|

시장보고서

상품코드

1851602

단열 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Thermal Insulation Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

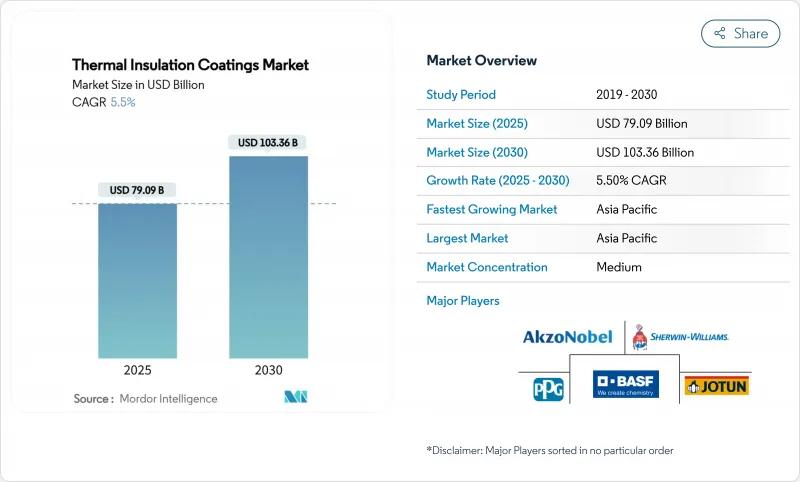

단열 코팅 시장 규모는 2025년에 790억 9,000만 달러로 추정되며 예측 기간(2025-2030년)의 CAGR은 5.5%로, 2030년에는 1,033억 6,000만 달러에 달할 것으로 예상됩니다.

이 실적은 기존의 건축 용도를 훨씬 뛰어넘어 전기 공정 열 시스템, LNG 인프라, 배터리 열 관리에 이르는 수요의 지속을 시사합니다. 에너지 효율 규정의 시행, 탈탄소화의 의무화, 유럽 전역에서 4세대 지역 난방 그리드의 구축에 의해 1200℃를 넘는 사용 온도에 대응할 수 있는 고도의 단열재의 채용이 가속하고 있습니다. 이와 병행하여 아시아태평양의 산업 확대가 정유소, 석유화학, 자동차 부품의 고성능 코팅 고객 기반을 확대하고, 북미 항공우주 프로그램이 초고온 이트리아 안정화 지르코니아(YSZ) 시스템의 채용을 자극하고 있습니다. 그 결과 생기는 경쟁 환경은 0.020W m-1 K-1 이하의 열전도율을 실현하는 에어로겔과 에폭시의 하이브리드 배합 등 수직 통합과 재료 과학의 진보를 조합한 공급자에게 보상하게 됩니다.

세계의 단열 코팅 시장 동향과 인사이트

새로운 정유소 건설

세계 정유소 건설은 단열 코팅 시장을 계속 지원합니다. 인도, 중국, 아라비아 만의 새로운 조합에서는 증류탑과 열교환기 쉘에 다층 에폭시 수지 장벽이 사용되며, 그 온도는 200°C-800°C 사이입니다. 프로젝트 소유자는 계획되지 않은 정지를 억제하고 자산의 수명을 연장하기 위해 내식성과 디지털 막 두께 모니터링을 동일한 코팅 패키지에 번들로 늘어나고 있습니다. 정상적인 온도 환경과 주기적인 온도 환경 모두에 해당하는 시스템을 인증할 수 있는 공급업체는 대규모 자본 프로젝트의 파이프라인에 대한 액세스를 획득했습니다.

지역냉난방망 확대

4세대 지역 냉난방망은 보다 낮은 공급 온도에서 운용되기 때문에 열 사이클의 반복을 견디면서 배전 손실을 저감할 수 있는 코팅이 요구됩니다. 덴마크의 지자체 에너지 협동조합은 고급 단열재가 연간 열 손실을 몇 퍼센트 줄이고 히트 펌프 효율을 향상시킬 수 있음을 입증합니다. 독일과 스웨덴에서는 보다 엄격한 보온 목표를 달성하기 위해 에어로겔 프라이머를 사용하여 유사한 개조가 이루어지고 있습니다.

높은 자본 요건

플라즈마 스프레이 부스, 자동 갠트리 및 제어된 대기압 경화 오븐은 수백만 달러의 비용이 소요되므로 신규 진입 생산 능력이 제한됩니다. 따라서 대규모 종합 제조업체가 장기 공급 계약을 독점하는 반면 소규모 애플리케이터는 자금 조달 장애물에 직면하고 있습니다. 다각화된 화학 그룹 내 최근 매각 논의에서 볼 수 있듯이 포트폴리오 재구성은 자본 집계의 압력을 강조합니다.

부문 분석

에폭시 시스템은 정유소 배관, 해양 데크 플레이트, 해양 플랫폼에 적합한 강력한 접착력과 내약품성에 힘입어 2024년 단열 코팅 시장에서 36.19%의 점유율을 유지했습니다. 이 제품은 APAC 및 중동에서 예정된 보호 라이닝 프로젝트의 단열 코팅 시장 규모의 대부분을 지원합니다. 중공 유리 미소구를 포함한 강화 배합에 의해 막의 강인성을 희생하지 않고 열전도율을 0.180W m-1 K-1 이하로 할 수 있습니다.

실리카 에어로겔 코팅은 현재 한 자리수의 매출 밖에 없지만, 2030년까지의 CAGR은 5.91%를 나타낼 전망입니다. 0.015 W m-1 K-1이라는 초저전도율은 한때 진공 단열 패널을 필요로 하는 상압 용도를 해제합니다. 제조업체는 에어로겔 분말을 에폭시 매트릭스에 공분산시킴으로써 기계적 강도와 초절연에 가까운 성능을 양립시켜, 이 분야가 장래의 사양에 미치는 영향력을 크게 하고 있습니다. 항공우주 프론티어에서는 엔트로피 안정화 산화물과 YSZ 플랫폼이 1,200℃ 이상에서 작동하는 터빈 블레이드 스킨을 대상으로 하며 추가 기술 크로스오버 기회를 제시합니다.

액체 용사 라인은 2024년 단열 코팅 시장 점유율의 45.19%를 차지했고 CAGR 6.45%로 다른 형태를 능가하고 있습니다. 주요 이점은 용접 피팅와 굽힘 반경을 원활하게 커버하고 로봇 통합 스프레이 헤드로 생산 속도를 향상시키는 것입니다. 공정 야드는 현재 습식 필름의 두께를 측정하고 건 속도를 자체 수정하는 비전 분석을 도입하고 오버 스프레이를 최소화하고 수율을 향상시킵니다. 파우더 라인은 그리드 쉘 아키텍처와 정전 인력에 의해 균일 한 멤브레인이 형성되는 특정 파이프라인 외부와 계속 관련이 있습니다.

단열 코팅 시장 보고서는 수지 유형(아크릴, 에폭시, 폴리우레탄, 기타), 코팅 형태(액체 스프레이, 분말, 진공 증착), 용도(건축 외벽, 산업 기기 및 파이프라인, 저장 탱크 및 용기, 기타), 최종 사용자 산업(건축 및 건설, 산업/제조, 자동차, 기타), 지역(아시아태평양, 북미, 유럽, 기타)로 구분

지역 분석

아시아태평양은 2024년 매출의 40.08%를 차지하며, 이는 중국, 인도, 한국의 거대 프로젝트 파이프라인을 반영했습니다. 이 지역의 정부는 정유소의 자급자족을 우선하고 있으며, 이것이 단열 코팅 시장을 직접 밀어 올리고 있습니다. 또한 일본의 LNG 콜드체인 터미널과 동남아시아 섬들에게 서비스를 제공하는 부체식 저장 재기화 유닛도 기세를 늘리고 있습니다.

북미는 항공우주 추진 프로그램과 중산업 골목에서 공정 열전화 조종사에 의해 지원됩니다. 연방 정부의 경기 자극 패키지는 배전 손실을 줄이는 첨단 코팅 오버레이로 지자체 유틸리티를 유도하고 지역 에너지 개수를 장려합니다. 2020년 캐나다 건축물 에너지 기준법과 같은 규제는 벽 구조물의 내열 요건을 끌어올려 세라믹 미소구 스프레이 도포 제품의 재 수요를 지원합니다.

유럽은 정책 주도의 탈탄소화로 리더십을 유지하고 가장 밀도가 높은 지역 난방 시장을 독점하고 있기 때문에 현장에서 열 사이클 내구성이 검증된 코팅의 지속적인 사양 업그레이드가 촉진되고 있습니다. 신축중산업 부족은 고온 히트펌프 시스템을 갖춘 노후산업단지의 리노베이션에 중점을 두고 있으며, 여기서 코팅은 열유 루프의 전도 손실을 완화하고 있습니다. 한편 중동 및 아프리카에서는 석유화학산업단지 채용을 확대하기 위해 석유설비투자계획을 활용하고 남미 광업지대에서는 부식성이 강한 산과 1일 온도차에 대한 공정용기의 완충재로서 코팅을 채용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신규 정유소의 건설

- 지역 냉난방 네트워크의 확대

- 건설 업계 수요 증가

- 중산업에서 공정 열의 전기

- LNG 콜드체인 물류의 급증

- 시장 성장 억제요인

- 높은 자본 요건

- 휘발성 원료(에폭시와 PU) 가격

- 초고온 자산에 있어서 한정적인 적용성

- 공급망 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 수지 유형별

- 아크릴

- 에폭시

- 폴리우레탄

- 이트리아 안정화 지르코니아(YSZ)

- 기타 수지 유형(실리카 에어로겔 기반 등)

- 코팅 형태별

- 액체 스프레이

- 분말

- 진공 증착

- 용도별

- 건물 외벽(벽, 지붕)

- 산업 장비 및 파이프라인

- 저장 탱크 및 용기

- 자동차 부품

- 선체 갑판 및 구조물

- 항공우주 및 터빈 부품

- 최종 사용자 업계별

- 건축 및 건설

- 산업/제조업

- 자동차

- 해양

- 기타(식품 가공, 제약)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- AkzoNobel NV

- BASF

- Behr Process LLC

- DAW SE

- Dow

- Evonik Industries AG

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd

- Mascoat

- Nippon Paint Holdings Co., Ltd

- OC Oerlikon Management AG

- PPG Industries, Inc.

- RPM International

- Sharpshell Engineering

- Sika AG

- Synavax

- The Sherwin-Williams Company

제7장 시장 기회와 향후 전망

KTH 25.11.13The Thermal Insulation Coatings Market size is estimated at USD 79.09 billion in 2025, and is expected to reach USD 103.36 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

This performance signals sustained demand that now stretches far beyond conventional construction use cases and into electrified process-heat systems, LNG infrastructure, and battery thermal management. Enforceable energy-efficiency codes, mounting decarbonization mandates, and the build-out of fourth-generation district-heating grids across Europe are accelerating the adoption of advanced thermal barriers capable of service temperatures above 1,200 °C. In parallel, Asia-Pacific's industrial expansion is widening the customer base for high-performance coatings in refineries, petrochemicals, and automotive components, while North American aerospace programs are stimulating uptake of ultra-high-temperature yttria-stabilized zirconia (YSZ) systems. The resulting competitive environment rewards suppliers that combine vertical integration with materials science advances, such as hybrid aerogel-epoxy formulations that deliver sub-0.020 W m-1 K-1 thermal conductivity.

Global Thermal Insulation Coatings Market Trends and Insights

Construction of New Refineries

Global refinery buildouts continue to anchor the thermal insulation coatings market. New complexes in India, China, and the Arabian Gulf specify multilayer epoxy barriers for distillation towers and heat-exchanger shells that run between 200 °C and 800 °C. Project owners increasingly bundle corrosion resistance and digital thickness monitoring into the same coating package to curb unplanned outages and extend asset life. Suppliers that can certify systems for both normal and cyclic temperature environments gain access to the largest capital projects pipeline.

Expansion of District Heating and Cooling Networks

Fourth-generation district-heating grids operate at lower supply temperatures, demanding coatings capable of reducing distribution losses while surviving repetitive thermal cycling. Denmark's municipal energy cooperatives demonstrate that advanced insulation can shave multiple percentage points from annual heat losses, thereby improving heat-pump efficiency. Similar retrofits across Germany and Sweden specify aerogel-infused primers to meet the stricter heat-retention targets.

High Capital Requirement

Plasma-spray booths, automated gantries, and controlled-atmosphere curing ovens can cost several million USD, limiting new-entrant capacity. Large integrated producers therefore dominate long-run supply contracts, while smaller applicators face financing hurdles. Portfolio restructuring, as seen in recent divestiture discussions inside diversified chemistry groups, underscores capital intensity pressures.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Construction Industry

- Electrification of Process-Heat in Heavy Industry

- Volatile Raw-Material (Epoxy and PU) Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy systems retained a 36.19% share of the thermal insulation coatings market in 2024, buoyed by strong adhesion and chemical resistance that suit refinery piping, marine deck plates, and offshore platforms. They underpin a significant portion of the thermal insulation coatings market size for protective-lining projects scheduled across APAC and the Middle East. Enhanced formulations embed hollow-glass microspheres to bring thermal conductivity below 0.180 W m-1 K-1 without sacrificing film toughness.

Silica-aerogel coatings, while holding only single-digit revenue today, record a 5.91% CAGR to 2030. Ultra-low conductivity readings of 0.015 W m-1 K-1 unlock ambient-pressure applications that once demanded vacuum-insulated panels. Manufacturers co-disperse aerogel powder into epoxy matrices to combine mechanical strength with near-super-insulating performance, giving the segment outsized influence on future specifications. At the aerospace frontier, entropy-stabilized oxide and YSZ platforms target turbine-blade skins running above 1,200 °C, suggesting further technology crossover opportunities.

Liquid spray lines captured 45.19% of thermal insulation coatings market share in 2024 and continue to outpace other forms at a 6.45% CAGR. Their chief advantages include seamless coverage on weld seams and radius bends, plus production-rate gains from robot-integrated spray heads. Process yards now deploy vision analytics to gauge wet-film thickness and self-correct gun speed, minimizing overspray and improving yield. Powder lines remain relevant in gridshell architecture and certain pipeline externals where electrostatic attraction ensures uniform film builds.

The Thermal Insulation Coatings Market Report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, and More), Coating Form (Liquid Spray, Powder, Vacuum-Deposited), Application (Building Envelope, Industrial Equipment and Pipelines, Storage Tanks and Vessels, and More), End-User Industry (Building and Construction, Industrial/Manufacturing, Automotive, and More), and Geography (Asia Pacific, North America, Europe, and More).

Geography Analysis

Asia-Pacific holds 40.08% of 2024 revenue, reflecting megaproject pipelines in China, India, and South Korea. Regional governments prioritize refinery self-sufficiency, which directly inflates the thermal insulation coatings market. Added momentum comes from LNG cold-chain terminals in Japan and floating storage regasification units serving Southeast Asian islands.

North America is assisted by aerospace propulsion programs and process-heat electrification pilots in heavy industry alleys. Federal stimulus packages encourage district-energy retrofits, steering municipal utilities toward advanced coating overlays that lower distribution losses. Regulations like Canada's National Energy Code for Buildings 2020, which lifts thermal-resistance requirements for wall assemblies, anchor recurrent demand for spray-applied ceramic microsphere products.

Europe maintains leadership in policy-driven decarbonization and commands the densest district-heating market, fostering continuous specification upgrades for coatings with validated ex-situ thermal-cycling endurance. Scarcity of new-build heavy industry shifts focus to retrofitting aging industrial parks with high-temperature heat-pump systems, where coatings moderate conductive losses on hot-oil loops. Meanwhile, the Middle-East and Africa leverages oil-capex programs to expand adoption in petrochemical parks, whereas South America's mining belts employ coatings to buffer process vessels against aggressive acids and wide daily temperature swings.

- AkzoNobel N.V.

- BASF

- Behr Process LLC

- DAW SE

- Dow

- Evonik Industries AG

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd

- Mascoat

- Nippon Paint Holdings Co., Ltd

- OC Oerlikon Management AG

- PPG Industries, Inc.

- RPM International

- Sharpshell Engineering

- Sika AG

- Synavax

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction of New Refineries

- 4.2.2 Expansion of District Heating and Cooling Networks

- 4.2.3 Increasing demand for the construction industry

- 4.2.4 Electrification of Process-Heat in Heavy Industry

- 4.2.5 Surge in LNG Cold-Chain Logistics

- 4.3 Market Restraints

- 4.3.1 High Capital Requirement

- 4.3.2 Volatile Raw-Material (Epoxy and PU) Prices

- 4.3.3 Limited Applicability in Ultra High Temperature Assets

- 4.4 Supply Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Yttria-Stabilised Zirconia (YSZ)

- 5.1.5 Other Resin Types (Silica Aerogel-Based, etc.)

- 5.2 By Coating Form

- 5.2.1 Liquid Spray

- 5.2.2 Powder

- 5.2.3 Vacuum-Deposited

- 5.3 By Application

- 5.3.1 Building Envelope (Walls, Roofs)

- 5.3.2 Industrial Equipment and Pipelines

- 5.3.3 Storage Tanks and Vessels

- 5.3.4 Automotive Components

- 5.3.5 Marine Hull and Deck Structures

- 5.3.6 Aerospace and Turbine Parts

- 5.4 By End-user Industry

- 5.4.1 Building and Construction

- 5.4.2 Industrial/Manufacturing

- 5.4.3 Automotive

- 5.4.4 Marine

- 5.4.5 Others (Food Processing, Pharma)

- 5.5 By Geography

- 5.5.1 Asia Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 BASF

- 6.4.3 Behr Process LLC

- 6.4.4 DAW SE

- 6.4.5 Dow

- 6.4.6 Evonik Industries AG

- 6.4.7 Hempel A/S

- 6.4.8 Jotun

- 6.4.9 Kansai Paint Co., Ltd

- 6.4.10 Mascoat

- 6.4.11 Nippon Paint Holdings Co., Ltd

- 6.4.12 OC Oerlikon Management AG

- 6.4.13 PPG Industries, Inc.

- 6.4.14 RPM International

- 6.4.15 Sharpshell Engineering

- 6.4.16 Sika AG

- 6.4.17 Synavax

- 6.4.18 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment