|

시장보고서

상품코드

1851643

자동 컨텐츠 인식 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automatic Content Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

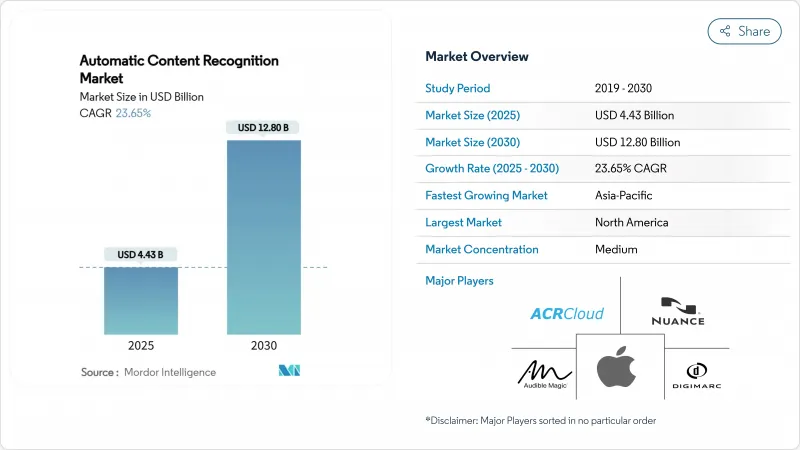

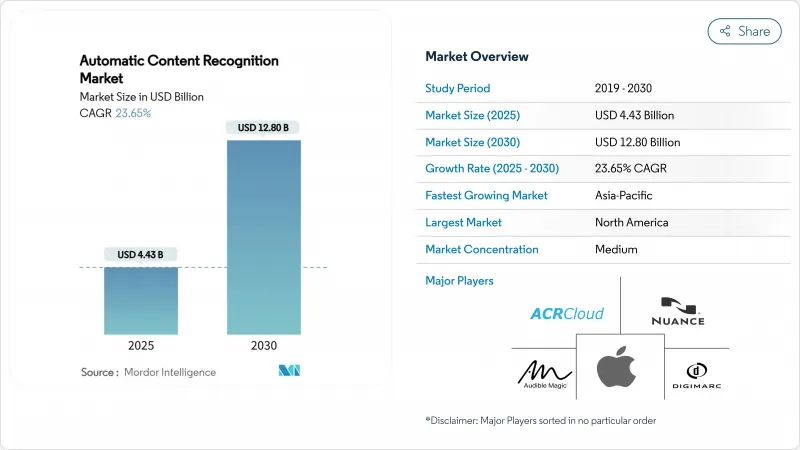

자동 컨텐츠 인식 시장은 2025년에 44억 3,000만 달러로 추정되고, 2030년에는 128억 달러에 이를 전망이며, CAGR 23.65%로 기세를 보이고 있습니다.

2025년 기준선은 스마트 TV의 광범위한 보급, 어드레서블 광고로의 결정적인 예산 이동, 최소한의 에너지 소비로 지문 작업을 로컬에서 수행할 수 있는 엣지 AI의 꾸준한 개선을 반영합니다. 2024년 애플의 Shazam이 누계 1,000억곡의 노래 인식을 기록한 획기적인 전개는 일상적인 소비자 환경에서 달성되는 규모의 크기를 보여줍니다. 디바이스 제조업체는 매일 ACR 실리콘을 보드 레벨에 통합하여 사용자 개입 없이 선형 방송, 스트리밍 앱, HDMI 입력에서 지속적인 서명 추출을 가능하게 합니다. 이 하드웨어의 피벗은 자동 컨텐츠 인식 시장의 주소 지정 가능한 데이터 풀을 확장하는 동시에 대기 시간을 단축합니다.

이 기세는 주요 데이터에서도 확인할 수 있습니다. 소프트웨어는 여전히 64%의 판매를 차지하지만 브랜드가 컴플라이언스와 모델 튜닝을 외주하기 때문에 관리형 클라우드 서비스는 24.48%의 속도로 확대되고 있습니다. 음성과 영상의 핑거프린팅은 여전히 46%의 점유율로 주요 기술이지만, 자동차 및 헬스케어에 있어서 음성 구동형의 이용 사례가 CAGR 24.11%로 가장 급속하게 확대하고 있습니다. 보안 및 저작권 보호는 29%의 점유율로 솔루션 지출의 대부분을 차지하지만, FAST 채널의 실시간 분석이 CAGR23.89%에서 가장 빠르게 성장하고 있습니다. 최종 사용자 믹스는 미디어 및 엔터테인먼트가 38%로 선도하고 있지만, 자동차 인포테인먼트가 음성 커머스의 파일럿에 의해 CAGR 23.78%로 차이를 줄이고 있습니다. 지역별로는 북미가 41%의 점유율을 획득하고 있는 반면 아시아태평양은 2030년까지 24.63%로 추이하고 있으며, 자동 컨텐츠 인식 시장의 활력이 성숙지역 및 신흥지역 모두에서 강화되고 있습니다.

세계의 자동 컨텐츠 인식 시장 동향 및 인사이트

ACR 칩 내장 스마트 TV 보급

스마트 TV 브랜드는 현재 ACR 처리를 용도 계층 아래에 위치한 시스템 온칩 블록으로 라우팅하여 프라이버 시트 글이 꺼져 있어도 지속적인 지문 획득을 가능하게 합니다. 삼성 기기는 약 1분마다, LG 모델은 15초마다 서명을 보내 라이브 방송, 스트리밍 앱 및 모든 HDMI 소스에 걸쳐 중단 없는 원격 측정 스트림을 만듭니다. 이러한 저지연 파이프라인은 광고 최적화를 위한 피드백 루프를 단축하고 자동 컨텐츠 인식 시장의 데이터 인벤토리를 확장합니다.

어드레서블 TV 광고 예산 확대

광고주는 프레임 수준의 ACR 인사이트를 활용하는 어드레서블 형식으로 광고비를 돌리고 있습니다. 어드레서블 TV에 대한 예산은 2025년에는 TV 총 지출의 3분의 1을 초과하고, 2027년에는 42%에 달하는 기세입니다. FAST의 유통업체는 이러한 인사이트를 프로그래매틱 워크플로우와 결합하여 인구통계 타겟팅을 넘어서는 참여를 실현하고 유럽의 새로운 HbbTV-TA 인증을 통해 기술적인 기준을 표준화합니다. 자동 컨텐츠 인식 시장은 정확하고 실시간 컨텐츠 라벨링에 의존하는 광고 삽입을 통해 이익을 얻고 있습니다.

e프라이버시법 개정에 의한 옵트인 동의 규칙의 엄격화

유럽 당국은 2024년 후반부터 보다 정교한 동의 배너와 'consent-or-pay' 지침을 시행하기 시작했으며, 스마트 TV 벤더에게 ACR 데이터를 핵심 기능과 분리하는 세밀한 토글을 만들도록 압박하고 있습니다. 컴플라이언스 준수는 엔지니어링 오버헤드를 늘리고 데이터 양을 줄일 수 있기 때문에 유럽 내 자동 컨텐츠 인식 시장의 성장 전망을 둔화시킵니다.

부문 분석

2024년 자동 컨텐츠 인식 시장 규모는 TV 운영 체제와 스트리밍 SDK에 확실히 통합된 코드로 소프트웨어 수익이 큰 점유율을 차지하고 있습니다. 그러나 OEM과 방송사가 모델 튜닝, 컴플라이언스, 업타임 관리를 아웃소싱하고 있기 때문에 클라우드 호스팅의 관리 서비스가 CAGR 24.48%로 확대되고 있습니다. Digimarc의 연간 경상 수익이 44% 증가한 2,390만 달러로 급증한 것은 개인정보보호규칙이 변화하는 가운데 턴키 컴플라이언스를 선호하는 고객에게 구독 과금이 어떻게 지지되고 있는지를 보여줍니다.

서비스 급증은 유지보수, 감사 로그 및 SLA 보증을 번들로 제공하는 OPEX 친화적인 계약에 대한 기업 IT의 광범위한 축을 반영합니다. 많은 중견 디바이스 브랜드의 경우 엔드 투 엔드 서비스를 라이선싱하는 것은 지역별 동의 프레임워크에 보조를 맞추어야 하는 사내 스택을 구축하는 것보다 낫습니다. 따라서 애널리스트는 소프트웨어가 기본적이면서 성장이 둔화되고 있는 동안 서비스가 2030년까지 매년 조금씩 자동 컨텐츠 인식 시장 점유율을 확대할 것으로 예상하고 있습니다.

음성 및 비디오 핑거프린팅은 라이브 TV 및 온디맨드 라이브러리에서 입증된 정확성으로 인해 성숙도와 수익의 46%를 차지합니다. 그러나 음성을 중심으로 한 인식은 자동 컨텐츠 인식 시장에서 가장 급성장하고 있으며, 차량용 음성 어시스턴트, 원격 건강 모니터링, 콘택트 센터 분석 등을 배경으로 24.11%의 성장을 이루고 있습니다. NTT의 초저지연 음성 변환은 실시간 품질이 기업의 임계값을 충족하는 방법을 돋보이게 합니다.

클라우드 체인에 비해 92%의 전력을 절감할 수 있는 엣지 실리콘은 배터리 구동 장치나 차량용 ECU로 음성 분석을 실현 가능하게 하고 있습니다. 한편, 전자 워터마크는 권리자에게 다시 중요성을 증가시키고, 광학 문자 인식은 소매업에서 판매량을 늘리고 있습니다. 이러한 궤적은 지문 알고리즘을 대체하지 않고 자동 컨텐츠 인식의 업계 툴킷을 다양화합니다.

자동 컨텐츠 인식 시장 보고서는 컴포넌트별(소프트웨어 및 서비스), 기술별(오디오 및 비디오 핑거 프린팅, 디지털 전자 워터마크 등), 솔루션별(실시간 컨텐츠 분석, 음성 및 음성 인터페이스 등), 최종 사용자 산업별(미디어 및 엔터테인먼트, 가전 제품 OEM, 통신 및 IT 등), 지역별로 분류됩니다.

지역 분석

북미는 2024년 자동 컨텐츠 인식 시장 매출의 41%를 차지했으며, 스마트 TV의 가구 보급률이 75%를 넘어서 어드레서블 광고 공급망이 확립되고 있는 것이 기여하고 있습니다. 플랫폼은 프레임 레벨 인식에 크게 의존하는 서버측 삽입을 통합하여 이 지역의 데이터의 이점을 증폭시킵니다. 연방정부의 개인정보보호법은 아직 초안 단계이지만, 주 수준의 규칙과 소비자의 의식이 높아짐에 따라 데이터의 흐름이 중기적으로 완화될 수 있으며, 벤더는 동의의 흐름을 강화하도록 촉구됩니다.

아시아태평양은 자동 성장 엔진이며 2030년까지 연평균 복합 성장률(CAGR)은 24.63%로 확대될 전망입니다. 스마트 TV의 대량 도입, 가처분 소득 증가, AI 실험실에 대한 정책적 지원이 협조하여 작용합니다. 한국 SK텔레콤과 LG CNS는 같은 ACR 음성을 기반으로 한 다국어 실시간 번역 레이어를 추가하고 있습니다. 현재 국회를 통과하는 일본의 AI 법안은 균형 잡힌 연구개발 가드 레일을 설정하고 공급업체에게 규제의 명확성을 부여하는 태세를 갖추고 있습니다. 중국에서는 국제 기업이 수출 장애물을 극복하면서 국내 칩 제조 및 알고리즘 하우스가 현지화된 스택에 박차를 가하고 있습니다. 이 누적 효과로 인해 APAC의 하위 지역 전반에 걸쳐 자동 컨텐츠 인식 시장이 활기차고 있습니다.

유럽은 기회와 제약이 섞여 있습니다. HbbTV-TA 인증은 광고교환을 위한 기술적인 길을 조화시켰지만, 이 대륙에서는 ePrivacy와 GDPR(EU 개인정보보호규정)의 규제가 강화되어 옵토인율이 변동 요인이 되고 있습니다. 페더레이티드 학습을 시도하는 공급업체는 정확성과 익명성을 조화시켜 나중에 다른 지역으로 수출되는 모범 사례를 만들 가능성을 기대합니다. 따라서 유럽의 자동 컨텐츠 인식 시장 전망은 수익화에 필수적인 데이터 풍부한 워크플로우를 유지하면서 업계가 규제 당국과 협력할 수 있는지 여부에 달려 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- ACR 칩 내장 스마트 TV의 보급

- 어드레서블 TV 광고 예산 확대

- ACR을 자동차 인포테인먼트 시스템에 통합

- FAST(무료 광고 포함 스트리밍 TV) 채널 성장

- 엣지 AI의 최적화에 의해 디바이스 상 ACR의 소비 전력 저하

- 프라이버시를 보호하는 새로운 연합 학습 모델

- 시장 성장 억제요인

- e프라이버시법 개정으로 옵트인 동의 룰이 엄격화

- 애플 및 구글, OS 업데이트로 지문 압박 방지의 움직임

- 종래의 선형 STB로부터의 한정된 SKU 레벨의 분석

- 워터마크 IP 포트폴리오를 둘러싼 로열티 분쟁

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 소프트웨어

- 서비스

- 기술별

- 오디오, 비디오 및 핑거 프린팅

- 전자 워터마크

- 음성 인식

- 광학식 문자 인식

- 솔루션별

- 실시간 컨텐츠 분석

- 보안 및 저작권 관리

- 음성 및 스피치 인터페이스

- 데이터 관리 및 메타데이터

- 기타

- 최종 사용자 업계별

- 미디어 및 엔터테인먼트

- 소비자 일렉트로닉스 OEM

- 광고 및 마케팅

- 통신 및 IT

- 자동차

- 헬스케어

- 기타(소매, 교육)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 아르헨티나

- 브라질

- 기타 남미

- 유럽

- 영국

- 프랑스

- 독일

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 나이지리아

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Apple Inc.(Shazam)

- Audible Magic Corp.

- ACRCloud

- Digimarc Corp.

- Vobile Group Ltd.

- Nuance Communications Inc.

- Kantar Media SAS

- Signalogic Inc.

- VoiceInteraction SA

- Beatgrid BV

- Gracenote(Nielsen)

- SoundHound AI Inc.

- Clarivate(ComScore ACR)

- Yospace Ltd.

- Alphonso(Verizon Media)

- Sorenson Media

- Enswers Inc.

- Intrasonics Ltd.

- Audible Insights LLC

- Civolution BV

제7장 시장 기회 및 향후 전망

AJY 25.11.24The Automatic Content Recognition market stood at USD 4.43 billion in 2025 and is on course to touch USD 12.80 billion by 2030, translating into a brisk 23.65% CAGR.

The 2025 baseline reflects broad-based adoption of smart TVs, a decisive budget shift toward addressable advertising, and steady improvements in edge AI that allow fingerprinting tasks to run locally with minimal energy draw. Milestone deployments such as Apple's Shazam logging 100 billion cumulative song recognitions in 2024 showcase the scale now achieved in everyday consumer settings. Device makers routinely embed ACR silicon at the board level, enabling continuous signature extraction from linear broadcasts, streaming apps, and HDMI inputs without user intervention. This hardware pivot enlarges the Automatic Content Recognition market addressable data pool while lowering latency, a combination that keeps advertisers, broadcasters, and analytics providers firmly invested in the technology.

Key data points confirm this momentum. Software still accounts for 64% revenue but managed cloud services are expanding at a 24.48% pace as brands outsource compliance and model tuning. Audio and video fingerprinting remains the leading technology with 46% share, yet speech-driven use cases in cars and healthcare are widening fastest at 24.11% CAGR. Security and copyright protection dominate solution spending with 29% share, although real-time analytics for FAST channels is the quickest riser at 23.89% CAGR. End-user mix is led by media and entertainment at 38%, while automotive infotainment is closing the gap at 23.78% CAGR thanks to voice commerce pilots. Regionally, North America commands 41% value share, whereas Asia Pacific is compounding at 24.63% through 2030-together reinforcing the Automatic Content Recognition market's vitality across both mature and emerging geographies.

Global Automatic Content Recognition Market Trends and Insights

Proliferation of Smart TVs with Embedded ACR Chips

Smart-TV brands now route ACR processing through system-on-chip blocks situated beneath the application layer, allowing continuous fingerprint capture even when privacy toggles are off. Samsung units dispatch signatures roughly every minute, while LG models do so every 15 seconds, creating an uninterrupted telemetry stream that spans live broadcasts, streaming apps, and any HDMI source. These low-latency pipelines shorten the feedback loop for ad optimization and broaden the Automatic Content Recognition market's data inventory.

Expansion of Addressable-TV Advertising Budgets

Advertisers are redirecting spend toward addressable formats that exploit frame-level ACR insights. Budgets dedicated to addressable TV surpassed one-third of total TV outlays in 2025 and are on track for 42% by 2027. FAST distributors pair these insights with programmatic workflows to lift engagement beyond demographic targeting, while new HbbTV-TA certifications in Europe standardize technical baselines. The Automatic Content Recognition market benefits as every incremental ad insertion relies on precise, real-time content labeling.

Stricter Opt-in Consent Rules Under Refreshed ePrivacy Law

European authorities began enforcing refined consent banners and "consent-or-pay" guidance in late 2024, pressuring smart-TV vendors to create granular toggles that isolate ACR data from core functions. Compliance adds engineering overhead and may shrink data volumes, dampening the Automatic Content Recognition market growth outlook within the bloc.

Other drivers and restraints analyzed in the detailed report include:

- Integration of ACR into Automotive Infotainment Systems

- Growth of FAST (Free Ad-Supported Streaming TV) Channels

- Apple/Google Anti-Fingerprinting Moves in OS Updates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software revenue formed the lion's share of the Automatic Content Recognition market size in 2024, thanks to code tightly woven into TV operating systems and streaming SDKs. However, cloud-hosted managed offerings are scaling at 24.48% CAGR as OEMs and broadcasters outsource model tuning, compliance, and uptime management. Digimarc's 44% jump in annual recurring revenue to USD 23.9 million underlines how subscription billing is resonating with customers who prefer turnkey compliance amid changing privacy rules.

The services surge mirrors a broader pivot in enterprise IT toward OPEX-friendly contracts that bundle maintenance, audit logs, and SLA guarantees, for many mid-tier device brands, licensing an end-to-end service beats building an in-house stack that must keep pace with region-specific consent frameworks. Accordingly, analysts expect services to nibble incremental Automatic Content Recognition market share each year through 2030 while software remains foundational yet slower growing.

Audio and video fingerprinting still anchors 46% of revenue due to its maturity and proven accuracy across live TV and on-demand libraries. Yet speech-centric recognition is the Automatic Content Recognition market's quickest riser, compounding at 24.11% on the back of in-car voice assistants, tele-health monitoring, and contact-center analytics. NTT's ultra-low-latency voice conversion work highlights how real-time quality now meets enterprise thresholds.

Edge silicon capable of shaving 92% power relative to cloud chains makes voice analytics feasible in battery-run devices and automotive ECUs. Meanwhile, watermarking gains renewed importance for rights holders, and optical character recognition adds incremental volume in retail. Together, these trajectories diversify the Automatic Content Recognition industry toolkit without displacing staple fingerprinting algorithms.

The Automatic Content Recognition Market Report is Segmented by Component (Software and Services), Technology (Audio and Video Fingerprinting, Digital Watermarking, and More), Solution (Real-Time Content Analytics, Voice and Speech Interfaces, and More), End-User Industry (Media and Entertainment, Consumer Electronics OEMs, Telecom and IT, and More), and Geography.

Geography Analysis

North America generated 41% of Automatic Content Recognition market revenue in 2024, benefiting from smart-TV household penetration above 75% and a well-established addressable-advertising supply chain. Platforms integrate server-side insertion that leans heavily on frame-level recognition, amplifying the region's data advantages. While federal privacy bills remain in draft form, state-level rules and greater consumer awareness could temper data flows mid-term, prompting vendors to reinforce consent flows.

Asia Pacific is the automatic growth engine, expanding at 24.63% CAGR through 2030. Mass-market smart-TV adoption, rising disposable incomes, and policy backing for AI labs act in concert. Korea's SK Telecom and LG CNS are adding multilingual real-time translation layers that rely on the same underlying ACR voices. Japan's AI Bill, now progressing through the Diet, is poised to set balanced R&D guardrails, giving suppliers regulatory clarity. In China, domestic chip fabrication and algorithm houses spur localized stacks even as international players navigate export hurdles. The cumulative effect keeps the Automatic Content Recognition market vibrant across APAC sub-regions.

Europe offers a mix of opportunity and constraint. HbbTV-TA certification has harmonized technical pathways for ad replacement, but the continent's reinforced ePrivacy and GDPR regimes make opt-in rates a swing factor. Vendors experimenting with federated learning expect to reconcile accuracy with anonymity, potentially birthing best practices that later export to other territories. The Automatic Content Recognition market outlook in Europe therefore hinges on the industry's ability to align with regulators while sustaining data-rich workflows critical for monetization.

- Apple Inc. (Shazam)

- Audible Magic Corp.

- ACRCloud

- Digimarc Corp.

- Vobile Group Ltd.

- Nuance Communications Inc.

- Kantar Media SAS

- Signalogic Inc.

- VoiceInteraction SA

- Beatgrid BV

- Gracenote (Nielsen)

- SoundHound AI Inc.

- Clarivate (ComScore ACR)

- Yospace Ltd.

- Alphonso (Verizon Media)

- Sorenson Media

- Enswers Inc.

- Intrasonics Ltd.

- Audible Insights LLC

- Civolution BV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Smart TVs with embedded ACR chips

- 4.2.2 Expansion of addressable-TV advertising budgets

- 4.2.3 Integration of ACR into automotive infotainment systems

- 4.2.4 Growth of FAST (Free Ad-Supported Streaming TV) channels

- 4.2.5 Edge AI optimisation lowering on-device ACR power draw

- 4.2.6 Emerging privacy-preserving federated learning models

- 4.3 Market Restraints

- 4.3.1 Stricter opt-in consent rules under refreshed ePrivacy law

- 4.3.2 Apple/Google anti-fingerprinting moves in OS updates

- 4.3.3 Limited SKU-level analytics from legacy linear STBs

- 4.3.4 Royalty disputes over watermark IP portfolios

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Technology

- 5.2.1 Audio and Video Fingerprinting

- 5.2.2 Digital Watermarking

- 5.2.3 Speech and Voice Recognition

- 5.2.4 Optical Character Recognition

- 5.3 By Solution

- 5.3.1 Real-time Content Analytics

- 5.3.2 Security and Copyright Management

- 5.3.3 Voice and Speech Interfaces

- 5.3.4 Data Management and Metadata

- 5.3.5 Others

- 5.4 By End-User Industry

- 5.4.1 Media and Entertainment

- 5.4.2 Consumer Electronics OEMs

- 5.4.3 Advertising and Marketing

- 5.4.4 Telecom and IT

- 5.4.5 Automotive

- 5.4.6 Healthcare

- 5.4.7 Others (Retail, Education)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Argentina

- 5.5.2.2 Brazil

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 France

- 5.5.3.3 Germany

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 Nigeria

- 5.5.6.2 South Africa

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Apple Inc. (Shazam)

- 6.4.2 Audible Magic Corp.

- 6.4.3 ACRCloud

- 6.4.4 Digimarc Corp.

- 6.4.5 Vobile Group Ltd.

- 6.4.6 Nuance Communications Inc.

- 6.4.7 Kantar Media SAS

- 6.4.8 Signalogic Inc.

- 6.4.9 VoiceInteraction SA

- 6.4.10 Beatgrid BV

- 6.4.11 Gracenote (Nielsen)

- 6.4.12 SoundHound AI Inc.

- 6.4.13 Clarivate (ComScore ACR)

- 6.4.14 Yospace Ltd.

- 6.4.15 Alphonso (Verizon Media)

- 6.4.16 Sorenson Media

- 6.4.17 Enswers Inc.

- 6.4.18 Intrasonics Ltd.

- 6.4.19 Audible Insights LLC

- 6.4.20 Civolution BV

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment