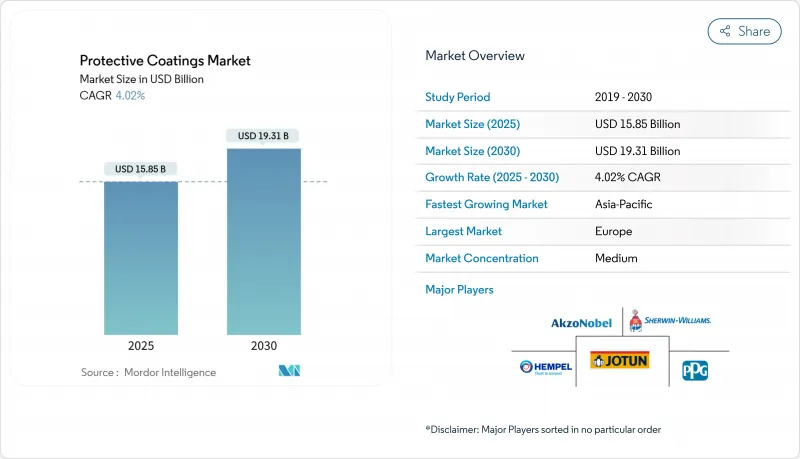

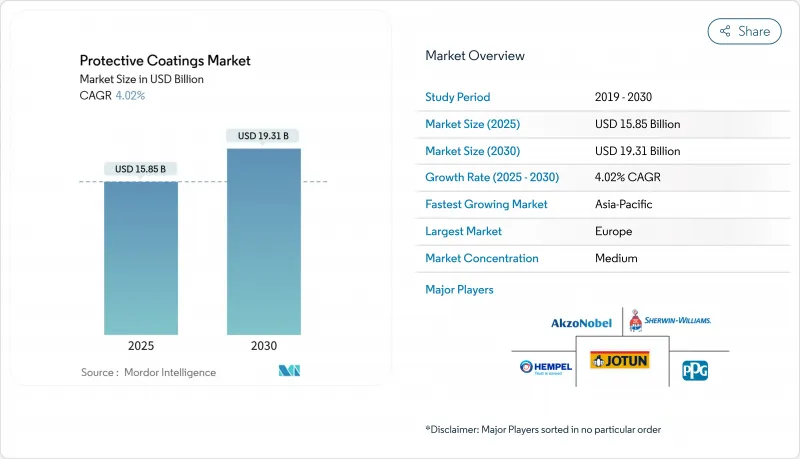

보호 코팅 시장 규모는 2025년에 158억 5,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 4.02%로, 2030년에는 193억 1,000만 달러에 달할 것으로 예상됩니다.

엄격한 환경 규제와 엄청난 인프라 지출을 지원하는 유럽이 가장 큰 점유율을 차지하며, 아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)로 가장 빠른 5.23%를 나타낼 것으로 예상됩니다. 인프라 정비, 환경친화적인 화학물질로의 전환, 재생가능에너지 및 자동차 경량화의 채용 증가가 가장 영향력 있는 성장 촉진요인입니다. 폴리우레탄 제품은 수지 수요를 선도하고, 용매계 화학물질은 VOC의 압력에도 불구하고 여전히 우세하며, 나노기술은 자기 복구와 스마트 표면의 새로운 지평을 열고 있습니다. 최상위 공급업체 간의 산업 재구성은 계속되고 있지만, 신흥 경제 국가 및 플라스틱 및 복합 기판을 위한 첨단 솔루션에는 백스페이스 기회가 남아 있습니다.

세계의 보호 코팅 시장 동향과 인사이트

인프라 건설 투자 증가

보호 코팅 시장을 지원하는 것은 교통, 에너지 및 시민 프로젝트에 대한 대규모 공공 투자입니다. 미국 인프라 투자·고용촉진법(Infrastructure Investment and Jobs Act)만으로도 다리와 도로 복구에 수십억 달러의 자금이 투입되어 긴 수명 방식 시스템 수요를 끌어올리고 있습니다. 중국, 인도, 유럽연합(EU)에서도 같은 프로그램이 실시되어 고성능의 배합이 선호되는 내구성의 의무화가 진행되고 있습니다. 자산 소유자는 초기 비용보다 라이프사이클의 경제성을 강조하는 경향이 커지고 있으며 유지보수 간격을 연장한 프리미엄 등급이 요구되고 있습니다. 이 때문에 폴리우레탄이나 진클리치 에폭시계는 강교와 철근 노출 콘크리트로 사양의 우선도를 높이고 있습니다. 염분, 습도 및 온도 사이클이 열화를 가속화하는 해안 지역에서는 시장의 이점이 더욱 커집니다.

증가하는 녹색 코팅 수요

VOC 배출량의 상한 규제는 해마다 강화되고 있으며, 특히 캘리포니아주 대기자원위원회의 규제치는 이제 세계적인 기준 벤치마크가 되고 있습니다. 배합 제조업체는 수계, 하이솔리드계, 분체계 등, 기존 용제계 제품과 동등한 내식성을 나타내는 제품으로 대응하고 있습니다. 또한 친환경 대체 제품은 자산 소유자가 기업의 지속가능성에 대한 맹세를 달성하는 데 도움이 됩니다. 보호 코팅 시장에서는 바이오 폴리우레탄 디스퍼전과 저에너지 큐어 파우더 블렌드의 급속한 스케일 업을 볼 수 있습니다. 기술 개발의 초점은 광택과 기계적 성능을 유지하면서 건조 시간을 단축하는 수지 개질입니다. 경쟁사와의 차별화는 물리적 특성뿐만 아니라 정량화 가능한 환경 실적가 점점 더 중요해지고 있습니다.

VOC 배출에 관한 규제

VOC의 상한 규제가 강화되면 재제조를 강요하고 원재료 비용을 증가시켜 생산 공장의 설비 갱신을 강요합니다. 또한 법규 규정 준수는 최종 사용자와 자격을 주기 사이클을 늘릴 수 있지만 궁극적으로 수성 또는 분말 기술을 활용하는 공급업체에게 유리합니다. 자산 소유자가 보다 환경친화적인 표준으로 축발을 옮기고 솔벤트 등급의 단계적 폐지로 인한 수익 감소를 완화함으로써 조기 진출기업은 점유율을 얻습니다. 시간이 지남에 따라 기술 혁신은 마진의 대부분의 감소를 상쇄하고 표준에 맞는 생산자를 우선 파트너로 자리 매김합니다.

부문 분석

2024년 폴리우레탄은 매출의 30.34%를 차지하며 인프라, 자동차, 에너지 자산의 탁월한 유연성을 반영했습니다. 이 부문은 2030년까지 연평균 복합 성장률(CAGR) 4.79%를 나타낼 것으로 예상되며, 이는 수지 중 가장 빠릅니다. 이러한 진보로 자산 소유자는 높은 내마모성과 긴 외장 내구성을 보여주는 시스템으로 이어지므로 보호 코팅 시장에서 폴리우레탄의 점유율이 증가합니다. 바이오 폴리올 및 습기 경화형 폴리올의 발전은 성능을 희생하지 않고 환경 프로파일을 더욱 향상시킵니다. 또, 탄성률의 밸런스와 내침식성이 중요해지는 해상 풍력 터빈의 블레이드 첨단 보호재가 급속하게 보급되고 있는 것도, 수요의 추풍이 되고 있습니다.

고고형분 및 감수성 등급은 경쟁 분야를 재형성합니다. 냄비 수명과 광택 유지성을 희생하지 않고 폴리우레탄을 배합할 수 있는 공급업체는 솔벤트 기반 에폭시에서 마이그레이션하는 프로젝트에서 점유율을 얻고 있습니다. 한편, 나노실리카와 그래핀 첨가제는 내스크래치성과 열안정성을 높여 자동차용 클리어코트의 매력을 높여줍니다. 그 결과 폴리우레탄 부문은 2030년까지 수지의 보호 코팅 시장 규모에서 차지하는 비율이 더욱 커질 것으로 예측됩니다.

솔벤트 시스템은 2024년 매출의 71.59%를 차지하며 가혹한 환경 조건 하에서 비교할 수 없는 코팅 형성을 반영합니다. 해양 플랫폼, 화학 플랜트 및 파이프라인의 유지보수용 페인트는 자산의 다운타임 비용이 환경 컴플라이언스 비용을 능가하기 때문에 솔벤트 시스템이 주류가 되고 있습니다. 규제의 역풍에도 불구하고 솔벤트 시스템은 2030년까지 상당한 시장 규모를 유지합니다. 하지만 배리어성을 높이고 건조를 촉진하는 수지 합성의 돌파구에 도움이 되며 수성 라인은 CAGR 4.58%로 가장 역동적인 궤도를 그립니다. 분말 기술은 또한 제로 VOC 인증과 오버 스프레이의 재활용 가능성을 활용하여 가공 스틸, 알루미늄 형재 및 소비자 장비 분야에서 발자국을 늘리고 있습니다.

지역 분석

지속가능성 정책과 건축 환경의 노후화가 융합되어 보호 코팅의 보급을 뒷받침하고 있습니다. 엄격한 REACH 규정은 수계 및 고 솔리드 처방의 채택을 뒷받침하고 공급업체는보다 환경 친화적인 화학 물질에 대한 투자를 강요하고 있습니다.

아시아태평양은 도시화와 산업 확대가 이어지는 가운데 가장 빠르게 도포량이 증가하고 있습니다. 중국은 보호 코팅 수요를 고속 철도 궤도 부지, 석유 화학 조합, 거대한 조선소로 향하고 있습니다. 또한, 내륙 수로의 교량을 업그레이드하는 지방의 대처도, 개수 사이클을 확대하고 있습니다. 인도에서는 국가 인프라 파이프라인(National Infrastructure Pipeline)이 이 궤적을 반영하고 부식 방지 시스템을 위한 철강과 콘크리트 표면적이 크게 증가하고 있습니다.

북미는 중간 위치를 차지하고 있지만, 하이스펙 기술에서는 매우 중요한 위치를 차지하고 있습니다. 미국의 인프라 패키지는 노후화된 주간 다리, 공항, 담수 시스템에 자본을 유도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 인프라 건설투자 증가

- 확대하는 그린 코팅 수요

- 자동차 산업으로부터의 이용 확대

- 신에너지 분야 수요 증가

- 해양산업으로부터의 소비 증가

- 시장 성장 억제요인

- VOC 배출규제

- 특정 지역에서의 숙련 노동자의 부족

- 변동하는 원재료 가격

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 수지 유형별

- 에폭시

- 폴리우레탄

- 비닐에스터

- 폴리에스터

- 알키드

- 기타 수지(아크릴, 아연 함유 등)

- 기술별

- 용제

- 수성

- 분체

- 기타 기술(하이솔리드, UV 경화 등)

- 기재별

- 금속

- 콘크리트

- 플라스틱 및 복합재료

- 기타 기재(목재, 유리 등)

- 최종 이용 산업별

- 석유 및 가스

- 파이프라인(수소 파이프라인 포함)

- 기타

- 광업

- 전력

- 풍력에너지

- 기타 발전 부문

- 인프라

- 수처리

- 배관망(식수 및 폐수 배출)

- 담수화 및 식수 처리

- 산업용 수자원 인프라

- 기타 최종 사용자 산업(화학 및 석유화학, 자동차, 해양)

- 석유 및 가스

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 전략적 동향

- 시장 점유율(%) 분석

- 기업 프로파일

- Advanced Polymer Coatings

- Akzo Nobel NV

- Asian Paints PPG Pvt. Ltd.

- Axalta Coating Systems, LLC

- BASF

- Belzona International Ltd.

- Berger Paints India

- Chugoku Marine Paints, Ltd.

- DuluxGroup Ltd.

- Hempel A/S

- Jotun

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tikkurila

제7장 시장 기회와 향후 전망

KTH 25.11.21The Protective Coatings Market size is estimated at USD 15.85 billion in 2025, and is expected to reach USD 19.31 billion by 2030, at a CAGR of 4.02% during the forecast period (2025-2030).

Europe commanded the largest share, sustained by rigorous environmental rules and sizable infrastructure outlays, while Asia-Pacific is projected to record the fastest 5.23% CAGR through 2030. Infrastructure development, the transition toward eco-friendly chemistries, and rising adoption in renewable energy and automotive lightweighting are the most influential growth drivers. Polyurethane products lead resin demand, solvent-borne chemistries still prevail despite VOC pressure, and nanotechnology is opening new horizons for self-healing and smart surfaces. Industry consolidation among top suppliers continues, yet white-space opportunities persist in emerging economies and in advanced solutions for plastic and composite substrates.

Global Protective Coatings Market Trends and Insights

Increasing Investments in Infrastructure Construction

Massive public spending on transport, energy, and civic projects underpins the protective coatings market. The United States Infrastructure Investment and Jobs Act alone is injecting multibillion-dollar capital into bridge and road rehabilitation, boosting demand for long-life anticorrosive systems. Similar programs in China, India, and the European Union converge on durability mandates that favor high-performance formulations. Asset owners increasingly weigh lifecycle economics over upfront cost, translating into premium grades with extended maintenance intervals. Polyurethane and zinc-rich epoxy systems are thus gaining specification priority in steel bridges and rebar-exposed concrete. The market benefit is magnified in coastal regions where salt, humidity, and temperature cycling accelerate degradation.

Growing Green Coatings Demand

Regulations capping VOC emissions tighten year by year, especially under California Air Resources Board limits that now set reference benchmarks worldwide. Formulators respond with waterborne, high-solids, and powder chemistries demonstrating parity in corrosion resistance with legacy solvent products. Eco-friendly alternatives also help asset owners meet corporate sustainability pledges. The protective coatings market sees rapid scale-up of bio-based polyurethane dispersions and low-energy-cure powder blends. Technology development focuses on resin modifications that shorten drying time while sustaining gloss and mechanical performance. Competitive differentiation increasingly rests on quantifiable environmental footprints rather than solely on physical properties.

Regulations Related to VOC Emissions

Stricter VOC caps force reformulation, drive raw-material cost inflation, and compel capital upgrades in production plants. Compliance also prolongs qualification cycles with end users but eventually favors suppliers that master water-borne or powder technologies. Early movers capture share as asset owners pivot to greener standards, cushioning revenue loss from solvent-grade phase-outs. Over time, innovation offsets most margin erosion and positions compliant producers as preferred partners.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Utilization from the Automotive Industry

- Growing Demand from the New Energy Sector

- Skilled Labor Shortage in Certain Geographies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, polyurethane captured 30.34% of revenue, reflecting unparalleled flexibility across infrastructure, automotive, and energy assets. The segment is forecast to expand at a 4.79% CAGR through 2030, the fastest among resins. These advance lifts the polyurethane share of the protective coatings market as asset owners gravitate to systems exhibiting high abrasion resistance and long exterior durability. Advancements in bio-based polyols and moisture-cure variants further improve environmental profiles without sacrificing performance. Demand also benefits from rapid uptake in blade leading-edge protection for offshore wind turbines, where elastic moduli balance and erosion resistance are critical.

High solids and water-reducible grades reshape the competitive field. Suppliers that can formulate polyurethane without sacrificing pot life or gloss retention gain share in projects migrating away from solvent-based epoxies. Meanwhile, nano-silica and graphene additives raise scratch resistance and thermal stability, heightening appeal in automotive clearcoats. As a result, the polyurethane segment is set to account for an even larger slice of the protective coatings market size for resins by 2030.

Solvent-borne systems held 71.59% of sales in 2024, reflecting unmatched film formation under extreme ambient conditions. They dominate maintenance coatings on offshore platforms, chemical plants, and pipelines where asset downtime costs eclipse environmental compliance fees. Despite regulatory headwinds, the protective coatings market maintains a sizable solvent-borne volume through 2030 because no alternate cures reliably at very low temperatures or high humidity. Nevertheless, waterborne lines chart the most dynamic trajectory with a 4.58% CAGR, aided by resin synthesis breakthroughs that enhance barrier properties and accelerate drying. Powder technology also expands footprints in fabricated steel, aluminum profiles, and consumer equipment, leveraging zero-VOC credentials and recyclability of overspray.

The Protective Coatings Market Report Segments the Industry by Resin Type (Epoxy, Polyurethane, Vinyl Ester, Polyester, and More), Technology (Solvent-Borne, Water-Borne, Powder, and Other Technologies), Substrate (Metal, Concrete, and More), End-User Industry (Oil and Gas, Mining, Power, Infrastructure, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Europe remained the principal regional stronghold in 2024 with a 50.37% share of the market, as sustainability policy blended with an aging built environment to drive protective coating uptake. Stringent REACH regulations turbocharge the adoption of waterborne and high-solids formulations, compelling suppliers to invest in greener chemistries.

Asia-Pacific delivers the swiftest volume escalation as urbanization and industrial expansion persist. China channels protective coating demand into high-speed rail track beds, petrochemical complexes, and massive shipyards. Provincial initiatives to upgrade inland waterway bridges also enlarge refurbishment cycles. India mirrors this trajectory with its National Infrastructure Pipeline, creating substantial steel and concrete surface areas for corrosion control systems.

North America occupies an intermediate position yet remains pivotal for high-specification technologies. United States infrastructure packages direct capital toward aging interstate bridges, airports, and freshwater systems.

- Advanced Polymer Coatings

- Akzo Nobel N.V.

- Asian Paints PPG Pvt. Ltd.

- Axalta Coating Systems, LLC

- BASF

- Belzona International Ltd.

- Berger Paints India

- Chugoku Marine Paints, Ltd.

- DuluxGroup Ltd.

- Hempel A/S

- Jotun

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Investments in Infrastructure Construction

- 4.2.2 Growing Green Coatings Demand

- 4.2.3 Increasing Utilzation from the Automotive Industry

- 4.2.4 Growing Demand from the New Energy Sector

- 4.2.5 Rising Consumption from the Marine Industry

- 4.3 Market Restraints

- 4.3.1 Regulations Related to VOC Emissions

- 4.3.2 Skilled Labor Shortage in Certain Geographies

- 4.3.3 Fluctuating Raw Material Prices

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Vinyl Ester

- 5.1.4 Polyester

- 5.1.5 Alkyd

- 5.1.6 Other Resins (Acrylic. Zinc-Rich, etc.)

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.2.3 Powder

- 5.2.4 Other Technologies (High-Solids, UV-Cured, etc.)

- 5.3 By Substrate

- 5.3.1 Metal

- 5.3.2 Concrete

- 5.3.3 Plastic and Composites

- 5.3.4 Other Substrates (Wood, Glass, etc)

- 5.4 By End-use Industry

- 5.4.1 Oil and Gas

- 5.4.1.1 Pipeline (incl. Hydrogen Pipeline)

- 5.4.1.2 Others

- 5.4.2 Mining

- 5.4.3 Power

- 5.4.3.1 Wind Energy

- 5.4.3.2 Other Power Generating Sectors

- 5.4.4 Infrastructure

- 5.4.5 Water Treatment

- 5.4.5.1 Distribution Pipeline (potable Water and Wastewater Discharge)

- 5.4.5.2 Desalination and Potable Water Treatment

- 5.4.5.3 Industrial Water Infrastructure

- 5.4.6 Other End-User Industries(Chemicals and Petrochemicals, Automotive, Marine)

- 5.4.1 Oil and Gas

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share(%) Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Advanced Polymer Coatings

- 6.3.2 Akzo Nobel N.V.

- 6.3.3 Asian Paints PPG Pvt. Ltd.

- 6.3.4 Axalta Coating Systems, LLC

- 6.3.5 BASF

- 6.3.6 Belzona International Ltd.

- 6.3.7 Berger Paints India

- 6.3.8 Chugoku Marine Paints, Ltd.

- 6.3.9 DuluxGroup Ltd.

- 6.3.10 Hempel A/S

- 6.3.11 Jotun

- 6.3.12 Kansai Paint Co.,Ltd.

- 6.3.13 Nippon Paint Holdings Co., Ltd.

- 6.3.14 PPG Industries, Inc.

- 6.3.15 RPM International Inc.

- 6.3.16 Sika AG

- 6.3.17 Teknos Group

- 6.3.18 The Sherwin-Williams Company

- 6.3.19 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Nano-engineered Smart Self-healing Coatings

- 7.3 Bio-based Resin Systems for Offshore Wind Towers