|

시장보고서

상품코드

1851720

마이크로크리스탈린 왁스 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Microcrystalline Wax - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

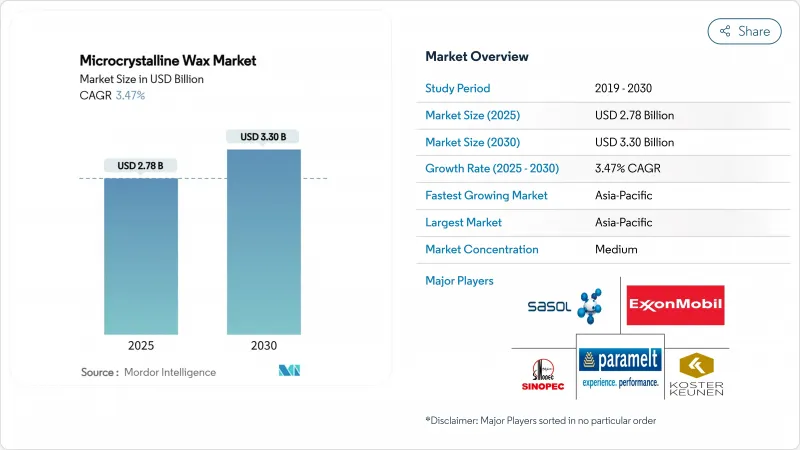

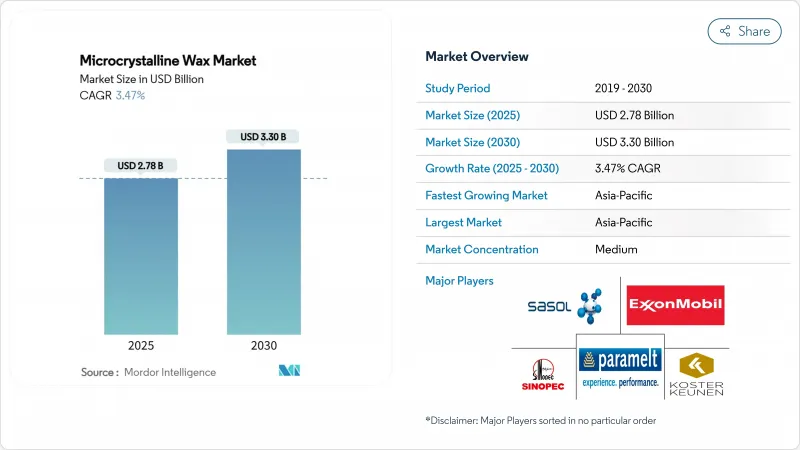

마이크로크리스탈린 왁스 시장 규모는 2025년에 27억 8,000만 달러로 평가되었고 예측 기간(2025-2030년)의 CAGR은 3.47%를 나타낼 것으로 예측되며 2030년에는 33억 달러에 달할 전망입니다.

화장품, 접착제 및 제약 분야의 꾸준한 확장이 이러한 성장세를 뒷받침하는 한편, 바이오 기반 원료로의 전환, 정유 시설 업그레이드 및 지속가능성 중심의 혁신이 경쟁 구도를 재조정하고 있습니다. 63-91°C의 높은 녹는점, 우수한 유연성 및 탁월한 향 유지력은 미세결정성 등급을 파라핀과 차별화하여 제형 개발자들이 열대 기후에서의 성능 요구를 충족할 수 있게 합니다. 아시아태평양 지역은 비용 효율적인 생산, 증가하는 내수 수요, 그리고 안정적인 원료 공급을 보장하는 중국과 인도의 대규모 정제소 프로젝트를 통해 주도권을 공고히 하고 있습니다. 한편, SASOLWAX LC100의 35% 낮은 배출량과 같은 지속가능성 지표는 이제 하류 사용자, 특히 프리미엄 뷰티 브랜드에게 중요한 구매 기준이 되고 있습니다.

세계의 마이크로크리스탈린 왁스 시장 동향 및 인사이트

화장품 및 퍼스널케어 제조거점의 확대

아시아태평양 지역의 계약 제조업체들은 립스틱, 립밤 및 프리미엄 스킨케어 제품 생산을 확대하고 있으며, 마이크로크리스탈린 왁스는 열대 기후에서도 텍스처 개선, 땀 방지, 유화 안정화 효과를 제공합니다. 중국과 인도의 대형 OEM 허브는 낮은 인건비와 탄탄한 공급망을 활용하여 식물성 오일과 완벽하게 혼합되는 유연한 등급의 대량 소비를 촉진합니다. FDA 및 EU 승인으로 국경 간 운송이 간소화되어 브랜드들은 규정 준수를 저해하지 않으면서 소수의 메가 시설에 생산을 집중할 수 있습니다. 인도네시아, 베트남, 필리핀의 중산층 소비 증가로 립컬러 신제품 출시가 두 자릿수 성장을 지속하며 지역 수요를 더욱 공고히 하고 있습니다. '클린 뷰티'를 추구하는 브랜드들은 식물성 왁스 혼합물을 시험 중이지만, 여전히 발색 품질과 제품 안정성을 유지하기 위해 마이크로크리스탈린 분획물에 의존하고 있습니다. 결과적으로 지속가능성 압박이 강화되는 가운데서도 마이크로크리스탈린 왁스 시장은 물량 확보를 지속하고 있습니다.

의약품 및 의료용도 수요 증가

의약품 제형 개발자들은 8-12시간 동안 용량 균일성을 보장하는 지속 방출 매트릭스 구축을 위해 마이크로크리스탈린 왁스를 채택합니다. 화학적 비활성 특성으로 인해 활성 성분과 직접 압축이 가능해 추가 장벽 코팅을 생략하고 개발 기간을 단축할 수 있습니다. 미국, 독일, 일본 등 고령화 시장에서 만성 질환 유병률이 증가함에 따라 왁스 기반 펠릿 기술을 활용한 지속형 통증 관리 및 내분비 치료제 수요가 높아지고 있습니다. ICH Q12에 따른 글로벌 규제 조화는 지역 간 허가 신청을 촉진하여 왁스 기반 제형의 한계 비용을 낮춥니다. 이에 따라 계약 개발 제조 기관(CDMO)들은 일관된 등급 사양을 확보하기 위해 장기 공급 계약을 체결하며, 고순도 경질 왁스 분획의 꾸준한 수요를 뒷받침합니다.

원유 공급의 변동이 원료 공급에 영향

지정학적 긴장과 OPEC 생산 제한으로 진공 잔류유 가용성이 주기적으로 위축되면서 정유사들은 특수 왁스 유동보다 고마진 연료 생산을 우선시합니다. 현물 가격 급등으로 마이크로크리스탈린 원료 비용이 최대 22% 상승하며 장기 구매 계약이 없는 독립 복합제조업체의 마진이 압박받고 있습니다. 서유럽 및 동아프리카의 수입 의존형 경제권은 운임 프리미엄이 변동성을 증폭시키므로 가장 심각한 차질을 겪습니다. 자체 원유 거래 데스크를 보유한 통합 메이저 기업들은 헤징을 통해 영향을 완화하지만, 중소 업체들은 재고 부족으로 고객 신뢰가 훼손될 위험에 직면합니다. 중기적으로는 합성 및 바이오매스 유래 왁스로의 다각화가 부분적 완화 방안을 제시하나, 규모 확대는 여전히 자본 집약적이고 시간이 소요됩니다.

부문 분석

경질 등급은 2025년에 더 강한 모멘텀으로 시작하여 2030년까지 연평균 4.18%의 성장률을 보일 것으로 예상되는 반면, 연질 등급은 2024년에 62.08%의 매출 우위를 유지할 것으로 보입니다. 65°C의 1형 라미네이팅 왁스는 인화지를 보호하고, 81°C의 2형 코팅 왁스는 식품 접촉 보드를 강화하며, 90°C의 3형 경화 왁스는 변압기 권선을 보호합니다. 이러한 미세 결정 구조는 우수한 절연 강도를 부여하고 지속적인 열 하에서 처짐을 방지하는 특성을 지니며, 이는 전기차 커패시터 제조사들이 점점 더 중요하게 여기는 요소입니다.

차동 스캐닝 열량계, 바늘 침투 시험, 링 앤 볼 연화점 시험을 기반으로 한 실험실 프로토콜은 배치 균일성을 보장하며 ISO 22007 정밀도 기준을 충족합니다. 지속적인 연구 개발은 점도를 저하시키지 않으면서 강성을 18% 향상시키는 나노 실리카 도핑을 탐구하여 EMI 차폐 코팅 분야의 새로운 틈새 시장을 개척하고 있습니다. 한편, 유연성 등급은 유연성과 유분 결합력이 중요한 립스틱, 립밤 및 보드 라미네이션 분야에서 점유율이 높습니다. 아시아태평양 지역의 계약 충전 공장 급속 확장은 유연성 등급의 안정적인 생산량을 뒷받침하며, 경질 등급 혁신이 가치 창출을 높이는 가운데 기초 수요를 유지합니다.

지역 분석

아시아태평양 지역은 2024년 매출의 47.22%를 차지했으며, 정유소 투자와 소비재 제조라는 두 가지 동력에 힘입어 2030년까지 연평균 3.91%의 성장률을 보일 것으로 전망됩니다. 인도는 2030년까지 일일 정유 능력을 80만 배럴 추가할 계획으로, 현지 왁스 생산자들의 원료 접근성을 확대할 것입니다. 중국의 수직 통합형 석유화학 단지와 라이프스타일 주도형 화장품 수요 증가는 원가 경쟁력을 확보합니다. 일본과 한국은 엄격한 공정 관리와 첨단 품질 관리 인프라를 활용해 전자제품용 고순도 경질 왁스에 집중합니다. 아세안 국가들은 관세 혜택과 원자재 공급 근접성으로 계약 제조를 유치하며 지역 자급률을 강화합니다.

북미는 특수 제형 개발사와 연구개발 중심 정유사를 통해 기술적 우위를 유지합니다. 식품 접촉용 FDA 승인 및 의약품 등급 USP 등재로 예측 가능한 규제 경로를 제공하여 안정적인 하류 소비를 뒷받침합니다. 미국은 국립 연구소에서 차세대 바이오 기반 왁스 블렌드를 개발 중이며, 멕시코의 확장 중인 자동차 조립 및 포장 클러스터는 접착제 및 코팅 수요를 촉진합니다. 캐나다 당국은 정제된 마이크로크리스탈린 분획물의 인체 건강 위험이 미미함을 확인하여 대중의 수용도를 높였다.

유럽은 엄격한 지속가능성 규정과 특수 혁신을 균형 있게 조율합니다. 브랜드들은 MOAH 및 MOSH 순도 의무를 준수해야 하므로 공급업체들은 인라인 GC-FID 모니터링을 설치하고 이중 수소화 공정을 도입하고 있습니다. 독일은 폐기물 바이오매스를 가스화하여 피셔-트로프쉬 왁스 중간체를 생산하는 순환형 탄소 프로젝트를 주도하는 반면, 네덜란드는 해양 생물 기원 원료를 시범 운영 중입니다. 동유럽 정제업체들은 지역 원유 흐름에서 가치를 확보하기 위해 하이드로크래커를 개조하여 현지 공급량을 늘리고 있습니다. 다른 지역에서는 브라질의 급성장하는 개인 위생용품 수출과 사우디아라비아의 특수화학 투자 프레임워크가 각각 남미와 중동 및 아프리카에서 점진적인 성장 기회를 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 확대하는 화장품 및 퍼스널케어 제조 거점

- 의약품 및 의료 용도 수요 증가

- 핫멜트 접착제에서 파라핀에서 마이크로크리스탈린 왁스로 대체

- 정유 공장에서 바이오 기반 원료로의 전환 가속화

- 지속가능한 포장을 위한 저온 식품 접촉 코팅 성장

- 시장 성장 억제요인

- 원유 공급의 변동이 원료 공급력에 영향

- 프리미엄 화장품에서 광물성 성분에 대한 규제적 저항

- 왁스 잔류물이 엄격한 해양 배출 규제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 가격 분석

- 무역 분석

제5장 시장 규모와 성장 예측

- 유형별

- 연질

- 경질

- 용도별

- 화장품 및 퍼스널케어

- 양초

- 접착제

- 패키지

- 고무

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Alfa Chemicals

- Alpha Wax

- Blended Waxes Inc.

- The British Wax Refining Company Ltd

- Calumet, Inc.,

- Clarus Specialty Products

- Exxon Mobil Corporation

- Indian Oil Corp. Ltd.

- Industrial Raw Materials LLC.

- Koster Keunen

- Kerax

- NIPPON SEIRO CO., LTD.

- Paramelt BV

- Sasol

- Sonneborn LLC

- The International Group Inc.

제7장 시장 기회와 장래의 전망

HBR 25.11.17The Microcrystalline Wax Market size is estimated at USD 2.78 billion in 2025, and is expected to reach USD 3.30 billion by 2030, at a CAGR of 3.47% during the forecast period (2025-2030).

Steady expansion in cosmetics, adhesives and pharmaceutical uses underpins this trajectory, while the shift toward bio-based feedstocks, refinery upgrades and sustainability-driven innovation recalibrate competitive positioning. Higher melting points of 63-91 °C, excellent flexibility and superior fragrance retention continue to differentiate microcrystalline grades from paraffin, enabling formulators to meet performance demands in tropical climates. Asia-Pacific entrenches its leadership through cost-effective production, rising domestic demand and large-scale refinery projects in China and India that ensure reliable feedstock. Meanwhile, sustainability metrics-such as SASOLWAX LC100's 35% lower emissions-now form a critical purchase criterion for downstream users, especially premium beauty brands.

Global Microcrystalline Wax Market Trends and Insights

Expanding Cosmetics and Personal-Care Manufacturing Bases

Asia-Pacific contract manufacturers scale up lipstick, balm and premium skin-care production, and microcrystalline wax enhances texture, prevents sweating and stabilizes emulsions under tropical temperatures. Large OEM hubs in China and India leverage lower labor costs and robust supply chains, raising bulk consumption for flexible grades that blend seamlessly with plant oils. FDA and EU approvals simplify cross-border shipping, allowing brands to consolidate output in a few mega-facilities without compromising compliance. Rising middle-class spending in Indonesia, Vietnam and the Philippines sustains double-digit growth in lip-color launches, further anchoring regional demand. Brands pursuing "clean beauty" narratives trial plant wax blends yet still rely on microcrystalline fractions to maintain payoff quality and product stability. Consequently, the microcrystalline wax market continues to secure volumes even as sustainability pressures intensify.

Growing Demand from Pharmaceutical and Medical Applications

Drug formulators adopt microcrystalline wax to build sustained-release matrices that ensure dose uniformity across 8-12 hour windows. Its chemical inertness allows direct compression with active ingredients, avoiding additional barrier coatings and shortening development timelines. Chronic disease prevalence in aging markets such as the United States, Germany and Japan elevates demand for long-acting pain management and endocrinology therapies, both of which leverage wax-based pellet technology. Global regulatory harmonization under ICH Q12 boosts cross-regional filings, lowering marginal costs for wax-enabled formulations. Contract development manufacturing organizations (CDMOs) therefore lock in long-term supply contracts to secure consistent grade specifications, reinforcing steady offtake for high-purity hard wax fractions.

Crude-Oil Supply Volatility Impacting Feedstock Availability

Geopolitical tensions and OPEC production curbs periodically tighten vacuum-resid availability, leading refiners to prioritize higher-margin fuels rather than specialty wax streams. Spot price spikes raise microcrystalline feed costs by up to 22%, compressing margins for independent compounders lacking long-term offtake contracts. Import-dependent economies in Western Europe and East Africa face the sharpest disruptions, since freight premiums amplify volatility. Integrated majors with captive crude trade desks cushion the impact through hedging, but smaller players risk stock-outs that erode customer trust. Over the medium term, diversification into synthetic and biomass-derived waxes offers partial mitigation, yet scaling remains capital intensive and time consuming.

Other drivers and restraints analyzed in the detailed report include:

- Substitution of Paraffin with Microcrystalline Wax in Hot-Melt Adhesives

- Shift Toward Bio-Based Feedstock Upgrading at Refineries

- Regulatory Pushback on Mineral-Based Ingredients in Premium Cosmetics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard-type grades opened 2025 with stronger momentum, forecast to climb at a 4.18% CAGR to 2030 while flexible grades maintained 62.08% revenue dominance in 2024. Type 1 laminating wax at 65 °C safeguards photographic paper, Type 2 coating wax at 81 °C fortifies food-contact boards, and Type 3 hardening wax at 90 °C protects transformer windings. These fine-crystal structures impart superior dielectric strength and resist slump under sustained heat, attributes increasingly valued by electric-vehicle capacitor makers.

Laboratory protocols relying on differential scanning calorimetry, needle penetration and ring-and-ball softening point testing ensure batch homogeneity, meeting ISO 22007 precision benchmarks. Ongoing R&D explores nano-silica doping that lifts modulus by 18% without sacrificing viscosity, opening new niches in EMI shielding coatings. Flexible grades, meanwhile, dominate lipstick, balm and board-laminating volumes where pliability and oil-binding are critical. Rapid expansion of APAC contract filling plants underpins consistent throughput for flexible fractions, anchoring baseline demand even as hard-grade innovations lift value capture.

The Microcrystalline Wax Market Report is Segmented by Type (Flexible and Hard), Application (Cosmetics and Personal Care, Candles, Adhesives, Packaging, Rubber, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 47.22% revenue in 2024 and is projected to expand at a 3.91% CAGR through 2030 on the twin engines of refinery investment and consumer-product manufacturing. India plans to add 800,000 barrels per day of refining capacity by 2030, broadening feedstock access for local wax producers. China's vertically integrated petrochemical complexes, coupled with lifestyle-driven cosmetics uptake, secure cost leadership. Japan and South Korea concentrate on high-purity hard grades for electronics, leveraging tight process controls and advanced QC infrastructure. ASEAN nations attract contract manufacturing owing to tariff advantages and proximity to raw-material supply, reinforcing regional self-sufficiency.

North America retains technological leadership via specialty formulators and R&D-oriented refiners. FDA clearances for food-contact use and USP listings for pharmaceutical grades provide predictable regulatory paths, supporting steady downstream consumption. The United States develops next-gen bio-based wax blends within national labs, while Mexico's expanding auto-assembly and packaging clusters stimulate adhesive and coating demand. Canadian authorities confirmed negligible human-health risk from refined microcrystalline fractions, bolstering public acceptance.

Europe balances stringent sustainability rules with specialty innovation. Brands face MOAH and MOSH purity mandates, prompting suppliers to install inline GC-FID monitoring and adopt double-hydrogenation routes. Germany champions circular-carbon projects that gasify waste biomass into Fischer-Tropsch wax intermediates, whereas the Netherlands pilots marine-biogenic feedstock. Eastern European refiners retrofit hydrocrackers to capture value from regional crude flows, raising local availability. Elsewhere, Brazil's booming personal-care exports and Saudi Arabia's specialty-chem investment frameworks hint at incremental pockets of growth in South America and Middle-East and Africa, respectively.

- Alfa Chemicals

- Alpha Wax

- Blended Waxes Inc.

- The British Wax Refining Company Ltd

- Calumet, Inc.,

- Clarus Specialty Products

- Exxon Mobil Corporation

- Indian Oil Corp. Ltd.

- Industrial Raw Materials LLC.

- Koster Keunen

- Kerax

- NIPPON SEIRO CO., LTD.

- Paramelt B.V

- Sasol

- Sonneborn LLC

- The International Group Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Cosmetics and Personal-Care Manufacturing Bases

- 4.2.2 Growing Demand from Pharmaceutical and Medical Applications

- 4.2.3 Substitution of Paraffin with Microcrystalline Wax in Hot-Melt Adhesives

- 4.2.4 Shift Toward Bio-Based Feedstock Upgrading at Refineries

- 4.2.5 Growth of Low-Temperature Food-Contact Coatings for Sustainable Packaging

- 4.3 Market Restraints

- 4.3.1 Crude-Oil Supply Volatility Impacting Feedstock Availability

- 4.3.2 Regulatory Pushback on Mineral-Based Ingredients in Premium Cosmetics

- 4.3.3 Tight Marine Discharge Regulations on Wax Residues

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

- 4.6 Price Analysis

- 4.7 Trade Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Flexible

- 5.1.2 Hard

- 5.2 By Application

- 5.2.1 Cosmetics and Personal Care

- 5.2.2 Candles

- 5.2.3 Adhesives

- 5.2.4 Packaging

- 5.2.5 Rubber

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alfa Chemicals

- 6.4.2 Alpha Wax

- 6.4.3 Blended Waxes Inc.

- 6.4.4 The British Wax Refining Company Ltd

- 6.4.5 Calumet, Inc.,

- 6.4.6 Clarus Specialty Products

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 Indian Oil Corp. Ltd.

- 6.4.9 Industrial Raw Materials LLC.

- 6.4.10 Koster Keunen

- 6.4.11 Kerax

- 6.4.12 NIPPON SEIRO CO., LTD.

- 6.4.13 Paramelt B.V

- 6.4.14 Sasol

- 6.4.15 Sonneborn LLC

- 6.4.16 The International Group Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment