|

시장보고서

상품코드

1851755

전술 무인기(UAV) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Tactical UAV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

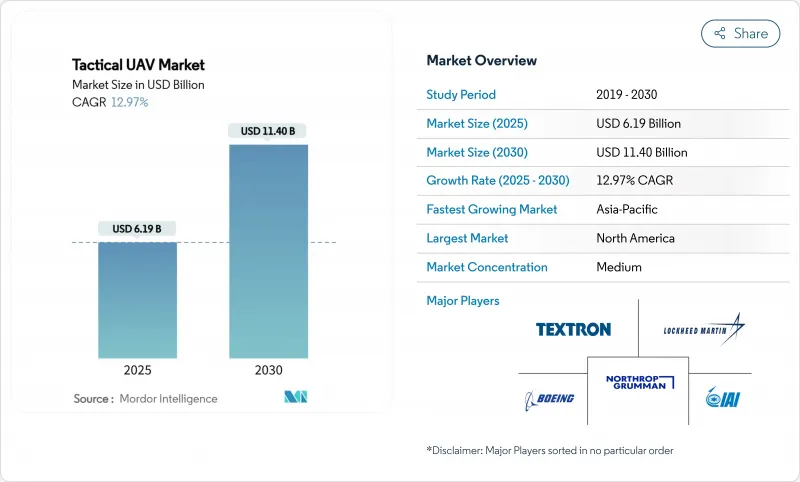

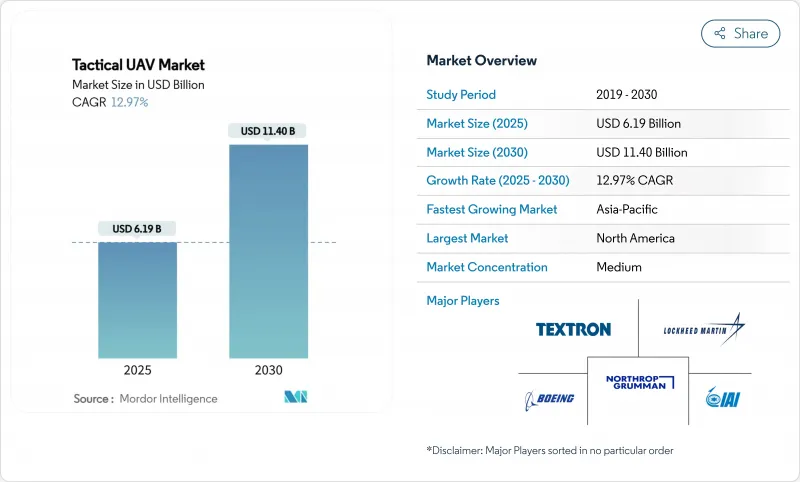

전술 UAV 시장 규모는 2025년에 61억 9,000만 달러로 평가되었고, 2030년에 114억 달러로 확대될 것으로 예측되며, CAGR은 12.97%를 나타낼 전망입니다.

상승 추세는 정보 수집, 정밀 타격, 전력 증강 역할을 위한 무인 시스템을 우선시하는 글로벌 방위 현대화 프로그램을 반영합니다. 자율 플랫폼에 대한 증가하는 예산 배정, 최근 고강도 분쟁에서 얻은 교훈, 항공 승무원 위험 감소 추진이 수요를 강화하고 있습니다. 유사한 유인 항공기에 비해 전술 드론의 낮은 수명 주기 비용 구조와 전기 추진, 소형화 센서, AI 기반 자율성의 급속한 발전 역시 군 구매자들의 관심을 끌고 있습니다. 동시에 공급업체들은 사이버 취약성과 주파수 대역 혼잡이 작전 확장성을 위협함에 따라 희토류 부품 공급망을 확보하고 전자전으로부터 지휘통제 연결을 강화하기 위해 경쟁하고 있습니다.

세계의 전술 UAV 시장 동향 및 인사이트

높아지는 방위 현대화 예산

주요 군대는 전투력을 증강시키면서 항공 승무원 위험을 최소화하는 무인 시스템으로 조달 방향을 전환하고 있습니다. 미국 국방부의 2025년 가속화된 드론 획득 경로는 이러한 우선순위 재조정을 보여주고 국내 프로그램에 새로운 자금을 투입합니다. 최근 러시아-우크라이나 교전에서 얻은 교훈은 표적 획득 및 정밀 타격을 위한 소형 전술 드론의 가치를 재확인시켜, 유럽 동맹국들이 무인 항공 시스템을 능력 로드맵에 추가하도록 촉발했습니다. 신흥 시장도 이 패턴을 따르고 있는데, 전술 플랫폼은 유인 항공기에 비해 진입 비용이 낮으면서도 유사한 감시 범위를 제공하기 때문입니다. 안전한 데이터 링크와 탄력적인 공급망에 대한 병행 투자는 단일 공급원 부품 위험 노출을 줄이고 강화되는 국가 안보 규정을 준수하기 위한 것입니다. 이러한 현대화 프로젝트들은 종합적으로 2020년대 말까지 두 자릿수 수요 증가를 유지할 것으로 예상됩니다.

ISR 및 실시간 데이터에 대한 수요 급증

지휘관들은 지속적인 정보, 감시, 정찰(ISR)에 의존하여 의사 결정 주기를 단축합니다. 전술 무인기 함대는 이제 다중 스펙트럼 센서를 탑재해 암호화된 영상을 이동 지휘소로 직접 전송함으로써 관측-정찰-결정-행동 루프를 수 시간에서 수 분으로 단축합니다. 여러 NATO 회원국 내 군집형 프로젝트는 수백 대의 상호운용 가능한 드론이 표적 데이터를 자율적으로 공유하는 방안을 모색하며, 분산된 전장 전반의 상황 인식을 확대합니다. 민간 기관들도 대규모 행사 군중 감시 및 자연재해 평가를 위해 유사한 ISR 능력을 도입하며 고객 기반을 더욱 확장하고 있습니다. 탑재 프로세서의 성능 향상으로 엣지 수준의 물체 인식이 가능해져 대역폭 요구량과 운영자 업무량이 감소했습니다. 이로 인한 운영 유연성 덕분에 전술 무인기 시장 수요는 핵심 방위 분야를 넘어 지속적 확장을 이어갈 전망입니다.

혼잡한 주파수 대역과 수출 규제의 한계

전술 무인항공기 작전에는 안정적인 지휘통제 및 데이터 링크 대역폭이 필수적입니다. 5G 네트워크, 마이크로파 통신, 전자전 방해기의 확산은 이미 혼잡한 주파수 할당을 더욱 복잡하게 만들어 임무 수행 중 통신 단절을 초래할 수 있는 간섭 위험을 높입니다. 규제 장벽은 수출을 더욱 복잡하게 만듭니다. 국제무기거래규정(ITAR)은 많은 첨단 무인기 기술을 방위 물자로 분류하여 공급업체가 개별 허가를 취득하고 해외 구매자를 위한 별도 변형을 설계하도록 의무화합니다. 주파수 부족과 규제 감독이라는 이중 압박은 거래 주기를 늦추고, 규정 준수 비용을 증가시키며, 일부 소규모 공급업체를 특정 해외 시장에서 퇴출시킵니다.

부문 분석

2024년 전술 무인항공기 시장은 고정익 드론이 61.32%를 차지하며 주도했습니다. 이는 국경 순찰 및 전역 정보·감시·정찰(ISR) 임무에 적합한 장시간 비행 성능 덕분입니다. 운영사들은 공중 급유 없이 8-12시간 작전이 가능한 순항 효율성을 중시합니다. 그러나 하이브리드 수직이착륙(VTOL) 설계는 활주로 없이 수직 이륙이 가능하면서도 고정익의 항속 성능을 결합해 15.62% CAGR로 가장 빠른 성장률을 기록 중입니다. 이러한 항공기는 임시 개활지나 함정 갑판에서 발진한 후 효율적인 전진 비행으로 전환할 수 있어 특수작전부대와 해상작전단에서 매력적인 선택지입니다. 회전익 드론은 인질 구출 및 도시 전투 지원 임무 시 정밀 호버링에 여전히 필수적이지만, 짧은 작전 반경으로 인해 주로 근접 전술 교전에 한정되어 채택됩니다. 공급업체들은 플러그 앤 플레이 방식의 탑재체 장착이 가능한 모듈식 기체를 강조하며, 이를 통해 고객은 새로운 항공기 구매 없이도 정찰, 전자전, 소구경탄약 임무 간 자산을 재할당할 수 있습니다.

하이브리드 수직이착륙(VTOL) 트렌드는 배터리 에너지 밀도 향상과 소형 기어드 터빈 엔진의 발전으로 탑재량 대비 중량 비율이 개선되며 이점을 얻고 있습니다. 해군 계획자들은 고정익 항공기 발사대 작전이 불가능한 해상 상태에서도 수직 발사 능력의 중요성을 강조합니다. 육군은 한편으로 활주로 독립형 드론을 활용해 기존 비행장 범위를 벗어난 분산 부대에 ISR(정보·감시·정찰)을 제공하며, 분산 작전으로의 교리 전환과 맞물려 있습니다. 그 결과 전술 무인기 시장은 2030년까지 기존 고정익 자산에서 하이브리드 개념으로의 지속적인 점유율 이동을 예상하고 있습니다.

150-600kg 중량대의 중형 모델은 2024년 전술 무인기 시장 규모의 42.25%를 차지하며, 탑재량과 원정 물류 사이의 균형을 이루고 있습니다. 이 차량들은 다중 센서 터렛, 합성개구레이더(SAR), 암호화 중계 노드를 탑재하여 최대 18시간 동안 여단급 상황 인식을 지원합니다. 그러나 5kg 미만의 마이크로/나노 항공기는 가장 역동적인 하위 범주로, 부대가 분대급 군집을 실험하며 영상 공유, 실내 공간 매핑, 대공 방어 체계에 대한 기만 기동을 수행함에 따라 16.32%의 연평균 성장률(CAGR)을 보이고 있습니다. 소형 짐벌과 저 SWaP(크기·무게·전력) 무선 기술의 도약은 과거 대형 드론에만 가능했던 ISR(정보·감시·정찰) 기능을 해제하여 소대 계층까지 정보를 확장합니다.

경전술형(20-150kg)은 밀집 지형에서 자체 정찰이 필요한 헬기 수송 부대의 특수 요구를 충족합니다. 상위급인 600kg 이상의 대형 전술 드론은 장시간 해상 순찰 및 원격 타격을 수행하지만, 대형으로 인해 전방 기지에서의 전개가 복잡하고 군집 전술 적용이 제한됩니다. 모든 등급에서 배터리 혁신과 경량 복합재 구조는 은밀성이나 탑재량을 희생하지 않으면서도 지속 시간을 향상시키고 있습니다. 소형화 추세는 작전 설계 원칙을 재정의하여 의사결정 품질 데이터를 접촉 지점에 더 가깝게 전달하고, 전술 무인기 시장의 모든 지휘 계층으로의 침투를 확대할 것입니다.

지역 분석

북미는 2024년 전 세계 전술 무인항공기 시장 매출의 31.87%를 차지했으며, 이는 세계 최대 규모의 국방 예산, 성숙한 항공우주 공급망, 그리고 현재 국내 드론 제조를 우선시하는 지원적 규제 환경에 기반합니다. 이 지역의 다년간 조달 프로그램은 기체 제조사, 센서 업체, 데이터 링크 공급업체에 예측 가능한 수요를 제공하며, 민간 기관들은 인프라 점검 및 산불 감시를 위한 BVLOS(시야 외 비행) 운영을 확대하고 있습니다. 캐나다의 차세대 감시 드론 투자와 멕시코의 남부 국경 감시 수요가 대륙 전체 물량을 더욱 견인하고 있습니다.

아시아태평양 지역은 중국, 인도, 한국의 국방 예산 증가, 국경 분쟁, 자체 R&D로 13.39%의 연평균 성장률(CAGR)을 기록하며 가장 빠른 성장세를 보입니다. 현지 주요 업체들은 비용 경쟁력 있는 기체에 지역별 맞춤형 센서 패키지를 통합해 국내 계약을 확보하며 서구 수출업체들에 도전장을 내밀고 있습니다. 일본 전자 기업과 국방부 간 협력은 AI 기반 항법 솔루션 개발을 가속화하고 있으며, 호주의 광활한 해상 접근로는 장시간 항해가 가능한 해양 순찰 드론 수요를 유지하고 있습니다. 이처럼 지역 전술 무인기 시장은 안보적 필요성과 산업 정책적 인센티브 모두로부터 추진력을 얻고 있습니다.

유럽은 유럽 방위 기금(EDF) 하의 협력 프로그램이 기술 주권을 촉진하며 꾸준한 확장을 유지합니다. 회원국들은 도시 정찰 및 대무인기(C-UAS) 전문 분야를 위한 초소형 무인기(micro-UAV)를 조달하여 외부 공급업체 의존도를 완화합니다. 중동과 아프리카는 영토 분쟁과 반군 진압 임무가 구매를 촉진하는 신흥 시장으로, 종종 에너지 수익이나 다자간 원조를 통해 자금이 조달됩니다. 터키와 이스라엘 제조사들은 지역 분쟁에서의 작전 경험을 바탕으로 사막 환경에 맞춤화된 비용 효율적인 시스템을 공급합니다. 이러한 지역적 역학은 종합적으로 판매 채널을 다각화하고 글로벌 전술 무인항공기 시장의 장기적 회복탄력성을 뒷받침합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 확대하는 방위 현대화 예산

- ISR 및 실시간 데이터 수요 급증

- 국경 경비와 대 테러 작전

- 유인 자산 대비 낮은 수명주기 비용

- AI 기반 군집 및 팀 작전 교리

- 해군 갑판 기반 발사 및 회수 요구사항

- 시장 성장 억제요인

- 혼잡한 스펙트럼 및 수출 통제 제한

- 높은 초기 조달 비용과 MRO 비용

- GPS 스푸핑/사이버 전자전 취약성

- 희토류 집약적 센서 공급 위험

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 플랫폼별

- 고정익

- 회전익

- 하이브리드 VTOL

- 중량 클래스별

- 마이크로/나노(5kg 미만)

- 미니(5-20kg)

- 경전술(20-150kg)

- 중형 전술(150-600kg)

- 대형 전술(600kg 이상)

- 범위별

- 근거리(50km 미만)

- 중거리(50-200km)

- 장거리(200km 이상)

- 추진 유형별

- 전기

- 하이브리드

- 기존(ICE)

- 용도별

- 군사

- 법 집행

- 재해 및 긴급 대응

- 환경 모니터링

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 이스라엘

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SZ DJI Technology Co. Ltd.

- Aeronautics Ltd.

- General Atomics

- BAYKAR AS

- BlueBird Aero Systems Ltd.

- Elbit Systems Ltd.

- AeroVironment, Inc.

- Israel Aerospace Industries Ltd.

- The Boeing Company

- Safran

- Leonardo SpA

- Textron Inc.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Saab AB

- Kratos Defense & Security Solutions, Inc.

- Thales Group

제7장 시장 기회와 장래의 전망

HBR 25.11.25The tactical UAV market size stands at USD 6.19 billion in 2025 and is forecasted to advance to USD 11.40 billion by 2030, translating into a 12.97% CAGR.

The upward trajectory reflects global defense-modernization programs prioritizing unmanned systems for intelligence gathering, precision strike, and force-multiplication roles. Growing allocations to autonomous platforms, lessons learned from recent high-intensity conflicts, and the push to reduce aircrew risk reinforce demand. The lower life-cycle cost profile of tactical drones versus comparable manned aircraft and rapid advances in electric propulsion, miniaturized sensors, and AI-enabled autonomy also draws military buyers. At the same time, suppliers are racing to secure rare-earth component chains and to harden command-and-control links against electronic warfare, as cyber vulnerabilities and spectrum congestion threaten operational scalability.

Global Tactical UAV Market Trends and Insights

Growing Defense-Modernization Budgets

Major armed forces are shifting procurement toward unmanned systems that augment combat power while minimizing aircrew risk. The US Department of Defense's 2025 accelerated drone acquisition pathway illustrates this re-prioritization and channels fresh funding into domestic programs. Lessons from recent Russo-Ukrainian engagements have reinforced the value of small tactical drones for target acquisition and precision strikes, prompting allied European nations to add uncrewed aerial systems to capability roadmaps. Emerging markets echo this pattern because tactical platforms offer a lower entry cost versus manned aircraft yet deliver comparable surveillance coverage. Parallel investments in secure datalinks and resilient supply chains aim to reduce exposure to single-source component risks and to comply with tightening national-security regulations. These modernization projects should collectively maintain double-digit demand growth through the end of the decade.

Soaring Demand for ISR and Real-Time Data

Commanders rely on persistent intelligence, surveillance, and reconnaissance to compress decision cycles. Tactical UAV fleets now carry multi-spectral sensors that stream encrypted video directly to mobile command posts, trimming the observe-orient-decide-act loop from hours to minutes. Swarm initiatives within several NATO member states explore hundreds of interoperable drones that share target data autonomously, broadening situational awareness over dispersed battlefields. Civil agencies adopt similar ISR capabilities for large-event crowd oversight and natural-disaster assessment, further expanding the customer base. Improvements in on-board processors permit edge-level object recognition, reducing bandwidth needs and operator workload. The resulting operational agility positions the tactical UAV market demand for sustained expansion even outside core defense niches.

Congested Spectrum and Export-Control Limits

Tactical UAV operations require dependable command, control, and data-link bandwidth. Proliferation of 5G networks, microwave communications, and electronic-warfare jammers crowds already busy frequency allocations, raising interference risks that could sever links mid-mission. Regulatory barriers further complicate exports; International Traffic in Arms Regulations classify many advanced UAV technologies as defense articles, obliging vendors to secure individual licenses and to engineer different variants for overseas buyers. The twin pressures of spectrum scarcity and regulatory oversight slow deal cycles, inflate compliance costs, and force some smaller suppliers out of specific foreign markets.

Other drivers and restraints analyzed in the detailed report include:

- Border Security and Counter-Terror Operations

- Lower Life-Cycle Cost versus Manned Assets

- High Upfront Procurement and MRO Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed-wing drones dominated the tactical UAV market in 2024, capturing 61.32%, thanks to long-endurance profiles suitable for border patrol and theater-wide ISR missions. Operators value cruise efficiency that permits 8-12-hour sorties without aerial refueling. Yet hybrid VTOL designs register the fastest ascent at a 15.62% CAGR because they combine runway-free vertical lift with fixed-wing range performance. These aircraft can launch from improvised clearings or naval decks, then transition to efficient forward flight, making them attractive for special-operations forces and maritime task groups. Rotary-wing drones remain indispensable for precision hovering during hostage-rescue and urban-combat support roles, although their shorter reach confines adoption mainly to close-tactical engagements. Suppliers emphasize modular airframes that accept plug-and-play payloads, enabling customers to re-task assets between reconnaissance, electronic-warfare, and small-diameter-munition missions without purchasing new air vehicles.

The hybrid VTOL trend benefits from maturing battery energy density and compact geared-turbine engines that boost payload-to-weight ratios. Naval planners underscore the importance of vertical launch capability under sea states that preclude fixed-wing catapult operations. Land forces, meanwhile, exploit runway-independent drones to deliver ISR for dispersed units beyond established airfields, dovetailing with doctrinal shifts toward distributed operations. As a result, the tactical UAV market anticipates sustained share migration from legacy fixed-wing assets toward hybrid concepts through 2030.

Medium models in the 150 to 600 kg bracket represented 42.25% of the tactical UAV market size in 2024, striking a balance between payload capacity and expeditionary logistics. These vehicles carry multi-sensor turrets, synthetic-aperture radars, and encrypted relay nodes, supporting brigade-level situational awareness for up to 18 hours. Yet micro/nano aircraft under 5 kg are the most dynamic subset, advancing at a 16.32% CAGR as forces experiment with squad-level swarms that share imagery, map interior spaces, and execute decoy maneuvers against air defenses. Technological leaps in miniature gimbals and low-SWaP radios unlock ISR functions once reserved for larger drones, extending intelligence to the platoon echelon.

Light tactical categories (20 to 150 kg) fill niche requirements for helicopter-borne insertion units that need organic reconnaissance in dense terrain. At the high end, heavy tactical drones above 600 kg undertake long-endurance maritime patrol and stand-off strike; however, their size complicates deployment from forward locations and limits suitability for swarm tactics. Across all classes, battery innovation and lightweight composite structures are improving endurance without sacrificing stealth or payload. The miniaturization trend is set to redefine force-design principles, moving decision-quality data closer to the point of contact and amplifying the tactical UAV market's penetration into every command level.

The Tactical UAV Market Report is Segmented by Platform (Fixed-Wing, Rotary-Wing, and Hybrid VTOL), Weight Class (Micro/Nano, Mini, Light, and More), Range (Short, Medium, and Extended), Propulsion (Electric, Hybrid, and Conventional), Application (Military, Law Enforcement, Emergency Response, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 31.87% of the global tactical UAV market revenue in 2024, underpinned by the world's largest defense appropriation, mature aerospace supply chains, and a supportive regulatory climate that now prioritizes domestic drone manufacturing. The region's multi-year procurement programs provide predictable demand for airframe producers, sensor houses, and data-link vendors, while civilian agencies expand BVLOS operations for infrastructure inspection and wildfire monitoring. Canada's investment in next-generation surveillance drones and Mexico's southern-border surveillance needs further reinforcement of continental volume.

Asia-Pacific exhibits the fastest growth at a 13.39% CAGR, propelled by rising defense budgets, border skirmishes, and indigenous R&D in China, India, and South Korea. Local primes integrate cost-competitive airframes with region-specific sensor suites, capturing domestic contracts and challenging Western exporters. Partnerships between Japanese electronics firms and defense ministries accelerate AI-based navigation solutions, and Australia's vast maritime approaches sustain demand for long-endurance oceanic patrol drones. The regional tactical UAV market thus gains momentum from both security imperatives and industrial-policy incentives.

Europe maintains steady expansion as collaborative programs under the European Defense Fund promote technology sovereignty. Member states procure micro-UAVs for urban reconnaissance and counter-UAS specialties, mitigating reliance on external suppliers. The Middle East and Africa represent emerging frontiers where territorial disputes and counter-insurgency missions spur acquisitions, often financed through energy revenue or multilateral aid. Turkish and Israeli manufacturers, benefiting from operational experience in regional conflicts, supply cost-effective systems tailored for desert environments. Collectively, these geographic dynamics diversify sales channels and underpin the long-term resilience of the global tactical UAV market.

- SZ DJI Technology Co. Ltd.

- Aeronautics Ltd.

- General Atomics

- BAYKAR A.S.

- BlueBird Aero Systems Ltd.

- Elbit Systems Ltd.

- AeroVironment, Inc.

- Israel Aerospace Industries Ltd.

- The Boeing Company

- Safran

- Leonardo S.p.A.

- Textron Inc.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Saab AB

- Kratos Defense & Security Solutions, Inc.

- Thales Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing defense-modernization budgets

- 4.2.2 Soaring demand for ISR and real-time data

- 4.2.3 Border security and counter-terror ops

- 4.2.4 Lower life-cycle cost versus manned assets

- 4.2.5 AI-enabled swarm and teaming doctrines

- 4.2.6 Naval deck-based launch and recovery needs

- 4.3 Market Restraints

- 4.3.1 Congested spectrum and export-control limits

- 4.3.2 High upfront procurement and MRO cost

- 4.3.3 Susceptibility to GPS spoofing/cyber-EW

- 4.3.4 Rare-earth-intensive sensor supply risks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Fixed-wing

- 5.1.2 Rotary-wing

- 5.1.3 Hybrid VTOL

- 5.2 By Weight Class

- 5.2.1 Micro/Nano (Less than 5 kg)

- 5.2.2 Mini (5 to 20 kg)

- 5.2.3 Light Tactical (20 to 150 kg)

- 5.2.4 Medium Tactical (150 to 600 kg)

- 5.2.5 Heavy Tactical (Greater than 600 kg)

- 5.3 By Range

- 5.3.1 Short-Range (Less than 50 km)

- 5.3.2 Medium-Range (50 to 200 km)

- 5.3.3 Extended-Range (Greater than 200 km)

- 5.4 By Propulsion Type

- 5.4.1 Electric

- 5.4.2 Hybrid

- 5.4.3 Conventional (ICE)

- 5.5 By Application

- 5.5.1 Military

- 5.5.2 Law Enforcement

- 5.5.3 Disaster and Emergency Response

- 5.5.4 Environmental Monitoring

- 5.5.5 Other Applications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Israel

- 5.6.5.1.4 Turkey

- 5.6.5.1.5 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SZ DJI Technology Co. Ltd.

- 6.4.2 Aeronautics Ltd.

- 6.4.3 General Atomics

- 6.4.4 BAYKAR A.S.

- 6.4.5 BlueBird Aero Systems Ltd.

- 6.4.6 Elbit Systems Ltd.

- 6.4.7 AeroVironment, Inc.

- 6.4.8 Israel Aerospace Industries Ltd.

- 6.4.9 The Boeing Company

- 6.4.10 Safran

- 6.4.11 Leonardo S.p.A.

- 6.4.12 Textron Inc.

- 6.4.13 Lockheed Martin Corporation

- 6.4.14 Northrop Grumman Corporation

- 6.4.15 Saab AB

- 6.4.16 Kratos Defense & Security Solutions, Inc.

- 6.4.17 Thales Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment