|

시장보고서

상품코드

1851758

홍채 인식 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Iris Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

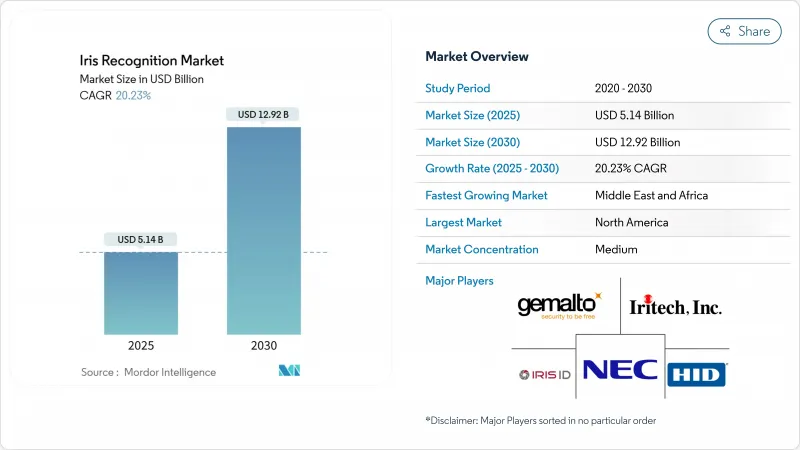

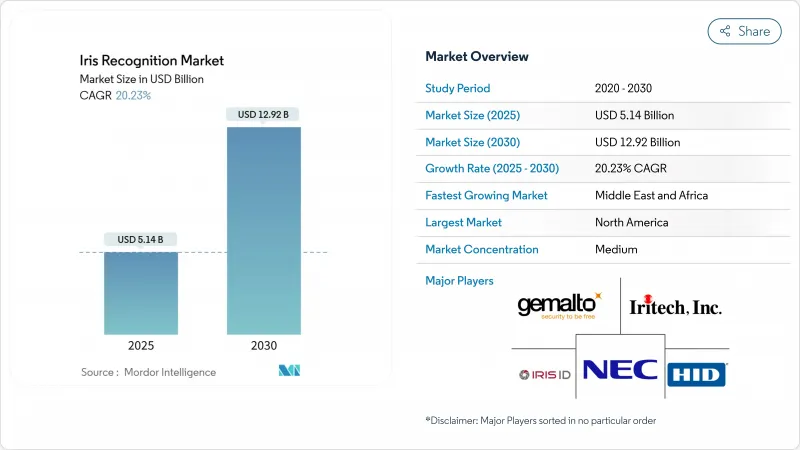

홍채 인식 시장 규모는 2025년에 51억 4,000만 달러로 평가되었고 2030년에는 129억 2,000만 달러로 확대될 것으로 예상되며, CAGR은 20.23%를 나타낼 전망입니다.

이 견고한 성장 궤적은 해당 기술이 정부 기관의 틈새 시장 적용을 넘어 일상적인 소비자 환경으로 확대된 과정을 보여줍니다. 비접촉 인증 수요 증가, 사이버 위협 노출 확대, 규제 기관의 강화된 규정 준수 요구사항이 은행, 의료, 여행, 소비자 가전 분야 전반에 걸친 기술 채택을 가속화했습니다. 하드웨어는 여전히 최대 비용 항목이지만, 클라우드 네이티브 매칭 엔진의 속도 향상과 중견 구매자의 진입 장벽 완화로 소프트웨어의 전략적 중요성이 커지고 있습니다. 아시아태평양 지역은 대규모 국가 신원 확인 프로그램을 통해 선점자 우위를 점하고 있으며, 중동은 공항 현대화 및 관광 촉진 정책에 힘입어 가장 빠른 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 경쟁 심화는 이제 알고리즘 정확도, 다중 모드 통합, 진화하는 데이터 주권 규정을 견딜 수 있는 프라이버시 중심 설계 기능 중심으로 전개되고 있습니다.

세계의 홍채 인식 시장 동향 및 인사이트

아시아의 확대되는 국가 신분증 및 전자 여권 프로그램

아시아태평양 지역 정부들은 공공 서비스 제공 및 금융 포용성 강화를 위해 홍채 기반 디지털 신원 플랫폼을 지속적으로 확장하고 있습니다. 인도의 DigiLocker 업그레이드를 통해 기업체는 Aadhaar 데이터베이스를 통해 직원 신원 정보를 확인할 수 있게 되어, 대상 기반이 개인 시민을 넘어 확대되었습니다. 태국 보건 당국은 이주 노동자를 위한 다중 모드 등록 키오스크를 도입하여 홍채 스캔을 예방접종 및 복지 수급 자격과 연계했습니다. 대량 생산 시 광학 모듈 비용이 한 자릿수 달러 수준으로 하락하면서 예산 제약 기관에도 진입점이 마련되었습니다. 등록 추진력이 지속됨에 따라 공급업체들은 유지보수 계약과 성능 기준 강화에 따른 주기적 센서 교체 주기로 지속적인 수익을 창출할 수 있을 것으로 전망합니다.

중동 지역 통로에서의 국경 통제 지출 증가

걸프 국가들은 주요 공항에서 보안 수준과 여객 흐름 목표를 균형 있게 조정하기 위해 대규모 홍채 인식 시스템을 도입하고 있습니다. IDEMIA와 협력하여 구현된 UAE의 eGate 프로그램은 원격 홍채 캡처 기술을 활용해 입국 심사대를 거치지 않고도 거주자와 방문객을 처리합니다. 사우디아라비아의 ‘비전 2030’ 태스크포스는 모든 신규 터미널에 다중 모드 생체 인식 시스템을 의무화하여 Invixium과 같은 공급업체들이 신속한 맞춤화를 위해 현지 조립 라인 구축을 추진하도록 하고 있습니다. 이에 따른 조달 파이프라인은 시간당 수천 명의 여행객을 처리하면서 출입국 관리관에게 감사 등급 증거를 기록할 수 있는 고처리량 스캐너와 클라우드 지원 매칭 엔진을 선호합니다.

공항 다중 모드 생체 인식 허브의 높은 자본 지출

공항은 기존 검문소에 홍채, 얼굴, 지문 옵션을 포함한 다중 모드 포드를 개조할 때 막대한 초기 비용에 직면합니다. 미국 교통안전청(TSA) 시범 운영 결과 승객 처리량 증가는 확인되었으나, 전용 차선, LED 안전 조명, 중앙 매칭 엔진으로의 전용 광섬유 백홀이 필요했습니다. 소규모 지역 공항들은 승객량이 투자 회수를 정당화할 때까지 도입을 연기하면서, 공급업체들이 모듈식 사용량 기반 요금 모델로 대응해야 하는 2단계 도입 곡선을 형성하고 있습니다.

부문 분석

정밀 광학 장치, 제어 조명, 견고한 하우징이 필요하기 때문에 하드웨어는 2024년 매출의 73%를 차지하며 계속해서 홍채 인식 시장의 핵심을 이루고 있습니다. 그러나 클라우드 추론 엔진이 인식 속도를 높이고 전면 교체 없이도 신속한 기능 업데이트를 가능하게 함에 따라 성장은 소프트웨어 쪽으로 이동하고 있습니다. 시스템 운영자들은 카메라의 평균 업그레이드 주기가 4-5년이라고 보고하지만, 변화하는 인구 구성에 대응하여 정확도를 높이기 위해 분기별로 알고리즘 패치를 전개하고 있습니다.

소프트웨어 부문은 2025년부터 2030년까지 연평균 22.8% 성장률을 기록하며 자본 지출에서 구독 모델로의 전환을 가속화하고 있습니다. 이를 통해 중소기업도 사용량 기반 API를 통해 기업급 정확도를 시험해볼 수 있게 되었습니다. 계층적 아키텍처는 새로운 개인정보 보호 규정이 등장할 때 신속한 적용을 지원하며, 이는 의료 및 금융 분야의 구매 위원회에 실질적인 영향을 미치는 요소입니다. 동시에 부품 공급업체들은 적외선 LED 어레이를 소형화하고 자동차 등급 온도 등급을 적용하여 조명이 예측 불가능한 야외 배치 가능성을 확대하고 있습니다. 오픈 API 렌즈는 교차 모달리티 융합을 가능하게 하여 운영자가 단일 센서에서 홍채 및 얼굴 이미지를 공통 백엔드로 동시에 스트리밍할 수 있게 합니다.

1:N 모드는 2024년 홍채 인식 시장 규모의 66.2%를 차지했으며, 수백만 건의 기록 갤러리를 대상으로 한 일대다 검색이 필요한 국경 통제, 유권자 등록, 복지 혜택 시행에 의해 뒷받침되었습니다. 정부는 여행 성수기에 대비해 상당한 컴퓨팅 예산을 확보함으로써 동시 쿼리에 대한 아키텍처의 복원력을 검증하고 있습니다.

향후 5년간 기업 및 모바일 지갑 제공업체들이 철저한 중복 제거보다 신속한 사용자 인증에 집중함에 따라 1:1 검증 시장은 연평균 20.6% 성장률을 기록할 전망입니다. 결제 포기 방지를 위해 지연 시간이 250밀리초 미만으로 유지되어야 하는 편의성 측면에서 특히 효과적입니다. 유럽의 초기 도입 은행들은 이제 홍채 스캔과 동적 QR 토큰을 결합해 거래 세션을 묶음으로써 눈에 띄는 사용자 불편 없이 피싱 위험을 줄입니다. 이러한 포인트 솔루션이 확장됨에 따라, 문화적으로 다양한 사용자 집단 전반에 걸쳐 오인식/오거부 균형을 개선하는 적응형 임계값 엔진에 데이터를 다시 공급합니다.

지역 분석

아시아태평양 지역은 2024년 전 세계 매출의 36%를 차지했으며, 이는 12억 명 이상의 시민이 등록된 인도의 아다하르(Aadhaar) 제도와 생체 인식 상호작용을 일상화한 스마트폰의 급속한 보급에 힘입은 결과입니다. 중국 휴대폰 제조사들은 알리페이 및 위챗 페이 송금을 뒷받침하기 위해 플래그십 모델에 홍채 인식 잠금 해제 기능을 탑재하고 있으며, 일본의 NEC는 교통 및 소매 셀프 체크아웃 레인에 Bio-IDiom 제품군을 상용화하고 있습니다. 규제 명확성, 강력한 모바일 데이터 커버리지, 가격에 민감하면서도 기술에 정통한 소비자들이 지속적인 설치 증가를 위한 유리한 환경을 조성하고 있습니다.

중동은 2030년까지 연평균 21.3%의 가장 빠른 성장률을 기록할 전망입니다. 걸프 지역 공항의 원활한 승객 통로 전환과 국가 디지털 신분증 로드맵이 이를 촉진합니다. 아랍에미리트(UAE)가 기존 에미레이트 신분증을 폐지하고 얼굴·홍채 인증 방식으로 전환하기로 한 결정은 기존 카드 체계를 뛰어넘겠다는 정책 의지를 보여줍니다. 사우디아라비아의 현지화 추진으로 공급업체들은 스캐너 공동 생산에 나서며, 해당 지역은 수요 중심지이자 생산 거점으로 자리매김하고 있습니다.

유럽과 북미는 성숙했으나 정책에 의해 형성된 수요 곡선을 보여줍니다. GDPR 의무는 프라이버시 바이 디자인(Privacy-by-Design) 아키텍처를 강제하여 국내 클라우드 노드 및 암호화 오버레이에 대한 투자를 촉진합니다. 미국 시장은 국경 검문소 및 항공 허브 업데이트를 위한 연방 자금에 의존하며, 세관 및 국경 보호국(CBP)은 홍채 인식 시범 운영을 추가 국경 검문소로 확대하고 있습니다. 시민 자유 단체들이 전개를 모니터링하고 있으므로, 정확한 생체 인식 검출과 투명한 감사 추적은 대중의 수용을 얻는 데 중요합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 및 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아 지역 내 국가 신분증 및 전자 여권 프로그램 확대

- 중동 지역 통로 전반에 걸친 국경 통제 지출 증가

- 스마트폰 OEM 업체의 기기 내장 홍채 센서 채택

- 미국 의료계에서 비접촉식 환자 신원 확인 의무화 확대

- EU 디지털 지갑 이니셔티브로 가속화되는 전자 KYC 수요

- BFSI 분야의 국경 간 자금 세탁 규정 준수

- 시장 성장 억제요인

- 공항 내 다중 모드 생체 인식 허브의 높은 자본 지출(CAPEX)

- 비협조적 캡처 시나리오에서의 정확도 저하

- 데이터 주권 및 생체 인식 템플릿 저장 규정(EU GDPR(EU 개인정보보호규정))

- 북미 지역의 공공 인식 및 시민 자유에 대한 반발

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 하드웨어

- 홍채 스캐너

- 카메라

- 통합 홍채 인식 시스템

- 기타 광학 모듈 및 조명

- 소프트웨어

- 독립 실행형 매칭 엔진

- SDK 및 미들웨어

- 클라우드 기반 플랫폼

- 하드웨어

- 인식 모드별

- 1:1

- 1:N

- 용도별

- 출입 통제 및 근태 관리

- 신분증 및 국경 통제

- 거래 및 결제 인식

- 환자 식별 및 EMR 연계

- 기타(KYC, 모니터링, 자동차 인포테인먼트)

- 최종 사용자 업계별

- 정부 및 법 집행 기관

- 은행, 금융서비스 및 보험(BFSI)

- 헬스케어 및 생명과학

- 소비자 가전

- 군 및 방위

- 여행 및 이민

- 상업 및 기업

- 기타(교육, 자동차 OEM)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 싱가포르

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 케냐

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- NEC Corporation

- IDEMIA

- HID Global(ASSA ABLOY)

- Thales Group(Gemalto)

- Iris ID Inc.

- IriTech Inc.

- EyeLock LLC

- Princeton Identity Inc.

- BioEnable Technologies Pvt. Ltd.

- IrisGuard UK Ltd.

- Aware Inc.

- Vision-Box

- DERMALOG Identification Systems

- Cognitec Systems GmbH

- Smartmatic

- Samsung Electronics Co., Ltd.

- Fujitsu Limited

- CLEAR Inc.

- CMITech Company Ltd.

- SRI International

제7장 시장 기회와 장래의 전망

HBR 25.11.17The iris recognition market size stands at USD 5.14 billion in 2025 and is forecast to expand to USD 12.92 billion by 2030, reflecting a compound annual growth rate (CAGR) of 20.23%.

This robust trajectory shows how the technology has moved beyond niche government deployments into everyday consumer environments. Heightened demand for contact-free authentication, rising cyber-threat exposure, and stronger compliance expectations from regulators have all accelerated adoption across banking, healthcare, travel, and consumer electronics. Hardware remains the largest cost center, yet software gains more strategic weight as cloud-native matching engines improve speed and lower entry barriers for mid-sized buyers. Asia-Pacific commands an early-mover advantage through scaled national identity programs, while the Middle East delivers the fastest CAGR on the back of airport modernization and tourism facilitation mandates. Intensifying competition now revolves around algorithmic accuracy, multimodal integration, and privacy-centric design features that can withstand evolving data-sovereignty rules.

Global Iris Recognition Market Trends and Insights

Growing National-ID & e-Passport Programs in Asia

Asia-Pacific governments keep scaling iris-enabled digital identity platforms to streamline public-service delivery and financial inclusion. India's DigiLocker upgrade now allows corporate entities to verify staff credentials through the Aadhaar database, widening the addressable base beyond individual citizens.Thailand's public-health authorities have introduced multimodal enrolment kiosks for migrant workers, linking iris scans to vaccination and benefits eligibility. Optical module costs have fallen toward single-digit USD levels in high-volume production, giving budget-constrained agencies an entry point. As enrollment momentum continues, vendors see durable revenue from maintenance contracts and periodic sensor refresh cycles that follow increased performance standards.

Rising Border-Control Spending Across Middle-East Corridors

Gulf states deploy iris recognition at scale to balance security thresholds with passenger-flow targets in flagship airports. The UAE's eGate program, delivered with IDEMIA, employs iris-at-distance capture to process residents and visitors without touching immigration counters. Saudi Arabia's Vision 2030 task force mandates multimodal biometrics for all new terminals, prompting suppliers such as Invixium to commit to local assembly lines for quicker customization. The resulting procurement pipeline favors high-throughput scanners and cloud-ready matching engines that can clear several thousand travelers per hour while logging audit-grade evidence for immigration officials.

High CAPEX of Multimodal Biometric Hubs at Airports

Airports face steep upfront costs when retrofitting existing checkpoints with multimodal pods that include iris, face, and fingerprint options. U.S. Transportation Security Administration trials show passenger throughput gains yet require specialized lanes, LED-safe lighting, and dedicated fiber backhauls to central matching engines. Smaller regional airports postpone rollouts until passenger volumes justify the payback, creating a two-tier adoption curve that suppliers must navigate with modular, pay-per-use pricing models.

Other drivers and restraints analyzed in the detailed report include:

- Smartphone OEM Adoption of On-Device Iris Sensors

- Expansion of Contactless Patient-ID Mandates in U.S. Healthcare

- Data-Sovereignty & Biometric-Template Storage Regulations (EU GDPR)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 73% of 2024 revenue and continues to anchor the iris recognition market, given the need for precision optics, controlled illumination, and rugged housings. Growth, however, shifts toward software as cloud inference engines raise recognition speeds and enable agile feature updates without forklift replacements. System operators report average upgrade cycles of four to five years for cameras, yet deploy quarterly algorithm patches to improve accuracy against evolving demographic mixes.

Software's 22.8% CAGR from 2025-2030 underscores the pivot from capital expenditure to subscription models, letting smaller enterprises trial enterprise-grade accuracy through pay-as-you-go APIs. The layered architecture supports quick rollouts when new privacy mandates emerge, a factor that materially influences procurement committees in health and finance. In parallel, component suppliers miniaturize infrared LED arrays and apply automotive-grade temperature ratings, expanding outdoor deployment windows where lighting is unpredictable. Open-API lenses invite cross-modality fusion, letting operators stream both iris and face images from a single sensor to common back ends.

The 1:N mode represented 66.2% iris recognition market size in 2024, supported by border-control, voter registry, and welfare-benefit rollouts requiring one-to-many searches against multimillion-record galleries. Governments reserve significant compute budgets for peak travel seasons, validating the architecture's resilience for concurrent queries.

Over the next five years, 1:1 verification is expected to record a 20.6% CAGR as corporates and mobile-wallet providers focus on rapid user validation rather than exhaustive de-duplication. The convenience angle resonates where latency must stay below 250 milliseconds to avoid checkout abandonment. Early adopter banks in Europe now pair iris scans with dynamic QR tokens to bind the transaction session, reducing phishing risk without noticeable user friction. As these point solutions scale, they feed data back into adaptive thresholding engines that improve false-accept/false-reject balances across culturally diverse user cohorts.

The Iris Recognition Market Report is Segmented by Component (Hardware, Software), Authentication Mode (1:1 Verification, 1:N Identification), Application (Access Control and Time-Attendance, ID and Border Control, and More), End-User Industry (Government and Law-Enforcement, BFSI, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 36% of global revenue in 2024, underpinned by India's Aadhaar enrollment of over 1.2 billion citizens and rapid smartphone penetration that normalizes biometric interactions. Chinese handset vendors bundle iris unlock in flagship models to underpin Alipay and WeChat Pay transfers, while Japan's NEC commercializes its Bio-IDiom suite across transportation and retail self-checkout lanes. Regulatory clarity, strong mobile data coverage, and price-sensitive yet tech-savvy consumers create a fertile setting for sustained installation growth.

The Middle East records the fastest trajectory at 21.3% CAGR through 2030, fueled by Gulf airports' shift to seamless passenger corridors and national digital-ID roadmaps. The UAE's decision to retire physical Emirates ID cards in favor of a facial-and-iris credential highlights the policy's will to leapfrog legacy cards. Saudi Arabia's localization drives push vendors to co-manufacture scanners, positioning the region as both a demand hub and a production base.

Europe and North America display mature yet policy-shaped demand curves. GDPR obligations force privacy-by-design architectures, prompting greater investment in in-country cloud nodes and encryption overlays. The U.S. market banks on federal funding to update border checkpoints and aviation hubs, with Customs and Border Protection extending iris capture pilots to additional crossings. Civil-liberties groups monitor deployments, so accurate liveness detection and transparent audit trails are critical to winning public acceptance.

- NEC Corporation

- IDEMIA

- HID Global (ASSA ABLOY)

- Thales Group (Gemalto)

- Iris ID Inc.

- IriTech Inc.

- EyeLock LLC

- Princeton Identity Inc.

- BioEnable Technologies Pvt. Ltd.

- IrisGuard UK Ltd.

- Aware Inc.

- Vision-Box

- DERMALOG Identification Systems

- Cognitec Systems GmbH

- Smartmatic

- Samsung Electronics Co., Ltd.

- Fujitsu Limited

- CLEAR Inc.

- CMITech Company Ltd.

- SRI International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing National-ID and e-Passport Programs in Asia

- 4.2.2 Rising Border-Control spending across Middle-East corridors

- 4.2.3 Smartphone OEM Adoption of On-Device Iris Sensors

- 4.2.4 Expansion of Contactless Patient ID mandates in U.S. Healthcare

- 4.2.5 EU Digital Wallet Initiatives accelerating e-KYC demand

- 4.2.6 Cross-Border Money-laundering Compliance in BFSI

- 4.3 Market Restraints

- 4.3.1 High CAPEX of Multimodal Biometric Hubs at Airports

- 4.3.2 Accuracy Degradation under Non-cooperative Capture Scenarios

- 4.3.3 Data-sovereignty and Biometric-template Storage Regulations (EU GDPR)

- 4.3.4 Public Perception and Civil-liberties Backlash in North America

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Iris Scanners

- 5.1.1.2 Cameras

- 5.1.1.3 Integrated Iris-Recognition Systems

- 5.1.1.4 Other Optical Modules and Illumination

- 5.1.2 Software

- 5.1.2.1 Stand-alone Matching Engines

- 5.1.2.2 SDKs and Middleware

- 5.1.2.3 Cloud-based Platforms

- 5.1.1 Hardware

- 5.2 By Authentication Mode

- 5.2.1 1:1 Verification

- 5.2.2 1:N Identification

- 5.3 By Application

- 5.3.1 Access Control and Time-Attendance

- 5.3.2 ID and Border Control

- 5.3.3 Transaction and Payment Authentication

- 5.3.4 Patient Identification and EMR Linkage

- 5.3.5 Others (KYC, Surveillance, Automotive Infotainment)

- 5.4 By End-user Industry

- 5.4.1 Government and Law-Enforcement

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Consumer Electronics

- 5.4.5 Military and Defense

- 5.4.6 Travel and Immigration

- 5.4.7 Commercial and Enterprise

- 5.4.8 Others (Education, Automotive OEMs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Singapore

- 5.5.4.6 Australia

- 5.5.4.7 New Zealand

- 5.5.4.8 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NEC Corporation

- 6.4.2 IDEMIA

- 6.4.3 HID Global (ASSA ABLOY)

- 6.4.4 Thales Group (Gemalto)

- 6.4.5 Iris ID Inc.

- 6.4.6 IriTech Inc.

- 6.4.7 EyeLock LLC

- 6.4.8 Princeton Identity Inc.

- 6.4.9 BioEnable Technologies Pvt. Ltd.

- 6.4.10 IrisGuard UK Ltd.

- 6.4.11 Aware Inc.

- 6.4.12 Vision-Box

- 6.4.13 DERMALOG Identification Systems

- 6.4.14 Cognitec Systems GmbH

- 6.4.15 Smartmatic

- 6.4.16 Samsung Electronics Co., Ltd.

- 6.4.17 Fujitsu Limited

- 6.4.18 CLEAR Inc.

- 6.4.19 CMITech Company Ltd.

- 6.4.20 SRI International

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment