|

시장보고서

상품코드

1851567

eClinical 솔루션 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)EClinical Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

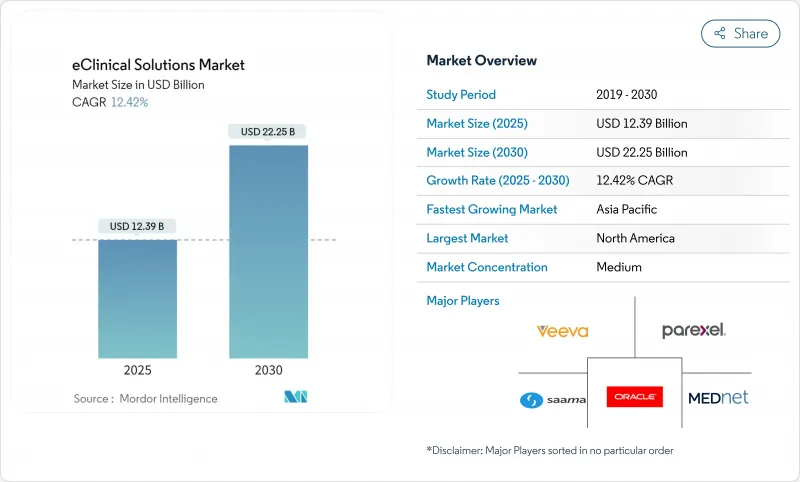

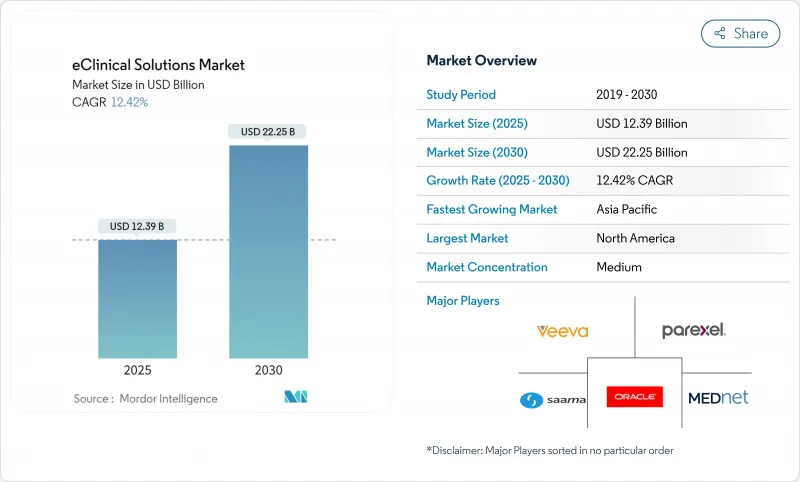

eClinical 솔루션 시장은 2025년에 123억 9,000만 달러에 이르고 2030년에는 222억 5,000만 달러에 달할 전망입니다.

런 레이트는 완전한 디지털 임상시험이 선택적 효율성에서 경쟁약 개발의 핵심 요건으로 바뀌었음을 보여줍니다. 스폰서는 현재 대규모 멀티모달 데이터세트를 보다 세계한 시설로 전송하고 보다 엄격한 정보 공개 마감일에 직면하고 있기 때문에 고급 캡처, 모니터링 및 분석 시스템이 필수적입니다. 분산형 임상시험과 하이브리드 임상시험이 긴급회피책에서 주류설계로 이행하고 참가자, 모니터, 통계담당자, 규제당국을 연결하는 통합플랫폼에 대한 수요가 가속화되는 가운데 거의 실시간 연결성은 더욱 가치를 늘리고 있습니다. Tier-1 공급업체는 전자 데이터 수집(EDC), 전자 임상 결과 평가(eCOA), 무작위화 및 시험 약물 공급 관리(RTSM), 안전 보고서를 단일 계약으로 번들로 제공하므로 가격 역학은 시험 수명주기에 적합하며 보다 슬림한 생명공학 예산을 지원하는 구독 모델을 지원합니다.

세계의 eClinical 솔루션 시장 동향과 인사이트

의료 산업의 방대한 데이터 양

임상시험 데이터의 양이 급증하고 스폰서는 자동화된 품질 검사, 자연어 처리, 예측 분석을 핵심 EDC 플랫폼에 직접 통합합니다. IQVIA의 보고에 따르면 AI에 의한 비구조화된 소스를 검토하면 감사 대응 능력을 유지하면서 데이터 클리닝 사이클을 반감할 수 있습니다. 그 결과 데이터 사이언스 팀은 단순히 첫 번째 환자가 들어온 후가 아니라 프로토콜 구축 중에 참여하고 하류 상호 운용성을 보장합니다. 클라우드 스토리지 예산은 탄력적인 용량이 하드웨어 구매 사이클을 초과함에 따라 On-Premise 지출을 초과합니다. 한때 틈새였던 해석의 프레임워크가 이제는 염증과 대사의 파이프라인 전체에서 재현되게 되었습니다. 피험자 1인당 데이터가 증가함에 따라 eClinical 솔루션 시장은 치료 영역의 초점에 의존하지 않는 안정적인 돌풍을 얻는다.

임상시험에서 소프트웨어 솔루션 채택 확대

스폰서는 일상적으로 하나의 시험에 대해 3개 이상의 개별 eClinical 솔루션 용도를 사용하지만, 단편 로그인과 동기화되지 않은 데이터 흐름이 명확한 병목 현상이 됩니다. Veeva의 2025년 로드맵은 시작, 모니터링 및 신청 워크플로우를 통합하는 싱글 사인온 환경에 대한 수요 증가를 소개합니다. 조기 도입 기업은 모듈 간의 중복 데이터 입력을 없애고 검증 비용을 줄일 수 있으므로 프로토콜의 최종화 사이클이 크게 단축된다고 보고했습니다. 통합된 제품군은 현재 최고의 블리드 구매를 능가하고 있으며, 거버넌스 팀은 수작업 쿼리에서 고급 통계 프로그래밍으로 인력을 이동할 수 있습니다. 그 결과 플랫폼의 다년간 계약이 증가하고 eClinical 솔루션 시장에서 산발적인 라이선스 비용이 예측 가능한 SaaS 수익으로 전환되었습니다.

높은 도입 비용

종합적인 플랫폼 롤아웃은 검증, 통합 및 다중 사용자 교육을 고려할 때 7자리 이상의 예산을 필요로 합니다. Merative의 벤치마크에 의하면, 자금이 반복되는 엄격한 스폰서는 단계적인 도입을 채용하고 있어, 우선 코어가 되는 EDC를 도입해, 나중에 RTSM이나 eTMF를 레이어화하고 있습니다. 단계적인 도입은 초기 비용을 억제할 수 있는 반면 프로젝트의 스케줄을 연장하고 완전한 스위트가 가져오는 생산성의 향상을 늦추게 됩니다. 따라서 유연한 소비 기반 가격을 제공하는 공급업체는 디지털화를 앞당기고 있던 고객을 확보할 수 있습니다. 그럼에도 불구하고 진입 비용은 여전히 중소 생명 공학 기업과 학술 후원자들에게 무거워지며 자원에 제한이있는 환경에서 eClinical 솔루션 시장의 성장을 억제하고 있습니다.

부문 분석

2024년 eClinical 솔루션 시장 규모는 전자 데이터 수집 및 임상 데이터 관리 시스템이 최대이며, 시험 시작 시 보편적인 배포로 총 매출의 33.13%를 차지했습니다. 스폰서가 시스템에 익숙해지고 중간 분석 전에 이상을 알리는 위험 기반 통합 모니터링 대시보드를 높이 평가하므로 라이선스 업데이트는 여전히 높은 수준에 있습니다. 시장은 현재 기본 데이터 입력보다 통합된 예측 쿼리에 가치를 두고 있으며, 프리미엄 가격을 요구하는 AI를 통합한 업그레이드로의 전환을 창출하고 있습니다. EDC를 RTSM 및 안전 모듈과 사전 통합한 공급업체는 스위칭 비용을 더욱 높여 리더로서의 입지를 강화하고 있습니다.

전자 임상 결과 평가 플랫폼은 가장 급속히 확장된 하위 부문이며, 환자 중심주의가 리트릭에서 요건으로 이동함에 따라 2030년까지의 CAGR은 15.24%를 나타낼 것으로 예상됩니다. Medable 장비 빌더는 심리 측정 및 QOL 도구를 드래그 앤 드롭으로 만들 수 있으며 수동으로 매핑하지 않고 EDC 테이블에 직접 입력할 수 있습니다. 스폰서는 원활한 핸드 오프를 높이 평가합니다. 이는 조정 주기를 몇 주간 단축하고 실시간 대시보드 검토를 지원하기 때문입니다. 분산형 임상시험이 보급됨에 따라 eCOA 기능이 플랫폼 선택 전체의 결정수가 되는 경우가 많아 eClinical 솔루션 시장 내 풀 스위트 벤더의 수익 증가를 뒷받침하고 있습니다.

클라우드 기반 배포는 2024년 딜리버리 모드별 eClinical 솔루션 시장 점유율에서 48.62%로 최대를 차지했고, 2030년까지의 CAGR은 14.58%를 나타낼 전망입니다. 멀티 테넌트의 SaaS 모델은 즉각적인 확장성, 자동 버전 업그레이드 및 감사 로그를 제공하며, 규제 당국은 On-Premise 관리와 동등한 것으로 간주되고 있습니다. 자사 소유 하드웨어에서 마이그레이션하는 스폰서는 유지보수 시간을 2자리 줄이고 IT 팀을 분석 업무로 돌릴 수 있습니다. 진입 비용 절감은 소규모 생명공학 스폰서가 테스트 마일스톤에 맞게 캐시 번을 유지하는 데 도움이 되어 클라우드 견인력을 강화하고 있습니다.

웹 호스트의 단일 테넌트 환경은 30% 중반의 점유율을 유지하며 멀티 테넌트 아키텍처로의 마이그레이션에 꺼린 조직의 마이그레이션 옵션 역할을 합니다. 이러한 환경은 인프라 소유의 부담을 줄이면서도 위험 회피를 선호하는 품질 그룹에게 선호되는 격리를 제공합니다. 그러나 최근 테넌트 수준의 암호화와 전용 키 관리의 발전은 웹 호스팅과 SaaS의 보안 격차를 줄이고 있습니다. 앞으로 멀티테넌트형으로의 전환이 진행될 것으로 예상되지만 보수적인 스폰서는 eClinical 솔루션 시장에서 웹 호스팅형 벤더를 유지하는 틈새를 유지할 것으로 보입니다.

지역 분석

북미는 2024년 최대의 eClinical 솔루션 시장 규모를 유지해 세계 매출의 49.11%에 기여했습니다. 그 이유는 풍부한 자본 수영장, 디지털 서명의 조기 규제 수용, 경험이 풍부한 시험 시설의 밀집에 있습니다. 공급업체는 미국과 캐나다에서 새로운 AI 모듈을 처음 출시하는 경우가 많습니다. 이는 현지 데이터 거버넌스 규범이 빠른 반복을 지원하기 때문입니다. 시장이 성숙함에도 불구하고 스폰서는 기존의 On-Premise 도입을 SaaS로 전환하고 검사 준비를 가속화하는 고급 분석을 추구하고 있기 때문에 2자리대 업데이트 성장이 계속되고 있습니다.

아시아태평양은 가장 빠른 성장 궤도를 나타내며 2030년까지의 CAGR은 14.84%를 나타낼 것으로 예상됩니다. 이는 세계 스폰서가 대규모 환자 수영장과 비용 효율적인 시설 네트워크에 대한 액세스를 요청하여 모집을 동쪽으로 이동하기 때문입니다. 중국, 한국, 인도 정부는 국내 바이오파마를 적극적으로 지원하고 도입 장애물을 낮추는 클라우드 인프라 보조금을 제공합니다. 각 지역의 벤더는 현지 언어와 개인정보보호법에 맞게 인터페이스를 미세조정하고, 구미의 기존 벤더에 대한 경쟁압력을 높이고, eClinical 솔루션 시장 내공급업체 기반을 다양화하고 있습니다.

유럽은 세계 매출의 약 4분의 1을 차지하고 있으며, EU 임상시험규칙에 따른 하모나이제이션의 혜택을 받아 여러 국가에 대한 신청이 효율화되고 있습니다. 이 지역의 엄격한 데이터 프라이버시 규칙은 나중에 전 세계적으로 배포되는 보안 기능의 실험실 역할을 합니다. 독일, 북유럽, 네덜란드에서는 전자 환자 일지와 eConsent의 채용이 증가하고 있으며 환자 기술에 대한 문화적 수용성을 보여줍니다. 규제 당국의 감시가 어려워지면 판매주기가 길어지면서 스폰서가 플랫폼의 범위에 컴플라이언스에 관한 헌신을 통합하기 때문에 장기적인 계약 가치가 높아집니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 헬스케어 업계로부터의 방대한 데이터 수집

- 확장 가능한 클라우드 플랫폼을 필요로 하는 APAC에서 2단계/3단계 종양 테스트 급증

- 임상시험에서 소프트웨어 솔루션 도입 확대

- 확대하는 바이오의약품의 연구개발투자

- 환자 중심·분산형 모델로의 급속한 변화

- 세계 임상시험활동 확대

- 시장 성장 억제요인

- 높은 도입 비용

- 레거시 모듈과 최신 e클리니컬 모듈 간의 데이터 상호 운용성의 갭

- 신흥 시장에서의 인증 클리니컬 데이터 매니저의 부족

- 높아지는 사이버 보안과 환자 데이터 유출의 우려

- 밸류체인 분석

- 규제와 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 전자 데이터 수집(EDC) 및 임상 데이터 관리 시스템(CDMS)

- 임상 시험 관리 시스템(CTMS)

- 무작위 배정 및 시험 공급 관리(IRT/RTSM)

- 전자 임상 결과 평가(eCOA/ePRO)

- 임상 분석 및 데이터 통합 플랫폼

- 안전성 및 약물 감시 솔루션

- 전자 시험 마스터 파일(eTMF)

- 기타 제품

- 배포 모드별

- 클라우드 기반(SaaS)

- 웹 호스팅(온디맨드)

- On-Premise

- 임상시험 Phase별

- Phase I

- Phase II

- Phase III

- Phase IV

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 계약 연구 기관(CRO)

- 의료기기 제조업체

- 학술 및 연구 기관

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 남아프리카

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Oracle Corporation

- Dassault Systemes(Medidata Solutions)

- Veeva Systems

- Clario(BioClinica)

- IQVIA Holdings Inc.

- PAREXEL International(Calyx)

- Covance(Labcorp Drug Development)

- Signant Health

- eClinical Solutions LLC

- Saama Technologies, Inc.

- Datatrak International Inc.

- Medrio, Inc.

- Castor EDC

- Mednet Solutions

- ArisGlobal

- Anju Software Inc.

- MasterControl, Inc.

- OpenClinica, LLC

- ClinCapture, Inc.

- Medable Inc.

- TransPerfect Life Sciences

제7장 시장 기회와 향후 전망

KTH 25.11.21The eClinical solutions market touched USD 12.39 billion in 2025 and is on track to reach USD 22.25 billion by 2030, reflecting a firm 12.42% CAGR that continues even under restrained funding scenarios.

The run-rate shows how fully digital trial execution has shifted from an optional efficiency play to a core requirement for competitive drug development. Sponsors now transmit larger, multi-modal data sets across more global sites and face tighter disclosure windows, making sophisticated capture, monitoring, and analytics systems indispensable. Near-real-time connectivity has become even more valuable as decentralized and hybrid trials move from emergency workaround to mainstream design, accelerating demand for unified platforms that connect participants, monitors, statisticians, and regulators. As Tier-1 vendors bundle electronic data capture (EDC), electronic clinical outcome assessment (eCOA), randomization and trial-supply management (RTSM), and safety reporting under single contracts, pricing dynamics favor subscription models that match study life cycles and support slimmer biotech budgets, implying that platform completeness rather than lowest point cost will decide future purchasing.

Global EClinical Solutions Market Trends and Insights

Enormous Data Mounting from Healthcare Industry

The volume of trial data has climbed steeply, prompting sponsors to embed automated quality checks, natural-language processing, and predictive analytics directly inside core EDC platforms. IQVIA reports that AI-driven review of unstructured sources halves data-cleaning cycles while preserving audit readiness. In turn, data-science teams are now engaged during protocol build, not merely after first-patient-in, ensuring downstream interoperability. Cloud storage budgets therefore outpace on-premise outlays as elastic capacity overtakes hardware purchase cycles. Oncology studies provide the blueprint: once niche, their analytics frameworks now replicate across inflammatory and metabolic pipelines. As data per subject multiplies, the eClinical solutions market gains a stable tailwind that is independent of therapeutic area focus.

Growing Incorporation of Software Solutions in Clinical Trial

Sponsors routinely juggle three or more discrete eClinical applications per study, yet fragmented log-ins and unsynchronized data flows have become a clear bottleneck. Veeva's 2025 roadmap showcases rising demand for single sign-on environments that merge start-up, monitoring, and submission workflows . Early adopters report materially shorter protocol-finalization cycles because duplicate data entry disappears between modules, reducing validation cost as well. Consolidated suites now outperform best-of-breed purchasing, allowing governance teams to shift head-count from manual queries to advanced statistical programming. The observable outcome is a rise in multiyear platform contracts, which converts sporadic license spend into predictable SaaS revenue inside the eClinical solutions market.

High Implementation Costs

Comprehensive platform roll-outs frequently require budgets well into seven figures once validation, integration, and multi-user training are considered. Merative benchmarks show that sponsors with tight treasury adopt phased deployment, starting with a core EDC and layering RTSM or eTMF later. While the staged path trims initial outlay, it extends project timelines, delaying productivity gains that full suites deliver. Vendors offering flexible, consumption-based pricing therefore capture accounts that might otherwise postpone digitization. Nevertheless, high entry costs still weigh on smaller biotech and academic sponsors, tempering eClinical solutions market growth in resource-constrained settings.

Other drivers and restraints analyzed in the detailed report include:

- Growing Biopharma R&D Investment

- Rapid Shift Toward Patient-Centric and Decentralized Models

- Expansion of Global Clinical Trial Activities

- Shortage of Certified Clinical Data Managers in Emerging Markets

- Escalating Cyber-security & Patient-Data Breach Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electronic data capture and clinical data management systems controlled the largest eClinical solutions market size in 2024, contributing 33.13% of total revenue on the strength of universal deployment at study start-up. License renewals remain high because sponsors prize system familiarity and integrated risk-based monitoring dashboards that flag anomalies before interim analysis. The market now values embedded predictive queries more than basic data entry, creating a shift toward AI-infused upgrades that command premium pricing. Vendors that pre-integrate EDC with RTSM and safety modules further raise switching costs, cementing leadership positions.

Electronic clinical outcome assessment platforms represent the fastest expanding subsegment, expected with 15.24% CAGR through 2030 as patient centricity moves from rhetoric to requirement. Medable's instrument builder allows drag-and-drop creation of psychometric and quality-of-life tools that feed directly into EDC tables without manual mapping. Sponsors appreciate the seamless handoff because it cuts reconciliation cycles by weeks and supports real-time dashboard review. As decentralized trials proliferate, eCOA functionality often decides overall platform selection, nudging incremental revenues toward full-suite vendors inside the eClinical solutions market.

Cloud-based deployments captured the largest eClinical solutions market share by delivery mode in 2024 at 48.62% and are projected to post a 14.58% CAGR to 2030. Multi-tenant SaaS models offer immediate scalability, automatic version upgrades, and audit logs that regulators increasingly deem equivalent to on-premise controls. Sponsors migrating from owned hardware document double-digit reductions in maintenance hours, freeing IT teams for analytics work. Lower entry cost also helps smaller biotech sponsors keep cash burn aligned with trial milestones, reinforcing cloud traction.

Web-hosted, single-tenant environments maintain a resilient mid-thirty-percent share, acting as a transitional option for organizations reluctant to jump straight to multi-tenant architecture. These environments still offload infrastructure ownership yet provide perceived isolation that risk-averse quality groups favor. Recent advances in tenant-level encryption and dedicated-key management, however, narrow the security gap between web-hosted and SaaS. Over the forecast horizon, some displacement toward multi-tenant offerings is likely, but conservative sponsors will preserve a viable niche that sustains web-hosted vendors within the eClinical solutions market.

The EClinical Solutions Market Report Segments the Industry by Product (Electronic Clinical Outcome Assessment, and More), by Delivery Mode (Cloud-Based, and More), Clinical Trial Phase (Phase I, Phase III, and More), by End User (Pharmaceutical and Biotechnology Companies, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained the largest eClinical solutions market size in 2024, contributing 49.11% of global revenue due to deep capital pools, early regulatory acceptance of digital signatures, and dense clusters of experienced investigative sites. Vendors often launch new AI modules first in the United States and Canada because local data-governance norms support rapid iteration. Despite market maturity, double-digit renewal growth persists as sponsors migrate legacy on-premise deployments to SaaS and pursue advanced analytics that speed inspection readiness.

Asia-Pacific represents the fastest growth trajectory, set to register a 14.84% CAGR through 2030 as global sponsors shift recruitment eastward to access large patient pools and cost-efficient site networks. Governments in China, South Korea, and India actively champion domestic biopharma, funding cloud infrastructure grants that reduce implementation hurdles. Regional vendors fine-tune interfaces to local languages and privacy statutes, increasing competitive pressure on Western incumbents and diversifying the supplier base inside the eClinical solutions market.

Europe commands roughly one-quarter of worldwide revenue and benefits from harmonization under the EU Clinical Trials Regulation, which streamlines multi-country submissions. The region's stringent data-privacy rules function as a proving ground for security features that later roll out globally. Germany, the Nordics, and the Netherlands exhibit rising adoption of electronic patient diaries and eConsent, signaling cultural receptivity to patient-facing technology. High regulatory oversight lengthens sales cycles yet boosts long-term contract values because sponsors embed compliance commitments within platform scopes.

- Oracle

- Dassault Systemes (Medidata Solutions)

- Veeva Systems

- Clario (BioClinica)

- IQVIA

- Parexel International

- Covance (Labcorp Drug Development)

- Signant Health

- eClinical Solutions

- Saama Technologies

- Datatrak International

- Medrio

- Castor EDC

- Mednet Solutions

- Aris Global

- Anju Software Inc.

- MasterControl, Inc.

- OpenClinica, LLC

- ClinCapture, Inc.

- Medable

- TransPerfect Life Sciences -

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enormous Data Mounting from Healthcare Industry

- 4.2.2 Surge in Phase II/III Oncology Trials in APAC Requiring Scalable Cloud Platforms

- 4.2.3 Growing Incorporation of Software Solutions in Clinical Trial

- 4.2.4 Growing Biopharma R&D Investment

- 4.2.5 Rapid Shift Towards Patient-Centric and Decentralized Models

- 4.2.6 Expansion of Global Clinical Trial Activities

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs

- 4.3.2 Data Interoperability Gaps Between Legacy & Modern eClinical Modules

- 4.3.3 Shortage of Certified Clinical Data Managers in Emerging Markets

- 4.3.4 Escalating Cyber-security & Patient-Data Breach Concerns

- 4.4 Value-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Electronic Data Capture (EDC) & Clinical Data Management Systems (CDMS)

- 5.1.2 Clinical Trial Management Systems (CTMS)

- 5.1.3 Randomization & Trial Supply Management (IRT/RTSM)

- 5.1.4 Electronic Clinical Outcome Assessment (eCOA/ePRO)

- 5.1.5 Clinical Analytics & Data-Integration Platforms

- 5.1.6 Safety & Pharmacovigilance Solutions

- 5.1.7 Electronic Trial Master File (eTMF)

- 5.1.8 Other Products

- 5.2 By Delivery Mode

- 5.2.1 Cloud-based (SaaS)

- 5.2.2 Web-hosted (On-Demand)

- 5.2.3 On-premise

- 5.3 By Clinical Trial Phase

- 5.3.1 Phase I

- 5.3.2 Phase II

- 5.3.3 Phase III

- 5.3.4 Phase IV

- 5.4 By End-user

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Research Organizations (CROs)

- 5.4.3 Medical Device Manufacturers

- 5.4.4 Academic & Research Institutions

- 5.4.5 Other End-users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Oracle Corporation

- 6.3.2 Dassault Systemes (Medidata Solutions)

- 6.3.3 Veeva Systems

- 6.3.4 Clario (BioClinica)

- 6.3.5 IQVIA Holdings Inc.

- 6.3.6 PAREXEL International (Calyx)

- 6.3.7 Covance (Labcorp Drug Development)

- 6.3.8 Signant Health

- 6.3.9 eClinical Solutions LLC

- 6.3.10 Saama Technologies, Inc.

- 6.3.11 Datatrak International Inc.

- 6.3.12 Medrio, Inc.

- 6.3.13 Castor EDC

- 6.3.14 Mednet Solutions

- 6.3.15 ArisGlobal

- 6.3.16 Anju Software Inc.

- 6.3.17 MasterControl, Inc.

- 6.3.18 OpenClinica, LLC

- 6.3.19 ClinCapture, Inc.

- 6.3.20 Medable Inc.

- 6.3.21 TransPerfect Life Sciences -

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment