|

시장보고서

상품코드

1851725

신속 진단 키트 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Rapid Diagnostic Kits - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

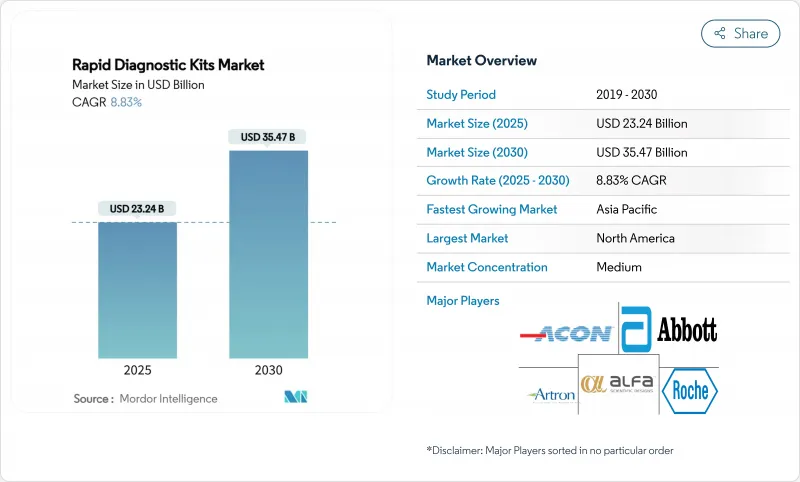

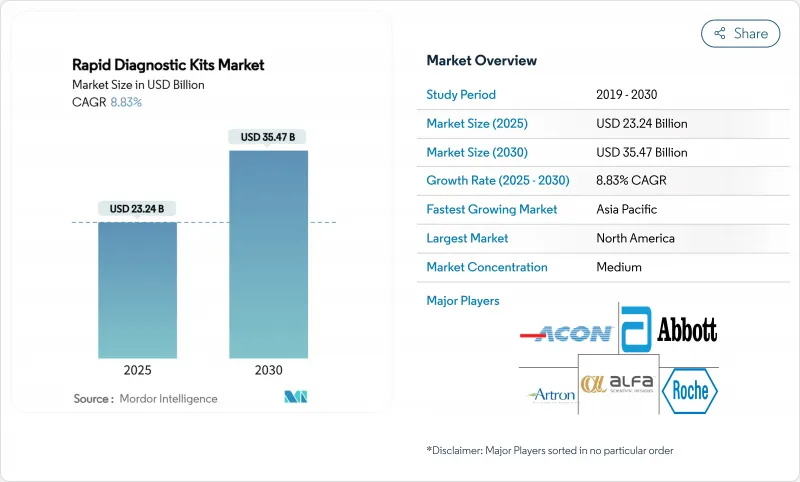

신속 진단 키트 시장 규모는 2025년에 232억 4,000만 달러로 평가되었고 예측 기간(2025-2030년)의 CAGR은 8.83%를 나타낼 것으로 예측되며 2030년에는 354억 7,000만 달러에 달할 전망입니다.

확장은 현장진단(POCT) 채택 증가, 병원 예산 긴축, 그리고 일시적 치료에서 예방 치료로의 글로벌 전환을 반영합니다. 다중 감지을 가능하게 하는 기술 업그레이드와 만성 질환 모니터링에 대한 지원적 보험 적용은 급성 팬데믹 물결 이후에도 수요를 높게 유지합니다. 제조사들은 연구개발(R&D) 위험을 줄여주는 정부 자금 지원의 혜택을 받는 한편, 고령화 인구는 일차 진료 및 가정 간호 환경 전반에 걸쳐 검사량을 증가시킵니다. 현재 경쟁 전략은 규모 확대, 수직적 통합, 데이터 연결성에 집중되고 있습니다. 병원과 소비자 모두 전자건강기록(EHR)과의 원활한 연동을 기대하기 때문입니다.

세계의 신속 진단 키트 시장 동향 및 인사이트

다중 호흡기 패널에 대한 정부 자금 지원 급증

공공 기관들은 SARS-CoV-2, 인플루엔자 A/B, RSV를 하나의 카트리지로 검사하는 다중 호흡기 패널에 대한 자금 지원을 지속하며, 공급업체들에게 확고한 다년간 주문량을 보장하고 있습니다. BARDA의 지출은 프로토타입에서 시장 출시까지의 기간을 단축시켰으며, 2024년 5월 승인된 로슈의 20분 소요 cobas liat 트리플 검사가 그 대표적인 사례입니다. 병원들은 증후군 모델을 채택하고 있습니다. 단일 면봉 채취로 검체 처리 절차가 간소화되고 격리 결정 시간이 단축되며 개인 보호 장비(PPE)를 절약할 수 있기 때문입니다. 실험실은 운영 비용을 절감하고, 제조사들은 추가 플랫폼 소형화를 정당화할 수 있는 물량 확보를 보장받는다. 이 모델은 이제 신종 병원체 패널로 확장되며 신속 진단 키트 시장 범위를 넓히고 분자 진단 공급업체의 수익 기반을 공고히 하고 있습니다.

만성 질환 자가 검사의 소비자 채택 증가

자가 검사는 임신 키트를 넘어 심혈관 대사 질환 및 감염성 질환 모니터링으로 확대되었습니다. FDA가 승인한 최초의 세균성 성병(STI) 자가 혈액 검사 키트인 랩코프의 ‘퍼스트 투 노우(First-to-Know)’ 매독 키트는 가정 내 모세혈관 채혈에 대한 소비자 수용성을 입증했습니다. 의료진에게 결과를 제공하는 디지털 헬스 플랫폼은 병원 방문을 줄이고 실험실 지연 없이 약물 용량 조절을 가능하게 합니다. 직접 결제 키트가 반복적인 채혈 관련 청구 건수를 감소시키므로 보험사도 이익을 얻습니다. 당뇨병 전단계 디지털 감지에 관한 규제 초안 지침은 비침습적 검진에 대한 공식적 지지를 강조하며, 공급업체들은 즉각적인 데이터 업로드를 위해 블루투스 또는 NFC 연결 기능을 탑재해 대응하고 있습니다. 이러한 행동 변화는 신속 진단 키트 시장에서 가정 관리가 가장 빠르게 성장하는 최종 사용자 채널임을 확고히 합니다.

중요 시약 공급망 취약점

특수 항체, 효소, 완충액은 주로 동아시아의 단일 시설 클러스터에서 생산됩니다. 무역 마찰이나 팬데믹은 수출을 급속히 중단시켜 배분 프로토콜을 강제하며, 이는 배송 기간을 연장하고 비용을 증가시킵니다. 코로나19 사태는 효소 부족으로 PCR 키트 생산이 제한되면서 이러한 병목 현상을 드러냈습니다. 제조사들은 이제 이중 공급원 확보나 시약 생산 내재화를 추진 중이지만, 자본 지출로 인해 투자 회수 기간이 길어지고 중소 기업들은 압박을 받고 있습니다. 특히 재고 완충 장치가 부족한 저소득 지역에서는 공공 클리닉의 필수 진단 키트 공급이 중단될 수 있어, 중복 계획이 성숙할 때까지 신속 진단 키트 시장 성장이 제약을 받을 전망입니다.

부문 분석

측류 면역분석법(Lateral flow immunoassay)은 성숙한 공급망, 낮은 단위 비용, 팬데믹 급증 시 신속한 확장 능력에 힘입어 2024년 신속 진단 키트 시장에서 42.76%의 매출로 가장 큰 비중을 차지했습니다. 이 부문은 상온에서 작동 가능하고 최소한의 훈련만 필요로 하기 때문에 자원 제한이 있는 진료소, 인도주의적 임무, 대규모 검진 프로그램에서 계속해서 성장하고 있습니다. 나노입자 표지 및 개선된 막 투과성과 같은 기술 발전은 분석 감도를 높여 실험실 기준이 높아지는 상황에서도 측면 유동 방식이 시장 점유율을 유지할 수 있게 합니다. 면역크로마토그래피는 규모는 작지만, 의사의 반정량적 결과물에 대한 수요 증가와 풍부한 데이터 계층을 제공하는 AI 지원 판독기의 등장으로 9.17%라는 가장 빠른 연평균 성장률(CAGR)을 기록하고 있습니다. 마이크로리터 단위의 정밀도가 요구되는 내분비학 및 신생아 선별 검사 분야에서 마이크로플루이딕 랩온칩 시스템이 점진적으로 진전 중입니다. 등온 증폭 또는 CRISPR 편집 기술을 활용한 분자 신속 검사는 호흡기 및 위장관 표적 검사를 통합한 증후군 패널을 활용해 두 자릿수 성장을 기록 중입니다. 생체 센서 플랫폼은 전기화학적 감지을 통해 연속적인 혈당 또는 심장 바이오마커 추이를 포착함으로써 신속 진단 키트 시장 전체를 확장하고 있습니다.

측류 카트리지와 통합 핵산 포집 모듈을 결합한 복합 시스템의 꾸준한 파이프라인이 구축 중입니다. 이러한 하이브리드 제품은 시약 사용량 감소, 단일 스트립 내 3중 표적 감지, 클라우드 대시보드와 연동되는 스마트폰 판독 기능을 약속합니다. FDA의 2025년 1월 신종 병원체 패널 검증 가이드라인은 이러한 설계의 승인을 가속화할 전망입니다. 병원들이 공급업체를 합리화함에 따라 기술 차별화는 이제 감지 화학에만 의존하기보다 처리량, 검체 유형의 다양성, 내장형 연결성에 달려 있습니다. 독점 시약과 개방형 분석 소프트웨어를 결합한 제조사들은 신속 진단 키트 시장에서 견고한 입지를 구축하고 있습니다.

감염성 질환은 지속적인 인플루엔자, RSV, 항생제 내성 감시 덕분에 2024년 매출의 36.03%를 차지했습니다. 그러나 정책 입안자들이 치료 비용 절감을 위해 조기 검진을 지원함에 따라 종양 표지자가 9.46%의 연평균 성장률(CAGR)로 가장 빠르게 발전하고 있습니다. 현장진단용 분변면역염색(FIT) 검사, 메틸화 DNA용 액체 생검 카트리지, VolitionRx의 패혈증 지표와 같은 뉴클레오좀 분석법이 종양학 분야를 주목받게 합니다. 고혈압 및 당뇨병 관리가 약국과 가정으로 이동함에 따라 심혈관-대사 모니터링이 성장합니다. 임신·생식력 검사 키트는 후기 임신과 원격 생식 서비스 확대로 기준 판매량을 유지합니다. 독성학·약물 남용 패널은 변화하는 오피오이드 정책과 다가오는 연방 직장 규정 개정에 발맞춰 진화 중입니다./p>

현재 규모는 작지만, 동물과 인간 질병 감시를 통합하는 원헬스(One Health) 프레임워크의 혜택을 받는 수의학 및 인수공통병 검진 시장이 성장 중입니다. 저소득 및 중간소득 국가(LMICs)의 감염병 검사용 신속 진단 키트 시장 규모는 다자간 보조금으로 뒷받침되며, 종양학 중심 스타트업들은 후생유전학적 표적 정밀화를 위해 벤처 캐피털을 확보하고 있습니다. 이러한 응용 분야 다각화는 공급업체들이 주기적 수요 변동에 대비할 수 있게 하며, 다목적 플랫폼이 부문 간 수익 창출을 가능케 합니다.

지역 분석

북미는 유리한 보험급여 코드, 높은 디지털 리터러시, 지속적인 혁신을 주도하는 BARDA 파이프라인의 지원으로 2024년 매출의 38.17%를 유지했습니다. 미국이 대부분을 차지하며, 로슈의 20분 성병 검사(STI)에 대한 CLIA 면제 조치로 12,000개 소매 클리닉에 광범위하게 도입되고 있습니다. 캐나다는 원주민 커뮤니티를 위한 국가 입찰 프로그램을 통해 일차 진료 도구 키트에 HIV 및 C형 간염 카트리지를 추가했습니다. 이 지역은 또한 전자 건강 기록과 통합되는 AI 판독기 시범 운영을 선도하며 신속 진단 키트 시장 내 초기 도입자에게 선점 우위를 창출하고 있습니다.

아시아태평양 지역은 공공 보험 확대와 국내 IVD 생산에 대한 정부 인센티브로 인해 가장 강력한 11.15% CAGR을 기록했습니다. 중국의 자립 추진으로 현지 공급업체들이 수입품 가격을 밑도는 시약 역설계에 나서고 있으며, 2선 도시 병원들은 새로운 호흡기 감시 의무를 충족하기 위해 휴대용 PCR 분석기를 조달 중입니다. 인도는 '아유슈만 바라트 디지털 미션'을 통해 원격의료를 확대하며 지역사회 보건 요원 키트에 신속 대사 패널을 포함시켰다. 동남아시아 보건부들은 몬순 시즌에 뎅기열-코로나 복합 카트리지를 전개하고, 일본 노인병원은 타액 기반 치매 바이오마커 시범 운영을 진행 중입니다. 이 지역의 이질성은 다양한 수요 패턴을 이끌지만, 유지보수가 적고 클라우드 연결이 가능한 시스템에 대한 공통된 필요성으로 수렴됩니다.

유럽은 국경을 넘나드는 기기 수용을 보장하는 조화된 IVDR 규정 덕분에 꾸준한 한 자릿수 중반 성장을 유지하고 있습니다. 독일은 요양원에 인공지능 지원 측면 유동 플랫폼을 지원하며, 프랑스는 심장내과 대기 시간을 줄이기 위해 약국 기반 심혈관 대사 검진을 보조합니다. 중동 및 아프리카 지역은 석유 수출국들의 실험실 인프라 업그레이드로 결핵 및 원숭이두창 감지 입찰 활동이 가속화되고 있으나, 외딴 지역에서의 유통은 여전히 제약받고 있습니다. 라틴 아메리카는 뎅기열, 지카, 치쿤구니야를 구분하는 다중 검사를 통해 아르보바이러스 동시 유행을 대응 중입니다. 글로벌 펀드와 같은 지역 간 기부 프로그램은 수요를 집약하고 통화 변동성을 완화하여 신흥 지역 전반에 걸쳐 신속 진단 키트 시장 규모를 안정화시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 다중 호흡기 패널에 대한 정부 자금 지원 급증

- 만성 질환 자가 검진 소비자 채택 증가

- 저소득 및 중간소득 국가(LMICs)에서의 분산형 분자 현장진단(PoC) 플랫폼 확대

- AI 기반 판독기 통합으로 향상된 검사 정확도

- CRISPR을 이용한 초고속 분석 등장

- 질병에 대한 의식의 고조가 검진 수요를 촉진

- 시장 성장 억제요인

- 중요 시약공급 체인 취약성

- 가정용 다중 검사 키트 규제 불확실성

- 판독기 장치 데이터 개인정보 보호 문제

- 일회용 플라스틱에 대한 지속 가능성 압박

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(단위 : 달러)

- 기술별

- 측면 유동 면역 분석법

- 마이크로플루이딕스 랩온칩

- 면역 크로마토그래피

- 응집 & 라텍스 검사

- 바이오센서 기반 신속검사

- 분자 신속검사

- 용도별

- 감염증

- 심장 대사 모니터링

- 임신과 불임

- 독물학과 남용 약물

- 종양 마커

- 수의학 및 인수 공통 감염증 스크리닝

- 샘플 유형별

- 혈액

- 비강

- 소변

- 타액

- 대변

- 최종 사용자별

- 병원&클리닉

- 의사 사무실 & 긴급 의료

- 홈케어

- 진단 실험실

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- F. Hoffmann-La Roche AG

- Danaher Corp.(Cepheid)

- Becton, Dickinson & Co.

- bioMerieux SA

- Siemens Healthineers

- QuidelOrtho Corp.

- Thermo Fisher Scientific

- Qiagen NV

- Hologic Inc.

- SD Biosensor Inc.

- OraSure Technologies Inc.

- Access Bio Inc.

- Alfa Scientific Designs Inc.

- ACON Laboratories Inc.

- BTNX Inc.

- Artron Laboratories Inc.

- LumiraDx Ltd.

- Bio-Rad Laboratories Inc.

- DiaSorin(Luminex)

- SureScreen Diagnostics

- Creative Diagnostics

- Biopanda Reagents

제7장 시장 기회와 장래의 전망

HBR 25.11.17The Rapid Diagnostic Kits Market size is estimated at USD 23.24 billion in 2025, and is expected to reach USD 35.47 billion by 2030, at a CAGR of 8.83% during the forecast period (2025-2030).

The expansion reflects rising point-of-care adoption, tighter hospital budgets, and the global shift from episodic to preventive care. Technology upgrades that allow multiplex detection, alongside supportive reimbursement for chronic disease monitoring, keep demand elevated even after the acute pandemic wave. Manufacturers benefit from government funding that de-risks R&D, while ageing populations increase test volumes across primary and home-care settings. Competitive strategies now focus on scale, vertical integration, and data connectivity as hospitals and consumers both expect seamless integration with electronic health records.

Global Rapid Diagnostic Kits Market Trends and Insights

Government Funding Surge for Multiplex Respiratory Panels

Public agencies continue to bankroll multiplex respiratory panels that test for SARS-CoV-2, influenza A/B, and RSV in one cartridge, giving suppliers firm multiyear order books. BARDA's outlays have accelerated prototype-to-market timelines, exemplified by Roche's 20-minute cobas liat triple assay cleared in May 2024. Hospitals embrace the syndromic model because a single swab trims sample handling, shortens isolation decisions, and conserves personal protective equipment. Laboratories capture operational savings, while manufacturers secure volume commitments that justify further platform miniaturization. The model is now migrating to emerging pathogen panels, widening the rapid diagnostics kits market scope and solidifying a revenue floor for molecular suppliers.

Rising Consumer Adoption of Self-Testing for Chronic Diseases

Self-testing has moved beyond pregnancy kits into cardiometabolic and infectious disease monitoring. Labcorp's First-to-Know syphilis kit, the first FDA-authorized over-the-counter blood test for a bacterial STI, validated consumer readiness for capillary sampling at home. Digital health platforms that curate results for care teams reduce clinic visits and enable medication titration without laboratory delays. Payers also gain, as direct-pay kits lower claims associated with repeated phlebotomy. Regulatory draft guidance on digital detection of prediabetes underscores official support for non-invasive screening, and suppliers respond by embedding Bluetooth or NFC connectivity for instant data upload. The behavioural shift cements home-care as the fastest end-user channel in the rapid diagnostics kits market.

Supply-Chain Fragility for Critical Reagents

Specialized antibodies, enzymes, and buffers are often produced in single-facility clusters across East Asia. Trade friction or pandemics quickly halt exports, forcing allocation protocols that lengthen delivery times and inflate costs. The COVID-19 crisis exposed these choke points when enzyme shortages limited PCR kit output. Manufacturers now dual-source or internalize reagent production, but capital outlays lengthen payback horizons and squeeze smaller firms. Disruptions can starve public clinics of essential diagnostics, especially in low-income regions that lack inventory buffers, restraining the rapid diagnostics kits market until redundancy plans mature.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Decentralized Molecular PoC Platforms in LMICs

- Integration of AI-Enabled Readers Improving Test Accuracy

- Regulatory Uncertainty for Home-Use Multiplex Kits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lateral flow immunoassay generated the largest slice of the rapid diagnostics kits market in 2024 with 42.76% revenue, underpinned by mature supply chains, low unit costs, and the ability to scale quickly during pandemic surges. The segment continues to thrive in resource-limited clinics, humanitarian missions, and mass-screening programs because it tolerates ambient temperatures and requires minimal training. Advances such as nanoparticle labels and improved membrane porosity are lifting analytical sensitivity, allowing lateral flow to defend share even as laboratory expectations rise. Immuno-chromatography, though smaller, logs the fastest 9.17% CAGR, fueled by growing physician demand for semi-quantitative output and by AI-assisted readers that unlock richer data layers. Microfluidic lab-on-chip systems inch forward in endocrinology and neonatal screening where microlitre volumes and high precision matter. Molecular rapid assays employing isothermal amplification or CRISPR editing record double-digit growth, capitalizing on syndromic panels that bundle respiratory and gastrointestinal targets. Biosensor platforms leverage electrochemical detection to capture continuous glucose or cardiac biomarker trends, expanding the total addressable rapid diagnostics kits market.

A steady pipeline of combination systems blends lateral flow cartridges with integrated nucleic-acid capture modules. Such hybrids promise lower reagent use, three-target detection in one strip, and smartphone readouts that sync to cloud dashboards. FDA's January 2025 validation guidance for emerging pathogen panels accelerates clearance of these designs. As hospitals rationalize suppliers, technology differentiation now hinges on throughput, sample type versatility, and embedded connectivity rather than solely on detection chemistry. Manufacturers that pair proprietary reagents with open-analytics software carve durable footholds within the rapid diagnostics kits market.

Infectious diseases contributed 36.03% of 2024 revenue, buoyed by perpetual influenza, RSV, and antimicrobial resistance surveillance. Yet oncology markers is advancing fastest at a 9.46% CAGR because policy makers back early detection to curb treatment costs. Point-of-care FIT tests, liquid biopsy cartridges for methylated DNA, and nucleosome assays such as VolitionRx's sepsis indicator keep oncology in the spotlight. Cardio-metabolic Monitoring gains as hypertension and diabetes management migrate to pharmacies and homes. Pregnancy & Fertility kits sustain baseline volume, expanded by later-life pregnancies and tele-reproductive services. Toxicology & Drugs-of-Abuse panels evolve in step with shifting opioid policies and upcoming federal workplace rule revisions.

Veterinary & zoonotic screening, though small today, benefits from One Health frameworks that integrate animal and human disease vigilance. The overall rapid diagnostics kits market size for infectious disease testing in LMICs is buttressed by multilateral grants, while oncology-focused start-ups secure venture capital to refine epigenetic targets. Application diversification thus cushions suppliers against cyclical demand swings and positions multipurpose platforms for cross-sector revenue.

The Rapid Diagnostics Kits Market Report is Segmented by Technology (Lateral Flow Immunoassay, Microfluidic Lab-On-Chip, and More), Application (Infectious Diseases, Cardio-Metabolic Monitoring, and More), Sample Type (Blood, Nasal, and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.17% of 2024 revenue, aided by favorable reimbursement codes, high digital literacy, and the BARDA pipeline that continuously seeds innovation. The United States accounts for a majority share, where CLIA waivers for Roche's 20-minute STI assays open wide deployment across 12,000 retail clinics. Canada follows through national tender programs for First Nations communities, adding HIV and hepatitis-C cartridges to primary-care tool kits. The region also leads in AI-reader pilots that integrate with electronic health records, creating first-mover advantages for early adopters within the rapid diagnostics kits market.

Asia-Pacific records the strongest 11.15% CAGR, spurred by public insurance expansion and government incentives for domestic IVD production. China's push for self-reliance lifted local suppliers who reverse-engineer reagents to undercut imports, while tier-2 city hospitals procure portable PCR analyzers to meet new respiratory surveillance mandates. India scales telemedicine through its Ayushman Bharat Digital Mission, embedding rapid metabolic panels into community health worker kits. Southeast Asian ministries deploy combination dengue-COVID cartridges during monsoon seasons, and Japanese geriatric clinics pilot saliva-based dementia biomarkers. The region's heterogeneity drives diverse demand patterns yet converges on a common need for low-maintenance, cloud-connected systems.

Europe sustains steady mid-single-digit growth undergirded by harmonized IVDR rules that assure cross-border device acceptance. Germany finances AI-assisted lateral flow platforms in nursing homes, while France subsidizes pharmacy-based cardiometabolic screens to shorten cardiologist queues. The Middle East & Africa sees accelerated tender activity for tuberculosis and mpox detection as petro-states upgrade lab infrastructure, though distribution remains hampered in remote zones. Latin America tackles arbovirus co-circulation with multiplex assays that differentiate dengue, Zika, and chikungunya. Cross-regional donor programs, such as the Global Fund, aggregate demand and smooth currency volatility, anchoring the rapid diagnostics kits market size across emerging geographies.

- Abbott Laboratories

- Roche

- Danaher Corp. (Cepheid)

- Beckton Dickinson

- bioMerieux

- Siemens Healthineers

- QuidelOrtho Corp.

- Thermo Fisher Scientific

- QIAGEN

- Hologic

- SD Biosensor Inc.

- Orasure Technologies

- Access Bio

- Alfa Scientific Designs

- Acon Laboratories

- BTNX

- Artron Laboratories

- LumiraDx Ltd.

- Bio-Rad Laboratories

- DiaSorin (Luminex)

- SureScreen Diagnostics

- Creative Diagnostics

- Biopanda Reagents

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Funding Surge for Multiplex Respiratory Panels

- 4.2.2 Rising Consumer Adoption of Self-Testing for Chronic Diseases

- 4.2.3 Expansion of Decentralized Molecular PoC Platforms in LMICs

- 4.2.4 Integration of AI-Enabled Readers Improving Test Accuracy

- 4.2.5 Emergence of CRISPR-Based Ultra-Rapid Assays

- 4.2.6 Increasing Awareness of Diseases Driving Screening Demand

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Fragility for Critical Reagents

- 4.3.2 Regulatory Uncertainty for Home-Use Multiplex Kits

- 4.3.3 Reader-Device Data-Privacy Concerns

- 4.3.4 Sustainability Pressure on Single-Use Plastics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Technology

- 5.1.1 Lateral Flow Immunoassay

- 5.1.2 Microfluidic Lab-on-Chip

- 5.1.3 Immuno-chromatography

- 5.1.4 Agglutination & Latex Tests

- 5.1.5 Biosensor-Based Rapid Tests

- 5.1.6 Molecular Rapid Tests

- 5.2 By Application

- 5.2.1 Infectious Diseases

- 5.2.2 Cardio-metabolic Monitoring

- 5.2.3 Pregnancy & Fertility

- 5.2.4 Toxicology & Drugs-of-Abuse

- 5.2.5 Oncology Markers

- 5.2.6 Veterinary & Zoonotic Screening

- 5.3 By Sample Type

- 5.3.1 Blood

- 5.3.2 Nasal

- 5.3.3 Urine

- 5.3.4 Saliva

- 5.3.5 Stool

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Physician Offices & Urgent Care

- 5.4.3 Home-care Setting

- 5.4.4 Diagnostic Laboratories

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche AG

- 6.3.3 Danaher Corp. (Cepheid)

- 6.3.4 Becton, Dickinson & Co.

- 6.3.5 bioMerieux SA

- 6.3.6 Siemens Healthineers

- 6.3.7 QuidelOrtho Corp.

- 6.3.8 Thermo Fisher Scientific

- 6.3.9 Qiagen NV

- 6.3.10 Hologic Inc.

- 6.3.11 SD Biosensor Inc.

- 6.3.12 OraSure Technologies Inc.

- 6.3.13 Access Bio Inc.

- 6.3.14 Alfa Scientific Designs Inc.

- 6.3.15 ACON Laboratories Inc.

- 6.3.16 BTNX Inc.

- 6.3.17 Artron Laboratories Inc.

- 6.3.18 LumiraDx Ltd.

- 6.3.19 Bio-Rad Laboratories Inc.

- 6.3.20 DiaSorin (Luminex)

- 6.3.21 SureScreen Diagnostics

- 6.3.22 Creative Diagnostics

- 6.3.23 Biopanda Reagents

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment