|

시장보고서

상품코드

1851728

LED 드라이버 시장 : 시장 점유율 분석, 산업 동향 및 촉진요인, 성장 예측(2025-2030년)LED Driver - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

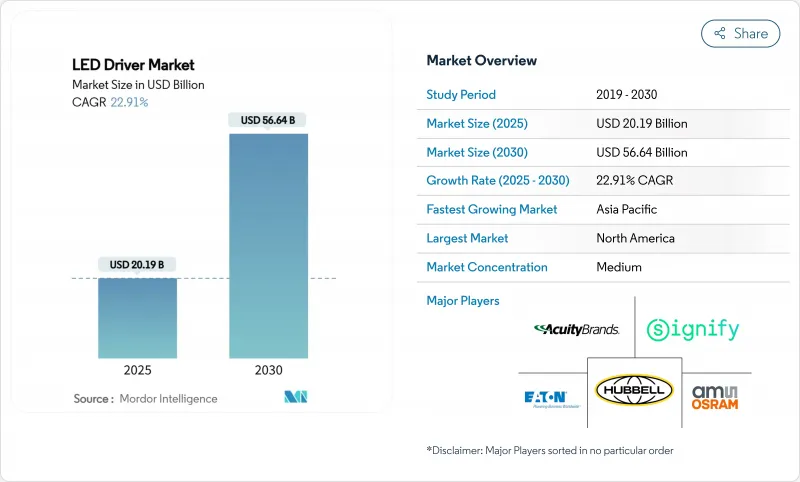

LED 드라이버 시장의 2025년 시장 규모는 201억 9,000만 달러로 추정되고, CAGR 22.91%로 성장할 전망이며, 2030년에는 566억 4,000만 달러로 성장할 것으로 예측되고 있습니다.

이 확대는 국가의 에너지 효율 지령의 조정, 무선 제어의 채용 가속, 변환 효율을 높이고 드라이버의 설치 면적을 축소하는 탄화규소 반도체와 질화갈륨 반도체의 전개에 지지되고 있습니다. 특히 아시아태평양에서는 정부가 자금을 제공하는 리노베이션 프로그램이 인터넷 제로 공약과 교차하여 대규모 교체 수요를 끌어올려 북미와 유럽에서는 신축 기준에 따라 지능형 조명의 통합 사양이 추진되고 있습니다. 자동차의 전동화에 의해 소형으로 고온의 드라이버에 대응할 수 있는 기반이 한층 더 넓어져, Matter/Thread의 표준화에 의해 오랫동안의 상호 운용성 장벽이 제거됩니다. 이러한 시프트를 종합하면 LED 드라이버 시장은 부품 공급 사업에서 커넥티드 빌딩 플랫폼 및 에너지 관리 서비스의 전략적 인에이블러로 승격합니다.

세계의 LED 드라이버 시장 동향 및 촉진요인

보조금을 통한 LED 복고풍 프로그램이 시장 가속 촉진

인도의 UJALA 이니셔티브는 효율적인 램프의 대규모 유통이 전력 수요를 20GW 줄이고 연간 8,000만 톤의 CO2를 피할 수 있는 방법을 보여줍니다. 이전 할인 시스템과는 달리, 이 프로그램 시장 성장 촉진요인은 공급업체의 금리를 유지하고 에너지 모니터링 기능을 갖춘 고급 드라이버에 중점을 둔 제품의 지속적인 업그레이드를 촉구했습니다. 중국, 말레이시아, 유럽 연합의 유사한 시스템은 전구 교환에서 전반적인 조명기구 교체로 전환하고 있고, 무선 제어를 지원하며, 0.9 이상의 역률을 목표로 IEC 플리커 기준을 충족하는 운전자에 대한 수요를 야기하고 있습니다. LED의 초기 물결이 2015년 경에 서비스 인했기 때문에 58억 유닛의 2차 교환 사이클이 2025-2028년 피크를 맞이하기 시작합니다. 이러한 프로그램은 예측 기간 동안 예측 가능한 대량 조달 파이프라인을 확보하고 LED 드라이버 시장에 기세를 증가시킵니다.

GaN-on-Si 드라이버 IC의 급속한 가격 하락으로 대량 채용 가능

텍사스 기기의 6인치에서 8인치 GaN 웨이퍼로의 전환은 수율을 향상시키면서 다이 비용을 절감하고 전력 변환 효율을 92% 이상으로 높여 열 예산을 줄입니다. 인피니언의 300mm 파일럿 라인은 2025년 실리콘 패리티 가격에 이를 전망으로 소매점 트럭 조명과 가전제품 조명 등 주류 채널을 개척합니다. GaN의 높은 스위칭 주파수는 자성체의 크기를 최대 40%까지 줄이고 조명기구를 얇게 만들고 칩 온보드 모듈에 중요한 요소인 인클로저 온도를 낮춥니다. 자동차용 헤드램프 시스템은 GaN의 높은 접합 온도에 대한 탄력성을 활용하여 전기자동차의 적응형 빔 아키텍처를 지원합니다. 이러한 경제성은 통합의 선순환을 지원합니다. 즉, 수량이 증가함에 따라 비용이 낮아지고 LED 드라이버 시장이 더욱 확대됩니다.

지속적인 실리콘 공급 제약으로 인해 드라이버 IC 생산에 병목 현상 발생

울프 스피드의 유동성 압력은 고출력 조명 및 EV 용도를 위한 실리콘 카바이드 웨이퍼 공급력을 위협합니다. 파운드리는 고급 3nm 로직을 선호하며 LED 드라이버에 사용되는 혼합 신호 프로세스에는 16-90nm 용량이 부족합니다. 일반적인 MOSFET의 리드 타임은 40주를 넘고 특수한 PMIC는 1년을 넘어 설계의 전환이나 멀티 소스 전략을 강요하고 있습니다. 이러한 제약은 중견 OEM 마진을 압박하는 가격 변동을 일으키고 입찰 상한이 확정된 옥외 조명 프로젝트와 같은 부문에서 단기 출하 가능성을 약화시킵니다. 동남아시아의 생산능력 증강이 궤도를 타기 전까지는 실리콘 부족이 LED 드라이버 시장의 발판이 될 것으로 보입니다.

부문 분석

2024년 LED 드라이버 시장 점유율은 정전류 디바이스가 61.2%를 차지했습니다. 그러나 정전력 드라이버는 최대 92%의 변환 효율을 실현하고 설계 변경 없이 가변 전압 LED 부하에 대응하기 때문에 2025-2030년 CAGR은 23.1%로 예측됩니다. 차량용 전조등의 틈새 분야에서 인피니언의 Litix Power Flex 시리즈는 성능의 도약을 보여줍니다.

적응 조명 시나리오의 상승은 이러한 변화를 강화합니다. 건축 정면, 스포츠 경기장, 조정가능한 백색 사무실 기구는 전류를 다이오드의 허용 범위 안에 유지하는 동안 출력을 동적으로 조정할 수 있는 경우에 혜택을 받습니다. 이 범용성은 조명기구 제조업체에게 SKU의 보급을 억제하고 현장 업그레이드 경로를 강화합니다. 무선 프로토콜이 보급됨에 따라 펌웨어에서 선택 가능한 출력 곡선으로 정전력 설계가 진화하는 LED 드라이버 시장에서 선호되는 플랫폼이 되었습니다.

DALI와 0-10V로 대표되는 유선 시스템은 2024년 LED 드라이버 시장 규모의 65.4%를 차지합니다. 그러나 무선 기능은 2030년까지 연평균 복합 성장률(CAGR)이 24.3%가 되어 채용 곡선의 급 곡선으로 향합니다. 르그랑의 Matter 인증 월박스 디머는 앱 기반 커미셔닝에 대한 소비자의 열정을 보여줍니다.

총 비용 렌즈에서 볼 때 제어 라인을 제거하면 상업 리노베이션 예산의 15-25% 노동력이 줄어들고 ROI는 종종 LED 플러스 제어를 지원합니다. Thread의 IPv6 기반은 건물 관리 통합을 용이하게 하며 BLE 메쉬는 비상 조명 점검을 위한 저에너지 폴백을 제공합니다. 무선 펌웨어 업데이트가 주류가 된 현재, 무선 드라이버는 장래의 기능에 대응하는 것으로, 동작 수명을 연장합니다. 이러한 이점으로 인해 무선은 LED 드라이버 시장의 기둥으로 확고한 지위를 구축하고 있습니다.

지역 분석

북미의 2024년 매출액 점유율 32.3%는 83-195 lm/W까지 기준을 끌어올리는 엄격한 램프 효율 규칙이 사양 책정자를 고효율 드라이버로 유도하고 있기 때문입니다. Coca-Cola Consolidated의 6개 시설 업그레이드와 같은 기업 리노베이션은 연간 9만 7,063달러를 절약하고 신속한 투자 회수 이야기를 강조합니다. CHIPS법은 국내 공장에 2,000억 달러가 할당되어 아날로그 및 파워 컴포넌트의 탄력성을 향상시키고 있습니다. 캐나다와 멕시코는 통합 공급망을 활용하여 기술 표준과 공인 실험실을 공유하고 국경을 넘어 선적을 원활하게 하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 24.2%로 성장이 예측되어 가장 빠른 구조 상승을 나타냅니다. 중국 제조업의 두께가 부품 비용을 줄이고 지자체의 스마트 시티 보조금이 NB-IoT와 LoRa 게이트웨이를 탑재한 드라이버의 현지 수요를 자극합니다. 인도의 기록적인 규모의 UJALA 프로그램은 사용된 램프의 재고를 보충하고 조명기구 업그레이드 사이클의 두 번째 파도를 시작합니다. 일본, 한국, 대만은 EV 주도의 헤드램프 혁신을 수출 가능한 어댑티브 빔 드라이버로 전환합니다. ASEAN 시장은 공급망의 다양화를 흡수하고, 베트남은 북미 브랜드의 마무리 및 조립 허브로서 대두합니다.

유럽은 2030년까지 연간 96TWh의 절약을 목표로 하는 Ecodesign 2019/2020을 통해 기세를 유지합니다. 독일 KfW 은행의 보조금은 우대 금리를 지능형 조명 도입에 연결하여 물류 창고에서 운전자 교체를 가속화합니다. 동유럽의 리노베이션 파이프라인은 결속 기금의 지원을 받고 있으며, 영국의 건축 규제 파트 L은 개방형 프로토콜 통신이 가능한 드라이버를 우대하는 동적 조명 지침을 언급하고 있습니다. 중동 및 아프리카는 사우디아라비아의 CAGR 10% LED 도입 전망으로 대표되는 비전 2030 프로그램으로 현지 조립 벤처가 지원하는 세계 LED 드라이버 시장을 보완하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 보조금에 의한 LED 개수 프로그램(2025년 이후 전개)

- GaN-on-Si 드라이버 IC의 급속한 가격 하락

- 신축 기준에서 스마트 라이트 의무화

- 마터 및 스레드 무선 컨트롤의 주류 채용

- EV용 헤드 램프 LED 드라이버 수요 급증

- 기업의 넷 제로 목표가 산업의 업그레이드 가속

- 시장 성장 억제요인

- 드라이버 IC의 실리콘 공급 제약 지속

- 레거시한 유선 프로토콜의 한정적인 상호 운용성

- 비절연형 드라이버의 디자인 인의 복잡성

- 중국제 정전류 모듈에 높은 수입 관세

- 공급망 분석

- 기술의 전망

- 규제 상황

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시경제 요인 평가

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 정전류 LED 드라이버

- 정전압 LED 드라이버

- 정전력 LED 드라이버

- 제어기능별

- 와이어 있음

- 0-10 V

- DALI

- DMX

- PLC

- Trailing-Edge

- 무선

- Wi-Fi

- Bluetooth/BLE

- Zigbee

- Thread/Matter

- Li-Fi

- 와이어 있음

- 출력별

- 25W 미만

- 25-65 W

- 65-150 W

- 150W 이상

- 폼 팩터별

- 외부 독립형 론

- 통합 및 온보드

- 리니어 드라이버

- 소형 및 모듈 드라이버

- 최종 용도별

- 주택

- 상업 및 사무실

- 소매 및 접객

- 옥외 조명 및 가로 조명

- 산업

- 헬스케어 및 교육

- 자동차용 조명 시스템

- 원예 및 농업

- 소비자 일렉트로닉스용 백라이트

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 카타르

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 케냐

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Signify

- ams OSRAM

- Acuity Brands Lighting

- Hubbell Incorporated

- Eaton(Cooper Lighting)

- Lutron Electronics

- Cree LED(SGH)

- MEAN WELL Enterprises

- Inventronics

- Tridonic(Zumtobel)

- Delta Electronics

- Shenzhen Done Power

- ERP Power

- Lifud Technology

- Helvar

- Murata Manufacturing

- Texas Instruments

- ON Semi

- Allegro MicroSystems

- ROHM Semiconductor

- Macroblock Inc.

- TCI Srl

- MOSO Power

- Current(GE)

제7장 시장 기회 및 향후 전망

제8장 투자 분석

AJY 25.11.24The LED driver market is valued at USD 20.19 billion in 2025 and is forecast to grow to USD 56.64 billion by 2030, reflecting a CAGR of 22.91%.

This expansion is underpinned by the alignment of national energy-efficiency mandates, accelerating wireless-control adoption and the deployment of silicon-carbide and gallium-nitride semiconductors that raise conversion efficiency and shrink driver footprints. Government-funded retrofit programs, particularly in Asia-Pacific, intersect with net-zero commitments to lift large-scale replacement demand, while new-build codes in North America and Europe push integrated intelligent-lighting specifications. Automotive electrification further widens the addressable base for compact, high-temperature drivers, and Matter/Thread standardization dismantles long-standing interoperability barriers. Collectively, these shifts elevate the LED driver market from a component-supply business to a strategic enabler of connected-building platforms and energy-management services.

Global LED Driver Market Trends and Insights

Subsidy-fuelled LED Retrofit Programs Drive Market Acceleration

India's UJALA initiative illustrates how large-scale distribution of efficient lamps can slash electricity demand by 20 GW and avoid 80 million t of CO2 annually. Unlike earlier discount schemes, the program's market-based approach sustained vendor margins, encouraging continual product upgrades that now emphasize advanced drivers with energy-monitoring functions. Similar schemes in China, Malaysia and the European Union are moving from bulb replacements toward holistic luminaire swaps, triggering demand for drivers that support wireless controls, target power factors above 0.9 and meet IEC flicker criteria. Because early LED waves entered service around 2015, a secondary replacement cycle of 5.8 billion units begins peaking between 2025 and 2028. These programs collectively add momentum to the LED driver market by ensuring predictable, large-volume procurement pipelines over the forecast period.

Rapid Price Declines in GaN-on-Si Driver ICs Enable Mass Adoption

Texas Instruments' migration from 6-inch to 8-inch GaN wafers cuts die cost while improving yield consistency, pushing power-conversion efficiency beyond 92% and shrinking thermal budgets.Infineon's 300 mm pilot line is expected to reach silicon-parity pricing in 2025, opening mainstream channels such as retail track lighting and appliance illumination. GaN's higher switching frequencies reduce magnetics size by up to 40%, enabling slimmer luminaire profiles and lowering enclosure temperatures, a critical factor for chip-on-board modules. Automotive headlamp systems benefit from GaN's resilience at high junction temperatures, supporting adaptive-beam architectures in electric vehicles. These economics support a virtuous cycle of integration: as volumes climb, cost drops deepen, broadening the LED driver market even further.

Persistent Silicon Supply Constraints Create Bottlenecks in Driver IC Production

Wolfspeed's liquidity pressures threaten silicon-carbide wafer availability for high-power lighting and EV applications. Foundries prioritize advanced 3-nm logic, leaving 16-90 nm capacity thin for the mixed-signal processes used in LED drivers. Lead times exceed 40 weeks for common MOSFETs; speciality PMICs stretch beyond a year, forcing design pivots and multi-sourcing strategies. The constraint drives price volatility that squeezes mid-tier OEM margins, dampening near-term shipment potential in segments such as outdoor lighting projects with firm bid ceilings. Until capacity additions in Southeast Asia come online, silicon shortfalls remain a measurable drag on the LED driver market.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Lighting Mandates in New-Build Codes Create Compliance-Driven Demand

- Mainstream Adoption of Matter/Thread Wireless Controls Standardizes Connectivity

- Limited Interoperability Across Legacy Wired Protocols Fragments Market Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Constant current devices held 61.2% LED driver market share in 2024, driven by decades of design familiarity in high-lumen applications. However, constant power drivers deliver up to 92% conversion efficiency and accommodate variable-voltage LED loads without redesign, supporting a projected 23.1% CAGR between 2025 and 2030. In the automotive front-lighting niche, Infineon's Litix Power Flex series illustrates the performance jump: SPI-controlled dimming and multi-string protection broaden functionality without thermal penalty.

The rise of adaptive lighting scenarios reinforces the shift. Architectural facades, sports arenas and tunable-white office fixtures benefit when output can adjust dynamically while current remains within diode tolerances. This versatility lowers SKU proliferation for luminaire makers and enhances field-upgrade paths. As wireless protocols proliferate, firmware-selectable power curves make constant power designs the preferred platform in the evolving LED driver market.

Wired systems, led by DALI and 0-10 V, accounted for 65.4% of the LED driver market size in 2024 because existing-bearing structures embed control cabling. Yet wireless features head into the steep part of the adoption curve, with a 24.3% CAGR through 2030. Legrand's Matter-approved wall-box dimmers demonstrate consumer enthusiasm for app-based commissioning.

From a total-cost lens, eliminating control wires trims labour 15-25% in commercial retrofit budgets, often swinging ROI in favour of LED plus controls. Thread's IPv6 foundation eases building-management integration, and BLE mesh provides low-energy fallback for emergency lighting checks. With over-the-air firmware updates now mainstream, wireless drivers extend operating lifetimes by accommodating future features. These advantages cement wireless as a pillar of the LED driver market.

LED Driver Market Report is Segmented by Product Type (Constant Current LED Drivers, and More), Control Feature (Wired, Wireless), Power Output (Less Than25W, 25-65W, and More), Form Factor (External Stand-Alone, Integrated/On-Board, and More), End-Use Application (Residential, Commercial and Office, Retail and Hospitality, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 32.3% revenue share in 2024 derives from rigorous lamp-efficacy rules that raise the bar to 83-195 lm/W, steering specifiers toward high-efficiency drivers. Corporate retrofits such as Coca-Cola Consolidated's six-facility upgrade realize USD 97,063 annual savings and underline the quick payback narrative. The CHIPS Act allocates USD 200 billion for domestic fabs, improving resilience for analog and power components. Canada and Mexico leverage integrated supply chains to share technical standards and qualification labs, smoothing cross-border shipments.

Asia-Pacific exhibits the fastest structural rise, projecting a 24.2% CAGR through 2030. China's manufacturing depth slashes BOM costs, and its municipal smart-city grants stimulate local demand for drivers with NB-IoT or LoRa gateways. India's record-scale UJALA program replenishes lamp inventories at end-of-life, kick-starting a second-wave luminaire upgrade cycle. Japan, South Korea and Taiwan channel EV-led headlamp innovations into exportable adaptive-beam drivers. ASEAN markets absorb supply-chain diversification, with Vietnam emerging as a finish-and-assembly hub for North American brands.

Europe sustains momentum through Ecodesign 2019/2020, which targets 96 TWh savings annually by 2030. Germany's KfW-bank subsidies tie preferential interest rates to intelligent-lighting deployment, accelerating driver replacements in logistics warehouses. Eastern European retrofit pipelines receive cohesion-fund backing, while the United Kingdom's Building Regulations Part L references dynamic-lighting guidance that favours drivers capable of open-protocol communication. The Middle East and Africa supplement the global LED driver market with Vision 2030 programs, typified by Saudi Arabia's 10% CAGR LED adoption outlook underpinned by local assembly ventures.

- Signify

- ams OSRAM

- Acuity Brands Lighting

- Hubbell Incorporated

- Eaton (Cooper Lighting)

- Lutron Electronics

- Cree LED (SGH)

- MEAN WELL Enterprises

- Inventronics

- Tridonic (Zumtobel)

- Delta Electronics

- Shenzhen Done Power

- ERP Power

- Lifud Technology

- Helvar

- Murata Manufacturing

- Texas Instruments

- ON Semi

- Allegro MicroSystems

- ROHM Semiconductor

- Macroblock Inc.

- TCI Srl

- MOSO Power

- Current (GE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidy-fuelled LED retrofit programs (post-2025 roll-outs)

- 4.2.2 Rapid price declines in GaN-on-Si driver ICs

- 4.2.3 Smart-lighting mandates in new-build codes

- 4.2.4 Mainstream adoption of Matter/Thread wireless controls

- 4.2.5 Surge in EV headlamp LED driver demand

- 4.2.6 Corporate net-zero targets accelerating industrial upgrades

- 4.3 Market Restraints

- 4.3.1 Persistent silicon supply constraints for driver ICs

- 4.3.2 Limited interoperability across legacy wired protocols

- 4.3.3 Design-in complexity for non-isolated drivers

- 4.3.4 High import tariffs on Chinese constant-current modules

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Constant Current LED Drivers

- 5.1.2 Constant Voltage LED Drivers

- 5.1.3 Constant Power LED Drivers

- 5.2 By Control Feature

- 5.2.1 Wired

- 5.2.1.1 0-10 V

- 5.2.1.2 DALI

- 5.2.1.3 DMX

- 5.2.1.4 PLC

- 5.2.1.5 Trailing-Edge

- 5.2.2 Wireless

- 5.2.2.1 Wi-Fi

- 5.2.2.2 Bluetooth/BLE

- 5.2.2.3 Zigbee

- 5.2.2.4 Thread / Matter

- 5.2.2.5 Li-Fi

- 5.2.1 Wired

- 5.3 By Power Output

- 5.3.1 Less than 25 W

- 5.3.2 25 - 65 W

- 5.3.3 65 -150 W

- 5.3.4 Greater than 150 W

- 5.4 By Form Factor

- 5.4.1 External Stand-Alone

- 5.4.2 Integrated / On-Board

- 5.4.3 Linear Drivers

- 5.4.4 Compact / Module Drivers

- 5.5 By End-Use Application

- 5.5.1 Residential

- 5.5.2 Commercial and Office

- 5.5.3 Retail and Hospitality

- 5.5.4 Outdoor and Street Lighting

- 5.5.5 Industrial

- 5.5.6 Healthcare and Education

- 5.5.7 Automotive Lighting Systems

- 5.5.8 Horticulture and Agriculture

- 5.5.9 Consumer-Electronics Backlighting

- 5.5.10 Other Applications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Qatar

- 5.6.5.1.5 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Kenya

- 5.6.5.2.5 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify

- 6.4.2 ams OSRAM

- 6.4.3 Acuity Brands Lighting

- 6.4.4 Hubbell Incorporated

- 6.4.5 Eaton (Cooper Lighting)

- 6.4.6 Lutron Electronics

- 6.4.7 Cree LED (SGH)

- 6.4.8 MEAN WELL Enterprises

- 6.4.9 Inventronics

- 6.4.10 Tridonic (Zumtobel)

- 6.4.11 Delta Electronics

- 6.4.12 Shenzhen Done Power

- 6.4.13 ERP Power

- 6.4.14 Lifud Technology

- 6.4.15 Helvar

- 6.4.16 Murata Manufacturing

- 6.4.17 Texas Instruments

- 6.4.18 ON Semi

- 6.4.19 Allegro MicroSystems

- 6.4.20 ROHM Semiconductor

- 6.4.21 Macroblock Inc.

- 6.4.22 TCI Srl

- 6.4.23 MOSO Power

- 6.4.24 Current (GE)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emerging Opportunities in Non-Isolated Drivers

- 7.3 Visible-Light Communication Integration

- 7.4 GaN and SiC-based Driver IC Adoption