|

시장보고서

상품코드

1851647

클라우드 모니터링 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cloud Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

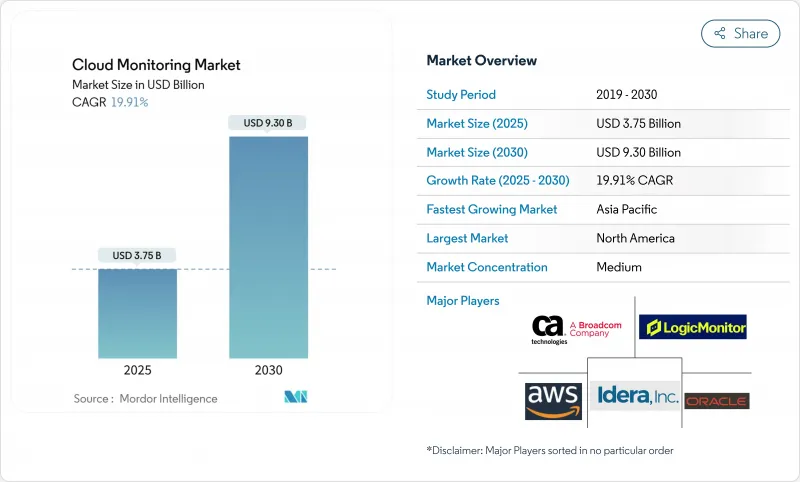

클라우드 모니터링 시장 규모는 2025년에 37억 5,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 19.91%로 성장할 전망이며, 2030년에는 93억 달러에 달할 것으로 예측됩니다.

가속화된 멀티클라우드 채택, AI 워크로드 시각화, FinOps 어카운터빌리티, 데이터 주권에 대한 의무화가 벤더의 로드맵을 재구성하고 있습니다. 엔터프라이즈는 로그, 메트릭, 추적, 사용자 경험 및 비용 신호를 실시간으로 통합하는 통합 플랫폼에서 포인트 모니터링 도구를 대체하려고 합니다. OpenTelemetry의 신속한 표준화는 통합 마찰을 줄이고, AI 구동의 이상 감지는 해결까지의 평균 시간을 단축합니다. 지출은 순수한 인프라 지표에서 기술적 건전성을 수익 영향에 연결하는 풀 스택 인텔리전스로 이동합니다. 하이퍼스케일 클라우드가 네이티브 툴을 통합하면서도 하이브리드 에스테이트에 대응하기 위해 독립 벤더와 제휴하고 있기 때문에 경쟁의 격렬함은 완만하게 남아 있습니다.

세계의 클라우드 모니터링 시장 동향 및 인사이트

가속화된 멀티클라우드 및 하이브리드 클라우드 채택

멀티클라우드 이용이 전환점을 넘어 2024년에는 금융 서비스 기업의 43%가 이미 2개 이상의 하이퍼스케일러에 워크로드를 분산하고 있습니다. 각 공급자는 자신의 지표를 내보내기 때문에 운영 팀은 원격 측정 난립과 맹점에 직면합니다. 따라서 AWS, Azure, Google Cloud 데이터를 정규화하는 통합 플랫폼이 단일 클라우드 모니터를 대체합니다. OpenTelemetry 에이전트의 채택이 급증한 것은 벤더 중립 계측기가 전체 에스테이트의 커버리지를 용이하게 하기 때문입니다. 조직은 또한 동일한 트랜잭션이 온프레미스 및 클라우드 노드에 걸쳐 있는 경우 상관성 있는 비용, 성능 및 규정 준수 뷰가 필요합니다. 이러한 압력으로 인해 하이브리드 클라우드 관측 가능성은 옵션에서 필수적인 기능으로 승격되고 클라우드 관측 가능성 시장은 더 깊은 엔드 투 엔드 컨텍스트로 향하고 있습니다.

DevOps/SRE 문화 및 실시간 관측 가능성

사이트 신뢰성 엔지니어링은 대기업에서 주류가 되어 시간당 100만 달러를 초과하는 평균 정지 비용을 줄입니다. 팀은 현재 CI/CD 파이프라인에 골든 시그널 및 서비스 레벨 목표를 통합하여 프로덕션 롤아웃 전에 결함이 표면화되도록 하고 있습니다. 풀 스택 인사이트는 사일로화된 툴체인에 비해 다운타임을 79% 절감했습니다. AI에 의한 비정상 감지는 로그와 추적으로부터 인시던트의 전조를 발견하고 인간을 확장합니다. 피드백 루프를 가속화하면 개발자의 생산성이 향상되고 옵저베이러빌리티는 직접적인 비즈니스 실현으로 이어집니다. 따라서 클라우드 관측 가능성 시장은 전통적인 IT 운영이 아닌 엔지니어링 팀으로 예산을 전환함으로써 혜택을 누릴 수 있습니다.

컨테이너화된 서버리스 스택의 제한된 가시성

컨테이너는 몇 초밖에 실행되지 않고 서버리스 기능은 에이전트 없이 스핀업하므로 레거시 모니터에서 채워지지 않는 틈이 남습니다. Kubernetes는 토런트 레벨 메타데이터를 추가하기 때문에 무차별 콜렉션은 스토리지 비용을 증가시킵니다. eBPF 기반의 낮은 오버헤드 인스트루먼테이션과 결합된 마이크로서비스 간의 요청 경로를 연결하는 분산 트레이스가 구제책으로 부상하고 있습니다. OpenTelemetry는 매우 중요하지만, 아직 도입이 복잡하고 자원에 제약이 있는 중소기업에서의 채용이 지연되고 있는 이유가 되고 있습니다. 턴키 계측이 성숙하기 전까지는 임시 환경에서의 관측 가능성의 격차가 클라우드 관측 가능성 시장의 CAGR의 발을 잡아 당길 것으로 보입니다.

부문 분석

SaaS 플랫폼은 2024년 매출의 48%를 차지하였고, 인프라 오버헤드를 제거하는 턴키 배포에 대한 수요를 뒷받침합니다. PaaS 솔루션은 가장 빠른 레인을 형성하여 CAGR 29.90% 성장했습니다. 수집가를 관리하지 않고도 더 깊은 코드 수준의 인사이트를 사용자가 갈망하기 때문입니다. IaaS 도구는 규제 대상 데이터 근처에 온프레미스 콜렉터가 필요한 하이브리드 시설에 대한 관련성을 유지합니다. SaaS의 클라우드 관측 가능성 시장 규모는 늦은 산업이 매니지드 서비스로 전환함에 따라, 2025-2030년 27억 달러가 확대될 것으로 예측됩니다.

PaaS의 기세는 플랫폼 엔지니어링 팀이 내부 개발자 포털에 관측 가능성을 통합하고 있음을 반영합니다. 주요 하이테크 벤더는 추적, 혼돈 테스트 및 KPI 대시보드를 빌드 파이프라인에 직접 통합하여 인지 부하를 줄입니다. OpenTelemetry의 자동 측정과 결합하여 이 시너지 효과는 가치 실현까지의 시간을 가속화합니다. 그 결과 클라우드 관측 가능성 시장은 AI 모델의 관측 가능성 및 비용 분석을 목표로 하는 PaaS 계약에 따른 순 신규 부킹의 거의 1/3을 기록하고 있습니다.

솔루션 스위트는 데이터 레이크, 상관 엔진 및 UX 애널리틱스를 다루며 2024년 매출의 62%를 차지했습니다. 서비스 컨설팅, 온보딩, 매니지드 옵서버빌리티는 기업이 옵서버빌리티 엔지니어 고용에 고전하는 가운데 CAGR 19.30%로 성장이 전망됩니다. 통합자 수요는 측정을 제어 프레임워크에 맞추어야 하는 규제 대상 수직 시장에서 가장 높습니다.

현재 공급업체의 로드맵에는 권고 시간, 공인 교육 및 가치 증명주기를 단축하는 빠른 시작 팩이 번들로 제공됩니다. LogicMonitor의 8억 달러의 자금 조달은 서비스 확장을 위한 것이며 전문 지식이 얼마나 중요한 해자가 되는지를 보여줍니다. 프레임워크가 진화함에 따라, 경상적인 서비스 계약은 클라우드 관측 가능성 시장 전체의 수익의 대부분을 차지하게 되어 파트너 생태계가 심화됩니다.

클라우드 모니터링 시장 보고서는 클라우드 서비스 모델별(IaaS, Saas, Paas), 컴포넌트별(솔루션 및 서비스), 전개 모드별(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 및 멀티클라우드), 조직 규모별(중소기업 및 대기업), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 소매, 전자상거래, IT 및 통신, 헬스케어 및 생명과학, 정부 및 공공기관, 제조업, 기타), 지역별로 분류되고 있습니다.

지역 분석

북미는 2024년 매출의 41%를 차지했으며, 수십년에 걸친 DevOps의 성숙과 AI에 대한 중점 투자를 반영하고 있습니다. 금융기관은 연간 1,044만 달러의 장애 손실의 중앙값을 들고 있으며, 프리미엄 도구의 정당성을 보여줍니다. 소블린 클라우드의 화제는 겸손하지만 개인정보보호법은 여전히 데이터 레지던시 기능을 뒷받침하고 있습니다. 2027년 이후 임베디드 사이클이 포화됨에 따라 성장은 10%대 전반에 둔화되지만 AI 관측 가능성 업그레이드는 라이선스 확대를 유지합니다.

아시아태평양은 클라우드 퍼스트 신흥 기업과 정부의 디지털화 추진에 힘입어 CAGR 21.30%에서 가장 빠르게 성장하고 있습니다. 인도의 퍼블릭 클라우드 투자는 2028년까지 255억 달러에 달할 가능성이 있습니다. 싱가포르와 인도네시아에서는 Observability의 ROI가 114%를 넘어 다운타임 삭감으로 인한 높은 보상을 나타냅니다. 알리바바 클라우드가 43%의 점유율을 가진 중국의 6조 1,920억 위안 클라우드 부문은 현지어 대시보드와 국내 데이터 레이크를 홍보합니다.

GDPR(EU 개인정보보호규정)과 향후 AI법이 데이터 보호 요구를 강화하는 가운데 유럽의 CAGR은 10%대 중반을 기록했습니다. Accenture에 따르면 소블린 클라우드에 투자하는 기업은 37%로 44%가 2년 이내에 추가 투자를 계획하고 있다고 합니다. 벤더는 지역의 호스트와 제휴해 EU역내의 로깅 파이프라인을 확보했습니다. 에너지 대시보드는 기후 변화 보고서가 실적 지표와 융합됨에 따라 인기를 얻고 있습니다. 이러한 지역적 뉘앙스의 차이로 인해 클라우드 관측 가능성 시장은 컴플라이언스를 의식한 다양한 전개로 향하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 가속하는 멀티 클라우드 및 하이브리드 클라우드의 도입

- DevOps/SRE 문화 및 실시간 관측성의 필요성

- GPU 레벨의 감시를 필요로 하는 AI/ML 워크로드의 폭발적 증가

- FinOps의 책임 및 비용 대 가치 최적화 압력

- 클라우드 카본 보고서를 위한 지속가능성 대시보드

- 소블린 클라우드 및 데이터 현지화의 의무화

- 시장 성장 억제요인

- 컨테이너화, 서버리스 스택의 가시성은 한정적

- 풀 스택 관측 가능 플랫폼의 TCO 상승

- 관측 가능성 공학의 스킬 및 갭

- Hyperscaler의 API 속도 제한에 의한 딥 텔레메트리의 스로틀링

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 클라우드 서비스 모델별

- IaaS

- PaaS

- SaaS

- 컴포넌트별

- 솔루션

- 서비스

- 전개 모드별

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 및 멀티클라우드

- 기업 규모별

- 중소기업

- 대기업

- 최종 사용자 업계별

- BFSI

- 소매 및 전자상거래

- IT 및 통신

- 헬스케어 및 생명과학

- 정부 및 공공 부문

- 제조업

- 기타(미디어, 에너지, 교육)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AWS

- Microsoft

- Google Cloud

- IBM

- Oracle

- Datadog

- Dynatrace

- New Relic

- Broadcom(CA Tech/AppDynamics)

- LogicMonitor

- Splunk

- SolarWinds

- PagerDuty

- Cisco ThousandEyes

- Grafana Labs

- Elastic

- Zenoss

- ScienceLogic

- Idera

제7장 시장 기회 및 향후 전망

AJY 25.11.24The Cloud Monitoring Market size is estimated at USD 3.75 billion in 2025, and is expected to reach USD 9.30 billion by 2030, at a CAGR of 19.91% during the forecast period (2025-2030).

Accelerated multi-cloud adoption, AI workload visibility, FinOps accountability, and data-sovereignty mandates are reshaping vendor roadmaps. Enterprises are replacing point monitoring tools with unified platforms that ingest logs, metrics, traces, user experience, and cost signals in real time. OpenTelemetry's rapid standardization is lowering integration friction, while AI-driven anomaly detection shortens the mean time to resolution. Spending is shifting from pure infrastructure metrics toward full-stack intelligence that ties technical health to revenue impact. Competitive intensity remains moderate as hyperscale clouds embed native tooling, yet still partner with independent vendors to address hybrid estates.

Global Cloud Monitoring Market Trends and Insights

Accelerated Multi-Cloud and Hybrid-Cloud Adoption

Multi-cloud usage crossed a tipping point, with 43% of financial-services firms already distributing workloads across two or more hyperscalers in 2024. Each provider exports unique metrics, so operations teams face telemetry sprawl and blind spots. Unified platforms that normalise data across AWS, Azure, and Google Cloud are therefore replacing single-cloud monitors. Adoption of OpenTelemetry agents rose sharply because vendor-neutral instrumentation eases estate-wide coverage. Organisations also need correlated cost, performance, and compliance views when the same transaction spans on-premises and cloud nodes. These pressures elevate hybrid-cloud observability from optional to indispensable capability, pushing the cloud observability market toward deeper end-to-end context.

DevOps/SRE Culture and Real-Time Observability

Site Reliability Engineering is mainstreamed in large enterprises, cutting mean outage costs that exceed USD 1 million per hour. Teams now embed golden signals and service-level objectives into CI/CD pipelines so that defects surface before production rollouts. Full-stack insight lowers downtime by 79% versus siloed toolchains. AI-driven anomaly detection augments humans by surfacing precursors to incidents across logs and traces. Faster feedback loops also boost developer productivity, turning observability into a direct business enabler. The cloud observability market, therefore, benefits from budgets shifting left toward engineering teams rather than traditional IT operations.

Limited Visibility in Containerised, Serverless Stacks

Containers may live for seconds, while serverless functions spin up without agents, leaving gaps that legacy monitors cannot fill. Kubernetes adds torrent-level metadata, so brute-force collection inflates storage bills. Distributed tracing that stitches request paths across microservices, combined with eBPF-based low-overhead instrumentation, is emerging as the remedy. OpenTelemetry is pivotal yet still complex to deploy, explaining slower adoption among resource-constrained SMEs. Until turnkey instrumentation matures, observability gaps in ephemeral environments will drag on the cloud observability market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- AI/ML Workload Explosion Requiring GPU-Level Monitoring

- FinOps Accountability and Cost-to-Value Optimisation Pressure

- Rising TCO of Full-Stack Observability Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SaaS platforms anchored 48% of 2024 revenue, underscoring demand for turnkey deployments that remove infrastructure overhead. PaaS solutions shape the fastest lane, growing 29.90% CAGR as users crave deeper code-level insight without managing collectors. IaaS tools retain relevance for hybrid estates that need on-premises collectors close to regulated data. The cloud observability market size for SaaS is forecast to widen by USD 2.7 billion between 2025 and 2030 as lagging industries migrate to managed services.

PaaS momentum reflects platform-engineering teams embedding observability into internal developer portals. Big-tech vendors integrate tracing, chaos testing, and KPI dashboards directly into build pipelines, reducing cognitive load. Combined with OpenTelemetry auto-instrumentation, this synergy accelerates time to value. Consequently, the cloud observability market records almost one-third of net-new bookings from PaaS deals targeting AI model observability and cost analytics.

Solution suites captured 62% revenue in 2024, covering data lakes, correlation engines, and UX analytics. Services consulting, onboarding, and managed observability grow 19.30% CAGR as enterprises struggle to hire observability engineers. Integrator demand is highest in regulated verticals where instrumentation must map to control frameworks.

Vendor roadmaps now bundle advisory hours, certified training, and quick-start packs that shorten proof-of-value cycles. LogicMonitor's USD 800 million funding earmarked for services expansion signals how professional expertise becomes a key moat. As frameworks evolve, recurring service contracts will comprise a larger slice of the overall cloud observability market revenue, deepening partner ecosystems.

The Cloud Monitoring Market Report is Segmented by Cloud Service Model (IaaS, Saas, Paas), Component (Solution and Services), Deployment Mode (Public Cloud, Private Cloud, and Hybrid/Multi-Cloud), Organization Size (SMEs and Large Enterprises), End-User Industry (BFSI, Retail and E-Commerce, IT and Telecommunications, Healthcare and Life Sciences, Government and Public Sector, Manufacturing, and Others), and Geography.

Geography Analysis

North America commanded 41% of 2024 revenue, reflecting decades-long DevOps maturity and heavy AI investment. Financial institutions cite median outage losses of USD 10.44 million per year, justifying premium tooling. Sovereign-cloud talk is muted, yet privacy laws still nudge data residency features. Growth moderates to low teens after 2027 as replacement cycles saturate, but AI observability upgrades sustain license expansion.

Asia Pacific is the fastest mover at 21.30% CAGR, propelled by cloud-first start-ups and government digital drives. India's public cloud outlay could reach USD 25.5 billion by 2028. Observability ROI tops 114% in Singapore and Indonesia, showcasing high payoff for downtime reduction. China's 6.192 trillion-yuan cloud sector, led by Alibaba Cloud's 43% hold, fuels local-language dashboards and in-country data lakes.

Europe records mid-teens CAGR as GDPR and upcoming AI Act cement data-protection demands. Accenture notes 37% of enterprises investing in sovereign cloud, with 44% planning more within two years. Vendors partner with regional hosts to ensure EU-located logging pipelines. Energy dashboards gain traction as climate reporting merges with performance metrics. These regional nuances collectively propel the cloud observability market toward diverse compliance-aware deployments.

- AWS

- Microsoft

- Google Cloud

- IBM

- Oracle

- Datadog

- Dynatrace

- New Relic

- Broadcom (CA Tech/AppDynamics)

- LogicMonitor

- Splunk

- SolarWinds

- PagerDuty

- Cisco ThousandEyes

- Grafana Labs

- Elastic

- Zenoss

- ScienceLogic

- Idera

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated multi-cloud and hybrid-cloud adoption

- 4.2.2 DevOps/SRE culture and need for real-time observability

- 4.2.3 AI/ML workload explosion requiring GPU-level monitoring

- 4.2.4 FinOps accountability and cost-to-value optimisation pressure

- 4.2.5 Sustainability dashboards for cloud-carbon reporting

- 4.2.6 Sovereign-cloud and data-localisation mandates

- 4.3 Market Restraints

- 4.3.1 Limited visibility in containerised, serverless stacks

- 4.3.2 Rising TCO of full-stack observability platforms

- 4.3.3 Skills gap for observability engineering

- 4.3.4 Hyperscaler API-rate limits throttling deep telemetry

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry Intensity

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cloud Service Model

- 5.1.1 IaaS

- 5.1.2 PaaS

- 5.1.3 SaaS

- 5.2 By Component

- 5.2.1 Solution

- 5.2.2 Services

- 5.3 By Deployment Mode

- 5.3.1 Public Cloud

- 5.3.2 Private Cloud

- 5.3.3 Hybrid/Multi-Cloud

- 5.4 By Organisation Size

- 5.4.1 SMEs

- 5.4.2 Large Enterprises

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Retail and e-Commerce

- 5.5.3 IT and Telecommunications

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Government and Public Sector

- 5.5.6 Manufacturing

- 5.5.7 Others (Media, Energy, Education)

- 5.6 By Region

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AWS

- 6.4.2 Microsoft

- 6.4.3 Google Cloud

- 6.4.4 IBM

- 6.4.5 Oracle

- 6.4.6 Datadog

- 6.4.7 Dynatrace

- 6.4.8 New Relic

- 6.4.9 Broadcom (CA Tech/AppDynamics)

- 6.4.10 LogicMonitor

- 6.4.11 Splunk

- 6.4.12 SolarWinds

- 6.4.13 PagerDuty

- 6.4.14 Cisco ThousandEyes

- 6.4.15 Grafana Labs

- 6.4.16 Elastic

- 6.4.17 Zenoss

- 6.4.18 ScienceLogic

- 6.4.19 Idera

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment