|

시장보고서

상품코드

1851593

플록 접착제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Flock Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

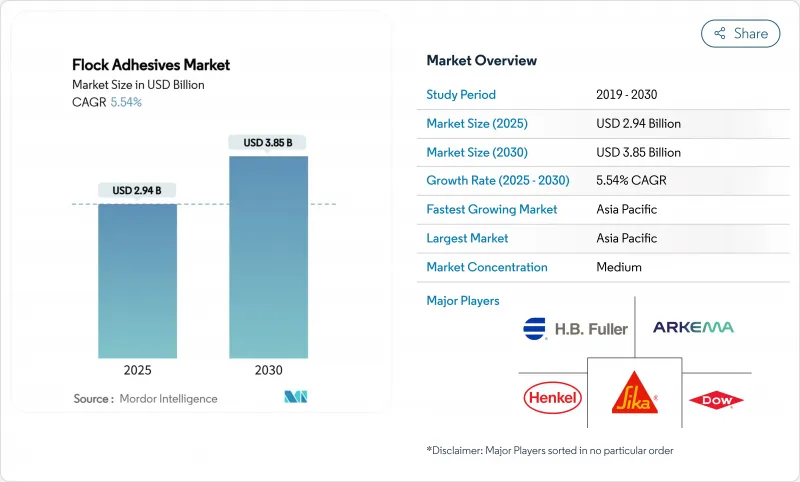

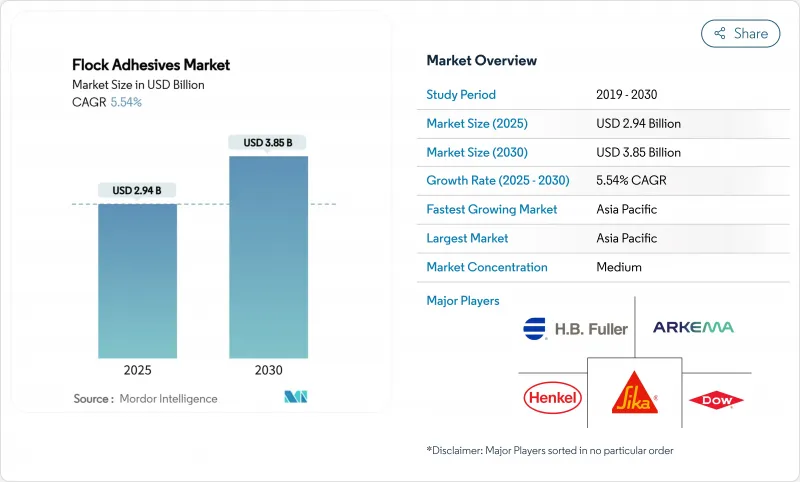

플록 접착제 시장 규모는 2025년에 29억 4,000만 달러, 2030년에는 38억 5,000만 달러에 이를 것으로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.54%를 나타낼 전망입니다.

성장은 전기자동차(EV) 생산 증가로 가속화되는 자동차 인테리어 수요에 힘입어 소프트 터치의 미관과 열기능성을 중시하는 고급 패키징 요건에 의해 강화됩니다. 특히 유럽연합(EU)이 디이소시아네이트를 제한하고 중국이 내장된 배기가스 규제를 강화하는 가운데 수성 화학물질과 VOC 프리 화학물질로의 규제 변화가 제품의 급속한 개량을 촉진하고 있습니다. 자동차 용도는 2024년에 42.56%와 플록 접착제 시장에서 가장 큰 점유율을 차지했고, CAGR도 6.42%로 가장 급속히 확대되었습니다. 아시아태평양은 2024년에 51.84%의 점유율을 차지했고, 2030년까지의 CAGR은 6.19%로 지리적 리더십을 유지합니다. 한편, 폴리우레탄 수지 시스템의 점유율은 38.19%로 압도적이지만, 「기타」의 화학물질이 CAGR 6.65%로 가장 높은 신장을 나타내고 있습니다.

세계의 플록 접착제 시장 동향과 인사이트

코팅 원단과 고급 마감 제품 수요 급증

자동차 및 고급 제품 제조업체는 높은 품질을 보여주기 위해 식모 소재의 사용을 강화하고 있습니다. 대시보드, 기둥, 수납 트레이 등의 캐빈 부품은 그립을 향상시키고 덜컹 거리는 소리를 자르는 고급스러운 느낌을 얻을 수 있습니다. 고급 패키지 제조업체도 같은 기술을 채용해, 보석상자나 스마트폰 케이스를 최초로 접했을 때부터 고급감이 느껴지도록 하고 있습니다. 촉감 업그레이드는 소매 가격 상승을 지원하고 브랜드 차별화를 강화합니다. 이러한 요인들이 결합되어 플록 접착제 수요 기반은 보다 넓고 안정적입니다.

경량, 저탄소 자동차 내장 부품이 채용을 뒷받침

자동차 제조업체는 무게가 있는 패스너를 접착제로 접착한 복합 패널로 대용하고, 모든 모델에서 그램 단위의 경량화를 도모하고 있습니다. 플록 접착제는 충돌 테스트, 진동 테스트 및 내구성 테스트를 완료하면서 얇은 플라스틱 및 직물 라미네이트를 보장합니다. 질량 감소는 소비자와 규제 당국이 주시하는 지표인 EV의 항속거리의 연장과 직결됩니다. 또한 클립과 나사의 수를 줄임으로써 사이클 시간을 단축하고 재활용을 간소화할 수 있으므로 조립 라인에도 이점이 있습니다. 전동화가 확산됨에 따라 경량화라는 주장이 무리 솔루션을 엔지니어링의 후보로 꼽고 있습니다.

휘발성 이소시아네이트·아크릴레이트 원료 가격

접착제 제조업체는 석유 화학 유도 제품에 따라 달라지며 비용은 석유 충격과 공급망 충격에 따라 달라집니다. 최근 메타크릴산 공급 과잉은 12%의 가격 하락을 일으켰지만, 수지 제조업체는 몇 주 후에 급격한 가격 인상을 실시했습니다. 자동차 OEM과의 장기 고정 가격 계약은 서차지를 전가하는 능력을 제한합니다. 소형 제제 제조업체는 위험 회피의 규모와 분산 포트폴리오가 없기 때문에 특히 위험에 노출됩니다. 마진이 불투명하기 때문에 혼란기에 대담한 설비 투자가 삼가됩니다.

부문 분석

2024년 플록 접착제 시장 점유율로 38.19%를 차지한 폴리우레탄은 자동차용 기재와의 폭넓은 적합성과 높은 내열성에 지지되고 있습니다. 그러나 이소시아네이트에 대한 규제의 감시가 수요를 변화시키고 있는 것은 「기타」의 수지 유형의 CAGR이 6.65%로 예측되고 있는 것으로부터도 분명합니다. 비이소시아네이트계 수지의 플록 접착제 시장 규모는 본질적으로 VOC가 낮고 취급이 용이한 아크릴이나 에폭시의 대체 수지가 인기를 끌면 기존 수지를 상회할 것으로 예측됩니다. 재생가능 성분을 71% 함유하는 헨켈의 바이오베이스 폴리우레탄은 표준 처방에 비해 60%의 CO2 감소를 입증하여 지속가능성 이야기가 구매 기준에 어떻게 반영되는지를 보여줍니다.

규제 당국은 디이소시아네이트 제품에 대한 근로자 교육 및 표시의 엄격화를 요구하고 있으며, OEM은 적합한 대체품을 요구하고 있습니다. 배합업자는 디이소시아네이트의 임계치 0.1%를 넘지 않고 접착성, 유연성, 히트 사이클의 요구를 충족시키는 아크릴계 디스퍼전과 비이소시아네이트·폴리우레탄(NIPU) 케미스트리를 확대함으로써 대응하고 있습니다. 컴플라이언스, 성능 및 비용의 균형을 맞출 수 있는 공급업체는 기존 옵션이 단계적 제한에 직면하는 동안 프리미엄 마진을 요구할 것으로 보입니다.

지역 분석

2024년 플록 접착제 시장 점유율은 아시아태평양이 51.84%를 차지했고 2030년까지 연평균 복합 성장률(CAGR)은 6.19%를 나타낼 전망입니다. 중국이 이 지역 수요의 중심이 되고 있으며, 국내 브랜드나 수출 지향의 조립업체가, 지각 품질의 향상과 낮은 VOC 규제에의 대응을 위해서 플록 가공 내장재를 채용하고 있습니다. 시카의 랴오닝성과 싱가포르에 신설된 공장은 리드 타임의 단축과 새로운 배터리 열 요구에 대응하기 위한 현지 능력 투자를 보여줍니다. 일본과 한국은 에폭시 기반의 저포름 방출 시스템을 전자기기 및 자동차용으로 확대하여 재료과학의 리더십으로 생산량을 보완하고 있습니다.

북미는 성숙하지만 기술적으로 요구되는 소비로 이어집니다. OEM은 지속가능성과 공급망 투명성에 대한 엄격한 조달 기준을 시행하고 수분산액 및 바이오 컨텐츠의 급속한 채용을 촉진하고 있습니다. 공공 인프라와 군수의 조달 루트는 철도 내장이나 항공우주 캐빈의 부속품 등 틈새 식모 용도를 지원하고 자동차 생산 대수의 정체에도 불구하고 기준선 수요를 유지하고 있습니다.

유럽에서는 엄격한 규제와 혁신 리더십이 융합되어 있습니다. 동대륙의 서큘러 이코노미 행동계획은 2027년까지 기기에 탈착 가능한 배터리를 탑재할 것을 의무화하고 있으며, 사용 종료 시에 플록이 깨끗이 분리되어야 하는 새로운 박리 가능한 접착제의 틈새를 만들어 내고 있습니다. Power Adhesives와 같은 기업은 최근 바이오 성분을 44% 포함한 인증된 생분해성 핫멜트 시스템을 발표했습니다. 남미, 중동, 아프리카는 전체적으로 수량은 겸손하지만 공급망의 다양화에 따라 중요성이 높아지고 있습니다. 브라질은 현지 조달의 모발 트림에 의존하는 자동차 조립 능력을 확대하고, 걸프의 석유 화학 통합은 경쟁력있는 수지 원료를 제공합니다. 아프리카 시장은 아직 초기 단계에 있지만, 고성장 도시에 근접한 소비자용 전자기기 패키지 제조업체로부터 투자를 끌고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 코팅 원단과 고급 마감 제품 수요 급증

- 자동차 내장 부품의 경량화, 저탄소화가 채용을 뒷받침

- 수성/VOC 프리 화학물질로의 규제 변화

- 전기자동차 배터리 팩의 플록 가공 열 관리 라이너

- 컨슈머 일렉트로닉스의 패키지에 있어서 프리미엄인 박스 개방 미학

- 시장 성장 억제요인

- 휘발성 이소시아네이트와 아크릴레이트 원료 가격

- 용제 배출 규제 강화

- 레이저 텍스처링과 대체 마무리에 의한 경쟁

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 수지 유형별

- 아크릴

- 폴리우레탄

- 에폭시

- 기타 수지 유형(알키드, 시아노아크릴레이트 등)

- 용도별

- 자동차

- 섬유

- 종이 및 포장

- 기타 용도(인쇄 및 그래픽 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- Argent International

- Arkema

- Dow

- HB Fuller Company

- Henkel AG and Co. KGaA

- International Coatings

- Kissel Wolf GmbH

- Nyatex

- Parker Hannifin

- Sika AG

- Stahl Holdings BV

- SwissFlock AG

- Toyochem Co. Ltd.

제7장 시장 기회와 향후 전망

KTH 25.11.13The Flock Adhesives Market size is estimated at USD 2.94 billion in 2025, and is expected to reach USD 3.85 billion by 2030, at a CAGR of 5.54% during the forecast period (2025-2030).

Growth is anchored in automotive interior demand, accelerated by rising electric-vehicle (EV) production, and reinforced by premium packaging requirements that emphasize soft-touch aesthetics and thermal functionality. Regulatory shifts toward water-based and VOC-free chemistries are prompting rapid product reformulation, especially as the European Union restricts diisocyanates and China tightens interior-emission limits. Automotive applications command the largest slice of the flock adhesives market at 42.56% in 2024 and also expand the fastest at 6.42% CAGR, underscoring the segment's dual role as volume base and innovation engine. Asia-Pacific retains geographic leadership with 51.84% share in 2024 and a 6.19% CAGR outlook through 2030, benefiting from concentrated automotive manufacturing footprints and expanding EV battery capacity. Meanwhile, polyurethane resin systems dominate with 38.19% share, yet "other" chemistries display the strongest 6.65% CAGR as formulators pivot toward acrylic, epoxy and non-isocyanate alternatives to stay ahead of incoming regulation.

Global Flock Adhesives Market Trends and Insights

Surging Demand for Coated Fabrics and Luxury Finish Products

Automotive and luxury-goods producers are stepping up use of flocked materials to signal elevated quality. Cabin parts such as dashboards, pillars and storage trays gain a plush feel that improves grip and cuts rattling noise. Premium packaging makers adopt the same technology so that jewelry boxes or smartphone cases feel exclusive from first touch. The tactile upgrade supports higher retail prices and strengthens brand differentiation. Together these factors translate into a wider, more stable demand base for flock adhesives.

Lightweight, Low-Carbon Vehicle Interior Parts Push Adoption

Car makers are substituting heavy fasteners with adhesive-bonded composite panels to shave grams from every model. Flock adhesives secure thin plastics and fabric laminates while meeting crash, vibration and durability tests. Mass reductions directly extend EV driving range, a metric closely watched by consumers and regulators. Assembly lines also benefit because fewer clips and screws cut cycle times and simplify recycling. As electrification spreads, the weight-saving argument keeps flock solutions on engineering shortlists.

Volatile Isocyanate and Acrylate Feedstock Prices

Adhesive makers rely on petrochemical derivatives whose costs whipsaw with oil and supply-chain shocks. Recent methacrylic-acid oversupply drove a 12% price drop, only for resin producers to impose sharp increases weeks later. Long fixed-price contracts with automotive OEMs limit the ability to pass surcharges through. Smaller formulators are especially exposed because they lack hedging scale and diversified portfolios. Margin uncertainty discourages bold capacity investments during turbulent periods.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift Toward Water-Based / VOC-Free Chemistries

- Flocked Thermal-Management Liners in Electric Vehicles Battery Packs

- Tightening Solvent-Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane captured 38.19% of flock adhesives market share in 2024, buoyed by broad compatibility with automotive substrates and strong thermal resilience. Yet regulatory scrutiny of isocyanates is shifting demand, evidenced by the 6.65% CAGR projected for "other" resin types. The flock adhesives market size for non-isocyanate chemistries is expected to outpace incumbents as acrylic and epoxy alternatives gain traction, driven by inherently lower VOCs and simplified handling. Henkel's bio-based polyurethane containing 71% renewable content demonstrates a 60% CO2 reduction versus standard formulas, signaling how sustainability narratives translate into purchasing criteria.

Regulators require worker training and stricter labelling for diisocyanate products, prompting OEMs to request compliant substitutes. Formulators respond by scaling acrylic dispersions and non-isocyanate polyurethane (NIPU) chemistries that meet adhesion, flexibility and heat-cycling needs without surpassing 0.1% diisocyanate thresholds. Suppliers able to balance compliance, performance and cost will command premium margins as legacy options face phased restriction.

The Flock Adhesives Market Report is Segmented by Resin Type (Acrylic, Polyurethane, Epoxy, Other Resin Types), Application (Automotive, Textiles, Paper and Packaging, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 51.84% flock adhesives market share in 2024 and is set to grow at 6.19% CAGR through 2030. China anchors regional demand as domestic brands and export-oriented assemblers adopt flocked interiors to elevate perceived quality and meet low-VOC mandates. Sika's new Liaoning and Singapore plants illustrate local capacity investments aimed at shortening lead times and tailoring chemistries for emerging battery-thermal needs. Japan and South Korea complement volume with materials science leadership, scaling epoxy-based and low-formal-emission systems for electronics as well as autos.

North America follows with mature but technologically demanding consumption. OEMs enforce strict sourcing criteria on sustainability and supply-chain transparency, incentivizing rapid adoption of water dispersions and bio-based content. Public infrastructure and military procurement channels support niche flocked applications in rail interiors and aerospace cabin fittings, keeping baseline demand intact despite plateaued vehicle output.

Europe blends tight regulation with innovation leadership. The continent's Circular Economy Action Plan requires removable batteries in devices by 2027, spawning new debondable-adhesive niches where flock must cleanly separate at end-of-life. Companies like Power Adhesives recently introduced certified biodegradable hot-melt systems containing 44% bio-based content, a template likely to spread into flock formulations. South America, the Middle East and Africa collectively represent modest volumes but rising importance as supply chains diversify. Brazil expands automotive assembly capacity that relies on locally sourced flocked trims, while petrochemical integration in the Gulf provides competitive resin feedstock. African markets remain early-stage yet draw investment from consumer-electronics packagers seeking proximity to high-growth urban centers.

- 3M

- Argent International

- Arkema

- Dow

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- International Coatings

- Kissel + Wolf GmbH

- Nyatex

- Parker Hannifin

- Sika AG

- Stahl Holdings B.V.

- SwissFlock AG

- Toyochem Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for coated fabrics and luxury finish products

- 4.2.2 Lightweight, low-carbon vehicle interior parts push adoption

- 4.2.3 Regulatory shift toward water-based / VOC-free chemistries

- 4.2.4 Flocked thermal-management liners in electric vehicles battery packs

- 4.2.5 Premium unboxing aesthetics in consumer-electronics packaging

- 4.3 Market Restraints

- 4.3.1 Volatile isocyanate and acrylate feedstock prices

- 4.3.2 Tightening solvent-emission regulations

- 4.3.3 Competition from laser-texturing and alternative finishes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Polyurethane

- 5.1.3 Epoxy

- 5.1.4 Other Resin Types (Alkyd, Cyanoacrylate, etc.)

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Textiles

- 5.2.3 Paper and Packaging

- 5.2.4 Other Applications (Printing and Graphics, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Argent International

- 6.4.3 Arkema

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG and Co. KGaA

- 6.4.7 International Coatings

- 6.4.8 Kissel + Wolf GmbH

- 6.4.9 Nyatex

- 6.4.10 Parker Hannifin

- 6.4.11 Sika AG

- 6.4.12 Stahl Holdings B.V.

- 6.4.13 SwissFlock AG

- 6.4.14 Toyochem Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment