|

시장보고서

상품코드

1851664

펌프 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

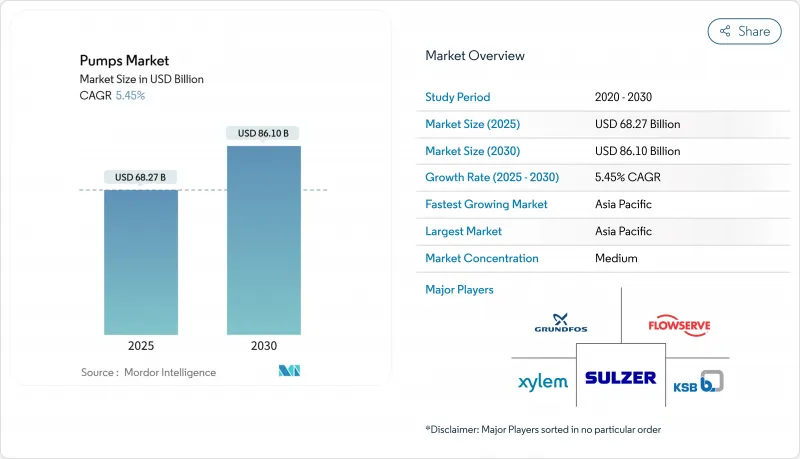

펌프 시장 규모는 2025년에 682억 7,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.45%로 성장할 전망이며, 2030년에는 861억 달러에 이를 것으로 예측됩니다.

성장을 지원하는 것은 대규모 물 인프라 업그레이드, 견조한 산업 설비 투자, 에너지 효율적인 장비를 요구하는 보편적인 움직임입니다. 전력 공급원은 여전히 전기가 주류이지만, 태양광 발전 시스템은 농업 및 오프 그리드 환경에서 급성장하고 있습니다. 기술 사양은 에너지 소비를 억제하고, 예지 보전을 가능하게 하며, 환경 규제의 강화에 대응하는 스마트하고 센서가 풍부한 펌프로 시프트하고 있습니다. 기존 공급업체가 인수를 통해 포트폴리오를 확대하고 아시아의 저비용 진출기업이 가격 및 납품 속도로 경쟁하기 때문에 경쟁의 치열성이 증가하고 있습니다. 공급망 전략은 원재료 가격 변동에 대항하기 위해 원재료 절약과 다지역 조달에 중점을 두는 경향이 커지고 있습니다.

세계의 펌프 시장 동향 및 인사이트

중동, 아프리카 및 아시아태평양의 해수 담수화 프로젝트에서 설비 투자 증가

사우디아라비아 및 아랍에미리트(UAE)의 해수 담수화 프로젝트는 2024년에 48억 달러를 넘어 스테인리스 동등품보다 40% 오래 지속되는 세라믹 복합 접액부를 갖춘 고압 펌프 수요에 박차를 가하고 있습니다. 에너지 회수 장치는 현재 새로운 플랜트에서 표준화되어 운전 비용을 최대 60% 절감하고 입증된 해양 등급 재료에 대한 전문 지식을 갖춘 공급업체에게 유리한 기술적 장벽을 향상시키고 있습니다. 해수 담수화에 대한 참조를 가진 제조업체는 경쟁사가 유사한 신용을 확보하려고 경쟁하면서 프리미엄 가격을 활용합니다.

유럽 및 북미에서 엄격한 폐수 재사용 의무화

개정 EU 도시 폐수 처리 지령은 인과 PFAS의 대폭 삭감을 목표로 하고 있으며, 고도 산화 및 막 여과를 지원하는 정밀 주입과 가변 유량 순환 펌프의 채용이 가속화되고 있습니다. 지자체는 통합 펌프 패키지에 많은 예산을 할당하여 평균 주문 금액을 27% 늘리고 있습니다. 유틸리티 기업이 성과 기반 조달로 이동하는 동안 제어 및 원격 모니터링 기능을 제공하는 공급업체가 낙찰됩니다.

니켈과 스테인레스 스틸 가격 변동이 BoM 팽창 초래

펌프 제조업체에 의하면, 용적식 펌프에는 스테인리스 스틸이 30-40% 사용되고 있기 때문에 가격 상승이 이폭을 압박하고 있습니다. 유럽의 주요 브랜드는 현재 계산 유체 역학을 이용하여 특정 모델에서 합금의 무게를 15% 줄이고 여러 지역의 조달을 통해 노출을 헤지하고 있습니다.

부문 분석

원심 펌프는 2024년 펌프 시장 점유율의 56.8%를 차지했습니다. 임펠러 형상 및 가이드 블레이드 프로파일의 지속적인 개선으로 유압 효율이 최대 15% 향상되었습니다. 이 부문의 CAGR은 6.2%로 펌프 시장 전체를 웃도는 것으로 예측되고 있습니다. 급수, HVAC 및 정유소 서비스에서 광범위한 사용이 안정적인 기반을 제공하는 반면, 신흥 탄소 포획 플랜트는 고급 씰과 내식성 합금을 갖춘 CO2 처리 모델을 사용자 정의해야 합니다.

특수화된 원심형은 액체 및 초임계 CO2가 복잡한 열역학적 거동을 나타내는 탄소 포집 및 저류(CCS) 회로에 진입하고 있습니다. 센서 어레이를 통합한 공급업체는 운영자가 에너지 소비 및 유지 보수 비용을 절감하고 최상의 효율 포인트에 가까운 운전을 가능하게 합니다. 체적식 설계는 계량, 화학약품 주입, 고압 슬러리 업무에 필수적이며, 이러한 틈새 분야에서 성능 공차가 엄격해져 가격이 비쌉니다.

수평 기계는 친숙하고 유지 보수가 쉽고 초기 비용이 낮기 때문에 여전히 펌프 시장 점유율의 60%를 차지합니다. 그러나 도시의 공공시설과 데이터센터 건설업자가 바닥 면적 제약에 직면하고 있기 때문에 수직 인라인형과 수중형은 CAGR 5.8%로 성장할 것으로 보입니다. ABB는 오로라 모터스(Aurora Motors) 인수를 앞두고 있으며, 종형 모터 라인업을 강화하고 공급업체가 장기 성장을 확신하고 있음을 보여줍니다.

수직 펌프는 깊은 우물의 급수, 광산의 탈수, 폐수의 습식 우물의 설치와 같은 드라이버가 유체 위에 남아있는 용도로 성장합니다. 업그레이드된 베어링 시스템과 내마모성 코팅으로 인상 간격을 늘릴 수 있습니다. 이 부문 수요는 컴팩트한 플랜트 룸과 적층된 기계 공간이 선호되는 보다 엄격한 건축 기준법에서도 혜택을 누리고 있습니다.

펌프 시장 보고서는 펌프 유형별(원심, 용적, 기타), 샤프트 방향별(수평, 수직), 구동력별(전기 구동, 엔진 구동, 공압 구동, 태양전지 구동), 최종 사용자별(물 및 폐수 유틸리티, 화학 및 석유 화학, 발전, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 구분되어 있습니다.

지역 분석

아시아태평양은 2024년에 51.60%의 점유율을 획득하여 펌프 시장을 선도하였고, 2030년까지 CAGR 6.0%로 성장할 것으로 예측됩니다. 대규모 도시화, 야심찬 해수 담수화 파이프라인, 강력한 농업 현대화가 성장을 지원합니다. 중국 히트펌프 국가 로드맵과 인도의 태양광 펌프 전개는 대량 수요를 유지합니다. 지역 제조업체는 밸류체인을 센서 대응 유닛으로 끌어 올려 지역 경쟁을 격화시키고 있습니다.

북미는 여전히 기술 혁신 주도형입니다. 2024년도에는 납 급수관 교환을 위해 30억 달러의 연방수 인프라 자금이 투입되어 고급 식수기의 수주가 활성화됩니다. 미국 걸프에서의 셰일 개발이 10,000psi의 프랙처링 장치(펌프) 수요를 밀어 올리는 한편, 캐나다의 광산업자는 내구성이 높은 슬러리 장치를 조달했습니다. 2024년에는 열 펌프가 가스로를 27% 상회하였고, 전기가 펌프 선택에 파급되는 것이 부각되었습니다.

유럽은 라이프사이클 효율과 환경 컴플라이언스를 중시합니다. EU의 폐수 지침이 업데이트되어 정밀 주입과 멤브레인 피드 펌프에 큰 시장이 탄생합니다. 북유럽 난방 네트워크는 급속히 확대되고, 저온 운전에 대응하는 대형 순환 펌프가 필요합니다. 독일과 영국의 유틸리티 사업자는 자산의 가동률을 높이고 교환 간격을 연장하기 위해 예지 보전 소프트웨어를 도입하고 있습니다. 중동에서는 해수 담수화와 지역 냉방에 많은 투자가 이루어지고 있습니다. 한편, 아프리카의 많은 국가에서는 농작물의 수확량을 늘리고 디젤 연료에 대한 의존성을 줄이기 위해 오프 그리드 태양 광 관개 솔루션이 우선합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 최근 동향

- 시장 성장 촉진요인

- 중동 및 아프리카와 아시아태평양에서 해수 담수화 프로젝트의 설비 투자 증가

- 유럽과 북미에서의 폐수 재이용의 엄격한 의무화

- 미국 걸프 및 브라질에서 셰일 및 심해 석유 및 가스 프로젝트의 급속한 확대

- 북유럽과 중동에서 급증하는 지역 냉난방 도입량

- 인도와 아프리카에서 농업 관개의 전화(솔라 펌프)

- 시장 성장 억제요인

- 니켈과 스테인리스 스틸의 가격 변동이 BoM 팽창 초래

- 저가 중국 제조 업체의 급증이 금리를 압축

- OECD 국가의 화력 발전 파이프라인 감소 및 순환 펌프 감소

- 지방자치단체의 교체 사이클이 길고(15-20년), 연간 매출 제한 초래

- 공급망 분석

- 규제 전망

- 기술 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 분석

제5장 시장 규모 및 성장 예측

- 펌프 유형별

- 원심식(레이디얼 플로우, 액셜 플로우, 믹스 플로우)

- 용적식(회전식(기어, 로브, 베인, 스크류), 왕복동식(피스톤, 다이어프램, 플런저))

- 기타(특수, 제트 펌프)

- 샤프트 방향별

- 수평형

- 세로형

- 원동력별

- 전동식

- 엔진 구동

- 공압 및 공기 작동식

- 태양광 발전

- 최종 사용자별

- 상하수도 사업

- 석유 및 가스(업스트림, 미드스트림, 다운스트림)

- 화학제품 및 석유화학제품

- 발전(화력, 원자력, 재생에너지)

- 광업 및 금속

- HVAC 및 빌딩 서비스

- 농업 및 관개

- 건설 및 인프라

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 북유럽 국가

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Flowserve Corporation

- Grundfos Holding A/S

- KSB SE & Co. KGaA

- ITT Inc.

- Sulzer Ltd.

- Ebara Corporation

- Weir Group plc

- Xylem Inc.

- Wilo SE

- Pentair plc

- Tsurumi Manufacturing Co. Ltd.

- Torishima Pump Mfg. Co. Ltd.

- Baker Hughes Company

- Schlumberger Limited

- Celeros Flow Technology LLC

- Atlas Copco AB

- Kirloskar Brothers Ltd.

- Ruhrpumpen Group

- Desmi A/S

- Zoeller Pump Co.

제7장 시장 기회 및 향후 전망

AJY 25.11.24The Pumps Market size is estimated at USD 68.27 billion in 2025, and is expected to reach USD 86.10 billion by 2030, at a CAGR of 5.45% during the forecast period (2025-2030).

Growth is supported by large-scale water infrastructure upgrades, steady industrial capital spending, and the universal push for energy-efficient equipment. Electrification remains the dominant power source, while solar-powered systems create a fast-growing niche in agriculture and off-grid settings. Technical specifications are shifting toward smart, sensor-rich pumps that lower energy consumption, enable predictive maintenance, and meet tightening environmental rules. Competitive intensity is rising as established suppliers broaden portfolios through acquisitions and low-cost Asian entrants compete on price and delivery speed. Supply-chain strategies increasingly emphasize material savings and multi-regional sourcing to counter raw-material price swings.

Global Pumps Market Trends and Insights

Escalating CAPEX in Desalination Projects across MENA & APAC

Seawater-desalination build-outs in Saudi Arabia and the UAE exceeded USD 4.8 billion in 2024, spurring demand for high-pressure pumps with ceramic composite wetted parts that last 40% longer than stainless-steel equivalents. Energy-recovery devices now standardize in new plants, trimming operating costs by up to 60% and raising technical barriers that favor suppliers with proven marine-grade materials expertise. Manufacturers with desalination references are capitalizing on premium pricing while competitors race to secure similar credentials.

Stringent Wastewater Reuse Mandates in Europe & North America

The revised EU Urban Waste Water Treatment Directive targets steep cuts in phosphorus and PFAS, accelerating adoption of precision-dosing and variable-flow circulation pumps able to support advanced oxidation and membrane filtration. Municipalities allocate more budget to integrated pump packages, raising the average order value by 27%. Suppliers offering controls and remote-monitoring capabilities are winning bids as utilities shift to outcome-based procurement.

Volatility in Nickel & Stainless-Steel Prices Inflating BoM

Pump producers report stainless-steel content of 30-40% in positive-displacement designs, so price spikes squeeze margins. Leading European brands now use computational fluid dynamics to reduce alloy weight by 15% in selected models and hedge exposure through multi-regional sourcing.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Shale & Deep-water O&G Projects in US Gulf & Brazil

- Surging District Cooling & Heating Installations in Nordics & Middle East

- Proliferation of Low-cost Chinese Manufacturers Compressing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal pumps accounted for 56.8% of pumps market share in 2024. Continuous improvements in impeller geometry and guide-blade profiles have lifted hydraulic efficiency by up to 15%. The segment is forecast to post a 6.2% CAGR, outpacing the overall pumps market. Widespread use in water supply, HVAC and refinery services provides a stable base, while emerging carbon-capture plants require tailored CO2-handling models with advanced seals and corrosion-resistant alloys.

Specialized centrifugal variants now enter carbon-capture and storage (CCS) circuits, where liquid and supercritical CO2 present complex thermodynamic behavior. Vendors integrating sensor arrays enable operators to run close to best-efficiency points, cutting energy consumption and maintenance costs. Positive-displacement designs remain indispensable in metering, chemical injection and high-pressure slurry duties, commanding premium pricing due to stricter performance tolerances across these niches.

Horizontal machines still dominate 60% of the pumps market share due to familiarity, straightforward maintenance, and lower initial cost. However, vertical inline and submersible models are set to grow by 5.8% CAGR as urban utilities and data-center builders confront floor-space constraints. ABB's pending addition of Aurora Motors strengthens its vertical-motor lineup, signaling supplier confidence in long-term upside.

Vertical pumps thrive in deep-well water supply, mining dewatering ,and wastewater wet-well installations where the driver remains above the fluid. Upgraded bearing systems and abrasion-resistant coatings allow longer run times between pulls. Segment demand also benefits from stricter building codes that favor compact plantrooms and stacked mechanical spaces.

The Pumps Market Report is Segmented by Pump Type (Centrifugal, Positive Displacement, and Others), Shaft Orientation (Horizontal and Vertical), Driving Force (Electric-Driven, Engine-Driven, Pneumatic, and Solar-Powered), End User (Water and Waste-Water Utilities, Chemicals and Petrochemicals, Power Generation, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific leads the pumps market with 51.60% share in 2024 and is expected to post a 6.0% CAGR through 2030. Massive urbanization, ambitious desalination pipelines, and strong agricultural modernization underpin growth. China's national heat-pump roadmap and India's solar-pump rollout sustain high-volume demand. Regional manufacturers move up the value chain toward sensor-enabled units, intensifying local competition.

North America remains innovation-driven. Federal water-infrastructure funding of USD 3.0 billion for lead-service-line replacement in FY2024 stimulates advanced potable-water equipment orders. Shale development in the US Gulf boosts demand for 10,000-psi fracturing pumps, while Canadian miners procure hard-wearing slurry units. Heat pumps outsold gas furnaces by 27% in 2024, highlighting electrification's ripple effect on pump selection.

Europe emphasizes lifecycle efficiency and environmental compliance. The updated EU wastewater directive creates a sizeable market for precision-dosing and membrane-feed pumps. Nordic district-heating networks scale rapidly, requiring large circulation pumps compatible with low-temperature operation. Utilities in Germany and the United Kingdom deploy predictive-maintenance software to lift asset availability and stretch replacement intervals. The Middle East channels heavy investment into desalination and district cooling, whereas many African economies prioritize off-grid solar irrigation solutions to raise farm yields and reduce diesel dependence.

- Flowserve Corporation

- Grundfos Holding A/S

- KSB SE & Co. KGaA

- ITT Inc.

- Sulzer Ltd.

- Ebara Corporation

- Weir Group plc

- Xylem Inc.

- Wilo SE

- Pentair plc

- Tsurumi Manufacturing Co. Ltd.

- Torishima Pump Mfg. Co. Ltd.

- Baker Hughes Company

- Schlumberger Limited

- Celeros Flow Technology LLC

- Atlas Copco AB

- Kirloskar Brothers Ltd.

- Ruhrpumpen Group

- Desmi A/S

- Zoeller Pump Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Recent Trends & Developments

- 4.3 Market Drivers

- 4.3.1 Escalating CAPEX in Desalination Projects across MENA & APAC

- 4.3.2 Stringent Waste-water Reuse Mandates in Europe & North America

- 4.3.3 Rapid Expansion of Shale & Deep-water O&G Projects in US Gulf & Brazil

- 4.3.4 Surging District Cooling & Heating Installations in Nordics & Middle East

- 4.3.5 Electrification of Agricultural Irrigation (Solar Pumps) in India & Africa

- 4.4 Market Restraints

- 4.4.1 Volatility in Nickel & Stainless-Steel Prices Inflating BoM

- 4.4.2 Proliferation of Low-cost Chinese Manufacturers Compressing Margins

- 4.4.3 Declining Thermal Power Pipeline in OECD Curtailing Circulation Pumps

- 4.4.4 Long Municipal Replacement Cycles (15?20 yrs) Limiting Annual Sales

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Investment Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Pump Type

- 5.1.1 Centrifugal (Radial-flow, Axial-flow and Mixed-flow)

- 5.1.2 Positive Displacement (Rotary (Gear, Lobe, Vane, Screw), and Reciprocating (Piston, Diaphragm, Plunger))

- 5.1.3 Others (Specialty, Jet Pumps)

- 5.2 By Shaft Orientation

- 5.2.1 Horizontal

- 5.2.2 Vertical

- 5.3 By Driving Force

- 5.3.1 Electric-driven

- 5.3.2 Engine-driven

- 5.3.3 Pneumatic/Air-operated

- 5.3.4 Solar-powered

- 5.4 By End-user

- 5.4.1 Water and Waste-water Utilities

- 5.4.2 Oil and Gas (Upstream, Midstream, Downstream)

- 5.4.3 Chemicals and Petrochemicals

- 5.4.4 Power Generation (Thermal, Nuclear, Renewables)

- 5.4.5 Mining and Metals

- 5.4.6 HVAC and Building Services

- 5.4.7 Agriculture and Irrigation

- 5.4.8 Construction and Infrastructure

- 5.4.9 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Nordic Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Malaysia

- 5.5.3.6 Thailand

- 5.5.3.7 Indonesia

- 5.5.3.8 Vietnam

- 5.5.3.9 Australia

- 5.5.3.10 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Flowserve Corporation

- 6.4.2 Grundfos Holding A/S

- 6.4.3 KSB SE & Co. KGaA

- 6.4.4 ITT Inc.

- 6.4.5 Sulzer Ltd.

- 6.4.6 Ebara Corporation

- 6.4.7 Weir Group plc

- 6.4.8 Xylem Inc.

- 6.4.9 Wilo SE

- 6.4.10 Pentair plc

- 6.4.11 Tsurumi Manufacturing Co. Ltd.

- 6.4.12 Torishima Pump Mfg. Co. Ltd.

- 6.4.13 Baker Hughes Company

- 6.4.14 Schlumberger Limited

- 6.4.15 Celeros Flow Technology LLC

- 6.4.16 Atlas Copco AB

- 6.4.17 Kirloskar Brothers Ltd.

- 6.4.18 Ruhrpumpen Group

- 6.4.19 Desmi A/S

- 6.4.20 Zoeller Pump Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment