|

시장보고서

상품코드

1851723

뇌 임플란트 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Brain Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

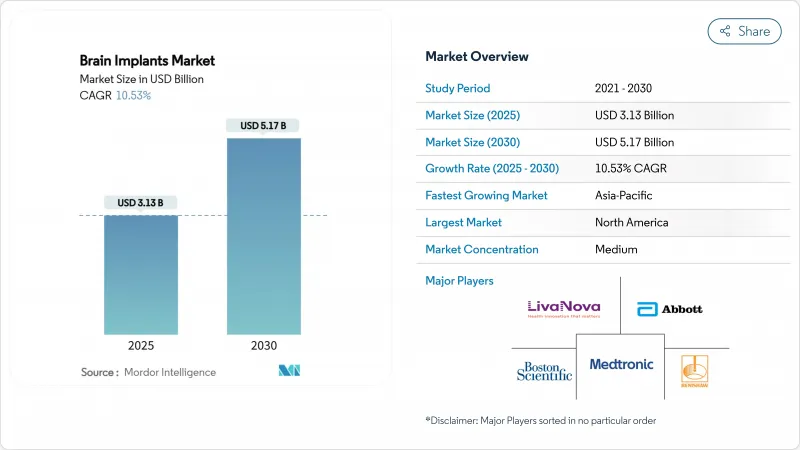

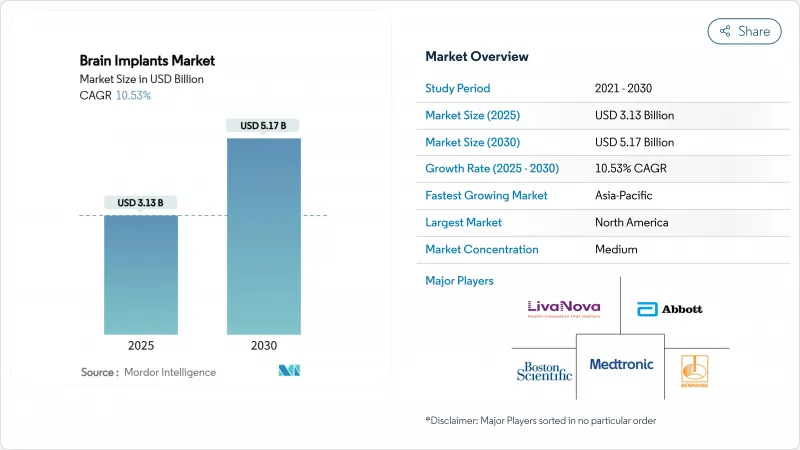

뇌 임플란트 시장 규모는 2025년에 31억 3,000만 달러로 평가되었고 2030년에는 51억 7,000만 달러에 이를 것으로 예측되며, CAGR은 10.53%를 나타낼 전망입니다. 이는 지속적인 투자 모멘텀과 전 세계 환자들의 치료 시간 단축을 가능케 하는 신속한 규제 승인을 반영합니다.

보험사 수용 확대, 센서 소형화, AI 기반 폐쇄 루프 시스템이 신경 중재 전략을 재정의하며 심부 뇌 자극(DBS), 미주신경 자극(VNS), 신흥 뇌-컴퓨터 인터페이스(BCI) 솔루션에 새로운 길을 열고 있습니다. 업체들은 그래핀 전극과 생체 적합성 코팅을 적극 도입해 기기 수명을 연장하는 한편, 유연한 미세전극 배열로 조직 손상을 줄이고 수술 후 회복을 가속화하고 있습니다. 블랙록 뉴로테크의 2억 달러(약 2,700억 원) 조달과 같은 10억 달러 규모의 투자 유입은 여러 치료 분야에서 상업적 준비 상태를 입증하고 있습니다. 한편, FDA 혁신 의료기기(Breakthrough Device) 및 EU 의료기기 규정(MDR) 신속 승인 경로는 차세대 신경 기술의 승인 기간을 지속적으로 단축시키며, 아시아태평양 지역이 시스템 전반의 도입을 가속화하는 가운데 북미의 선도적 위치를 공고히 하고 있습니다.

세계의 뇌 임플란트 시장 동향 및 인사이트

신경 퇴행성 질환과 운동 장애의 유병률 상승

전 세계 파킨슨병 환자는 2050년까지 2,520만 명에 달할 전망으로, 현재 부담의 두 배에 이르며 DBS(심부 뇌 자극술) 대상자 풀을 확대할 것입니다. 약물 내성 간질은 이미 1,010만 명에게 영향을 미치며 이들은 여전히 수술적 개입 대상자이며, 치료 저항성 우울증은 정신과적 기기 채택을 지속적으로 주도하고 있습니다. 선진 시장의 고령화 인구와 신흥 경제권의 진단 자원 개선이 결합되어 시술 건수가 꾸준히 유지될 전망입니다. 보건경제학 연구에 따르면 2024년 DBS 시술은 환자당 연간 약물 비용 2만-3만5,000달러를 절감하여 총 지출을 일반적으로 인정되는 비용 효율성 기준선 아래로 유지할 수 있습니다.

소형화 및 폐쇄 루프 기술의 발전

그래핀 전극과 나노다공성 금속은 이식 부위를 최대 70%까지 축소시켜 신호 정확도를 높이고 수술 후 염증을 감소시켰습니다. 전력 소모를 줄이는 신경모방 프로세서 덕분에 배터리 수명이 연장되었으며, 애보트의 인피니티 DBS와 같은 충전식 플랫폼은 스마트폰 기반 매개변수 업데이트를 가능하게 합니다. 기기 내 머신러닝 펌웨어는 실시간으로 자극을 조정하여 치료를 정적 설정에서 동적 환자 맞춤형 프로토콜로 전환합니다. 이러한 발전은 종합적으로 외래 환자 회복을 가속화하고 장기적 효능을 높이며 의사의 수용도를 확대합니다.

고가의 장비와 수술 비용

하드웨어, 수술, 1년차 프로그래밍을 포함한 전체 DBS 에피소드 비용은 140,000-190,000달러이며, 연간 유지 관리비는 4,500-7,800달러입니다. 많은 신흥국에서는 이러한 비용이 연간 가구 소득을 초과하여 보급률을 저해하고 있습니다. 공급자와 제조사 간의 가치 기반 계약이 진화하고 있지만, 여전히 소수의 고소득 환경에 국한되어 있어 경제성 격차가 지속되고 있습니다.

부문 분석

뇌심부 자극 장치는 파킨슨병, 본태성 진전, 근긴장 이상증에 대한 30년간의 임상적 근거를 바탕으로 2024년 뇌 임플란트 시장 점유율의 압도적인 42.52%를 차지했습니다. 전 세계적으로 16만 건 이상의 이식이 이루어져 외과의 및 보험사 사이에서 타의 추종을 불허하는 시술 친숙도를 확보했습니다. 강박 장애와 같은 새로운 적응증이 중추적 임상시험을 통과함에 따라 글로벌 성장세는 건실하게 유지되고 있습니다. 한편, 척수 자극 장치는 만성 통증 및 당뇨병성 신경병증 사례 전반에 걸쳐 견실한 판매량을 유지하며 기존 업체들의 수익원을 더욱 다각화하고 있습니다.

미주신경 자극 장치는 2030년까지 연평균 11.71%의 성장률을 기록하며 가장 빠르게 성장하는 기회로 부상하고 있습니다. 약물 내성 간질, 치료 저항성 우울증, 염증성 질환에 대한 다각적 효용성이 다학제적 도입을 촉진하고 있습니다. 기술 선도 기업들은 펄스 발생기를 소형화하고 전극의 내구성을 개선하여 수술 시간을 단축하고 재수술 횟수를 줄이고 있습니다. 전반적으로 뇌 임플란트 시장은 제품 혁신이 주도하는 양상을 유지하며, 폐쇄형 DBS 시스템과 발작 반응형 신경자극 장치가 적용 사례를 확대하는 동시에 안정적인 평균판매가격(ASP)을 뒷받침하고 있습니다.

정밀한 전극 위치 설정과 높은 보험 적용률 덕분에 2024년 뇌 임플란트 시장에서 침습적 정위 수술은 여전히 71.46%의 점유율을 차지하고 있습니다. 2025년 코호트를 대상으로 한 메타분석에 따르면 뇌혈관 사건 발생률은 2.71%, 영구적 장애는 1.0%, 사망률은 0.4%로 나타나 외과 의사와 규제 기관 모두를 안심시키는 수치입니다. 로봇 보조 내비게이션과 3-Tesla MRI 유도 기술의 동시 도입으로 합병증 발생률은 지속적으로 감소 추세를 보이고 있습니다.

그러나 Synchron의 혈관내 스텐트로드(Stentrode)와 같은 최소 침습적 접근법이 12.18%의 연평균 복합 성장률(CAGR)로 성장세를 보이고 있습니다. 경정맥을 통한 이식은 두개골 절개술을 없애고 시술 시간을 단축하며 외래 수술 센터로의 확장을 가능하게 합니다. 항염증제로 코팅된 유연한 폴리머 전극선은 이물질 반응을 줄이고, 단일 접근법으로의 전달은 감염 위험을 낮춥니다. 이러한 저침습 전략이 성숙해짐에 따라 대상 환자 풀이 확대되고 지역별 출시 속도가 빨라져 점진적인 물량 증가를 촉진하고 있습니다.

뇌 임플란트 시장 보고서는 제품 유형별(뇌심부 자극 장치, 척수 자극 장치, 미주신경 자극 장치), 기술별(침습성, 저침습성, 비침습성), 용도별(파킨슨병, 만성 통증, 간질, 기타), 최종 사용자별(병원 및 뇌신경외과센터, 전문클리닉, 기타), 지역별(북미)

지역별 분석

북미는 FDA 신속 심사 절차, 풍부한 자본 풀, 다중 적응증에 대한 확고한 보험 적용 범위 덕분에 글로벌 매출의 53.18%를 차지하며 선두를 유지하고 있습니다. 미국 병원들은 펠로우십 훈련을 받은 기능적 신경외과 전문의의 높은 집중도와 Neuralink, Precision Neuroscience, Synchron이 주도하는 신생 기업 생태계의 번성으로 혜택을 받고 있습니다. 캐나다는 파킨슨병과 본태성 진전에 대해 DBS를 의학적으로 필요한 치료로 인정하는 보편적 건강보험을 통해 지역 총량을 확대합니다.

유럽은 혁신적인 임플란트 시술을 신속하게 진행하는 조정된 HTA 프로세스와 EU 의료기기 규정(MDR) 가속화 심사 트랙을 바탕으로 근접한 추세를 보입니다. 독일, 프랑스, 영국은 다수의 DBS 우수 센터를 공동 운영하며 대규모 VNS(부교감신경자극술) 및 RNS(재발성 신경자극술) 보험 적용 시범 사업을 지속하고 있습니다. 북유럽 국가들은 원격 DBS 프로그래밍을 지원하는 디지털 헬스 프레임워크를 활용해 효율적인 장거리 진료 모델을 입증하고 있습니다.

아시아태평양 지역은 12.67%의 연평균 복합 성장률(CAGR) 전망으로 가장 역동적인 시장으로 부상하고 있습니다. 중국은 신경과학 연구개발과 고급 의료기기 제조에 막대한 투자를 진행하며 서구 국가와의 기술 격차를 좁혀가고 있습니다. 일본의 고령화 인구는 운동장애 치료 솔루션에 대한 수요를 촉진하며, 국민건강보험제도는 환자 접근성을 높입니다. 인도, 한국, 호주는 공공-민간 협력과 선도적 학술 연구를 결합해 임상시험 수행률을 높이며 지역 성장을 주도합니다. 중동 및 아프리카와 남미는 아직 초기 단계이지만 유망한 시장입니다. GCC 국가들은 국가 보건 혁신 의제의 일환으로 신경외과 중심 허브를 지원하고 있으며, 브라질과 아르헨티나는 거시경제적 변동성 속에서도 표적 보상 시범 사업을 추진 중입니다. 장기적 성장 가능성은 전문의 양성 확대, 통화 위험 안정화, 농촌 지역 원격 의료 프로그램 인프라 확장에 달려 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 및 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신경 퇴행성 질환과 운동 장애의 유병률 상승

- 소형화와 폐쇄 루프 기술 발전

- 미국/EU에서 유리한 보험 적용 확대

- AI 기반 적응형 자극 알고리즘(보고 부족)

- FDA 혁신적 치료법 지정 및 EU 의료기기 규정 신속 심사 절차(보고 부족)

- 신경기술 분야 대규모 자금 조달 및 벤처 캐피털 활동 급증

- 시장 성장 억제요인

- 고가 장비와 수술 비용

- 일부 적응증에서 제한된 장기 임상 증거

- 사이버 보안 및 데이터 개인정보 보호 우려(보고 부족)

- 신흥 시장에서의 뇌신경외과 전문의 부족(과소보고)

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌의 격렬함

제5장 시장 규모와 성장 예측

- 제품 유형별

- 뇌심부 자극 장치

- 척수 자극 장치

- 미주신경 자극 장치

- 기술별

- 침습성(외과 수술)

- 저침습성/경피적

- 비침습성(경두개)

- 용도별

- 파킨슨병

- 만성 통증

- 간질

- 우울증 및 정신질환

- 본태성 진전

- 기타 용도

- 최종 사용자별

- 병원 및 뇌신경외과 센터

- 전문 클리닉

- 외래수술센터(ASC)

- 학술기관 및 연구기관

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Abbott

- Boston Scientific Corporation

- Medtronic

- LivaNova PLC

- NeuroPace, Inc.

- Aleva Neurotherapeutics

- Newronika SpA

- Saluda Medical Pty Ltd.

- Renishaw plc.

- Paradromics

- MicroTransponder, Inc.

- Synchron

- Blackrock Neurotech

- Precision Neuroscience Corporation

- Synergia Medical

제7장 시장 기회와 장래의 전망

HBR 25.11.17The brain implants market size stands at USD 3.13 billion in 2025 and is projected to expand to USD 5.17 billion by 2030 at a robust 10.53% CAGR, underscoring sustained investment momentum and rapid regulatory clearances that shorten time-to-therapy for patients worldwide.

Broader payer acceptance, sensor miniaturization, and AI-enabled closed-loop systems are collectively redefining neuro-intervention strategies, creating new avenues for deep brain stimulation (DBS), vagus nerve stimulation (VNS), and emerging brain-computer interface (BCI) solutions. Players are aggressively integrating graphene electrodes and biocompatible coatings to extend device longevity, while flexible microelectrode arrays reduce tissue trauma and accelerate post-operative recovery. Venture capital inflows-led by nine-figure rounds such as Blackrock Neurotech's USD 200 million raise-validate commercial readiness across several therapeutic categories.Meanwhile, FDA Breakthrough Device and EU MDR fast-track pathways continue to compress approval timelines for next-generation neural technologies and cement North America's leadership position even as Asia-Pacific accelerates system-wide adoption.

Global Brain Implants Market Trends and Insights

Rising Prevalence of Neuro-degenerative & Movement Disorders

Global Parkinson's disease cases are on track to hit 25.2 million by 2050, doubling today's burden and widening the pool of DBS candidates. Drug-resistant epilepsy already affects 10.1 million people who remain eligible for surgical intervention, while treatment-resistant depression continues to drive psychiatric device adoption. Aging demographics in developed markets and improved diagnostic resources in emerging economies combine to ensure consistent procedure volumes. Health-economic studies showed 2024 DBS procedures saving USD 20,000-35,000 per patient annually in medication costs, keeping total expenditures below commonly accepted cost-effectiveness thresholds.

Miniaturization & Closed-loop Technology Advances

Graphene electrodes and nanoporous metals have shrunk implant footprints by up to 70%, improving signal fidelity and lowering post-surgical inflammation. Batteries now last longer thanks to neuromorphic processors that cut power draw, with rechargeable platforms such as Abbott's Infinity DBS allowing smartphone-based parameter updates. On-device machine-learning firmware adjusts stimulation in real time, moving therapy from static settings to dynamic, patient-specific protocols. These advances collectively accelerate outpatient recovery, lift long-term efficacy, and fuel wider physician acceptance.

High Device & Surgical Procedure Cost

A full DBS episode, including hardware, surgery, and year-one programming, ranges from USD 140,000 to 190,000, with follow-up maintenance at USD 4,500-7,800 per year. In many emerging countries these fees outstrip annual household income, curbing penetration. Value-based contracting between providers and manufacturers is evolving, yet remains confined to a handful of high-income settings, prolonging the affordability gap.

Other drivers and restraints analyzed in the detailed report include:

- Favorable Reimbursement Expansion in U.S./EU

- AI-driven Adaptive Stimulation Algorithms

- Cybersecurity & Data-privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Deep brain stimulators held a commanding 42.52% of brain implants market share in 2024, anchored by three-decade clinical evidence for Parkinson's, essential tremor, and dystonia. More than 160,000 implants have been placed worldwide, giving the modality unrivalled procedural familiarity among surgeons and payers. Global growth remains healthy as new indications such as obsessive-compulsive disorder move past pivotal trials. Meanwhile, spinal cord stimulators maintain solid volumes across chronic pain and diabetic neuropathy cases, further diversifying revenue streams for incumbents.

Vagus nerve stimulators represent the fastest-moving opportunity, charting an 11.71% CAGR through 2030. Multipronged utility in drug-resistant epilepsy, treatment-resistant depression, and inflammatory disorders boosts cross-specialty adoption. Technology front-runners are miniaturising pulse generators and improving lead durability, allowing shorter operating times and fewer revision surgeries. Overall, the brain implants market remains product-innovation led, with closed-loop DBS systems and seizure-responsive neurostimulators expanding use cases while supporting stable ASPs.

Invasive stereotactic surgery continues to account for a 71.46% foothold within the brain implants market in 2024 thanks to precise electrode positioning and well-reimbursed care pathways. Meta-analyses covering 2025 cohorts document cerebrovascular events at 2.71%, permanent impairment at 1.0%, and mortality at 0.4%, numbers that reassure surgeons and regulators alike. Concurrent adoption of robot-assisted navigation and 3-Tesla MRI guidance keeps complication rates on a downward trajectory.

Yet, minimally-invasive approaches such as Synchron's endovascular Stentrode are gaining momentum with a forecast 12.18% CAGR. Implantation via the jugular vein eliminates craniotomy, cuts procedure time, and may allow expansion into ambulatory surgical centers. Flexible polymer leads coated with anti-inflammatory agents reduce foreign-body responses, while single-access delivery lowers infection risks. As these less-invasive strategies mature, they broaden candidate pools and speed geographic roll-outs, propelling incremental volume growth.

The Brain Implants Market Report is Segmented by Product Type (Deep Brain Stimulators, Spinal Cord Stimulators, Vagus Nerve Stimulators), by Technology (Invasive, Minimally-Invasive, Non-Invasive), by Application (Parkinson's Disease, Chronic Pain, Epilepsy, and More), by End User (Hospitals & Neurosurgical Centers, Specialty Clinics, and More), by Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America retains primacy, contributing 53.18% of global revenue, anchored by FDA fast-track pathways, deep capital pools, and entrenched reimbursement coverage for multiple indications. U.S. hospitals also benefit from a dense concentration of fellowship-trained functional neurosurgeons and a flourishing start-up ecosystem led by Neuralink, Precision Neuroscience, and Synchron. Canada amplifies regional totals through universal health insurance that recognises DBS as medically necessary for Parkinson's and essential tremor.

Europe follows closely, underpinned by coordinated HTA processes and EU MDR accelerated review tracks that expedite innovative implants. Germany, France, and the United Kingdom collectively host scores of DBS centers of excellence and continue to pilot large-scale VNS and RNS reimbursements. Nordic countries leverage digital health frameworks to support remote DBS programming, demonstrating efficient long-distance care models.

Asia-Pacific emerges as the most dynamic corridor with a 12.67% CAGR outlook. China invests heavily in neuroscience R&D and high-end device manufacturing, narrowing technology gaps with Western peers. Japan's aging population fuels strong demand for movement-disorder solutions, while the nation's universal insurance simplifies patient uptake. India, South Korea, and Australia round out regional growth by combining public-private partnerships with leading academic research to spur clinical trial throughput. The Middle East & Africa and South America remain nascent yet promising. GCC states back flagship neurosurgical hubs as part of national health-innovation agendas, while Brazil and Argentina push forward targeted reimbursement pilots despite macroeconomic volatility. Long-term upside hinges on scaling specialist training, stabilizing currency risk, and expanding tele-programming infrastructure in rural locales.

- Abbott Laboratories

- Boston Scientific

- Medtronic

- LivaNova

- NeuroPace

- Aleva Neurotherapeutics

- Newronika S.p.A.

- Saluda Medical

- Renishaw

- Paradromics

- MicroTransponder, Inc.

- Synchron

- Blackrock Neurotech

- Precision Neuroscience Corporation

- Synergia Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of neuro-degenerative & movement disorders

- 4.2.2 Miniaturization & closed-loop technology advances

- 4.2.3 Favorable reimbursement expansion in U.S./EU

- 4.2.4 AI-driven adaptive stimulation algorithms (under-reported)

- 4.2.5 FDA Breakthrough & EU MDR fast-track pathways (under-reported)

- 4.2.6 Surge in neurotech mega-funding & VC activity

- 4.3 Market Restraints

- 4.3.1 High device & surgical procedure cost

- 4.3.2 Limited long-term clinical evidence in some indications

- 4.3.3 Cyber-security & data-privacy concerns (under-reported)

- 4.3.4 Scarcity of specialist neurosurgeons in emerging markets (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Deep Brain Stimulators

- 5.1.2 Spinal Cord Stimulators

- 5.1.3 Vagus Nerve Stimulators

- 5.2 By Technology

- 5.2.1 Invasive (Surgical)

- 5.2.2 Minimally-Invasive / Percutaneous

- 5.2.3 Non-invasive (Trans-cranial)

- 5.3 By Application

- 5.3.1 Parkinson's Disease

- 5.3.2 Chronic Pain

- 5.3.3 Epilepsy

- 5.3.4 Depression & Psychiatric Disorders

- 5.3.5 Essential Tremor

- 5.3.6 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals & Neurosurgical Centers

- 5.4.2 Specialty Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Academic & Research Institutes

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of APAC

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, ... Recent Developments)

- 6.4.1 Abbott

- 6.4.2 Boston Scientific Corporation

- 6.4.3 Medtronic

- 6.4.4 LivaNova PLC

- 6.4.5 NeuroPace, Inc.

- 6.4.6 Aleva Neurotherapeutics

- 6.4.7 Newronika S.p.A.

- 6.4.8 Saluda Medical Pty Ltd.

- 6.4.9 Renishaw plc.

- 6.4.10 Paradromics

- 6.4.11 MicroTransponder, Inc.

- 6.4.12 Synchron

- 6.4.13 Blackrock Neurotech

- 6.4.14 Precision Neuroscience Corporation

- 6.4.15 Synergia Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment