|

시장보고서

상품코드

1851721

혈전증 치료제 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Thrombosis Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

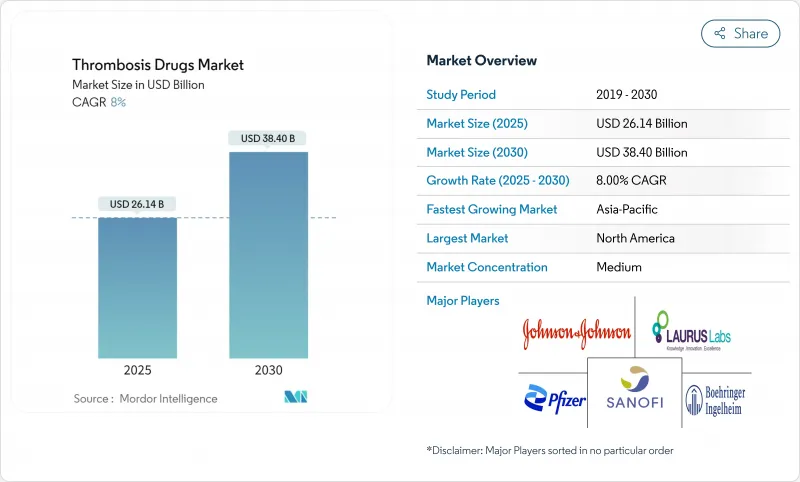

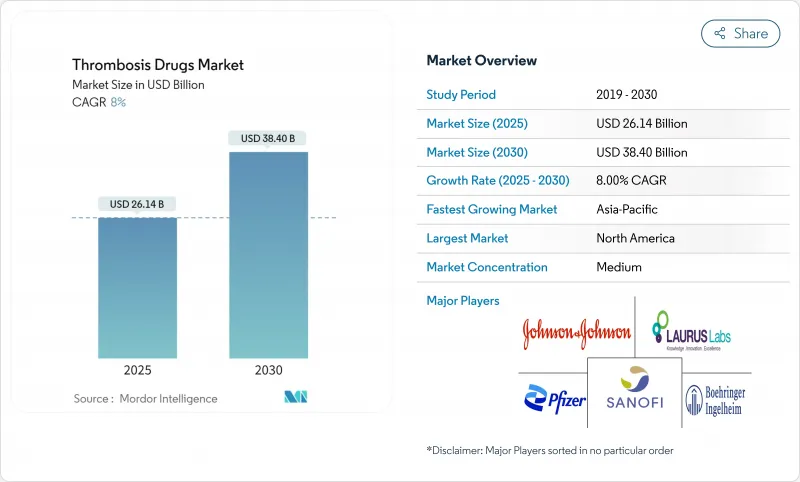

혈전증 치료제 시장 규모는 2025년에 261억 4,000만 달러로 추정되고, 2030년에는 384억 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 8.0%로 추이할 전망입니다.

평균 수명 연장, 정맥 혈전 색전증(VTE) 이환율 상승, 경구 직접 항응고제(DOAC)의 채용 가속이 견조한 수요를 지지하고 있습니다. First-in-class 인자 XI 인자 억제제에 대한 규제 Greenlight는 인공지능을 이용한 위험 계층화 도구와 함께 와파린 및 헤파린 이외 치료법의 선택을 재구성하고 있습니다. 1일 1회 투여의 경구 DOAC를 외래로 사용하는 것이 일상적인 표준이 되고 있는 현재에도, 병원은 급성기 의료에 있어서 속효성 주사제를 선호하고 사용하고 있습니다. 특허의 절벽이 다가오고 있는 것에 대한 경쟁의 대응으로는 보다 안전한 작용기전을 중심으로 한 통합, 브랜드로부터 제네릭 의약품으로 이행기에서의 충성도 유지를 목적으로 한 할인 프로그램 등을 들 수 있습니다.

세계의 혈전증 치료제 시장 동향 및 인사이트

VTE 유병률 상승

평균 수명 연장과 암 생존율의 급증으로 VTE 발병률이 상승하고 장기적인 항응고 요법이 만성 질환 치료에 필수적인 요소가 되고 있습니다. 폐암 환자의 폐색전증 이환율은 기준치의 약 6배이며, 보다 안전한 경구약에 대한 수요가 높아지고 있습니다. 병원은 항응고 요법을 단발적인 것에서 지속적인 것으로 전환시키기 위해 혈전증 프로토콜을 종양 내과의 경로에 통합함으로써 대응합니다.

DOAC의 급속한 보급

ROCKET-AF와 ARISTOTLE에서 얻은 증거는 리버 록사반과 아픽 사반에 대한 처방자의 신뢰를 높이고 있습니다. 브리스톨 마이어스 스퀴브와 파이저는 2024년 4분기에 Eliquis 매출 32억 달러를 기록했습니다. 2026년 1월에 발효된 메디케어 협상 가격에 따라 환자의 자기 부담액이 하락하고, 이폭을 해치지 않으며 대상이 확대됩니다.

신규 항응고제의 고비용

신규 항응고제의 정가는 워팔린의 정가를 밑도는 경우가 많아 가격에 민감한 지역에서의 사용을 억제하고 있습니다. 브리스톨 마이어스 스퀴브와 파이저는 현재 엘릭스를 40% 할인으로 환자에게 직접 판매하고 있으며 월간 비용을 346달러까지 낮추고 있습니다. 메디케어 협상과 같은 정책 전환은 보다 광범위한 가격 압력이 임박하고 있음을 시사합니다.

부문 분석

DOAC는 2024년 혈전증 치료제 시장 점유율의 55.1%를 차지하였고, 투여가 간편화되고 모니터링의 필요성이 감소한 것을 배경으로 확대해 혈전증 치료제 시장 규모의 144억 달러를 차지했습니다. 인자 XI 억제제는 출혈을 싫어하는 임상의와 환자를 전환시켜 CAGR 8.61%에서 상승할 것으로 예측됩니다.

헤파린과 LMWH는 입원 환자의 브리징과 종양학 프로토콜 간의 연관성을 유지합니다. 비타민 K 길항제는 자원이 제한된 환경에서의 사용에 머물며 혈전 용해제는 뇌졸중과 대량 폐색전증 긴급 시 틈새 역할을 유지합니다. 월 1회 피하 투여의 인자 XI 제제의 출현은 전통적인 경구제와 주사제의 경계를 모호하게 하여 혈전증 치료제 시장에서 경쟁 요인의 배치를 재구성할 수 있습니다.

심부정맥혈전증은 2024년 혈전증 치료제 시장 규모의 31.81%를 차지했으며, 정형외과 수술 후 가이드라인에 따른 항응고요법이 견인합니다. 폐색전증은 CAGR 8.43%로 가장 급속히 확대될 전망이며, CT 혈관 조영 진단의 개선에 뒷받침됩니다.

폐색전증 대응팀(PERT)의 채용에 의해 신속한 치료가 표준화되는 한편, 암 관련 혈전증은 생존율의 상승에 따라 인지도가 높아집니다. 심방 세동 환자의 뇌졸중 예방은 특히 XI 인자 제형의 안전성 데이터에 의해 더 광범위한 적용이 기대되고 여전히 가치있는 용도입니다.

지역 분석

북미의 상환제도와 DOAC의 조기 도입으로 2024년 혈전증 치료제 시장 점유율은 38.2%가 되었습니다. 연방 정부의 가격 협상은 합리적인 가격과 기술 혁신의 균형을 맞추기 위해 연구 개발 투자를 방해하지 않고 약물에 대한 접근을 확대할 수 있습니다.

유럽은 획기적인 약물의 도입을 가속화하는 임상 지침의 조화를 유지하고 있으며, 이 지역은 인구 역학의 고령화에 힘입어 일관되게 한 자릿수 중반의 성장을 보여주고 있습니다.

아시아태평양의 CAGR은 7.93%로 예측되며, 인프라 정비와 선택적 수술 건수 증가로부터 혜택을 받습니다. 중국의 단계적 병원 개혁과 인도의 아유슈만 발라트 제도는 피보험자층을 확대하고 일본의 초고령화 사회는 1인당 항응고제 사용량이 많습니다. 라틴아메리카와 중동 및 아프리카는 뒤쳐지고 있지만, 인지도 향상 캠페인 및 수입 제네릭 의약품이 진입 장벽을 낮추고 혈전증 치료제 시장의 발자취를 점차 확대하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정맥혈전색전증(VTE) 유병률 상승

- 직접 경구 항응고제(DOAC)의 급속한 보급

- 증대하는 수술 건수 및 주술기 예방의 필요성

- 출혈 리스크의 저하가 기대되는 제XI 인자 억제제의 파이프라인

- 입원 환자의 혈전 예방을 위한 COVID 트리거 프로토콜

- 표적 치료를 가능하게 하는 AI 기반의 리스크 층별화의 확대

- 시장 성장 억제요인

- 신규 항응고제의 고비용

- 특허 만료 및 제네릭의 침식

- 안전성에 대한 우려-대출혈 및 한정된 중화약

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 약제 클래스별

- 직접 경구 항응고제(DOACs)

- 헤파린 및 저분자 헤파린

- 비타민 K 길항제

- 혈전 용해제 및 선용약

- P2Y12 혈소판 억제제

- 제XI/XII인자 억제제(신흥)

- 기타

- 질환 유형별

- 심부정맥혈전증

- 폐색전증

- 심방세동

- 말초동맥질환

- 뇌졸중 및 일시적인 뇌허혈 발작

- 기타

- 투여 경로별

- 경구

- 주사

- 외용

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 통신 판매 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Bristol Myers Squibb

- Pfizer Inc.

- Bayer AG

- Johnson & Johnson(Janssen)

- Boehringer Ingelheim

- Daiichi Sankyo

- Sanofi SA

- Aspen Pharmacare

- LEO Pharma

- CSL Behring

- Grifols SA

- F. Hoffmann-La Roche

- Fresenius Kabi

- Viatris

- Cipla Ltd.

- Natco Pharma

- Glenmark Pharmaceuticals

- Alkem Laboratories

- Dr. Reddy's Laboratories

- Hikma Pharmaceuticals

제7장 시장 기회 및 향후 전망

AJY 25.11.24The thrombosis drugs market size stands at USD 26.14 billion in 2025 and is projected to attain USD 38.40 billion by 2030, advancing at an 8.0% CAGR during the forecast period.

Expanded life expectancy, rising venous thrombo-embolism (VTE) incidence, and accelerated adoption of direct oral anticoagulants (DOACs) are underpinning steady demand. Regulatory green lights for first-in-class Factor XI inhibitors, together with artificial-intelligence risk stratification tools, are recasting therapy selection beyond warfarin and heparin. Hospitals continue to favor rapid-onset injectables for acute care even as outpatient use of once-daily oral DOACs becomes the routine standard. Competitive responses to approaching patent cliffs include consolidation around safer mechanisms of action and discount programs aimed at sustaining loyalty during the shift from brands to generics.

Global Thrombosis Drugs Market Trends and Insights

Rising VTE prevalence

Higher life expectancy and a surge in cancer survival elevate VTE incidence, making long-term anticoagulation an essential component of chronic disease care. Lung-cancer patients face pulmonary-embolism rates roughly six times the population baseline, creating durable demand for safer oral agents. Hospitals respond by embedding thrombosis protocols within oncology pathways, shifting anticoagulation from episodic to continuous management.

Rapid adoption of DOACs

Evidence from ROCKET-AF and ARISTOTLE continues to drive prescriber confidence in rivaroxaban and apixaban. Bristol Myers Squibb and Pfizer recorded USD 3.2 billion in Eliquis sales in Q4 2024. Upcoming Medicare-negotiated prices effective January 2026 lower patient out-of-pocket costs, broadening eligibility without compromising margins.

High cost of novel anticoagulants

List prices often dwarf those of warfarin, curbing uptake in price-sensitive regions. Bristol Myers Squibb and Pfizer now sell Eliquis direct to patients at 40% discount, dropping monthly costs to USD 346. Policy shifts such as Medicare negotiations suggest broader price pressure is imminent.

Other drivers and restraints analyzed in the detailed report include:

- Growing surgical volumes & peri-operative prophylaxis

- Expanding pipeline of Factor XI inhibitors

- Patent expiries & generic erosion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DOACs yielded 55.1% thrombosis drugs market share in 2024 and represent a USD 14.4 billion slice of the thrombosis drugs market size, expanding on the back of simplified dosing and fewer monitoring demands. Factor XI inhibitors are forecast to climb at an 8.61% CAGR, converting bleeding-averse clinicians and patients.

Heparin and LMWHs sustain relevance for in-patient bridging and oncology protocols. Vitamin K antagonists retreat to resource-limited settings, while thrombolytics retain niche roles in stroke and massive pulmonary-embolism emergencies. The arrival of once-monthly subcutaneous Factor XI agents could blur traditional oral-versus-injectable boundaries, recasting competitive alignment within the thrombosis drugs market.

Deep-vein thrombosis accounted for 31.81% of thrombosis drugs market size in 2024, driven by guideline-mandated anticoagulation post-orthopedic surgery. Pulmonary embolism is set to expand fastest at 8.43% CAGR, fueled by improved CT angiography diagnostics.

Adoption of Pulmonary Embolism Response Teams (PERTs) standardizes rapid treatment, while cancer-associated thrombosis gains visibility as survival rates rise. Stroke prevention in atrial-fibrillation patients remains a high-value application, especially with Factor XI safety data promising broader eligibility.

The Thrombosis Drugs Market Report is Segmented by Drug Class (Direct Oral Anticoagulants, Heparin & Low-Molecular-Weight Heparin, and More), Disease Type (Deep Vein Thrombosis, Pulmonary Embolism, and More), Route of Administration (Oral, Injectable, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's reimbursement systems and early DOAC adoption anchored 38.2% thrombosis drugs market share in 2024. Federal price negotiations aim to balance affordability with innovation, potentially widening drug access without hampering R&D investments.

Europe maintains harmonized clinical guidelines that speed incorporation of breakthrough agents; the region shows consistent mid-single-digit growth supported by aging demographics.

Asia-Pacific, projected at 7.93% CAGR, benefits from infrastructure upgrades and higher elective-surgery volumes. China's tiered hospital reform and India's Ayushman Bharat scheme expand insured cohorts, while Japan's super-aged society sustains high per-capita anticoagulant use. Latin America and the Middle East & Africa trail but show rising awareness campaigns and imported generics that lower entry barriers, gradually enlarging their footprint in the thrombosis drugs market.

- Bristol-Myers Squibb

- Pfizer

- Bayer

- Johnson & Johnson

- Boehringer Ingelheim

- Daiichi Sankyo

- Sanofi

- Aspen Pharmacare

- Leo Pharma

- CSL Behring

- Grifols

- Roche

- Fresenius

- Viatris

- Cipla

- NATCO Pharma

- Glenmark Pharmaceuticals

- Alkem Laboratories

- Dr. Reddy's Laboratories

- Hikma Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising venous thrombo-embolism (VTE) prevalence

- 4.2.2 Rapid adoption of direct oral anticoagulants (DOACs)

- 4.2.3 Growing surgical volumes & peri-operative prophylaxis need

- 4.2.4 Pipeline of Factor XI inhibitors promising lower bleed risk

- 4.2.5 COVID-triggered protocols for inpatient thromboprophylaxis (under-reported)

- 4.2.6 Expansion of AI-based risk stratification enabling targeted therapy (under-reported)

- 4.3 Market Restraints

- 4.3.1 High cost of novel anticoagulants

- 4.3.2 Patent expiries & generic erosion

- 4.3.3 Safety concerns - major bleeding & limited reversal agents

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Drug Class (Value)

- 5.1.1 Direct Oral Anticoagulants (DOACs)

- 5.1.2 Heparin & Low-Molecular-Weight Heparin

- 5.1.3 Vitamin K Antagonists

- 5.1.4 Thrombolytics / Fibrinolytics

- 5.1.5 P2Y12 Platelet Inhibitors

- 5.1.6 Factor XI / XII Inhibitors (emerging)

- 5.1.7 Others

- 5.2 By Disease Type (Value)

- 5.2.1 Deep Vein Thrombosis

- 5.2.2 Pulmonary Embolism

- 5.2.3 Atrial Fibrillation

- 5.2.4 Peripheral Arterial Disease

- 5.2.5 Stroke & Transient Ischemic Attack

- 5.2.6 Others

- 5.3 By Route of Administration (Value)

- 5.3.1 Oral

- 5.3.2 Injectable

- 5.3.3 Topical

- 5.4 By Distribution Channel (Value)

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Mail-Order Pharmacies

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Bristol Myers Squibb

- 6.3.2 Pfizer Inc.

- 6.3.3 Bayer AG

- 6.3.4 Johnson & Johnson (Janssen)

- 6.3.5 Boehringer Ingelheim

- 6.3.6 Daiichi Sankyo

- 6.3.7 Sanofi S.A.

- 6.3.8 Aspen Pharmacare

- 6.3.9 LEO Pharma

- 6.3.10 CSL Behring

- 6.3.11 Grifols S.A.

- 6.3.12 F. Hoffmann-La Roche

- 6.3.13 Fresenius Kabi

- 6.3.14 Viatris

- 6.3.15 Cipla Ltd.

- 6.3.16 Natco Pharma

- 6.3.17 Glenmark Pharmaceuticals

- 6.3.18 Alkem Laboratories

- 6.3.19 Dr. Reddy's Laboratories

- 6.3.20 Hikma Pharmaceuticals

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment