|

시장보고서

상품코드

1851570

반려동물 사료 포장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Pet Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

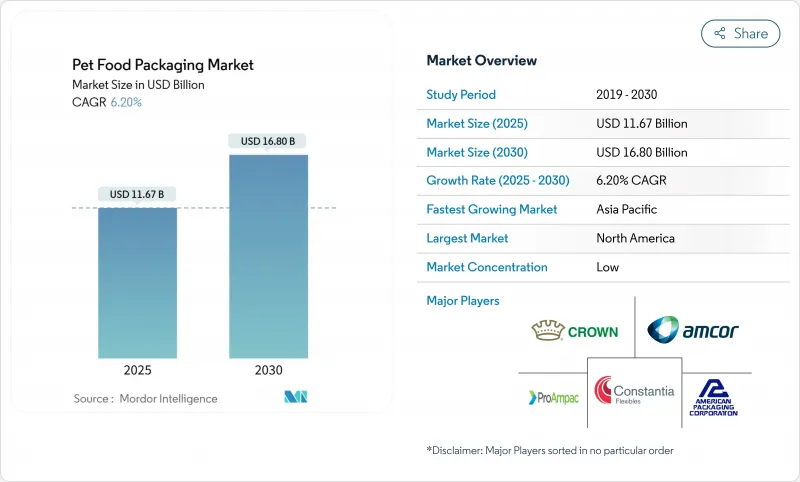

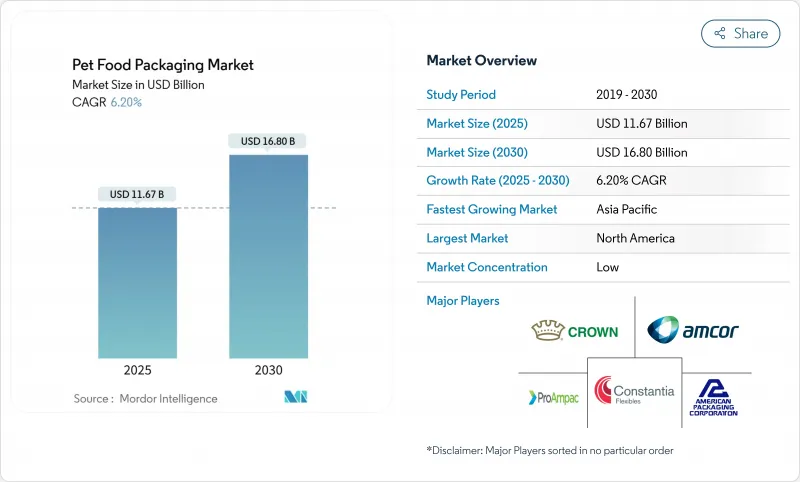

반려동물 사료 포장 시장 규모는 2025년에 116억 7,000만 달러에 이르고, 2030년에는 168억 달러로 확대되며, CAGR 6.2%를 나타낼 것으로 예측됩니다.

유럽과 미국의 규제 압력 증가, 습식 포맷의 급속한 프리미엄화, 파괴적인 재료 과학의 혁신이 결합되어 장벽 보호와 재활용성의 균형을 맞추는 솔루션에 대한 안정적인 수요 파이프라인이 형성되고 있습니다. 북미는 E-Commerce의 강력한 보급과 모노머티리얼 플렉서블의 조기 도입에 힘입어 여전히 최대의 소비지역인 반면 아시아태평양은 중국의 도시 지역에서 반려동물 사육 증가에 따라 지역별로 가장 빠른 성장을 기록하고 있습니다. 브랜드 소유자에 의한 2025년 지속가능성 약속, 원재료 변동성 상승, FDA에 의한 35개의 PFAS 식품 접촉 승인의 단계적 폐지는 컨버터가 기존의 다층 플라스틱에서 재활용 가능한 종이, 모노 PE 및 바이오 복합재로 이동할 필요성을 강화하고 있습니다. 경쟁의 격렬함은 대기업 종합 제조업체가 규모를 살리고 있기 때문에 중간 정도에 머물지만, PFAS 프리 배리어, 스마트한 포장 기능, 대기업 브랜드 오너가 점점 필요로 하는 리사이클 대응 설계 서비스 등을 제공함으로써 민첩한 전문 제조업체가 점유율을 확대하고 있습니다.

세계의 반려동물 사료 포장 시장 동향과 인사이트

SUP 지령 후 재활용 가능한 단일 소재 파우치 수요 급증

Siegwerk의 CIRKIT 코팅은 모노 PE 내부에서 그리스, 오일, 산소 보호를 가능하게 하며 Longdapac의 북미 브랜드를 위한 100% 재활용 가능한 하이베리어 파우치는 유럽 이외 지역에도 규제 파급 효과를 가져오고 있습니다.

습식 개밥의 프리미엄화가 레토르트 파우치의 채용을 촉진

북미 소비자는 요리사 스타일의 습식 형식에 30-50%의 프리미엄을 지불하기 위해 열 살균 시 영양소를 보유하는 Amcor의 AmLite HeatFlex 재활용 대응 파우치에 투자에 박차를 가하고 있습니다. Special Dog Company의 100% 커버 모델과 같은 인라인 씰 검사 시스템은 품질을 보호하며 NaturPak Pet의 연간 5,000만 카톤 생산 능력은 프리미엄 성장에 필요한 확장성을 보여줍니다.

불안정한 PET와 알루미늄 가격이 컨버터 마진을 압박

반덤핑 조치와 물류의 혼란으로 인해 유럽 PET는 2025년 초에 1,130톤 유로를 넘어 세계 캔용 알루미늄 수요가 590억 달러를 넘어 컨버터의 이익을 압박하고 재활용 소재와 대체 기재에 대한 관심을 앞당겼습니다.

부문 분석

플라스틱은 2024년 매출의 67%를 차지하고 소재 부문은 시장 세분화의 경제적 백본이 되었습니다. 그러나 브랜드 커미트먼트와 EU 규정에 따라 바이오베이스와 컴포지트의 CAGR은 10.6%가 됩니다. 폴리에틸렌은 단일 소재 설계로 번성하고 있지만 PET는 불안정하기 때문에 화학 재활용과 rPET 블렌드에 대한 관심이 높아지고 있습니다. 판지는 포장 폐기물 규제의 기한이 가까워짐에 따라 진보하고, 리그닌-바이오나노복합재는 장래의 하이베리어 채용을 향해 산화 방지 기능을 나타냅니다. 종이 및 판지에 수반되는 반려동물 사료 포장 시장 규모는 2030년까지 10%대 중반의 속도로 확대될 것으로 예측되며, 이는 Billerud사가 연간 300킬로톤의 카톤보드를 공급할 계획에 뒷받침됩니다.

2세대 바이오 복합재료는 농업 폐기물의 흐름을 활용하여 기계 가공성을 손상시키지 않고 탄소 강도를 줄이고 컨버터에 화석 원료 위험에 대한 위험 회피를 제공합니다. Amcor사가 NOVA Chemicals사와 체결한 인디애나 재생 PE는 북미의 순환형 플랫폼을 지원하는 것으로, 모노PE파우치용 수지공급을 보증하는 것입니다. 한편, 알루미늄의 높은 재활용률은 비용면에서 역풍을 완화하고, 컨버터가 PFAS 프리 에폭시 수지의 대체품을 검토하는 중에서도, 통조림은 레토르트의 습식 식품에 적합합니다.

파우치는 편의성, 선반 진열, 전자상거래 적합성으로 2024년 점유율 43%를 차지했습니다. 레토르트 식품은 웨트 푸드의 프리미엄화를 지지하고, 스탠드업 식품은 도시의 소비자들 사이에서 지퍼 씰의 동향으로부터 혜택을 받고 있습니다. CAGR 9.5%로 확장되는 다른 제품 유형의 버킷은 스마트 라벨, 물약 제어 디스펜서, 섬유 강도 및 장벽 코팅이 융합된 종이 기반 컵을 커버합니다. Amcor의 80% 재활용 가능한 AmFiber Performance Paper는 브랜드 표면을 희생하지 않고 습기에 민감한 용도로 종이를 사용할 수 있음을 입증합니다.

그래픽 품질, 취급 효율성, 팩 대 제품 비율은 파우치가 유리한 상태를 유지하지만, 커브사이드 재활용을 위한 소매업체의 인수 조종사는 여전히 제한되어 있습니다. 신선도 센서와 컬러 체인지 잉크를 포함한 스마트 포장의 프로토타입도 있지만, 대량 도입에는 비용면에서 동등성이 필요합니다. 대용량 건식 식품은 여전히 주머니가 가방이지만, 단일 서브의 동향은 점차 부피를 유연하게 전환시킬 수 있습니다. 금속 캔은 견고한 재활용 인프라를 지원하며 알루미늄의 변동에도 불구하고 전통적인 습식 라인을위한 틈새 충성도를 유지합니다.

반려동물 사료 포장 시장 보고서는 재료별(플라스틱, 종이, 금속, 바이오베이스 재료), 제품 유형별(파우치, 가방, 금속 캔 등), 식품 유형별(건식 식품, 웨트 토푸드, 냉장·냉동, 간식), 반려동물 유형별(독후드, 캣푸드, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)으로 분류되어 있습니다.

지역별 분석

북미는 2024년 매출의 34%를 차지했으며, 이 지역의 소유율 확립과 재활용 대응 파우치에 대한 조기 축발을 반영했습니다. 2021년 이후 생산자 가격 상승으로 비용과 탄소에 대한 포장 최적화가 진행되어 전자상거래 충격을 위한 경량 유연성의 보급이 진행되고 있습니다. FDA에 의한 PFAS의 단계적 폐지는 종이와 폴리머의 장벽 연구 개발을 가속화하지만, 캘리포니아와 메인의 의무화는 실험실에서 검증된 컴플라이언스 툴킷을 갖춘 공급업체에게 유리한 패치워크를 만들어 냅니다.

아시아태평양은 CAGR 7.5%로 가장 급성장하는 지역으로 중국의 418억 달러 반려동물 경제와 디지털 우선 구매 습관이 견인하고 있습니다. 현지 컨버터는 EVOH 수지의 부족에 시달리고 있으며, 파우치의 생산 능력에 한계가 있기 때문에 대체 배리어로서 실리콘 옥사이드나 플라즈마 코팅된 모노 PVC의 연구 개발을 촉구하고 있습니다. Tier-2 도시에서는 국내 브랜드가 현지화된 그래픽과 QR코드에 의한 추적 가능성를 추진해 중간소득층의 반려동물 소유자가 늘고 있습니다.

유럽은 재활용 가능성과 재활용 컨텐츠의 통합을 강제하는 견고한 규제에 힘입어 안정적인 성장을 유지하고 있습니다. 포장·포장 폐기물 규제는 2030년 목표를 확실히 정하고, 종이 기반의 가방 라인이나 새로운 방유 코팅에 대한 투자에 박차를 가하고 있습니다. 단일 사용 플라스틱 요구 사항은 건조 식품에서 기존의 다층 구조를 대체하는 재활용을위한 디자인 가이드 라인을 전진시킵니다. Saica-Mondelez과 같은 업계를 넘어서는 제휴는 반려동물 식품에 노하우를 이전하여 종이 유연한 공급을 확대합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유럽 SUP 지령 후의 리사이클 가능한 단일 소재 파우치 수요 급증

- 웨트독후드의 프리미엄화가 북미에 있어서 하이베리어 레토르트 파우치의 채용을 촉진

- 중국에 있어서 도시에서 반려동물 사육 붐이 지퍼 첨부 소분 팩에 박차

- 특수식의 E-Commerce의 성장이 미국의 경량 연포장을 가속

- 브랜드 오너의 2025년 지속가능성 서약이 유럽에서 종이 베이스 백 투자를 촉진

- 광물유의 이행에 관한 EU 규칙 2024/354가 기능성 배리어 라미네이트에 박차

- 시장 성장 억제요인

- 불안정한 PET와 알루미늄 가격이 웨트 푸드캔의 컨버터 마진을 압박

- 미국, 식품접촉판에 있어서 PFAS의 사용 금지에 의해 코스트 높은 배합 변경을 강요

- EVOH 배리어 수지의 부족이 APAC의 스탠드업 파우치 생산 능력을 제한

- 레토르트 구조물의 한정된 커브 사이드에서 재활용 가능성이 소매업체 의욕 저하

- 공급망 분석

- 기술의 전망

- 규제 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 소재별

- 플라스틱

- 폴리에틸렌(PE)

- 폴리프로필렌(PP)

- 폴리에틸렌 테레프탈레이트(PET)

- 기타 플라스틱

- 종이 및 판지

- 금속

- 바이오 베이스 및 퇴비 재료

- 플라스틱

- 제품 유형별

- 파우치

- 가방

- 금속 캔

- 기타 제품 유형

- 식품 유형별

- 건식 사료

- 습식 사료

- 냉장 및 냉동 사료

- 간식 및 간식

- 반려동물 유형별

- 개 사료

- 고양이 사료

- 기타 반려동물

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 케냐

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Mondi plc

- ProAmpac LLC

- Sonoco Products Company

- Constantia Flexibles Group GmbH

- Crown Holdings Inc.

- Ardagh Group SA

- Silgan Holdings Inc.

- Coveris Holdings SA

- American Packaging Corporation

- Huhtamaki Oyj

- Sealed Air Corporation

- Printpack Inc.

- AptarGroup Inc.

- Smurfit Westrock plc

- Goglio SpA

- Glenroy Inc.

- Winpak Ltd.

- Tetra Pak International SA

- Wipak Oy

제7장 시장 기회와 향후 전망

KTH 25.11.13The pet food packaging market size reached USD 11.67 billion in 2025 and is projected to expand to USD 16.8 billion by 2030, advancing at a 6.2% CAGR.

Growing regulatory pressure in Europe and the United States, rapid premiumization of wet formats, and disruptive material science innovations together create a steady demand pipeline for solutions that balance barrier protection with recyclability. North America remains the largest consuming region, supported by strong e-commerce penetration and early adoption of mono-material flexibles, while Asia-Pacific records the fastest regional growth as urban pet ownership rises in China. Brand owners' 2025 sustainability pledges, rising raw-material volatility, and the FDA's phase-out of 35 PFAS food-contact approvals reinforce the need for converters to shift away from conventional multi-layer plastics toward recyclable paper, mono-PE, and bio-composite alternatives. Competitive intensity stays moderate as large integrated players capitalize on scale, but nimble specialists gain share by offering PFAS-free barriers, smart-packaging features, and design-for-recycling services that major brand owners increasingly require.

Global Pet Food Packaging Market Trends and Insights

Surge in demand for recyclable mono-material pouches post-SUP Directive

European Single-Use Plastics rules compel brand owners to abandon complex laminates, prompting converters to commercialize mono-PE structures that equal traditional barrier performance yet meet recyclability targets.Siegwerk's CIRKIT coatings now enable grease, oil, and oxygen protection inside mono-PE, while Longdapac's 100% recyclable high-barrier pouches for North American brands confirm regulatory ripple effects beyond Europe.

Premiumization of wet dog food driving retort pouch adoption

North American consumers pay 30-50% premiums for chef-style wet formats, spurring investments in Amcor's AmLite HeatFlex recycle-ready pouches that preserve nutrients during thermal sterilization. Inline seal-inspection systems such as Special Dog Company's 100% coverage model safeguard quality, and NaturPak Pet's 50 million-carton annual capacity illustrates scalability requirements for premium growth.

Volatile PET and aluminum prices squeezing converter margins

Anti-dumping measures and logistics disruptions pushed European PET above EUR 1,130 t in early 2025, while global aluminum demand for cans topped USD 59 billion, compressing converter profits and hastening interest in recycled content or alternative substrates.

Other drivers and restraints analyzed in the detailed report include:

- Urban pet ownership boom in China fueling small formats

- E-commerce growth for specialty diets accelerating flexibles

- U.S. PFAS bans triggering costly reformulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics supplied 67% of 2024 revenues, making the material segment the economic backbone of the pet food packaging market. Yet brand commitments and EU rules spur a 10.6% CAGR for bio-based and composite formats. Polyethylene thrives in mono-material designs, whereas PET's volatility drives interest in chemically recycled and rPET blends. Paperboard progresses as Packaging-and-Waste Regulation deadlines approach, while lignin-bionanocomposites showcase antioxidant capabilities for future high-barrier adoption. The pet food packaging market size attached to paper and board is projected to expand at a mid-teens pace through 2030, supported by Billerud's plan to supply 300 kilotons of cartonboard annually.

Second-generation bio-composites use agricultural waste streams to cut carbon intensity without compromising machinability, offering converters a hedge against fossil feedstock risk. Amcor's Indiana recycled-PE agreement with NOVA Chemicals underpins a North American circular platform, ensuring resin availability for mono-PE pouches. Meanwhile, aluminum's high recycling rate cushions cost headwinds, keeping cans relevant for retort wet food even as converters investigate PFAS-free epoxy replacements.

Pouches captured 43% 2024 share owing to convenience, shelf appeal, and e-commerce compatibility. Retort variants underpin wet-food premiumization, while stand-up formats benefit from zipper-reseal trends among urban consumers. The other-product-types bucket, expanding at 9.5% CAGR, covers smart labels, portion-controlled dispensers, and paper-based cups that meld fiber strength with barrier coatings. Amcor's 80%-recyclable AmFiber Performance Paper proves the viability of paper for moisture-sensitive applications without sacrificing branding surface.

Graphics quality, handling efficiency, and pack-to-product ratios keep pouches favorable, yet retailer take-back pilots for curbside recycling remain limited. Smart-packaging prototypes embed freshness sensors and color-change inks, but mass uptake awaits cost parity. Bags still dominate large-volume dry food, though single-serve trends could gradually migrate volume into flexibles. Metal cans hold niche loyalty for heritage wet lines despite aluminum volatility, supported by robust recycling infrastructure.

The Pet Food Packaging Market Report is Segmented by Material (Plastic, Paper, Metal, Biobased Materials), Product Type (Pouches, Bags, Metal Cans, and More), Food Type (Dry Food, Wet Food, Chilled and Frozen, Treats), Pet Type (Dog Food, Cat Food, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts in Value (USD).

Geography Analysis

North America controlled 34% of 2024 sales, reflecting established ownership rates and the region's early pivot to recycle-ready pouches. High producer-price inflation since 2021 elevates packaging optimization on cost and carbon, driving uptake of lightweight flexibles seasoned for e-commerce shocks. The FDA's PFAS phase-out accelerates paper-and-polymer barrier R&D, while California and Maine mandates create a patchwork that favors suppliers with lab-validated compliance toolkits.

Asia-Pacific is the fastest-growing region at 7.5% CAGR, led by China's USD 41.8 billion pet economy and digital-first purchasing habits. Local converters grapple with EVOH resin shortages that cap pouch capacity, prompting R&D into silicon-oxide and plasma-coated mono-PE as substitute barriers. Tier-2 cities show domestic brands advancing localized graphics and QR code traceability to court rising middle-income pet owners.

Europe's growth remains steady, anchored by robust regulation that forces recyclability and recycled-content integration. The Packaging-and-Packaging-Waste Regulation sets firm 2030 targets, spurring investment in paper-based bag lines and new grease-proof coatings. Single-Use Plastics requirements bring forward design-for-recycling guidelines that displace legacy multilayer structures in dry food. Cross-industry alliances such as Saica-Mondelez transfers know-how to pet food, widening supply of paper flexibles.

- Amcor plc

- Mondi plc

- ProAmpac LLC

- Sonoco Products Company

- Constantia Flexibles Group GmbH

- Crown Holdings Inc.

- Ardagh Group SA

- Silgan Holdings Inc.

- Coveris Holdings SA

- American Packaging Corporation

- Huhtamaki Oyj

- Sealed Air Corporation

- Printpack Inc.

- AptarGroup Inc.

- Smurfit Westrock plc

- Goglio SpA

- Glenroy Inc.

- Winpak Ltd.

- Tetra Pak International SA

- Wipak Oy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Demand for Recyclable Mono-Material Pouches Post-Europe SUP Directive

- 4.2.2 Premiumization of Wet Dog Food Driving High-Barrier Retort Pouch Adoption in North America

- 4.2.3 Urban Pet Ownership Boom in China Fueling Small-Pack Formats with Reclosable Zippers

- 4.2.4 E-commerce Growth for Specialty Diets Accelerating Lightweight Flexible Packaging in the US

- 4.2.5 Brand Owner 2025 Sustainability Pledges Catalyzing Paper-Based Bag Investments in Europe

- 4.2.6 EU Regulation 2024/354 on Mineral-Oil Migration Spurring Functional Barrier Laminates

- 4.3 Market Restraints

- 4.3.1 Volatile PET and Aluminum Prices Squeezing Converter Margins for Wet-Food Cans

- 4.3.2 US PFAS Bans in Food-Contact Boards Forcing Costly Reformulations

- 4.3.3 EVOH Barrier Resin Shortages Limiting Stand-Up Pouch Capacity in APAC

- 4.3.4 Limited Curb-Side Recyclability of Retort Structures Discouraging Retailers

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.4 Other Plastics

- 5.1.2 Paper and Paperboard

- 5.1.3 Metal

- 5.1.4 Biobased and Compostie Materials

- 5.1.1 Plastic

- 5.2 By Product Type

- 5.2.1 Pouches

- 5.2.2 Bags

- 5.2.3 Metal Cans

- 5.2.4 Other Product Types

- 5.3 By Type of Food

- 5.3.1 Dry Food

- 5.3.2 Wet Food

- 5.3.3 Chilled and Frozen

- 5.3.4 Treats and Snacks

- 5.4 By Pet Type

- 5.4.1 Dog Food

- 5.4.2 Cat Food

- 5.4.3 Other Pet Food

- 5.5 By Geography

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.6 Middle East and Africa

- 5.5.6.1 Middle East

- 5.5.6.1.1 Saudi Arabia

- 5.5.6.1.2 United Arab Emirates

- 5.5.6.1.3 Rest of Middle East

- 5.5.6.2 Africa

- 5.5.6.2.1 South Africa

- 5.5.6.2.2 Kenya

- 5.5.6.2.3 Nigeria

- 5.5.6.2.4 Rest of Africa

- 5.5.2 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amcor plc

- 6.4.2 Mondi plc

- 6.4.3 ProAmpac LLC

- 6.4.4 Sonoco Products Company

- 6.4.5 Constantia Flexibles Group GmbH

- 6.4.6 Crown Holdings Inc.

- 6.4.7 Ardagh Group SA

- 6.4.8 Silgan Holdings Inc.

- 6.4.9 Coveris Holdings SA

- 6.4.10 American Packaging Corporation

- 6.4.11 Huhtamaki Oyj

- 6.4.12 Sealed Air Corporation

- 6.4.13 Printpack Inc.

- 6.4.14 AptarGroup Inc.

- 6.4.15 Smurfit Westrock plc

- 6.4.16 Goglio SpA

- 6.4.17 Glenroy Inc.

- 6.4.18 Winpak Ltd.

- 6.4.19 Tetra Pak International SA

- 6.4.20 Wipak Oy

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment