|

시장보고서

상품코드

1910594

파워 일렉트로닉스 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Power Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

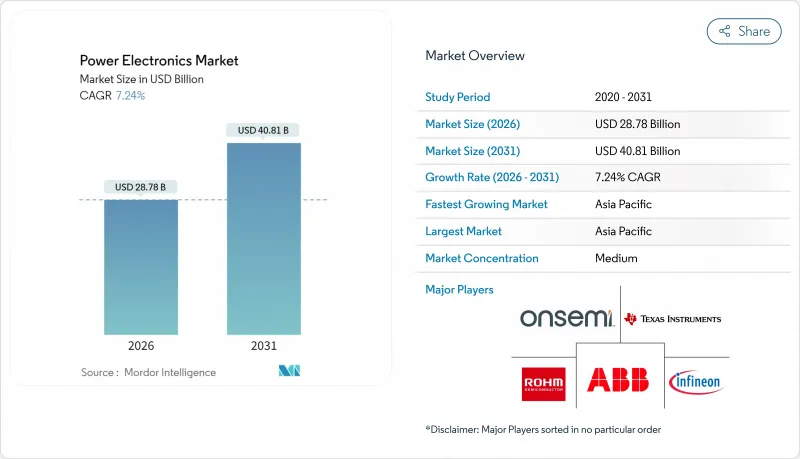

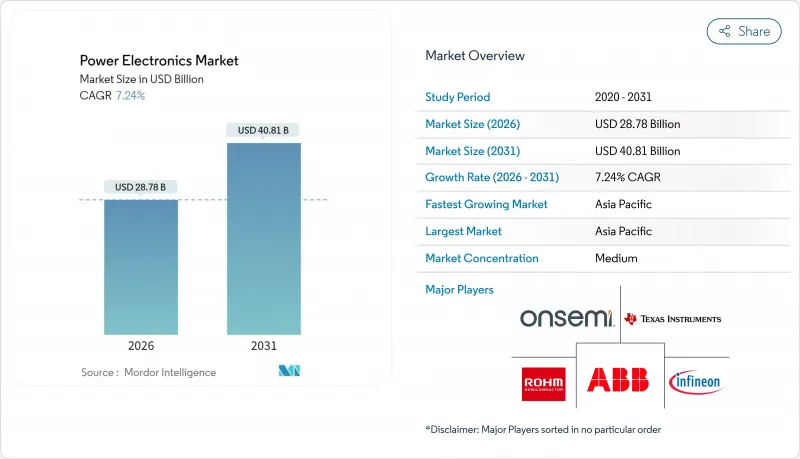

세계의 파워 일렉트로닉스 시장은 2025년 268억 4,000만 달러에서 2026년에는 287억 8,000만 달러로 성장하고, 2026년부터 2031년까지 CAGR 7.24%로 성장을 지속해 2031년까지 408억 1,000만 달러에 달할 것으로 전망됩니다.

기존의 실리콘 시스템에서 탄화규소(SiC) 및 질화갈륨(GaN) 솔루션으로 전환이 계속되고 있는 것이 이 진전을 지원하고 있습니다. 이를 통해 중요한 용도에서 보다 높은 효율, 전력 밀도 및 소형 폼 팩터가 실현됩니다. 자동차 제조업체의 전기자동차 생산 확대, 전력 회사의 재생에너지 인버터 업데이트, 데이터센터 사업자의 고전압 직류(HVDC) 아키텍처 채택으로 수요가 가속화되었습니다. 와이드 밴드갭 재료의 채용은 국내 반도체 제조 및 전기자동차 인프라를 촉진하는 지역 정책의 지원도 받았습니다. 한편, 특히 아시아태평양의 공급망 다양화 이니셔티브는 기판, 에피택시 및 첨단 패키징의 현지 생산을 강화하여 리드 타임과 운송 위험을 줄였습니다.

세계의 파워 일렉트로닉스 시장 동향과 통찰

EV 급속 충전 인프라에서 SiC 및 GaN 디바이스 채택 가속

유럽의 충전 네트워크 사업자는 계통 연계 효율 목표 달성을 위해 1,200V 및 1,700V SiC MOSFET이 필요한 800V 아키텍처를 우선적으로 채택했습니다. 인센티브 프로그램을 통한 지원 프로젝트는 에너지 손실을 줄이고 냉각 서브시스템을 소형화하는 SiC 파워 스테이지를 표준화합니다. 시스템 통합사업자와 반도체 공급업체의 연계로 설계 사이클이 단축되고, 자동차 제조업체와의 제휴 계약에 의해 장기적인 양산 확보가 도모되었습니다. 상호 운용성 규제는 광대역 갭 디바이스를 기반으로 한 모듈형 고밀도 충전기가 유리한 공정한 경쟁 환경을 추가로 구축했습니다. 성공적인 도입 사례가 세계의 주목을 받고, 유럽은 차세대 급속 충전 솔루션의 기준 시장으로서의 지위를 확립하고 있습니다.

아시아의 대규모 태양광 및 풍력발전소 인버터 갱신

중국, 인도 및 베트남의 유틸리티 규모 태양광 발전소에서는 고온 다습 환경 하에서 높은 스위칭 주파수를 견디는 SiC 기반 모듈로 기존 실리콘 인버터를 대체했습니다. Wolfspeed의 최신 유틸리티 모듈은 중앙 집중식 3-5MW 인버터가 요구하는 열 사이클 신뢰성을 제공했습니다. 해상풍력 개발업자도 터빈 나셀의 사이즈 및 중량 제한을 만족시키기 위해 같은 파워 스테이지를 채용하고 있습니다. 지역 수탁 제조 업체는 수입 관세 회피를 위해 현지 조립을 추진하고 기존 실리콘 제품과 가격 경쟁력을 가속화했습니다. 이러한 업그레이드는 정부의 신재생에너지 도입 기준에 부합하며 신흥경제권 전체에서 경쟁력 있는 전력요금을 유지하고 있습니다.

150mm 이상의 SiC 웨이퍼에서 공급망의 병목

만성적인 기판 부족은 양산 확대를 제약하고 평균 판매 가격이 높은 수준에서 유지되었습니다. Wolfspeed의 일시적인 자금 조달 과제는 회사의 200mm 로드맵에 의존했던 파트너 기업의 위험을 증가시켜 Renesas가 계획한 SiC 플랫폼에서 철수하게 되었습니다. 중국의 신규 참가기업은 생산능력 확대를 가속화했지만 자동차 제조업체 고객과의 인증 취득에 과제를 안고 있습니다. 공장 출시부터 생산 준비 완료에 이르기까지 다년간의 시간 지연은 디바이스 제조업체와 시스템 OEM 모두 수요 예측 정확도를 복잡하게 만들었습니다. 그 결과, 복수의 자동차 제조업체가 웨이퍼의 할당을 확보하기 위한 듀얼 소싱 전략을 실시했습니다.

부문 분석

파워 모듈은 2031년까지 연평균 복합 성장률(CAGR) 8.49%를 달성했습니다. 2025년에도 이산 트랜지스터와 다이오드는 매출액의 45.92%를 차지했으며 민생기기 및 저전력 공장 설비에서 유연성을 유지했습니다. 모듈 수요는 게이트 드라이버, 온도 센서, 절연 기능을 통합하여 개발 사이클을 단축할 수 있는 50kW 이상의 트랙션 인버터와 재생에너지 변환 장치로 급증했습니다. 내장 냉각 기판이 시험 생산 단계에 들어가 모듈의 전력 밀도 향상과 전기자동차용 소형 인버터 케이스의 실현을 추진하고 있습니다. 통합 파워 IC는 100W 미만의 급속 충전 어댑터 시장에서 점유율을 확대하고 엄격한 크기 제약을 충족하는 단일 플라스틱 패키지 내에 제어 및 스위칭 기능을 통합했습니다. 스마트폰 제조업체는 컴팩트한 벽면 플러그로 65W 충전을 실현하기 위해 이러한 모놀리식 GaN 솔루션을 채택했습니다. 자동차 공급업체가 800V 플랫폼으로 전환하는 동안 모듈용 전력 전자 시장 규모는 꾸준히 확대될 것으로 예측됩니다. 한편, 소비자용 설계 채용이 이산 소자의 수량을 지원하고 있습니다.

시장 전반에 걸친 트랜스퍼 몰딩 패키지의 표준화는 가혹한 기후 하에서 작동하는 산업용 드라이브를 위한 비용 절감과 우수한 내습성을 실현했습니다. 제조업체 각사는 특히 아시아태평양에서 증가하는 생산 수요에 대응하기 위해 자동 조립 라인을 활용했습니다. 그러나 조명용 밸러스트, 가전제품, 로봇제어장치 등의 분야에서는 커스터마이즈된 기판 레이아웃과 다양한 전압 클래스가 통합의 이점을 웃돌아, 이산 소자가 여전히 큰 존재감을 유지하고 있습니다. 예측기간에 탄화규소 웨이퍼 공급 증가에 의해 모듈로의 점유율 이행이 더욱 진행되는 한편, 이산제품의 수량은 급격한 낙하가 아니라 점진적으로 감소할 전망입니다.

MOSFET은 2025년 매출의 43.62%를 차지했으며, 8.98%의 연평균 복합 성장률(CAGR)을 통해 최대 성장 속도가 가장 빠른 디바이스 범주로 자리매김했습니다. 이 아키텍처는 단계적 R&D에 적합하며 Wolfspeed의 4세대 플랫폼이 기존 게이트 구동 요구 사항을 유지하면서 온 저항을 줄인 것이 좋은 예입니다. 충전 어댑터와 태양광 마이크로 인버터의 고주파 공진 토폴로지는 GaN 인핸스먼트 모드 MOSFET을 채용하는 경향이 강해지는 반면, 100kW를 초과하는 차량 구동 스테이지에서는 SiC 평면 MOSFET이 우위성을 나타냈습니다. IGBT는 철도 추진 시스템과 대형 산업용 구동 장치에서 여전히 필수적이며 MOSFET의 실용 한계를 넘는 전력 클래스에서 수요를 지속적으로 유지하고 있습니다. 사이리스터는 계통 연계 소프트 스타터나 HVDC 링크용으로 계속 채용되었지만, 전체적인 공헌도는 축소되었습니다.

디바이스 제조업체는 SiC MOSFET과 쇼트키 다이오드의 공봉 패키지를 도입하여 역회복의 제약을 완화함과 동시에 기판 레이아웃을 간소화했습니다. 한편, 질화 갈륨 공급업체는 하드 스위칭 조건 하에서 디바이스 수명 연장을 위해 동적 RDS(on) 특성의 개선을 진행하고 있습니다. 파워 일렉트로닉스 시장에서는 MOSFET의 혁신이 지속적으로 평가되고 있습니다. 폼 팩터가 기존의 드라이버 에코시스템과 일치하여 시스템 엔지니어의 설계 장벽을 줄이기 위해서입니다. 향후 점유율 변동은 와이드 밴드갭 웨이퍼의 가격 동향과 차세대 MOSFET 게이트 기술의 자동차 인증 획득 속도에 달려 있습니다.

파워 일렉트로닉스 시장의 세분화는 컴포넌트별(이산, 모듈, 집적 파워 IC), 디바이스 종별(MOSFET, IGBT, 사이리스터, 다이오드), 재료별(실리콘, 탄화 규소, 기타), 최종 사용 산업(소비자용 전자기기, 자동차, ICT 및 통신, 산업용, 에너지 및 전력, 항공우주 및 방위 등), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)에 의해 구분됩니다.

지역별 분석

아시아태평양은 2025년 세계 수익의 53.88%를 차지하며 10.05%의 연평균 복합 성장률(CAGR)로 리드를 확대하고 있습니다. 중국, 일본, 한국의 국가 프로그램은 웨이퍼 공장, 모듈 조립, 전기자동차 공급망에 자금을 제공하여 기판 및 첨단 패키징의 현지 조달을 확보했습니다. 일본 정부는 국내 반도체 산업 지원을 위해 670억 달러를 기여할 것을 표명해, Sony나 Mitsubishi Electric 등의 기업을 지원하는 것과 동시에, 대학과의 연구 제휴를 강화했습니다. 중국 본토는 재료 성장과 후공정 조립에 있어서의 규모의 경제를 활용해 최첨단 기술에서는 차이가 있지만, 지역 고객에 대한 신속한 공급과 착륙 비용의 저감을 실현했습니다.

북미는 여전히 2위의 지역이며, AI 서버, 전기 픽업 트럭, 재생에너지 마이크로그리드 등 활기찬 최종 시장과 혁신의 강점을 결합하고 있습니다. 주 차원의 우대 조치로 새로운 SiC 웨이퍼 공장이 유치되어 200mm로의 이행을 위한 자금 확보가 촉진되었습니다. 방위 조달에 의해 방사선 내성 GaN의 조사가 지속적으로 자금 제공되고 나중에 상용 통신 시스템에 응용되었습니다. 북미의 파워 일렉트로닉스 시장 규모는 상승 경향이 있으며, 데이터센터 사업자가 구리 사용량을 줄이고 랙 밀도를 향상시키는 400V DC 아키텍처를 채택하고 있기 때문입니다. 유럽에서는 전기 이동성 충전 회랑과 그리드 레벨 축전에 자원을 집중시켰습니다. 정책 입안자는 충전 하드웨어의 상호 운용성을 의무화하고, 800V에서의 효율성에서 간접적으로 SiC 채용을 촉진했습니다. 자동차 Tier 1 공급업체는 반도체 벤더와 제휴하여 트랙션 인버터를 공동 개발합니다. 통합 참조 플랫폼을 구축하여 형식 인증을 가속화했습니다. 중동 및 아프리카는 기반 규모는 작지만, 견고한 인버터 단을 필요로 하는 대규모 태양광 발전소나 해수 담수화 시설에 대한 투자가 진행되었습니다. 남미에서는 브라질과 아르헨티나의 풍력 회랑과 지역 내 파워 모듈 조립을 촉진하는 현지 조달 규제가 기회를 창출하고 있습니다. 이러한 동향이 합쳐져, 산업의 성숙도나 정책 지원의 정도에는 차이가 있지만, 모든 대륙에서 파워 일렉트로닉스 시장은 계속해서 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유럽 전역에서 EV 급속 충전 인프라용 SiC/GaN 디바이스 채용 가속

- 아시아의 대규모 태양광 및 풍력 발전소용 인버터 갱신 수요가, 고전압 파워 모듈 시장을 견인

- 북미에서 5G 기지국의 전개에 고효율 RF 파워 앰프 수요 발생

- 동남아시아에서 7.5kW 이상의 산업용 모터 구동 장치의 전동화

- 중국의 그리드 레벨 축전지 프로그램이 양방향 전력 변환기 수요를 촉진

- 미국 방위부의 완전 전기식 플랫폼으로의 현대화가, 견고한 파워 일렉트로닉스를 촉진

- 시장 성장 억제요인

- 150mm 이상의 SiC 웨이퍼에서 공급망 병목이 양산을 제한

- 1.2kV 초모듈에서의 패키징 열 관리상 제약

- 200mm 와이드 밴드갭 팹의 고액 설비 투자가 신규 진입을 저해

- 공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자 및 자금 조달 분석

- 시장에 대한 거시경제적 요인의 평가

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 이산

- 모듈

- 통합형 파워 IC

- 디바이스 유형별

- MOSFET

- IGBT

- 사이리스터

- 다이오드

- 소재별

- 실리콘(Si)

- 탄화규소(SiC)

- 질화갈륨(GaN)

- 최종 사용 산업별

- 소비자용 전자 기기

- 자동차(xEV, 충전)

- 정보통신기술(ICT) 및 전기통신

- 산업용(구동장치, 자동화)

- 에너지 및 전력(재생에너지, 고압 직류 송전)

- 항공우주 및 방위

- 의료기기

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 대만

- 인도

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 합작사업, 라이선싱)

- 시장 점유율 분석

- 기업 프로파일

- Infineon Technologies AG

- Mitsubishi Electric Corporation

- ON Semiconductor Corporation

- STMicroelectronics NV

- Texas Instruments Inc.

- ROHM Co., Ltd.

- ABB Ltd.

- Toshiba Electronic Devices & Storage Corp.

- Vishay Intertechnology Inc.

- Renesas Electronics Corp.

- Wolfspeed Inc.

- Fuji Electric Co., Ltd.

- SEMIKRON Danfoss

- Littelfuse Inc.

- GeneSiC Semiconductor

- Navitas Semiconductor Corp.

- GaN Systems Inc.

- Alpha & Omega Semiconductor

- Microchip Technology Inc.

- Diodes Incorporated

제7장 시장 기회와 미래 전망

SHW 26.01.26The power electronics market is expected to grow from USD 26.84 billion in 2025 to USD 28.78 billion in 2026 and is forecast to reach USD 40.81 billion by 2031 at 7.24% CAGR over 2026-2031.

Continued migration from legacy silicon systems toward silicon-carbide and gallium-nitride solutions underpins this advance, enabling higher efficiency, power density, and smaller form factors in critical applications. Demand accelerated as automakers scaled electric-vehicle production, utilities upgraded renewable-energy inverters, and data-center operators adopted high-voltage direct-current architectures. Wide-bandgap adoption also benefited from regional policy support that encouraged domestic semiconductor manufacturing and electric-mobility infrastructure. Meanwhile, supply-chain diversification initiatives, especially across Asia-Pacific, bolstered localized production of substrates, epitaxy, and advanced packaging, reducing lead times and transportation risk.

Global Power Electronics Market Trends and Insights

Accelerated adoption of SiC and GaN devices in EV fast-charging infrastructure

European charging-network operators prioritized 800 V architectures that require 1,200 V and 1,700 V SiC MOSFETs to meet grid-connection efficiency targets. Projects backed by incentive programs are standardized on SiC power stages that cut energy losses and shrink cooling subsystems. Collaboration between system integrators and semiconductor suppliers shortened design cycles, while alliance agreements with automotive OEMs ensured long-term volume commitments. Interoperability regulations further created a level playing field that favors modular, high-density chargers based on wide-bandgap devices. Successful deployments draw global attention, positioning Europe as the reference market for next-generation fast-charging solutions.

Large-scale solar and wind farm inverter upgrades in Asia

Utility-scale solar farms in China, India, and Vietnam replaced legacy silicon inverters with SiC-based modules that withstand high switching frequencies in hot, humid environments. Wolfspeed's latest utility modules provided the thermal-cycling reliability demanded by centralized 3 MW to 5 MW inverters. Offshore wind developers adopted similar power stages to meet size and weight limits on turbine nacelles. Regional contract manufacturers localized assembly to avoid import duties, accelerating price parity with conventional silicon alternatives. These upgrades align with government renewable portfolio standards, keeping energy tariffs competitive across emerging economies.

Supply-chain bottlenecks for 150 mm and larger SiC wafers

Chronic substrate shortages constrained volume ramps, keeping average selling prices elevated. Wolfspeed's temporary liquidity challenges increased risk exposure for partners that relied on its 200 mm roadmap, leading Renesas to exit its planned SiC platform. Chinese entrants accelerated capacity additions yet faced qualification hurdles with automotive customers. The multiyear lag between announced fabs and production readiness complicated demand-forecast accuracy for both device makers and system OEMs. As a result, several automakers executed dual-sourcing strategies to hedge wafer allocations.

Other drivers and restraints analyzed in the detailed report include:

- 5G base-station roll-outs requiring high-efficiency RF power amplifiers

- Electrification of industrial motor drives above 7.5 kW in Southeast Asia

- Packaging thermal-management constraints above 1.2 kV modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Power modules delivered 8.49% CAGR through 2031 as design teams opted for pre-packaged assemblies that simplify thermal layout and electromagnetic shielding. In 2025, discrete transistors and diodes still contributed 45.92% of revenue, preserving flexibility in consumer and low-power factory equipment. Demand for modules surged in traction inverters and renewable-energy converters above 50 kW where integrating gate drivers, temperature sensors, and isolation reduced development cycles. Embedded-cooling substrates entered pilot production, pushing module power density upward and enabling smaller inverter housings in electric vehicles. Integrated power ICs gained share in fast-charger adapters below 100 W, combining control and switching in a single plastic package that meets stringent size constraints. Smartphone brands adopted these monolithic GaN solutions to achieve 65 W charging in compact wall plugs. The power electronics market size for modules is forecast to expand steadily as automotive suppliers transition to 800 V platforms, while consumer design wins sustain volume in discrete devices.

Market-wide standardization on transfer-molded packages offered cost reductions and better moisture resistance for industrial drives operating in harsh climates. Manufacturers leveraged automated assembly lines to meet rising output needs, particularly across Asia-Pacific. Discrete devices nevertheless preserved a sizeable presence in lighting ballasts, home appliances, and robotic controllers, where customized board layouts and diverse voltage classes outweighed the integration advantage. Over the forecast span, increased silicon-carbide wafer availability will further tilt the share toward modules, yet discrete volumes will decline gradually rather than collapse.

MOSFETs captured 43.62% of 2025 revenue and their 8.98% CAGR positions them as both the largest and fastest-growing device category. The architecture lends itself to incremental R&D, evident in Wolfspeed's Gen 4 platform that reduced on-state resistance while maintaining familiar gate-drive requirements. High-frequency resonance topologies in charger adapters and solar micro-inverters gravitated to GaN enhancement-mode MOSFETs, whereas SiC planar MOSFETs excelled in vehicle traction stages above 100 kW. IGBTs remained essential in rail propulsion and large industrial drives, sustaining demand in power classes beyond practical MOSFET limits. Thyristors continued serving grid-tied soft-starters and HVDC links, though their overall contribution shrank.

Device-makers introduced co-packaged Schottky diodes with SiC MOSFETs, easing reverse-recovery constraints and simplifying board layouts. Meanwhile, gallium-nitride suppliers improved dynamic-RDS(on) behavior to extend device life in hard-switching conditions. The power electronics market continues to reward MOSFET innovation because the form factor aligns with existing driver ecosystems, lowering design barriers for system engineers. Future share shifts will hinge on wide-bandgap wafer pricing and the speed of automotive qualification for next-generation MOSFET gates.

Power Electronics Market is Segmented by Component (Discrete, Module, and Integrated Power IC), Device Type (MOSFET, IGBT, Thyristor, and Diode), Material (Silicon, Silicon Carbide, and More), End-User Industry (Consumer Electronics, Automotive, ICT and Telecommunication, Industrial, Energy and Power, Aerospace and Defense, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific generated 53.88% of global revenue in 2025 and is widening its lead with a 10.05% CAGR. National programs in China, Japan, and South Korea funded wafer fabs, module assembly, and electric-vehicle supply chains, ensuring local availability of substrates and advanced packaging. Japanese authorities pledged USD 67 billion to support domestic semiconductor fleets, aiding companies such as Sony and Mitsubishi Electric, and reinforcing university research collaborations. Mainland China leveraged economies of scale in material growth and backend assembly to supply regional customers quickly, lowering landed cost despite technology gaps in the leading edge.

North America remained the second-largest region, pairing innovation strengths with thriving end-markets in AI servers, electric pickup trucks, and renewable microgrids. State-level incentives attracted new SiC wafer plants and helped secure capital for 200 mm transitions. Defense procurement continued to fund radiation-tolerant GaN research, which later filtered into commercial telecom systems. The power electronics market size in North America is on an upward trajectory as data-center operators adopt 400 V DC architectures that reduce copper usage and improve rack density. Europe focused resources on e-mobility charging corridors and grid-level storage. Policymakers mandated interoperability of charging hardware, indirectly favoring SiC adoption due to its efficiency at 800 V. Automotive Tier 1 suppliers partnered with semiconductor vendors to co-develop traction inverters, creating integrated reference platforms that accelerate homologation. The Middle East and Africa region, while starting from a smaller base, invested in large photovoltaic plants and desalination facilities that require robust inverter stages. South America's opportunities emerged from wind corridors in Brazil and Argentina and from local content rules that encourage assembly of power modules within the region. Collectively, these dynamics keep the power electronics market expanding on every continent, though rates vary with industrial maturity and policy support.

- Infineon Technologies AG

- Mitsubishi Electric Corporation

- ON Semiconductor Corporation

- STMicroelectronics N.V.

- Texas Instruments Inc.

- ROHM Co., Ltd.

- ABB Ltd.

- Toshiba Electronic Devices & Storage Corp.

- Vishay Intertechnology Inc.

- Renesas Electronics Corp.

- Wolfspeed Inc.

- Fuji Electric Co., Ltd.

- SEMIKRON Danfoss

- Littelfuse Inc.

- GeneSiC Semiconductor

- Navitas Semiconductor Corp.

- GaN Systems Inc.

- Alpha & Omega Semiconductor

- Microchip Technology Inc.

- Diodes Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of SiC/GaN Devices in EV Fast-Charging Infrastructure across Europe

- 4.2.2 Large-Scale Solar and Wind Farm Inverter Upgrades in Asia Driving High-Voltage Power Modules

- 4.2.3 5G Base-Station Roll-outs Requiring High-Efficiency RF Power Amplifiers in North America

- 4.2.4 Electrification of Industrial Motor Drives Exceeding 7.5 kW in South-East Asia

- 4.2.5 Grid-Level Battery Storage Programs in China Boosting Bidirectional Power Converters

- 4.2.6 U.S. DoD Modernization Toward All-Electric Platforms Stimulating Rugged Power Electronics

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Bottlenecks for 150 mm+ SiC Wafers Limiting Volume Production

- 4.3.2 Packaging Thermal-Management Constraints Above 1.2 kV Modules

- 4.3.3 High CAPEX for 200 mm Wide-Bandgap Fabs Hindering New Entrants

- 4.4 Supply Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment and Funding Analysis

- 4.8 Assessment of macroeconomic factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Discrete

- 5.1.2 Module

- 5.1.3 Integrated Power IC

- 5.2 By Device Type

- 5.2.1 MOSFET

- 5.2.2 IGBT

- 5.2.3 Thyristor

- 5.2.4 Diode

- 5.3 By Material

- 5.3.1 Silicon (Si)

- 5.3.2 Silicon Carbide (SiC)

- 5.3.3 Gallium Nitride (GaN)

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive (xEV, Charging)

- 5.4.3 ICT and Telecommunication

- 5.4.4 Industrial (Drives, Automation)

- 5.4.5 Energy and Power (Renewables, HVDC)

- 5.4.6 Aerospace and Defense

- 5.4.7 Healthcare Equipment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 Taiwan

- 5.5.3.5 India

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Licensing)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Mitsubishi Electric Corporation

- 6.4.3 ON Semiconductor Corporation

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Texas Instruments Inc.

- 6.4.6 ROHM Co., Ltd.

- 6.4.7 ABB Ltd.

- 6.4.8 Toshiba Electronic Devices & Storage Corp.

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Renesas Electronics Corp.

- 6.4.11 Wolfspeed Inc.

- 6.4.12 Fuji Electric Co., Ltd.

- 6.4.13 SEMIKRON Danfoss

- 6.4.14 Littelfuse Inc.

- 6.4.15 GeneSiC Semiconductor

- 6.4.16 Navitas Semiconductor Corp.

- 6.4.17 GaN Systems Inc.

- 6.4.18 Alpha & Omega Semiconductor

- 6.4.19 Microchip Technology Inc.

- 6.4.20 Diodes Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment