|

시장보고서

상품코드

1851579

서명 검증 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Signature Verification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

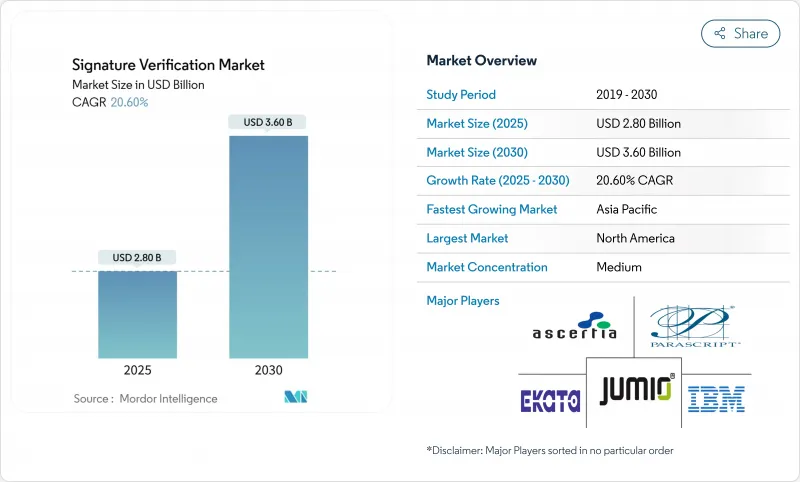

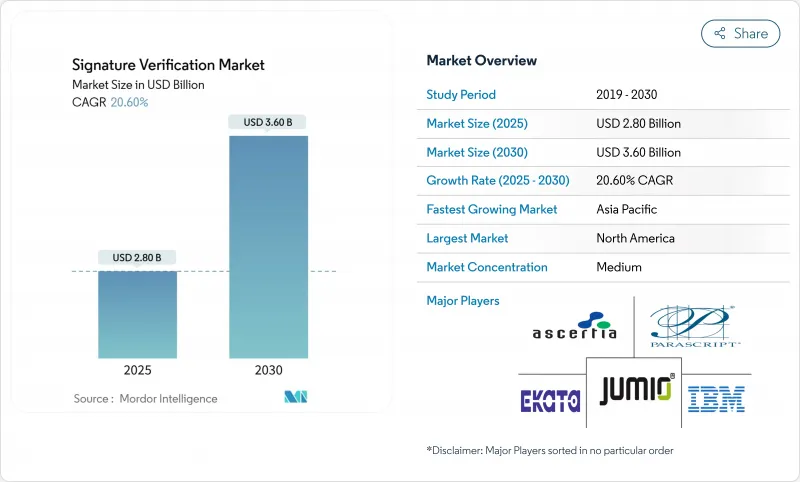

서명 검증 시장은 2025년에 28억 달러에 이르고, 2030년에는 36억 달러로 성장할 것으로 예상되며, 예측 기간의 CAGR은 20.6%를 나타낼 전망입니다.

유럽에서는 eIDAS 2.0, 미국에서는 21 CFR Part 11이 그 기세를 가속화하고 있으며, 모두 규제 부문에 신뢰성 높은 디지털 서명 검증의 채용을 촉구하고 있습니다. 부정피해 증가, AI에 의한 위조분석의 진보, 클라우드로의 급속한 전환이 수요를 더욱 높여 가고 있습니다. AI에 의한 우편 투표 처리부터 Aadhaar에 연결된 지갑까지 정부 프로그램은 이용 사례와 지리적 범위를 확대하고 있습니다. 반면에 멀티모달 인증과 API First Delivery 모델은 서명 검증 시장 전체의 경쟁 포지셔닝을 재구성하고 있습니다.

세계의 서명 검증 시장 동향과 인사이트

eIDAS 2.0 및 미국 CFR Part 11에 따른 컴플라이언스 의무화

eIDAS 2.0은 2026년까지 모든 EU 시민들이 상호 운용 가능한 디지털 ID 지갑을 보유할 것을 의무화하고, 인증된 트러스트 서비스 제공업체에게 뒷받침된 적격 전자 서명 기준을 인상하고 있습니다. 동시에 FDA 지침이 업데이트되고 감사 추적과 위험 기반 검증이 강조되고 제약 스폰서는 AI 지원 서명 검증 플랫폼으로의 전환을 강요하고 있습니다. 그 결과 다국적 기업은 양 제도를 충족하는 통일된 검증 아키텍처를 요구하고 세계 정책 컴플라이언스가 가능한 클라우드 기업을 중심으로 한 통합이 가속화되고 있습니다.

2024년 선거 후 우송 투표 서명 체크 급증

미국에서는 31개 주에서 부재자 투표에 서명 검증이 필요하며, 높은 처리량 시스템에 대한 수요가 높아지고 있습니다. 노스캐롤라이나의 시험 운용은 자동화된 플랫폼이 시간당 1,000장의 투표 용지를 처리하고 수작업으로 심사 시간을 95% 단축하는 것으로 입증되었습니다. 그 후 캘리포니아에서는 속도보다 감사성을 강조했으며, 수작업으로 인한 페일 세이프를 갖춘 기술 지원 검토를 의무화했습니다. 다문화 간 서명의 변동과 연령에 따른 변화에 대응할 수 있는 공급업체는 선거기관이 정확성, 재결의 투명성, 규제 당국의 감사 기능에 대가를 지불하기 때문에 가격이 비쌉니다.

캡처 장치 간의 편차와 레거시 사일로 통합

조직은 종종 서명 패드, 태블릿 및 모바일 앱의 패치워크에 의존하며, 각각은 서로 다른 해상도와 샘플링 속도로 데이터를 생성합니다. 알고리즘은 일관성 없는 압력 곡선 및 타이밍 데이터를 보정해야 하며, 이는 불합격률을 높이고 총 소유 비용을 증가시킵니다. 최신 검증을 레거시 레코딩 시스템과 통합하면 데이터가 사일로화되어 전반적인 불법 분석이 불가능해지고 복잡성이 커집니다. 소규모 금융기관에서는 하드웨어 교체가 인식되는 이점을 능가하기 때문에 업그레이드가 늘어나고 보안 향상이 기대될 수 있음에도 불구하고 단기적인 배포가 억제됩니다.

부문 분석

2024년 서명 검증 시장의 58%를 소프트웨어가 차지했습니다. 이는 웹, 모바일 및 지사의 각 채널에서 실시간 사기 감지를 실현하는 클라우드 네이티브 AI 모델의 보급을 반영합니다. 서명 패드와 같은 하드웨어 장치는 규제된 환경에서 여전히 정착되어 있지만, 원격 워크플로우가 주류가 됨에 따라 그 점유율은 계속 하락할 것으로 보입니다. 소프트웨어 분야는 은행, 헬스케어, 정부기관의 포털에 인증을 포함하는 SDK에 힘입어 2030년까지 연평균 복합 성장률(CAGR) 23.7%를 나타낼 것으로 예측됩니다. 공급업체는 정적 이미지 비교를 통해 행동 분석을 중첩하여 수동 검토 비율을 줄이고 의사 결정 대기 시간을 단축합니다. 에지 전개가 가능한 모델은 연결이 간헐적인 위치에도 대응하여 물류 및 현장 서비스 이용 사례에 대한 호소력을 높이고 있습니다. 또한 지속적인 모델 재교육을 통해 공급업체는 고객 측에서 코드를 변경하지 않고도 새로운 공격 패턴에 대응할 수 있게 되었으며, 서명 검증 시장에서 소프트웨어의 구조적 이점을 명확히 했습니다.

하드웨어는 성장이 둔화되고 있으며 습식 잉크 서명의 물리적 저장이 양보 할 수없는 틈새 관련성을 유지합니다. 법원, 공증인 및 일부 생명 과학 연구소는 여전히 암호화 타임스탬프를 추가하는 인증된 장치를 사용하여 대면 캡처를 요구하고 있습니다. 그러나 이러한 산업에서 조달주기는 여전히 길고 자본 예산은 고정되어 있으며 리노베이션 비용은 높습니다. 클라우드 경제학이 의사 결정 기준을 운영 지출로 전환시키는 동안 많은 구매자는 현재 서비스 수명이 끝날 때 디바이스를 단계적으로 폐지하고 모바일 캡처 및 백엔드 AI 검증으로 전환하고 있습니다. 이 마이그레이션은 소프트웨어 중심 비즈니스 모델의 이점을 강화하여 공급업체가 일회성 하드웨어 판매가 아닌 구독 수익원에 중점을 두도록 보장합니다.

2024년 서명 검증 시장 규모의 55%는 On-Premise로 규제가 엄격한 은행, 보험사, 생명과학기업이 감사 및 대기 시간 관점에서 로컬 관리를 선호했기 때문입니다. 그러나 클라우드/SaaS의 도입은 2030년까지 매년 28.2%씩 증가하고, 스케일 메리트와 보편적인 API 리치에 의해 도입 기반의 격차가 축소될 것으로 예측되고 있습니다. 클라우드 플랫폼은 모델 교육을 중앙 집중화된 환경에 집중시키고 깊은 가짜 위협에 대한 정확성을 극대화하는 다양한 데이터 세트를 활용합니다. 탄력적인 컴퓨팅 프로비저닝은 유휴 인프라 지출을 줄입니다. 이것은 투표의 최고 시간에 워크로드를 집중적으로 처리하는 선거 관리위원회에 중요한 이점입니다.

지역 클라우드 영역은 GDPR(EU 개인정보보호규정) 및 eIDAS 2.0을 기반으로 데이터 거주 의무를 지원하고 통합된 정책 엔진을 유지합니다. 서명 아티팩트의 로컬 스토리지와 클라우드 기반 추론을 결합한 하이브리드 아키텍처는 신중한 채용 기업에게 컴플라이언스에 적합한 브리지가 됩니다. 공급자는 가동 시간 SLA, 자동화된 패치 적용 및 원활한 기능 롤아웃을 통해 가치 제안을 강화합니다. 기업이 운영의 민첩성이 인식된 소블린 리스크보다 높다고 결론을 내리면서 서명 검증 시장은 SaaS 구독으로의 전환을 가속화하는 태세를 마련하고 있습니다.

지역 분석

북미는 2024년 매출의 34%를 차지하며, 성숙한 규제체제와 벤처지원에 의한 혁신 에코시스템에 지지되었습니다. 각 주는 2024년 주기 이후 선거 무결성을 높이기 위해 자동 투표 용지 서명 시스템을 도입하여 선거 관리 위원회의 급속한 업그레이드를 촉구했습니다. 금융기관도 고도화·대규모화하는 수표 사기를 저지하기 위해 AI 분석을 활용해 입금 시 미묘한 서명의 어긋남을 검출하는 시스템 도입을 확대했습니다. USAA의 지속적인 라이선스 승리는 수익을 창출하지만 원격 예금 모듈을 통합하는 은행의 컴플라이언스 비용을 증가시킵니다. 이 지역은 FDA Part 11의 감사 대응에 중점을 두고 있기 때문에 서명 증명과 체인 오브 캐스트 디를 문서화하는 전문 플랫폼에 대한 수요가 더욱 높아지고 있습니다.

아시아태평양은 2025년부터 2030년까지의 CAGR이 25.44%로 가장 높을 것으로 예측되며, 인도의 Aadhaar와 연동한 월렛과 모바일 결제 생태계의 급성장이 그 요인이 되고 있습니다. 엄청난 거래량과 빈번한 사기 사건이 인도 준비 은행에 의한 KYC 기준의 엄격화를 촉구하고, 은행이 온보딩 워크플로우에 다중 모드 서명 검증을 통합하도록 촉구하고 있습니다. 일본과 한국은 손가락 정맥과 행동 생체 인식 조사를 진행하고 있으며, 이러한 기술과 서명 분석을 결합하여 종종 신뢰할 수 있는 기업 로그인을 실현하고 있습니다. 클라우드 하이퍼스케일은 국내 가용 영역을 통해 서명 검증 시장이 세계 위협 인텔리전스 피드를 활용하면서도 엄격한 거주 규칙을 충족할 수 있도록 보장합니다.

유럽의 성장 시나리오는 eIDAS 2.0을 중심으로 배포됩니다. eIDAS 2.0은 자격을 갖춘 전자 서명을 공식화하고 지역 내 국경을 넘어 상호 운용성을 강제합니다. 공인 트러스트 서비스 제공업체는 서명 페이로드에 내장된 디지털 인증서를 발행하는 데 매우 중요한 역할을 하며 알고리즘 검증의 기술적 요구 사항을 높입니다. 브렉짓은 영국과 EU의 워크플로우를 복잡하게 하며, 공급업체들은 이중 컴플라이언스 스택을 유지하기 위해 매끄러운 사용자 경험을 약속합니다. 프라이버시 바이 디자인에 대한 GDPR(EU 개인정보보호규정)의 기대를 통해 공급자는 페더레이티드 학습 기술을 채택하고 관할 경계를 넘어 서명 아티팩트를 내보내지 않고 모델을 교육해야 합니다. 그 결과 유럽의 구매자는 알고리즘의 정확성과 입증 가능한 개인 정보 보호 조치를 비교 검토하고 둘 다 제공하는 공급업체를 선호합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- eIDAS 2.0 및 미국 CFR Part 11에 따른 컴플라이언스 지침

- 2024년 선거 후 우송 투표 서명 체크의 급증

- AI 기반 수표 사기 분석을 촉진하는 금융 범죄 피해

- 전자 서명 스위트에 클라우드 네이티브 API 포함

- GenAI의 위조 서명 검출 알고리즘

- 인도의 Aadhaar 연동 디지털 서명 지갑(UPI 3.0)

- 시장 성장 억제요인

- 캡처 디바이스 간 편차와 레거시 사일로의 통합

- 다문화 유권자 명부가 높은 FRR이 소송 촉진

- 데이터 주권에 의한 국경을 넘은 모델 트레이닝의 제한

- 특허 소송 위험(예 : MITK vs USAA)

- 가치/공급망 분석

- 규제 상황

- 기술적 전망(AI, Edge, GenAI)

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 솔루션 유형별

- 하드웨어

- 서명 패드 및 센서

- 생체 인식 단말/키오스크

- 소프트웨어

- 정적(오프라인) 검증

- 동적(온라인) 검증

- SDK/API 플랫폼

- 하드웨어

- 배포 모델별

- On-Premise

- 클라우드/SaaS

- 인증 모드별

- 독립형 서명

- 다중 모드(서명+문서 이미지/ID/생체 인식)

- 최종 사용자 업계별

- 금융 서비스

- 정부 및 선거

- 헬스케어

- 운송 및 물류

- 법률 및 부동산

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Mitek Systems Inc.

- Parascript LLC

- IBM Corp.

- Adobe Inc.

- DocuSign Inc.

- Ascertia Ltd

- Jumio Corp.

- Ekata Inc.

- Acuant Inc.

- SutiSoft Inc.

- CERTIFY Global Inc.

- Scriptel Corp.

- iSign Solutions Inc.

- Veriff

- Hitachi Ltd.(Biometric systems)

- HID Global(Assa Abloy)

- Signicat AS

- Topaz Systems Inc.

- Aratek Biometrics

- Biometric Signature ID

제7장 시장 기회와 향후 전망

KTH 25.11.24The signature verification market reached USD 2.8 billion in 2025 and is expected to grow to USD 3.6 billion by 2030, delivering a 20.6% CAGR over the forecast period.

Momentum is fueled by eIDAS 2.0 in Europe and 21 CFR Part 11 in the United States, both of which compel regulated sectors to adopt trustworthy digital-signature validation. Rising fraud losses, advances in AI-driven forgery analytics, and rapid cloud migration further elevate demand. Government programs ranging from AI-assisted mail-in ballot processing to Aadhaar-linked wallets expand use-cases and geographic reach. Meanwhile, multimodal authentication and API-first delivery models are reshaping competitive positioning across the signature verification market.

Global Signature Verification Market Trends and Insights

Compliance mandates under eIDAS 2.0 & U.S. CFR Part 11

The harmonized push from Brussels and Washington is forcing enterprises to modernize outdated electronic-record systems. eIDAS 2.0 obliges all EU citizens to hold interoperable digital identity wallets by 2026, raising the bar for qualified electronic signatures backed by certified trust service providers. Simultaneously, updated FDA guidance stresses audit trails and risk-based validation, compelling pharmaceutical sponsors to shift toward AI-enabled signature verification platforms. Multinationals consequently seek unified verification architectures that satisfy both regimes, accelerating consolidation around cloud players capable of global policy compliance.

Surge in mail-in ballot signature checks post-2024 elections

Thirty-one U.S. states now require signature verification for absentee ballots, elevating demand for high-throughput systems. North Carolina's pilot demonstrated that automated platforms processed 1,000 ballots per hour, cutting manual review time by 95%. California subsequently mandated technology-assisted review with manual fail-safes, placing auditability above speed. Vendors able to accommodate multicultural signature variation and age-related changes command premium pricing as election agencies pay for accuracy, adjudication transparency, and regulatory audit features.

Variability across capture devices & legacy silo integration

Organizations often rely on a patchwork of signature pads, tablets, and mobile apps, each producing data at different resolutions and sampling rates. Algorithms must compensate for inconsistent pressure curves and timing data, which inflates false-reject rates and raises total cost of ownership. Integrating modern verification with legacy record systems adds complexity, as siloed data prevents holistic fraud analytics. Smaller institutions postpone upgrades because replacing hardware exceeds perceived benefits, restraining near-term adoption despite compelling security gains.

Other drivers and restraints analyzed in the detailed report include:

- Fin-crime losses driving AI-based check-fraud analytics

- Cloud-native APIs embedded in e-signature suites

- High FRR in multicultural voter rolls sparks litigation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 58% of the 2024 signature verification market, reflecting widespread adoption of cloud-native AI models that deliver real-time fraud detection across web, mobile, and branch channels. Hardware devices such as signature pads remain entrenched in regulated environments, yet their share will continue to erode as remote workflows dominate. The software segment is forecast to post a 23.7% CAGR through 2030, propelled by SDKs that embed verification inside banking, healthcare, and government portals. Vendors are layering behavioral analytics atop static image comparison, thereby reducing manual review rates and shrinking decision latency. Edge-deployable models address locations with intermittent connectivity, broadening appeal to logistics and field-service use-cases. Continuous model retraining also enables vendors to counter emerging attack patterns without customer-side code changes, underscoring software's structural advantage within the signature verification market.

Hardware, though slower-growing, retains niche relevance where physical custody of wet-ink signatures is non-negotiable. Courts, notaries, and select life-sciences labs still require in-person capture using certified devices that append cryptographic timestamps. Yet procurement cycles in these verticals remain long, capital budgets fixed, and retrofit costs high. As cloud economics shift decision criteria toward operating expenditure, many buyers now phase out devices at end-of-life, migrating to mobile capture plus back-end AI validation. This transition reinforces the ascendancy of software-centric business models and cements provider focus on subscription revenue streams rather than one-time hardware sales.

On-premises deployments represented 55% of the signature verification market size in 2024 as heavily regulated banks, insurers, and life-sciences firms favored local control for audit and latency reasons. However, cloud/SaaS installations are projected to compound at 28.2% annually through 2030, narrowing the installed-base gap on economies of scale and universal API reach. Cloud platforms concentrate model training in centralized environments, leveraging diverse datasets that sharpen accuracy against deepfake threats. Elastic compute provisioning cuts idle infrastructure spending, a critical advantage for election boards that process workloads in intense bursts during peak voting periods.

Regional cloud zones support data-residency mandates under GDPR and eIDAS 2.0 while maintaining uniform policy engines. Hybrid architectures-local storage of signature artefacts combined with cloud-based inference-offer a compliance-friendly bridge for cautious adopters. Providers bolster value propositions with uptime SLAs, automated patching, and seamless feature rollouts that would be cost-prohibitive in isolated data centers. As organizations conclude that operational agility outweighs perceived sovereignty risks, the signature verification market is poised for an accelerated shift toward SaaS subscriptions.

Signature Verification Market Report is Segmented by Solution Type (Hardware, Software), Deployment Model (On-Premises, Cloud / SaaS), Authentication Mode (Stand-Alone Signature, Multimodal (signature + Doc Image / ID / Liveness)), End-User Industry (Financial Services, Healthcare and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 34% of 2024 revenue, supported by mature regulatory regimes and venture-backed innovation ecosystems. States introduced automated ballot-signature systems to enhance electoral integrity after the 2024 cycle, driving rapid upgrades among election boards. Financial institutions also escalated adoption to blunt check-fraud schemes that escalated in sophistication and scale, leveraging AI analytics to detect subtle signature deviations at deposit time. Patent enforcement remains a double-edged sword: USAA's ongoing licensing victories generate revenue but elevate compliance costs for banks integrating remote-deposit modules. The region's focus on audit readiness under FDA Part 11 further solidifies demand for specialized platforms that document signature provenance and chain-of-custody.

Asia Pacific is forecast to deliver the highest regional CAGR of 25.44% between 2025 and 2030, anchored by India's Aadhaar-linked wallets and surging mobile-payment ecosystems. Massive transaction volumes and episodic fraud incidents encourage the Reserve Bank of India to tighten KYC norms, prompting banks to embed multimodal signature verification in onboarding workflows. Japan and South Korea advance finger-vein and behavioural-biometric research, often pairing those technologies with signature analysis for high-trust enterprise login. Local data-sovereignty mandates spur demand for regionally hosted inference clusters, which cloud hyperscale's provide through in-country availability zones, ensuring that the signature verification market meets stringent residency rules while still leveraging global threat-intelligence feeds.

Europe's growth narrative revolves around eIDAS 2.0, which formalizes qualified electronic signatures and compels cross-border interoperability throughout the bloc. Certified trust service providers play a pivotal role in issuing digital certificates embedded within signature payloads, raising technical requirements for algorithmic verification. Brexit complicates UK-EU workflows, forcing vendors to maintain dual compliance stacks while promising seamless user experiences. GDPR expectations of privacy-by-design push providers to adopt federated-learning techniques, training models without exporting signature artefacts beyond jurisdictional boundaries. As a result, European buyers weigh algorithmic precision alongside demonstrable privacy safeguards, favouring vendors that deliver both.

- Mitek Systems Inc.

- Parascript LLC

- IBM Corp.

- Adobe Inc.

- DocuSign Inc.

- Ascertia Ltd

- Jumio Corp.

- Ekata Inc.

- Acuant Inc.

- SutiSoft Inc.

- CERTIFY Global Inc.

- Scriptel Corp.

- iSign Solutions Inc.

- Veriff

- Hitachi Ltd. (Biometric systems)

- HID Global (Assa Abloy)

- Signicat AS

- Topaz Systems Inc.

- Aratek Biometrics

- Biometric Signature ID

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Compliance mandates under eIDAS 2.0 and U.S. CFR Part 11

- 4.2.2 Surge in mail in ballot signature checks post-2024 elections

- 4.2.3 Fin-crime losses driving AI-based check-fraud analytics

- 4.2.4 Cloud-native APIs embedded in e-signature suites

- 4.2.5 GenAI forged-signature detection algorithms

- 4.2.6 Indias Aadhaar linked digital signature wallets (UPI 3.0)

- 4.3 Market Restraints

- 4.3.1 Variability across capture devices and legacy silo integration

- 4.3.2 High FRR in multicultural voter rolls sparks litigation

- 4.3.3 Data-sovereignty limits on cross-border model training

- 4.3.4 Patent litigation risk (e.g., MITK vs USAA)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (AI, edge, GenAI)

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Hardware

- 5.1.1.1 Signature pads and sensors

- 5.1.1.2 Biometric terminals / kiosks

- 5.1.2 Software

- 5.1.2.1 Static (offline) verification

- 5.1.2.2 Dynamic (online) verification

- 5.1.2.3 SDK / API platforms

- 5.1.1 Hardware

- 5.2 By Deployment Model

- 5.2.1 On-premise

- 5.2.2 Cloud / SaaS

- 5.3 By Authentication Mode

- 5.3.1 Stand-alone signature

- 5.3.2 Multimodal (signature + doc image / ID / liveness)

- 5.4 By End-user Industry

- 5.4.1 Financial Services

- 5.4.2 Government and Elections

- 5.4.3 Healthcare

- 5.4.4 Transport and Logistics

- 5.4.5 Legal and Real-estate

- 5.4.6 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Recent Devs.)

- 6.4.1 Mitek Systems Inc.

- 6.4.2 Parascript LLC

- 6.4.3 IBM Corp.

- 6.4.4 Adobe Inc.

- 6.4.5 DocuSign Inc.

- 6.4.6 Ascertia Ltd

- 6.4.7 Jumio Corp.

- 6.4.8 Ekata Inc.

- 6.4.9 Acuant Inc.

- 6.4.10 SutiSoft Inc.

- 6.4.11 CERTIFY Global Inc.

- 6.4.12 Scriptel Corp.

- 6.4.13 iSign Solutions Inc.

- 6.4.14 Veriff

- 6.4.15 Hitachi Ltd. (Biometric systems)

- 6.4.16 HID Global (Assa Abloy)

- 6.4.17 Signicat AS

- 6.4.18 Topaz Systems Inc.

- 6.4.19 Aratek Biometrics

- 6.4.20 Biometric Signature ID

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment