|

시장보고서

상품코드

1910536

조명 제어 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Lighting Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

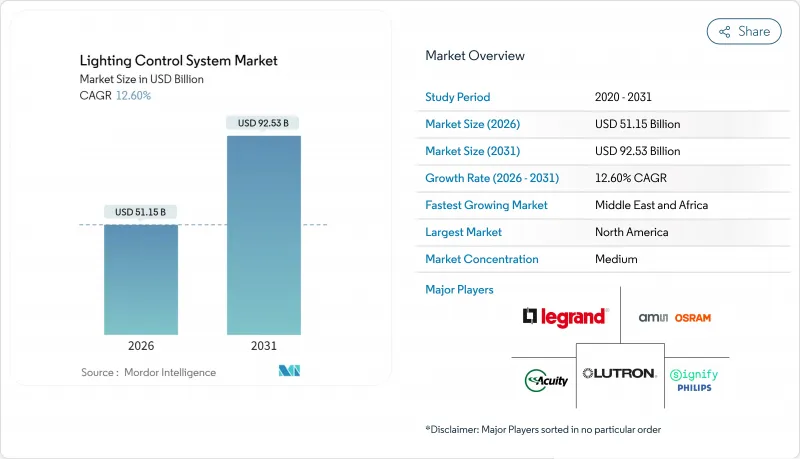

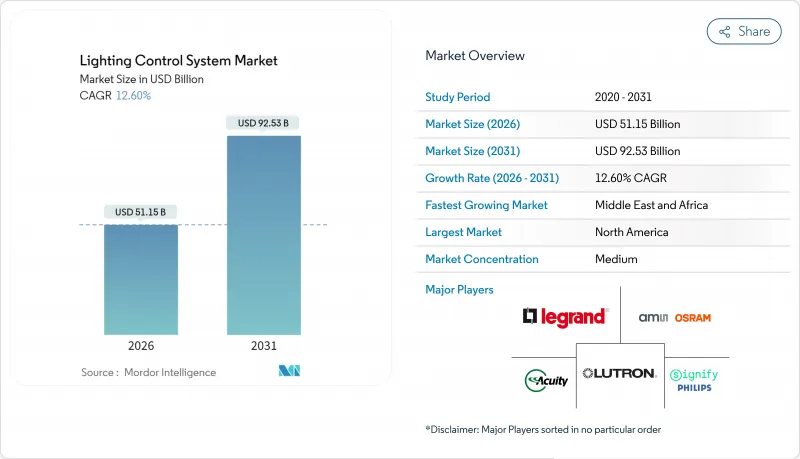

조명 제어 시스템 시장은 2025년 454억 3,000만 달러에서 2026년에는 511억 5,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 12.6%를 나타낼 전망입니다. 2031년까지 925억 3,000만 달러에 이를 것으로 예측됩니다.

이 성장 가속은 의무화된 에너지 절약 요건, 스마트 시티 계획의 보급, 조명기구를 데이터 소스로 전환하는 IoT 지원 빌딩 자동화의 광범위한 사용을 반영합니다. 정부는 현재 자동소등, 일광조광, 재실검지를 건축기준에 통합하고 있으며, 이에 따라 비임의적인 수요가 창출되고 있습니다. LED 부품의 가격 하락에 의해 투자 회수 기간이 단축되어 소규모 시설에서도 종합적인 제어 시스템의 도입이 경제적으로 실현 가능하게 되었습니다. 무선 메쉬 프로토콜의 보급으로 설치의 복잡성이 줄어들고 2020년 이전에 건설된 기존 시설로의 개수 기회가 확대되고 있습니다. 반면에 사이버 보안 위협이 증가하고 반도체 공급 병목 현상이 지속되고 있으며 공급업체와 시설 소유자에게 단기적인 운영 위험이 존재합니다.

세계의 조명 제어 시스템 시장 동향과 인사이트

에너지 절약형 조명 시스템에 대한 수요 증가

세계의 시설에서는 기존의 형광등 설비에 비해 조명 에너지를 최대 80% 삭감하는 지능형 제어와 LED를 조합함으로써 운용 비용과 탄소 실적의 저감을 추구하고 있습니다. 입증된 산업 프로젝트는 도입 후 12개월에 조명 에너지를 87% 삭감한 사례가 있어 대규모 플랜트에서도 단기간에 투자 회수가 가능하다는 것을 뒷받침하고 있습니다. 재실검지, 자연광이용, 스케줄 제어에 의해 업무 흐름에 영향을 주지 않고 지속적인 최적화를 실현할 수 있기 때문에 광열비가 계속 상승하는 상황에서도 설비투자의 승인이 용이해집니다. 건물 소유자는 많은 프로젝트가 1 회계 연도 이내에 투자 회수를 실현하는 점을 높이 평가하고 있으며, 다른 건설 지출이 조사되는 가운데도 수요를 지속시키는 추풍이 되고 있습니다.

엄격한 건축물 에너지 기준 및 녹색 인증 의무

국제 에너지 절약 기준 2021(IECC 2021)은 상업시설에서 자동 꺼짐 기능과 자연광 대응 제어를 의무화하여 모든 업그레이드에서 필수 요건으로 전환했습니다. 캘리포니아 주 타이틀 24(2022년)는 4kW 이상의 프로젝트에서 수요 반응형 조광을 추진하여 사실상 모든 대규모 건축물에 대한 제어 시스템의 도입을 보장합니다. LEED 평가 시스템은 첨단 조명 제어에 포인트를 부여하고 규제 압력과 현재 ESG 대응 자산을 선호하는 자본 시장을 일치시킵니다. 규정 준수는 양도할 수 없는 요구사항이기 때문에 조명 제어 시스템 시장은 거시 경제의 변동을 완화하는 방어적인 성장 기반을 획득하고 있습니다.

초기 도입·통합 비용의 높이

종합적인 제어 시스템 리노베이션은 기본 LED 램프 교체의 2-3 배 자본을 필요로하기 때문에 중소기업은 장벽이됩니다. 복잡한 프로젝트에서는 숙련된 시운전 기술자가 필요하지만, 특히 성숙지역 이외에서는 인재 부족이 인건비를 밀어 올리고 있습니다. 연간 10만 831달러의 절약 효과가 있는 저명한 호텔 개수 사례조차도, 엄청난 자본과 1.62년의 회수 기간을 필요로 하고, 중소기업의 자금 조달 장벽을 부각하고 있습니다. 신흥 시장에서는 에너지 대출이 부족하기 때문에 자금 조달의 격차가 가장 큽니다.

부문 분석

2025년에는 하드웨어가 수익의 56.80%를 차지했습니다. 드라이버, 센서, 게이트웨이는 모든 지능형 업그레이드의 기반이 되기 때문입니다. 서비스 분야는 12.83%라는 가장 빠른 CAGR이 전망되고 있습니다. 대규모 도입에는 설계 컨설팅, 현장 시운전, 정기적 최적화가 필수적이기 때문입니다. AI 기반 분석은 지속적인 조정이 요구되므로 조명 제어 시스템의 서비스 시장 규모는 앞으로 더욱 확대될 전망입니다. 에너지 관리 공동 프로젝트(EMC)의 블루투스 메쉬 프로젝트(43개 지역에서 3,685대의 컨트롤러 도입)와 같은 세계 배포는 서비스 의존도가 높은 복잡성과 지속적인 수익 가능성을 보여줍니다.

전문 서비스는 장기 계약을 보장하고 단발 자본 프로젝트를 예측 가능한 현금 흐름으로 변환합니다. 펌웨어 갱신, 고장 분석, 에너지 보고는 기업이 외부 위탁하는 매니지드 서비스 계약의 대상이 되는 경우가 증가하고 있습니다. 그 결과, 하드웨어 벤더는 라이프사이클 계약을 번들링하여 조명 제어 시스템 시장을 부품 판매가 아닌 솔루션 에코시스템으로 인도하고 있습니다. 이 전략적 전환은 설계 및 지원 리소스가 부족한 기업의 진입 장벽을 높입니다.

유선 프로토콜은 2025년 시점에서 63.40%의 점유율을 유지해 미션 크리티컬한 공장이 요구하는 EMI 내성과 안정된 지연이 평가되었습니다. 네트워크 다운타임이 허용되지 않는 병원 및 데이터센터에서는 유선 DALI-2 설치에 연결되는 조명 제어 시스템 시장 규모가 여전히 큰 상황입니다. 엔지니어는 전용 배선의 결정 론적 성능과 고유한 물리적 보안을 강조합니다.

무선 도입은 14.85%의 연평균 복합 성장률(CAGR)로 차이를 줄이고 있습니다. 블루투스 메쉬는 자체 복구 경로와 스마트폰 기반의 커미셔닝을 제공하여 인건비를 크게 줄일 수 있습니다. Matter 생태계와의 통합은 주거용 및 상업용 디바이스를 공통 관리 쉘 하에서 연동시켜 사양 결정자의 수용을 가속화합니다. 2026년까지 계획된 Thread 1.4 업그레이드는 테두리 라우터의 유연성을 추가하여 시설 관리 팀은 배선 변경 없이 네트워크를 확장할 수 있습니다. 역사적 건축물이나 영업중의 소매점포 등, 정지시간이 제한되는 환경에서는 혼란의 저감이 큰 매력이 됩니다.

조명 제어 시스템 시장은 제공 형태(하드웨어, 소프트웨어, 서비스), 통신 프로토콜(유선, 무선), 설치 유형(신축, 리노베이션), 용도(옥외, 실내), 지역별로 세분화됩니다. 시장 예측은 금액(달러) 기준으로 제공됩니다.

지역별 분석

북미는 엄격한 에너지 절약 기준과 스마트 시티 도입의 선행으로 2025년에 34.10%의 수익 점유율을 차지했습니다. 조명 제어 시스템 시장은 투자 회수를 촉진하는 연방 정부의 효율화 프로그램과 세제 우대 조치의 혜택을 받고 있습니다. 센서 패키지를 대상으로 하는 유틸리티 리베이트 제도는 상업시설 리노베이션의 경제성을 더욱 높입니다. 캐나다 주는 미국 기준을 반영하고 있으며 멕시코의 산업 회랑에서는 마키라도라 확장에 조명 제어를 통합하여 운영비를 최소화하고 있습니다.

유럽은 2030년까지 확고한 탈탄소 목표로 기세를 유지하고 있습니다. 독일, 프랑스, 영국에서는 공공 부문 조달 규칙에 지능형 조명이 내장되어 있습니다. EU 택소노미 공개는 부동산 소유자에게 에너지 강도 감소를 입증할 의무를 발생시켜 센서를 풍부하게 갖춘 업그레이드로 자본을 유도합니다. DALI-2와 새롭게 등장한 ETSI EN 303 645 보안 프레임워크를 통한 표준화 노력은 여러 공급업체의 전개 위험을 줄이고 단일 시장 전반에 걸친 보급을 촉진합니다.

중동 및 아프리카에서는 2031년까지 연평균 복합 성장률(CAGR) 12.74%라는 가장 빠른 성장이 전망됩니다. 사우디아라비아와 UAE에서 건설중인 메가 시티에서는 제어 가능 조명기구가 처음부터 마스터 플랜에 통합되었습니다. 스마트 인프라를 위한 정부 예산은 석유 수입이 변동하더라도 프로젝트 파이프라인을 견조하게 유지합니다. 사하라 이남 아프리카에서는 전력망의 불안정성이 전압 저하 시 부하를 조광하는 센서 도입을 촉진하여 설비 보호와 조명기구의 수명 연장을 실현하고 있습니다. 개발 은행의 대출 지원은 초기 비용 장벽 해소에 기여하고 지속적인 수량 성장을 보장합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 에너지 절약형 조명 시스템에 대한 수요 증가

- 엄격한 건축물 에너지 기준 및 녹색 인증 의무

- LED 가격의 급격한 하락에 의한 ROI 확대

- 적응형 가로 조명을 활용한 스마트 시티 계획

- ESG 연동형 금융이 스마트 개수를 가속

- Li-Fi 도입 준비가 새로운 수익원을 개척

- 시장 성장 억제요인

- 초기 도입·통합 비용의 높이

- 멀티 벤더 환경에서의 상호 운용성의 과제

- 사이버 보안 및 데이터 프라이버시 위험

- 유자격 시운전 전문가 부족

- 공급망 분석

- 규제 상황

- 기술 전망(IoT 엣지 제어, AI, Li-Fi)

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장에 대한 거시경제적 요인의 평가

제5장 시장 규모와 성장 예측

- 제공별

- 하드웨어

- LED 드라이버

- 센서

- 스위치 및 디머

- 릴레이 유닛

- 게이트웨이 및 제어 패널

- 소프트웨어

- 서비스

- 하드웨어

- 통신 프로토콜별

- 유선

- 무선

- 설치 유형별

- 신축

- 리모델링

- 용도별

- 실내

- 상업용 사무실

- 산업 및 창고

- 주택용

- 호텔 및 레저

- 기타

- 옥외

- 도로 및 거리

- 건축 및 외관

- 스포츠 및 경기장

- 기타

- 실내

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 이집트

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 전략적 동향

- 기업 프로파일

- Signify(Philips Lighting)

- Acuity Brands

- Legrand

- Lutron Electronics

- ams OSRAM

- Schneider Electric

- Eaton(Cooper Lighting)

- Hubbell Lighting

- Honeywell

- Cisco Systems

- Siemens(Enlighted)

- Delta Electronics

- Panasonic

- Zumtobel Group

- Helvar

- Synapse Wireless

- WAGO

- Cree Lighting

- Leviton Manufacturing

- Digital Lumens

- ABB

제7장 시장 기회와 향후 전망

KTH 26.01.22The lighting control system market is expected to grow from USD 45.43 billion in 2025 to USD 51.15 billion in 2026 and is forecast to reach USD 92.53 billion by 2031 at 12.6% CAGR over 2026-2031.

Accelerated growth reflects mandated energy-efficiency requirements, the spread of smart city programs, and wider use of IoT-enabled building automation that turns luminaires into data sources. Governments now anchor automatic shut-off, daylight-responsive dimming, and occupancy sensing in building standards, which creates non-discretionary demand. Price erosion in LED components has shortened payback periods, making comprehensive controls economically viable even for smaller facilities. Wireless mesh protocols have reduced installation complexity, opening retrofit opportunities in stock built before 2020. At the same time, escalating cybersecurity threats and lingering semiconductor supply bottlenecks present near-term operational risks for suppliers and facility owners.

Global Lighting Control System Market Trends and Insights

Growing Demand for Energy-Efficient Lighting Systems

Facilities worldwide pursue lower operating costs and carbon footprints by pairing LEDs with intelligent controls that trim lighting energy as much as 80% compared with legacy fluorescent installations. Documented industrial projects have reached 87% lighting-energy savings in the first twelve months, underscoring quick payback even in large plants. Occupancy sensing, daylight harvesting, and scheduling allow continuous optimisation without impacting workflow, which makes capital approval easier when utility prices keep rising. Building owners value that many projects now return cash within a single fiscal year, creating momentum that sustains demand when other construction outlays are under scrutiny.

Stringent Building-Energy Codes and Green Certification Mandates

The International Energy Conservation Code 2021 requires automatic shut-off and daylight-responsive controls in commercial spaces, converting optional upgrades into mandatory scope. California Title 24 (2022) pushes demand-responsive dimming on projects above 4 kW, guaranteeing control deployment in virtually every large build. LEED rating systems award points for advanced lighting controls, aligning regulatory pressure with capital markets that now prioritise ESG-ready assets. Because compliance is non-negotiable, the lighting control system market gains a defensive growth pillar that softens macro-economic swings.

High Upfront Installation and Integration Cost

Comprehensive control retrofits still command two- to three-times the capital of basic LED lamp swaps, which discourages smaller businesses. Complex projects rely on skilled commissioning engineers whose limited availability inflates labour fees, especially outside mature regions.Even high-profile hotel retrofits that now yield USD 100,831 annual savings required sizeable capital and a 1.62-year payback, highlighting the cash hurdle that smaller enterprises face. Financing gaps remain widest in emerging markets where energy loans are scarce.

Other drivers and restraints analyzed in the detailed report include:

- Rapid LED Price Erosion Expanding ROI

- Smart-City Programs Using Adaptive Street Lighting

- Interoperability Issues Across Multi-Vendor Ecosystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 56.80% revenue in 2025 as drivers, sensors, and gateways form the backbone of any intelligent upgrade. Services are poised for the fastest 12.83% CAGR because every significant deployment requires design consultation, site commissioning, and periodic optimisation. The lighting control system market size for services is projected to gain momentum as AI-based analytics demand continuous tuning. Global roll-outs such as Energy Management Collaborative's Bluetooth Mesh project, which involved 3,685 controllers in 43 areas, illustrate service-heavy complexity and recurring revenue potential.

Professional services secure long-term contracts that convert one-time capital projects into predictable cash flows. Firmware updates, fault analytics, and energy reporting increasingly fall under managed-service agreements that enterprises outsource. As a result, hardware vendors bundle lifecycle contracts, pushing the lighting control system market toward solution ecosystems rather than component sales. This strategic shift raises entry barriers for firms that lack design and support resources.

Wired protocols preserved 63.40% share in 2025, valued for EMI immunity and stable latency that mission-critical factories demand. The lighting control system market size tied to wired DALI-2 installations remains considerable among hospitals and data centres where network downtime is unacceptable. Engineers favour deterministic performance and inherent physical security of dedicated cabling.

Wireless deployments are closing the gap at a 14.85% CAGR. Bluetooth Mesh offers self-healing paths and smartphone-based commissioning that slash labour costs. Integration into the Matter ecosystem aligns residential and commercial devices under common management shells, which accelerates specifier acceptance. Thread 1.4 upgrades planned by 2026 will add border-router flexibility, allowing facility teams to scale networks without rewiring. Reduced disruption is compelling for heritage sites and live retail stores where shutdown time is limited.

Lighting Control System Market is Segmented by Offering (Hardware, Software, Services), Communication Protocol (Wired, Wireless), Installation Type (New Construction, Retrofit), Application (Outdoor, Indoor) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 34.10% revenue in 2025 due to strict energy codes and early smart-city adoption. The lighting control system market benefits from federal efficiency programmes and tax incentives that improve investment payback. Utility rebate schemes covering sensor packages further sweeten economics for commercial retrofits. Canadian provinces mirror United States standards, while Mexico's industrial corridors integrate lighting controls into maquiladora expansions to minimise operational spend.

Europe maintains momentum with firm decarbonisation targets set for 2030. Germany, France, and the United Kingdom embed intelligent lighting in public-sector procurement rules. EU taxonomy disclosures oblige property owners to prove energy intensity reductions, which steers capital toward sensor-rich upgrades. Standardisation efforts through DALI-2 and the emerging ETSI EN 303 645 security framework make multi-vendor deployments less risky, reinforcing uptake across the single market.

The Middle East and Africa post the fastest 12.74% CAGR through 2031. Mega-cities under construction in Saudi Arabia and the UAE incorporate control-ready luminaires into master plans from the start. Government budgets earmarked for smart infrastructure keep project pipelines robust even when oil revenues fluctuate. In sub-Saharan Africa, grid instability motivates adoption of sensors that dim loads during voltage dips, protecting equipment and extending luminaire life. Financing backed by development banks helps bridge initial cost hurdles, ensuring sustained volume growth.

- Signify (Philips Lighting)

- Acuity Brands

- Legrand

- Lutron Electronics

- ams OSRAM

- Schneider Electric

- Eaton (Cooper Lighting)

- Hubbell Lighting

- Honeywell

- Cisco Systems

- Siemens (Enlighted)

- Delta Electronics

- Panasonic

- Zumtobel Group

- Helvar

- Synapse Wireless

- WAGO

- Cree Lighting

- Leviton Manufacturing

- Digital Lumens

- ABB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for energy-efficient lighting systems

- 4.2.2 Stringent building-energy codes and green certification mandates

- 4.2.3 Rapid LED price erosion expanding ROI

- 4.2.4 Smart-city programs using adaptive street lighting

- 4.2.5 ESG-linked finance accelerating smart retrofits

- 4.2.6 Li-Fi readiness unlocking new revenue streams

- 4.3 Market Restraints

- 4.3.1 High upfront installation and integration cost

- 4.3.2 Interoperability issues across multi-vendor ecosystems

- 4.3.3 Cyber-security and data-privacy risks

- 4.3.4 Shortage of qualified commissioning professionals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (IoT-edge controls, AI, Li-Fi)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.1.1 LED Drivers

- 5.1.1.2 Sensors

- 5.1.1.3 Switches and Dimmers

- 5.1.1.4 Relay Units

- 5.1.1.5 Gateways and Control Panels

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Communication Protocol

- 5.2.1 Wired

- 5.2.2 Wireless

- 5.3 By Installation Type

- 5.3.1 New Construction

- 5.3.2 Retrofit

- 5.4 By Application

- 5.4.1 Indoor

- 5.4.1.1 Commercial Offices

- 5.4.1.2 Industrial and Warehousing

- 5.4.1.3 Residential

- 5.4.1.4 Hospitality and Leisure

- 5.4.1.5 Others

- 5.4.2 Outdoor

- 5.4.2.1 Roadway and Street

- 5.4.2.2 Architectural and Facade

- 5.4.2.3 Sports and Stadium

- 5.4.2.4 Others

- 5.4.1 Indoor

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.2.5 Egypt

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Strategic Moves

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Signify (Philips Lighting)

- 6.4.2 Acuity Brands

- 6.4.3 Legrand

- 6.4.4 Lutron Electronics

- 6.4.5 ams OSRAM

- 6.4.6 Schneider Electric

- 6.4.7 Eaton (Cooper Lighting)

- 6.4.8 Hubbell Lighting

- 6.4.9 Honeywell

- 6.4.10 Cisco Systems

- 6.4.11 Siemens (Enlighted)

- 6.4.12 Delta Electronics

- 6.4.13 Panasonic

- 6.4.14 Zumtobel Group

- 6.4.15 Helvar

- 6.4.16 Synapse Wireless

- 6.4.17 WAGO

- 6.4.18 Cree Lighting

- 6.4.19 Leviton Manufacturing

- 6.4.20 Digital Lumens

- 6.4.21 ABB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment