|

시장보고서

상품코드

1851732

액상 실리콘 고무(LSR) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Liquid Silicone Rubber (LSR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

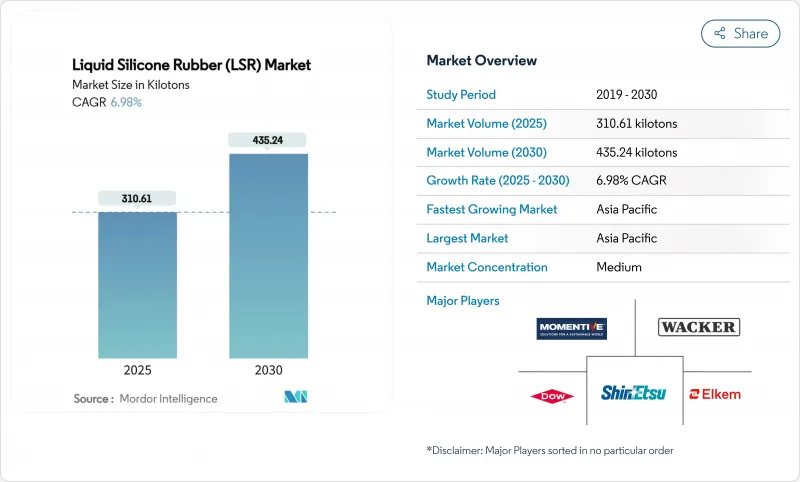

액상 실리콘 고무 시장 규모는 2025년 310.61킬로톤으로 평가되었고, 2030년에는 435.24킬로톤으로 확대될 것으로 예측되며, 2025-2030년 CAGR은 6.98%를 나타낼 전망입니다.

의료 기기, 프리미엄 유아용품, 초고전압 전기차(EV) 배터리 팩에서 생체적합성 소재에 대한 수요 증가가 이러한 성장 추세를 지속시키고 있습니다. 아시아태평양 지역은 전자제품 및 자동차 제조를 바탕으로 현재 소비를 주도하고 있으며, 북미와 유럽에서는 의료 혁신이 채택을 가속화하고 있습니다. 액상 사출 성형(LIM)은 정밀한 공차, 최소한의 플래시, 높은 생산성을 제공하기 때문에 여전히 선호되는 가공 기술입니다.

세계의 액상 실리콘 고무(LSR) 시장 동향 및 인사이트

헬스케어 산업에서의 수요 증가

병원과 기기 제조업체들은 이 소재가 ISO 10993 세포독성 및 USP Class VI 기준을 충족하고, 감마선 및 증기 멸균에 저항하며, 언더컷이 있는 복잡한 형상을 지원하기 때문에 의료용 등급의 배합을 지정합니다. 최근 기술 발전으로 단일 임플란트에서 다중 약물 방출이 가능해져 의사가 항암 및 통증 관리 치료에 맞춤형 방출 프로파일을 설계할 수 있게 되었습니다. 압축 변형 저항성은 임플란트 수명을 연장하여 재수술 위험과 총 치료 비용을 낮춥니다. FDA의 추적성 요구와 더 엄격한 입자 제한으로 인해 카테터 허브 및 마이크로 밸브에 청정실 LIM 공정이 표준화되었습니다. 이러한 요소들이 종합적으로 작용하여 글로벌 사양 적용률을 높이고 액상 실리콘 고무 시장을 고마진 의료 분야로 확장시키는 데 기여하고 있습니다.

유아용품 산업의 수요 증가

보호자들은 가소제, BPA, 라텍스 단백질이 포함되지 않은 젖꼭지, 치발기, 젖병을 점점 더 선호하고 있습니다. 액상 실리콘 고무는 수백 번의 식기세척기 또는 멸균 사이클 후에도 탄성을 유지하여 TPE 대체재 대비 브랜드에 뚜렷한 내구성 우위를 제공합니다. 저자극성 및 무취 특성은 엄격한 국제 장난감 안전 지침과 부합하며, 생동감 있는 색상 옵션은 프리미엄 제품이 소매 진열대에서 두드러지게 하는 데 기여합니다. 100% 식품 등급 유아용 칫솔과 같은 생산자 혁신은 이 틈새 시장이 일상 위생용품으로 지속적으로 확장되는 방식을 보여줍니다. 이러한 트렌드들은 종합적으로 소비자 기반을 확대하고 액상 실리콘 고무 시장 내 매출 밀도를 높입니다.

액상 실리콘 고무 제품의 높은 비용

전용 도징 펌프, 폐쇄형 온도 제어 시스템, 플런저식 사출 기계는 열가소성 성형 대비 자본 지출을 증가시킵니다. 의료용 순도, 식품 접촉 인증, 난연성 패키지 등 부가가치 기능은 일반 탄성체 대비 배합 가격을 25-60% 상승시킵니다. 공정 통합 센서는 사이클 시간 단축과 불량품 감소를 제공하지만, 인더스트리 4.0 하드웨어에 대한 선행 투자가 필요합니다. 개인 위생 용품 디스펜서와 같은 예산 제약이 있는 부문은 때때로 개질 TPE로 전환하여 단기 성장을 저해합니다. 생산자들은 더 높은 캐비티 금형, 예측 유지보수 플랫폼, 지역별 컴파운딩 확대를 통해 운송비를 절감함으로써 액상 실리콘 고무 시장에 대한 이러한 제동을 점차 완화하고 있습니다.

부문 분석

산업용 등급은 2024년 47.38%로 최대 점유율을 유지하며, 다양한 산업 분야의 씰, 그로밋, 키패드 하우징에 비용 효율적인 성능을 제공합니다. 높은 인열 강도와 내유성은 자동차 엔진룸 부품 및 소비자 전자제품 버튼에 적합함을 뒷받침하여 액상 실리콘 고무 시장 내 안정적인 기본 수요를 보장합니다.

의료/이식용 등급은 전 세계적으로 최소 침습 치료가 확산되면서 연평균 7.15% 성장률을 보이고 있습니다. 미국 FDA의 심장 리드 및 신경 조절 임플란트 승인 시 백금 경화 LSR이 제공하는 낮은 추출물 데이터와 안정적인 압축 변형률 값이 자주 인용됩니다. 이 프리미엄 가격대는 액상 실리콘 고무 시장 전체 수익성을 개선하며, 주요 공급업체들은 엄격한 추적성 요구사항을 충족하기 위해 ISO 13485 인증 생산 라인을 확장하고 있습니다. 식품 접촉 등급은 재사용 가능한 베이킹 몰드와 유아용 식기에서 기반을 둔 틈새 성장 분야를 형성합니다. 반복적인 멸균 후에도 성능이 유지되어 일회용 플라스틱에 대한 친환경 대안으로 자리매김하고 있습니다.

액상 사출 성형(LIH)은 완전 자동화 혼합, 짧은 경화 사이클, 최소한의 후처리로 인해 2024년 69.19%의 점유율을 기록했습니다. 다중 구성 요소 LIM(Liquid Injection Molding)은 단일 사출로 경질 플라스틱 기판과 연질 LSR 오버몰드를 통합하여 의료용 밸브 및 스마트워치 스트랩의 조립 시간을 단축합니다. 이러한 장점은 OEM이 택트 타임 단축과 반복 가능한 고수율 생산을 추구함에 따라 결정적이며, 이는 액상 실리콘 고무 시장에서 LIM의 위상을 강화합니다.

이송 성형 및 압축 성형은 캐비티 수보다 프레스 톤수가 경제성을 좌우하는 산업용 다이어프램과 같은 초대형 부품에 여전히 중요합니다. 초기 적층 제조 파일럿은 3D 프린팅된 LSR 격자 구조가 맞춤형 의족의 완충 성능을 조절할 수 있음을 보여주며, 향후 프로토타입의 유연성과 대량 생산 품질 간의 가교 역할을 암시합니다.

지역 분석

아시아태평양 지역은 2024년 전 세계 물량의 53.96%를 차지했으며, 중국이 지역 소비량의 절반 이상을 차지했습니다. 윈카 타이뇽(Wynca Tinyo)과 장쑤 톈천(Jiangsu Tianchen)의 확장 움직임은 원료 비용 절감과 공급 안정성을 확보하기 위한 현지 상류 통합으로의 전환을 시사합니다. 신에너지차에 대한 정부 인센티브는 배터리 냉각 패드 및 셀-모듈 개스킷 분야의 LSR 수요를 높여, 해당 지역의 액상 실리콘 고무 시장 영향력을 공고히 하고 있습니다.

북미는 미네소타, 캘리포니아 및 멕시코 바히오(Bajio) 지역의 고순도 의료기기 생산 클러스터를 기반으로 2위를 차지했습니다. 최근 추가된 생산 능력(예: 다트와일러의 2성분 성형 라인)은 미국 및 캐나다 OEM의 리드 타임을 단축시키면서 동시에 운송비 변동성으로부터 보호합니다. 워싱턴과 앨라배마의 항공우주 1차 공급업체들은 객실 및 엔진 씰에 난연 등급을 지정하여 경량화 목표를 달성하기 위해 LSR의 넓은 열적 범위를 활용합니다.

유럽은 공정 혁신과 지속가능성 분야에서 선도적 위치를 유지하고 있습니다. 독일 기계 제조사들은 도징 정밀도를 지속적으로 개선해 불량률을 낮추고 있으며, 이탈리아 금형 제조사들은 사이클 시간을 단축하는 컨포멀 쿨링 레이아웃을 선도하고 있습니다. 유럽연합 집행위원회의 순환경제 집중은 뉴 던 실리콘즈(New Dawn Silicones)와 같은 화학적 재활용 사업에 대한 연구개발을 촉진하며, 폐쇄형 시스템이 액상 실리콘 고무 시장의 추가 성장 채널을 열어줄 미래를 예고하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 헬스케어 산업의 수요 증가

- 높은 생체 적합성으로 인한 유아용품 산업의 수요 증가

- 초고전압 EV 배터리 씰 수요가 자동차 등급의 채택을 촉진

- 독특한 특성으로 인한 전자 산업의 활용도 증가

- 경량화 목표에 따른 항공우주 산업에서의 채택 증가

- 시장 성장 억제요인

- 액상 실리콘 고무 제품의 고비용

- 소비재 분야의 신형 TPE(열가소성 엘라스토머)에 의한 저비용 경쟁

- 액상 실리콘 고무의 재활용 과제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유형별

- 산업용 LSR

- 의료용 LSR

- 식품 접촉 등급 LSR

- 가공 방법별

- 액상 사출 성형

- 이송 및 압축 성형

- 용도별

- 씰, 개스킷, O링

- 카테터와 의료용 튜브

- 전기 커넥터 및 하우징

- 젖꼭지, 포유기, 유아용 우유

- 웨어러블 및 이식형 약물전달 시스템

- 최종 이용 산업별

- 헬스케어 및 의료기기

- 자동차

- 전기 및 전자

- 소비재

- 뷰티&퍼스널케어

- 기타 최종 사용자 산업(산업기계, 씰 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Avantor, Inc.

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- Jiangsu Tianchen New Material Co. Ltd

- KCC SILICONE CORPORATION

- Momentive

- RICO Elastomere Projecting GmbH

- RICO GROUP GmbH

- Shin-Etsu Chemical Co. Ltd

- Stockwell Elastomerics Inc.

- Trelleborg Group

- Wacker Chemie AG

- Wynca Tinyo Silicone Co., Ltd.

제7장 시장 기회와 장래의 전망

HBR 25.11.17The liquid silicone rubber market size reached 310.61 kilotons in 2025 and is projected to expand to 435.24 kilotons by 2030, reflecting a 6.98% CAGR over 2025-2030.

Rising demand for biocompatible materials in medical devices, premium baby products, and ultra-high-voltage electric-vehicle (EV) battery packs sustains this growth trajectory. Asia-Pacific dominates current consumption on the back of electronics and automotive manufacturing, while healthcare innovation is accelerating adoption in North America and Europe. Liquid injection molding (LIM) remains the preferred processing technology because it delivers tight tolerances, minimal flash, and high output rates.

Global Liquid Silicone Rubber (LSR) Market Trends and Insights

Increasing Demand From the Healthcare Industry

Hospitals and device makers specify medical-grade formulations because the material meets ISO 10993 cytotoxicity and USP Class VI criteria, resists gamma and steam sterilization, and supports complex geometries with undercuts. Recent breakthroughs enable multi-drug elution from a single implant, allowing physicians to tailor release profiles for oncology and pain-management therapies. Compression-set resistance extends implant life, lowering revision-surgery risk and total cost of care. Clean-room LIM has become routine for catheter hubs and micro-valves, driven by FDA expectations for traceability and tighter particulate limits. These factors together lift global specification rates and help propel the liquid silicone rubber market toward higher-margin medical segments.

Rising Demand From the Baby Care Industry

Caregivers increasingly favor pacifiers, teething rings, and feeding bottles that contain no plasticizers, BPA, or latex proteins. Liquid silicone rubber maintains elasticity after hundreds of dishwasher or sterilization cycles, giving brands a clear durability advantage over TPE alternatives. Hypoallergenic and odor-neutral traits align with strict international toy-safety directives, while vibrant pigmentation options help premium lines stand out on retail shelves. Producer innovation-such as 100% food-grade infant toothbrushes-illustrates how this niche keeps expanding into everyday hygiene items. Together, these trends enlarge the consumer base and lift revenue density inside the liquid silicone rubber market.

High Cost of Liquid Silicone Rubber Products

Dedicated dosing pumps, closed-loop temperature control, and plunger-type injection machines inflate capital outlays relative to thermoplastic molding. Added-value features-medical purity, food-contact certification, or flame-retardancy packages-increase formulation prices by 25%-60% versus commodity elastomers. Process-integration sensors provide cycle-time savings and scrap reduction but require upfront investment in Industry 4.0 hardware. Budget-constrained segments such as personal-care dispensers sometimes switch to modified TPEs, dragging near-term growth. Producers are countering with higher cavity molds, predictive maintenance platforms, and expanded regional compounding to shrink freight costs, gradually easing this brake on the liquid silicone rubber market.

Other drivers and restraints analyzed in the detailed report include:

- Demand for EV Battery Sealing

- Growing Utilization From the Electronics Industry

- Recycling Challenges for Liquid Silicone Rubber

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial grade maintained the lion's share at 47.38% in 2024, delivering cost-effective performance for seals, grommets, and keypad housings across diverse industries. High tear strength and oil resistance underpin its suitability for under-hood automotive parts and consumer-electronics buttons, ensuring stable baseline demand inside the liquid silicone rubber market.

Medical/implant grade is advancing at a 7.15% CAGR as minimally invasive therapies gain traction globally. United States FDA approvals for cardiac leads and neuromodulation implants frequently cite low extractables data and stable compression-set values made possible by platinum-cured LSR. This premium pricing tier improves overall liquid silicone rubber market size profitability, with top suppliers scaling ISO 13485-certified production cells to meet stringent traceability requirements. Food-contact grade forms a niche growth pocket anchored in reusable baking molds and baby utensils; performance parity after repeated sterilizations positions it as an eco-friendly alternative to single-use plastics.

Liquid Injection Holding held 69.19% in 2024, stemming from fully automated mixing, short cure cycles, and minimal post-processing. Multi-component LIM integrates hard-plastic substrates with soft LSR over-molds in a single shot, cutting assembly time for medical valves and smart-watch straps. These advantages are critical as OEMs chase takt-time reductions and repeatable high yields, reinforcing LIM's status in the liquid silicone rubber market.

Transfer and compression molding retain relevance for very large parts such as industrial diaphragms, where press tonnage rather than cavity count dictates economics. Early additive-manufacturing pilots demonstrate how 3D-printed LSR lattices can tune cushioning in custom prosthetics, hinting at a future bridge between prototype agility and mass-production quality.

The Liquid Silicone Rubber Market Report Segments the Industry by Type (Food-Contact Grade LSR, Industrial Grade LSR, Medical Grade LSR), Processing Method (Liquid Injection Molding, Transfer and Compression Molding), Application (Seals, Gaskets and O Rings, Catheters and Medical Tubing, and More), End-User Industry (Healthcare and Medical Devices, Automotive, and More), and Geography (Asia-Pacific, North America, and More).

Geography Analysis

Asia-Pacific held 53.96% of global volume in 2024, with China accounting for more than half of regional consumption. Expansions by Wynca Tinyo and Jiangsu Tianchen signal a shift toward local upstream integration that lowers feedstock costs and secures supply continuity. Government incentives for new-energy vehicles elevate LSR demand in battery cooling pads and cell-module gaskets, cementing the region's influence on the liquid silicone rubber market.

North America ranks second, anchored by high-purity medical-device production clusters in Minnesota, California, and Mexico's Bajio corridor. Recent capacity additions-such as Datwyler's two-component molding lines-shorten lead times for U.S. and Canadian OEMs while shielding them from freight volatility. Aerospace tier-ones in Washington and Alabama specify flame-retardant grades for cabin and engine seals, tapping LSR's broad thermal window to meet weight-saving goals.

Europe maintains leadership in process innovation and sustainability. German machine builders continuously refine dosing precision to shrink scrap rates, and Italian mold-makers pioneer conformal-cooling layouts that lower cycle times. The European Commission's focus on circularity spurs R&D into chemical recycling ventures like New Dawn Silicones, foreshadowing a future where closed-loop systems unlock additional growth channels for the liquid silicone rubber market.

- Avantor, Inc.

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- Jiangsu Tianchen New Material Co. Ltd

- KCC SILICONE CORPORATION

- Momentive

- RICO Elastomere Projecting GmbH

- RICO GROUP GmbH

- Shin-Etsu Chemical Co. Ltd

- Stockwell Elastomerics Inc.

- Trelleborg Group

- Wacker Chemie AG

- Wynca Tinyo Silicone Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand From the Healthcare Industry

- 4.2.2 Rising Demand From the Baby Care Industry due to its High Biocompatibility

- 4.2.3 Demand for Ultra-High-Voltage EV Battery Sealing Drives Automotive Grade Adoption

- 4.2.4 Growing Utilization from the Electronics Industry due to its Unique Properties

- 4.2.5 Increasing Adoption in the Aerospace Industry Driven by Light weighting Targets

- 4.3 Market Restraints

- 4.3.1 High Cost of Liquid Silicone Rubber Products

- 4.3.2 Low-cost Competition from Novel TPEs in Consumer Goods

- 4.3.3 Recycling Challenges for Liquid Silicone Rubber

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Industrial Grade LSR

- 5.1.2 Medical Grade LSR

- 5.1.3 Food-Contact Grade LSR

- 5.2 By Processing Method

- 5.2.1 Liquid Injection Molding

- 5.2.2 Transfer and Compression Molding

- 5.3 By Application

- 5.3.1 Seals, Gaskets and O Rings

- 5.3.2 Catheters and Medical Tubing

- 5.3.3 Electrical Connectors and Housings

- 5.3.4 Teats, Soothers and Infant Feeding

- 5.3.5 Wearable and Implantable Drug Delivery Systems

- 5.4 By End-use Industry

- 5.4.1 Healthcare and Medical Devices

- 5.4.2 Automotive

- 5.4.3 Electrical and Electronics

- 5.4.4 Consumer Goods

- 5.4.5 Beauty and Personal Care

- 5.4.6 Other End-user Industries(Industrial Machinery and Seals, etc.)

- 5.5 By Geography

- 5.5.1 Asia Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Avantor, Inc.

- 6.4.2 CHT Germany GmbH

- 6.4.3 Dow

- 6.4.4 DuPont

- 6.4.5 Elkem ASA

- 6.4.6 Jiangsu Tianchen New Material Co. Ltd

- 6.4.7 KCC SILICONE CORPORATION

- 6.4.8 Momentive

- 6.4.9 RICO Elastomere Projecting GmbH

- 6.4.10 RICO GROUP GmbH

- 6.4.11 Shin-Etsu Chemical Co. Ltd

- 6.4.12 Stockwell Elastomerics Inc.

- 6.4.13 Trelleborg Group

- 6.4.14 Wacker Chemie AG

- 6.4.15 Wynca Tinyo Silicone Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Advancements in Miniaturization and Smart Device Integration