|

시장보고서

상품코드

1851619

오소바이오로직스 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Orthobiologics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

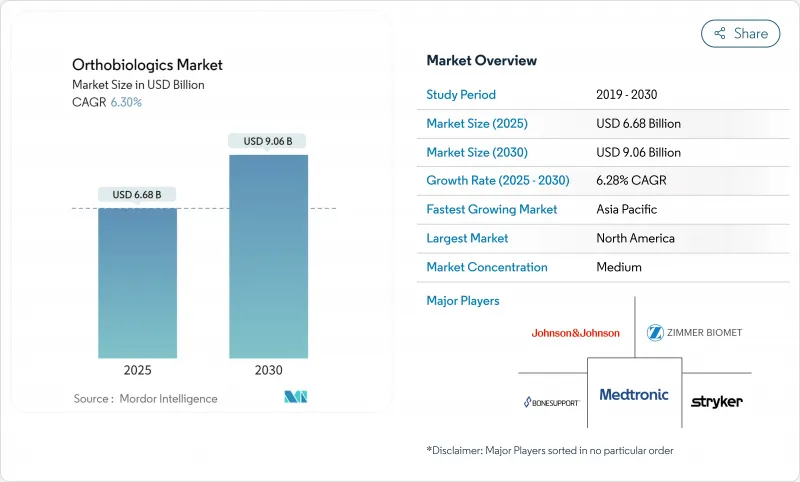

오소바이오로직스 시장 규모는 2025년에 66억 8,000만 달러, 2030년에는 90억 6,000만 달러에 이를 것으로 예측되며, CAGR은 6.28%를 나타낼 전망입니다.

이 성장은 개복 수술에서 치유를 빨리 장기적인 기능을 개선하는 생물학적 주도의 저침습 치료로 꾸준히 전환하고 있기 때문입니다. 성과 보상형 모델, 스포츠 관련 상해의 급증, 외래 수술 네트워크의 확대에 의해 수요는 취급하기 쉬운 주사제나 합성 이식편 제품으로 향하고 있습니다. 북미는 양호한 커버리지와 깊은 임상 전문 지식을 바탕으로 주도적 지위를 유지하고 있지만, 아시아태평양은 현지 의료기기 제조업체가 생산 규모를 확대하고 규제 당국이 승인을 합리화함에 따라 가속화하고 있습니다. 경쟁업체 간의 적대관계는 선도적인 의료기기 제조업체가 재생의료 포트폴리오를 확대하고 민첩한 신흥기업이 기존의 이식편에 과제하는 펩티드 스캐폴드와 디지털 플래닝 플랫폼을 도입함에 따라 첨예화되고 있습니다.

세계의 오소바이오로직스 시장 동향과 인사이트

신속한 생물학적 치유가 필요한 고성능 스포츠 의학 절차의 급증

운동 선수와 활동적인 성인 수요는 다혈소판 혈장(PRP)과 간엽 줄기 세포(MSC)의 사용을 뒷받침하고 있습니다. 무작위 연구는 외상 과염과 골관절염에서 코르티코 스테로이드에 비해 우수한 증상 완화와 조직 회복 속도를 보여줍니다. 팀 닥터는 이러한 생물학적 제제를 첫 번째 선택 요법으로 옮기고 재활을 단축하며 경쟁 리그에서 조기 플레이 복귀를 지원합니다.

골관절염 관리에서 히알루 론산 다중 주사 프로토콜의 가속 채택

ViSCNOVAS와 같은 새로운 분류 도구는 임상가가 점도와 가교 특성에 따라 가장 효과적인 제형을 선택할 수 있도록 안내하고 임상 일관성을 향상시킵니다. 일본과 미국의 대규모 정형외과 진료소에서는 현재 단회 주사 제형에 비해 장기 통증 완화와 관절 기능 향상을 보여주는 3회 주사 요법이 지지되고 있습니다.

오소바이오로직스 자가세포를 이용한 치료에 대한 보험 상환 틀의 부족 자가부담 비용 증가

선도적인 보험 회사는 많은 MSC 주사에 임상시험 약이라고 하는 레텔을 붙이고 있습니다. 따라서 환자는 자기 부담이 되고 사회경제적으로 높은 층에 대한 접근이 제한되고 일상적인 도입이 지연됩니다.

부문 분석

관절내 보충요법은 2024년 오소바이오로직스 시장 점유율의 61.34%를 차지하며, 지불보험사의 적용 범위와 예측 가능한 치료효과에 의해 변형성 무릎관절증의 주력치료제로 남았습니다. 관절 내 보충 요법과 관련된 오소바이오로직스 시장 규모는 여러 주사 프로토콜이 지속적인 완화를 입증함에 따라 꾸준히 상승할 것으로 보입니다. 가교제제의 연구도 병행하여 진행되고 있어 관절강 내에서의 체류시간이 연장되어 병원의 처방전에 채용되는 프리미엄층이 형성되고 있습니다.

줄기세포 치료는 2025년 매출 기준으로는 한 자리수 중반에 불과하지만 CAGR은 9.20%로 제품 믹스 중에서 가장 빠릅니다. Ryoncil의 FDA 승인은 동종 이식 플랫폼의 효과를 입증하며 Cocoon과 같은 자동 생물반응기는 배치 간의 편차와 비용 절감을 약속합니다. 탈회골 매트릭스, 동종이식편, 뼈 형태형성 단백질은 복잡한 융합을 관리하는 외과의사에게 여전히 중요하며, 레노보스의 펩티드 고정형 BMP-2는 중요한 데이터가 성숙하면 미국에서 판매될 예정입니다.

무릎 관절 수술은 2024년 매출의 35.29%를 차지하며, 고령화하면서도 활동적인 사람들 사이에서 변형성 관절증이나 인대 손상의 발생률이 높은 것으로 지지되었습니다. 임상 지침은 무릎 퇴행성 질환에 대한 부신 피질 스테로이드보다 PRP를 선호하며 치료 건수가 증가하고 있습니다.

발과 발목 분야는 베이스는 작지만 기존의 이식편에서는 충분한 효과를 얻을 수 없는 아킬레스건이나 중족부의 재건에 생물학적 제제를 적용하는 의사가 증가하고 있으며, CAGR은 8.74%를 나타낼 전망입니다. 척추는 고정술의 필요성에서 계속 핵심이며, 고관절, 어깨 관절 및 팔꿈치 관절은 스포츠 외과 의사가 힘줄과 관절 입술의 복구 프로토콜을 확대함에 따라 점유율을 계속 확대하고 있습니다.

지역 분석

북미는 2024년 세계 매출의 43.52%를 차지했습니다. 미국에서는 관절내 보충요법에 대한 상환의 틀이 성숙하고 있어 외래센터로의 수술의 이행이 급속히 진행되고 있습니다. 미국의 오소바이오로직스 시장 규모는 RENOVITE BMP-2와 같은 합성 이식편이 획기적인 지정으로 상시까지의 기간이 단축됨에 따라 CAGR 5.86%로 확대되고 있습니다. 캐나다는 이러한 추세를 반영하고 있으며, 각 국가의 계획에서 변형성 무릎 관절증에 대한 PRP가 점차 추가되고 있습니다.

유럽은 두 번째로 CAGR 6.19%를 나타낼 전망입니다. 독일, 프랑스, 이탈리아에서는 채용이 꾸준히 진행되고 있으며, 주 의료제도가 확립된 이식편을 상환하고 있습니다. 새로운 SoHO 규칙에 대한 대응 작업으로 조직 유래 요법의 승인주기가 늘어나면서 본 지원 회사와 같은 기업은 장치 코드로 지울 수 있는 합성 매트릭스를 선호합니다. 북유럽 국가는 지불자의 신뢰를 높이는 레지스트리 기반 증거 작성을 이끌고 있습니다.

아시아태평양은 CAGR 8.62%로 가장 빠르게 성장하고 있습니다. 일본의 히알루론산 다중 주사 프로토콜은 임상 벤치마크를 설정하고, 중국의 "건강한 중국 2030" 로드맵은 국내 혁신자에게 범용 동종이식편에서 고급 펩타이드 비계로의 업그레이드에 박차를 가하고 있습니다. 인도의 의료기술 정책은 2030년까지 의료기술 부문을 500억 달러로 확대하는 것을 목표로 현지 제조 인센티브를 개방하고 있습니다. 남미와 중동의 소규모이면서 고성장을 이루고 있는 시장은 민간보험의 적용 범위가 확대되어 곧바로 사용할 수 있는 주사제를 수입하는 전문의원 네트워크로부터 이익을 얻고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신속한 생물학적 치유를 필요로 하는 고성능 스포츠 의학 수술의 급증

- 골관절염 관리에서 히알루 론산 기반 다회 주사 관절 내 보충 요법 프로토콜의 채택 가속화

- 척추고정술에서 정형생물학적 보조구의 통합이 증가하고, 재수술률이 저하

- 정형외과 임상에서 PRP 및 세포 기반 치료를 지원하는 임상 증거의 확대

- 외래 환자 센터로의 업계 변화가 주사제와 곧바로 사용할 수 있는 골 이식편 대체품 수요를 견인

- 차세대 합성 펩티드 골 이식편의 신속한 파이프라인이 승인

- 시장 성장 억제요인

- 자기 세포 기반 정형 생물학적 제제에 대한 상환 프레임 워크의 부족은 자기 부담액을 증가

- 생물학적 제제의 규제 구분의 엄격화와 진화가 신규 제품 시장 투입까지의 시간을 증가

- PRP/줄기세포 제제에 있어서 높은 배치 간 편차와 표준화의 부족이 임상가의 신뢰를 손상

- 고도성장인자제제의 프리미엄 채용을 제한하는 동종이식편 공급업체로부터의 가격 공세

- 공급망 분석

- 규제 전망

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 점도 보충제 제품

- 탈염 뼈 기질

- 동종 이식편

- 합성 뼈 대체재

- 골형성 단백질

- 혈소판 풍부 플라즈마

- 줄기세포 치료법

- 기타 오소바이오로직스

- 수술 부위별

- 무릎

- 고관절

- 척추

- 어깨 및 팔꿈치

- 발 및 발목

- 기타 관절

- 투여 방법별

- 주사용 생물학적 제제

- 이식형/스캐폴드 이식편

- 국소 및 표면 코팅제

- 용도별

- 척추 유합술

- 스포츠 연부 조직 손상

- 외상 및 골절 회복

- 기타 용도

- 최종 사용자별

- 병원 및 정형외과 센터

- 외래 수술 센터(ASC)

- 스포츠 의학 및 재활 클리닉

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- Acumed LLC

- AlloSource

- Arthrex Inc.

- Bioventus Inc.

- BoneSupport AB

- Cerapedics Inc.

- Globus Medical Inc.

- Integra LifeSciences Holdings Corp.

- Isto Biologics

- Johnson & Johnson

- Kuros Biosciences AG

- Medtronic PLC

- MTF Biologics

- NuVasive Inc.

- Organogenesis Holdings Inc.

- Orthofix Medical Inc.

- Royal Biologics Inc.

- Stryker Corporation

- Terumo Corporation

- Zimmer Biomet Holdings Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.24The orthobiologics market size is USD 6.68 billion in 2025 and is forecast to reach USD 9.06 billion by 2030, reflecting a 6.28% CAGR.

Growth stems from the steady move away from open surgery toward biologically driven, minimally invasive care that speeds healing and improves long-term function. Pay-for-outcome models, a spike in sports-related injuries, and expanding outpatient surgery networks are channeling demand toward easy-to-handle injectable and synthetic graft products. North America retains leadership on the back of favorable coverage and deep clinical expertise, while Asia-Pacific is accelerating as local device makers scale up production and regulators streamline approvals. Competitive rivalry is sharpening as large device companies widen regenerative portfolios and agile start-ups introduce peptide scaffolds and digital-planning platforms that challenge legacy grafts.

Global Orthobiologics Market Trends and Insights

Surge in High-Performance Sports Medicine Procedures Requiring Rapid Biological Healing

Demand from athletes and active adults is boosting platelet-rich plasma (PRP) and mesenchymal stem cell (MSC) use. Randomized studies now show superior symptom relief and faster tissue recovery versus corticosteroids in lateral epicondylitis and knee osteoarthritis. Team physicians are moving these biologics to first-line therapy, shortening rehabilitation and supporting an early return to play across competitive leagues.

Accelerated Adoption of Hyaluronic-Acid Multi-Injection Protocols in Osteoarthritis Management

Novel classification tools such as ViSCNOVAS guide clinicians to choose the most effective formulation by viscosity and cross-linking features, improving clinical consistency. Large orthopedic practices in Japan and the United States now favor three-injection regimens that show longer pain relief and joint function gains compared with single-shot products.

Absence of Reimbursement Frameworks for Autologous Cell-Based Orthobiologics Elevating Out-of-Pocket Costs

Major insurers still label many MSC injections as investigational. Patients therefore self-pay, which restricts access to higher socioeconomic groups and slows routine adoption.

Other drivers and restraints analyzed in the detailed report include:

- Rising Integration of Orthobiologics Adjuncts in Spinal Fusion to Reduce Revision Surgery Rates

- Expanding Clinical Evidence Supporting PRP and Cell-Based Therapies in Orthopedic Clinics

- Stringent and Evolving Biologics Regulatory Classification Increasing Time-To-Market for Novel Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Viscosupplementation commanded 61.34% of orthobiologics market share in 2024 and remained a mainstay for knee osteoarthritis thanks to established payer coverage and predictable outcomes. The orthobiologics market size tied to viscosupplementation is set to climb steadily as multi-injection protocols demonstrate durable relief. Parallel research into cross-linked formulations is extending dwell time inside the joint space, creating premium tiers that hospital formularies are adopting.

Stem cell therapies hold only a mid-single-digit revenue base in 2025 yet are posting a 9.20% CAGR, the fastest within the product mix. FDA approval of Ryoncil validated allogeneic platforms, while automated bioreactors like Cocoon promise lower batch-to-batch variation and cost. Demineralized bone matrix, allografts, and bone morphogenetic proteins remain important for surgeons managing complex fusions, with Renovos' peptide-anchored BMP-2 poised to enter U.S. distribution once pivotal data mature.

Knee procedures accounted for 35.29% of 2024 revenue, underpinned by the high incidence of osteoarthritis and ligament injuries among aging yet active populations. Clinical guidelines now place PRP ahead of corticosteroids for degenerative knee disease, lifting unit volumes.

The foot and ankle segment holds a smaller base but is on track for an 8.74% CAGR as physicians apply biologics to Achilles and mid-foot reconstruction where traditional grafts underperform. Spine remains core because of fusion necessity, and hip, shoulder, and elbow continue to gain share as sports surgeons broaden rotator cuff and labral repair protocols.

The Orthobiologics Market Report is Segmented by Product (Viscosupplementation Products and More), Surgical Site (Knee, Hip, and More), Delivery Method (Injectable Biologics and More), Application (Spinal Fusion and More), End-User (Hospitals & Orthopedic Centers, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 43.52% of 2024 global revenue. Uptake in the United States is reinforced by a mature reimbursement framework for viscosupplementation and rapid procedure migration to ambulatory centers. The orthobiologics market size in the U.S. is expanding at 5.86% CAGR as breakthrough designations shorten the time to launch for synthetic grafts like RENOVITE BMP-2. Canada mirrors these trends, with provincial plans gradually adding PRP for knee osteoarthritis.

Europe ranks second and is growing at 6.19% CAGR. Adoption is steady in Germany, France, and Italy, where state health systems reimburse established grafts. Compliance work for new SoHO rules is extending approval cycles for tissue-derived therapies, so firms such as Bonesupport are prioritizing synthetic matrices that clear under device codes. Nordic countries lead registry-based evidence generation that bolsters payer confidence.

Asia-Pacific is the fastest riser at 8.62% CAGR. Japan's multi-injection hyaluronic acid protocols set clinical benchmarks, while China's "Healthy China 2030" roadmap is spurring domestic innovators to upgrade from commodity allografts to advanced peptide scaffolds. India's MedTech policy aims to scale the sector to USD 50 billion by 2030, opening local manufacturing incentives for orthobiologics. Smaller yet high-growth markets in South America and the Middle East benefit from rising private insurance coverage and specialist clinic networks that import ready-to-use injectables.

- Acumed

- AlloSource

- Arthrex

- Bioventus Inc.

- BoneSupport AB

- Cerapedics Inc.

- Globus Medical

- Integra LifeSciences Holdings Corp.

- Isto Biologics

- Johnson & Johnson

- Kuros Biosciences AG

- Medtronic

- MTF Biologics

- NuVasive

- Organogenesis

- Orthofix

- Royal Biologics Inc.

- Stryker

- Terumo

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in High-Performance Sports Medicine Procedures Requiring Rapid Biological Healing

- 4.2.2 Accelerated Adoption of Hyaluronic Acid-based Multi-Injection Viscosupplementation Protocols in Osteoarthritis Management

- 4.2.3 Rising Integration of Orthobiologic Adjuncts in Spinal Fusion to Reduce Revision Surgery Rates

- 4.2.4 Expanding Clinical Evidence Supporting PRP and Cell-Based Therapies in Orthopedic Clinics

- 4.2.5 Industry Shift Toward Outpatient Centers Driving Demand for Injectables and Ready-to-Use Bone Graft Substitutes

- 4.2.6 Rapid Pipeline of Next-Generation Synthetic Peptide Bone Grafts Approved Under Expedited Regulatory Pathways

- 4.3 Market Restraints

- 4.3.1 Absence of Reimbursement Frameworks for Autologous Cell-Based Orthobiologics Elevating Out-of-Pocket Costs

- 4.3.2 Stringent and Evolving Biologics Regulatory Classification Increasing Time-to-Market for Novel Products

- 4.3.3 High Batch-to-Batch Variability and Lack of Standardization in PRP/Stem Cell Preparations Undermining Clinician Confidence

- 4.3.4 Price Intensity from Commodity Allograft Providers Limiting Premium Adoption of Advanced Growth-Factor Formulations

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Viscosupplementation Products

- 5.1.2 Demineralized Bone Matrix

- 5.1.3 Allografts

- 5.1.4 Synthetic Bone Substitutes

- 5.1.5 Bone Morphogenetic Proteins

- 5.1.6 Platelet-Rich Plasma

- 5.1.7 Stem Cell Therapies

- 5.1.8 Other Orthobiologics

- 5.2 By Surgical Site

- 5.2.1 Knee

- 5.2.2 Hip

- 5.2.3 Spine

- 5.2.4 Shoulder & Elbow

- 5.2.5 Foot & Ankle

- 5.2.6 Other Joints

- 5.3 By Delivery Method

- 5.3.1 Injectable Biologics

- 5.3.2 Implantable/Scaffold Grafts

- 5.3.3 Topical & Surface Coatings

- 5.4 By Application

- 5.4.1 Spinal Fusion

- 5.4.2 Sports Soft-Tissue Injuries

- 5.4.3 Trauma & Fracture Recovery

- 5.4.4 Other Applications

- 5.5 By End-User

- 5.5.1 Hospitals & Orthopedic Centers

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Sports Medicine & Rehabilitation Clinics

- 5.5.4 Other End-Users

- 5.6 By Geography (Value)

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Acumed LLC

- 6.4.2 AlloSource

- 6.4.3 Arthrex Inc.

- 6.4.4 Bioventus Inc.

- 6.4.5 BoneSupport AB

- 6.4.6 Cerapedics Inc.

- 6.4.7 Globus Medical Inc.

- 6.4.8 Integra LifeSciences Holdings Corp.

- 6.4.9 Isto Biologics

- 6.4.10 Johnson & Johnson

- 6.4.11 Kuros Biosciences AG

- 6.4.12 Medtronic PLC

- 6.4.13 MTF Biologics

- 6.4.14 NuVasive Inc.

- 6.4.15 Organogenesis Holdings Inc.

- 6.4.16 Orthofix Medical Inc.

- 6.4.17 Royal Biologics Inc.

- 6.4.18 Stryker Corporation

- 6.4.19 Terumo Corporation

- 6.4.20 Zimmer Biomet Holdings Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment