|

시장보고서

상품코드

1851786

인원 계수 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)People Counting System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

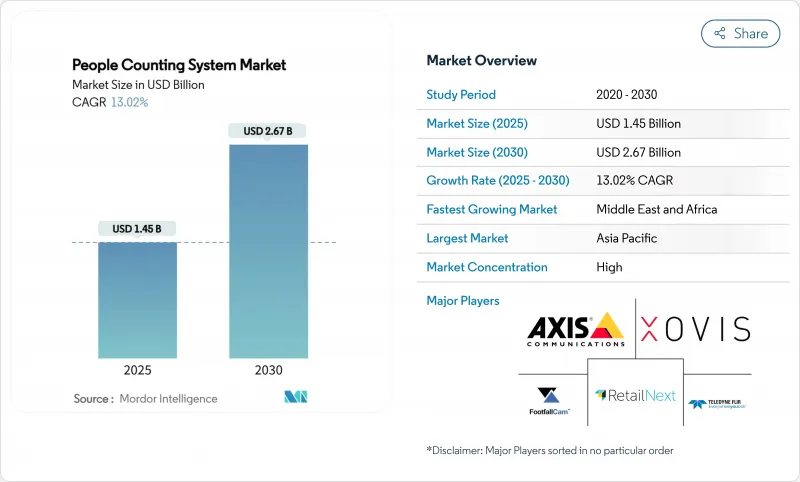

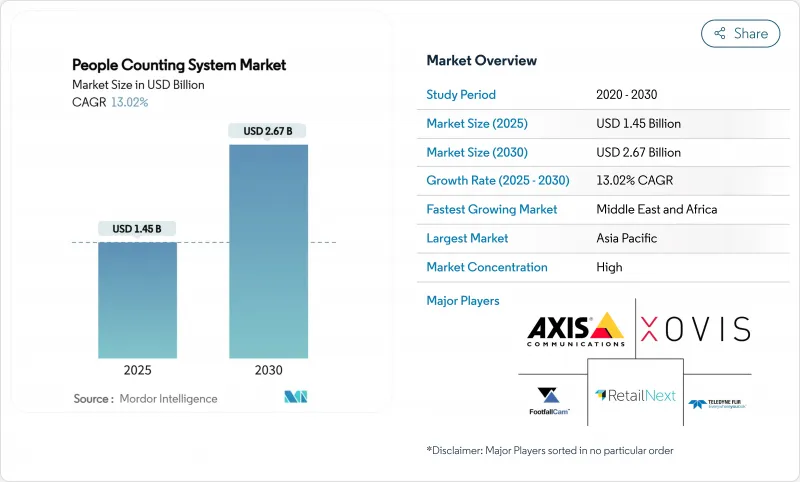

세계의 인원 계수 시스템 시장 규모는 2025년 14억 5,000만 달러로, 예측 기간 중(2025-2030년) CAGR은 13.02%로 확대되어, 2030년까지 26억 7,000만 달러에 이를 것으로 예측됩니다.

견고한 수요는 스마트 시티에 대한 지출, 유행 후의 거주 요건, 운영 비용을 낮추면서 정확도를 높이는 AI 대응 센서 퓨전으로의 지속적인 이동으로 이어집니다. 비행 시간형(ToF) 센서가 99.8%의 정확도를 실현하고 소유자가 GDPR(EU 개인정보보호규정) 및 CCPA의 의무를 충족하는 데 도움이 되는 프라이버시 바이 디자인 기능을 통합함에 따라 채용이 가속화됩니다. HVAC 시스템과의 에너지 절약 협력은 포인트 분석에서 전체 포트폴리오 최적화로의 전환을 강조하며, 상업용 빌딩의 실증 실험에서 12.5%의 에너지 절감을 기록했습니다. 아시아태평양 전역의 스마트 교통 프로젝트, 중동 지하철 확대, 미국의 쇼핑몰 트래픽 회복이 다방면에 걸친 기세를 유지하고 있습니다. 동시에 반도체 공급의 혼란과 컴플라이언스 비용 증가로 인해 중소매 업체는 가격면에서 긴장을 겪고 있습니다.

세계 인원 계수 시스템 시장 동향과 통찰

북미와 유럽에서 실시간 고객 수 분석에 대한 스마트 소매 기업 수요

미국 쇼핑몰에서는 애널리틱스 도입 후 5-15%의 수익 증가가 나타났습니다. Link Retail의 LinkVision 카메라 소프트웨어는 기존 CCTV를 활용하여 95% 이상의 정밀도를 실현하여 유럽 체인점의 리노베이션 비용을 절감하고 있습니다. Telstra는 2024년 호주 매장에 전개하여 95% 이상의 정확성과 개인정보 보호 위험에 대응하는 장치에서 처리를 결합하여 세계 배포를 강조합니다. 트래픽 수를 인구통계 메타데이터로 강화함으로써 소매업체는 데이터를 공유하지 않고 레이아웃을 조정하고 타겟팅된 프로모션을 수행할 수 있습니다. 이러한 트랙션 포인트는 옴니채널 전략의 핵심인 인원 계수 시스템 시장을 강화합니다.

COVID 이후의 입주 컴플라이언스가 급유 설비의 설치를 의무화(EU, 미국)

개정된 건축기준법에서는 긴급 피난과 실내 공기질의 감시를 지원하기 위해 인원 계수가 의료시설이나 관공청에서의 채용에 박차가 가해지고 있습니다. GSA 오클라호마시티 연방 빌딩은 거주 센서를 BMS에 연결하여 에너지 사용량을 41% 줄이고 정부 바이어에게 ROI를 증명했습니다. FootfallCam의 GDPR(EU 개인정보보호규정) 지원 설계는 칩 레벨에서 데이터를 익명화하고 카운트의 충실도를 유지하면서 개인 이미지의 저장을 방지합니다. 국토 안보부(Homeland Security)의 2024년 조사에서는 15개의 클라우드 분석 도구가 승인되었으며, 이 기술이 공공 안전 준비와 관련되어 있음을 확인했습니다. 따라서 컴플라이언스 요구 사항의 강화는 촉매와 필터 모두로 작동하며 방어 가능한 프라이버시 인증서가 있는 공급업체에게 보상합니다.

GDPR(EU 개인정보보호규정)/CCPA 프라이버시 컴플라이언스가 EU와 CA에서 카메라 기반 채택을 방해

엄격한 동의 규칙은 공급업체에게 익명화 및 로컬 처리의 통합을 강력하게 합니다. 오라비전의 온 디바이스 분석은 이미지 저장을 피하고 규제 당국을 만족시키면서 방향 카운트를 캡처합니다. ToF 센서는 식별 가능한 프레임 없이 95% 이상의 정확도를 제공하여 인증 장애물을 낮춥니다. 엔드 투 엔드 컴플라이언스를 검증할 수 있는 공급업체는 공공 입찰에서 점점 더 유리해지고 시장 경쟁 역학을 형성하고 있습니다.

부문 분석

하드웨어가 계속해서 인원 계수 시스템 시장의 수익을 독점해, 2024년에는 64%의 점유율을 차지했습니다. 자본 지출은 소매점 문, 공항 터미널, 공공시설에 설치된 ToF 센서 및 LiDAR 센서에 집중되어 있습니다. 반면 관리 서비스는 운영자가 분석, 규정 준수 감사 및 지속적인 교정 아웃소싱을 요구하기 때문에 CAGR 13.7%로 상승하고 있습니다. 단일 설치에서 구독 모델로의 전환은 수익의 가시성을 변경하고 지속 가능한 성장을 지원합니다. 인원 계수 시스템 업계 참가자들은 센서 업그레이드와 대시보드 교육을 결합한 교차 판매를 활용하여 다년간 계약을 체결합니다. 소프트웨어 플랫폼은 타사 데이터를 캡처하는 마이크로서비스로 마이그레이션하여 예측적 인력 배치 및 에너지 최적화 이용 사례를 지원합니다.

통합의 깊이는 복잡성을 증가시키고 서비스 회사는 IT 보안, 장비 관리 및 마케팅을 조정하는 오케스트레이터로 자리매김합니다. 가동률 데이터와 에어컨 스케줄을 통합하는 프로젝트는 구체적인 OPEX 이익을 보여주고 빌딩 소유자가 고정 자산에서 성과 기반 계약으로 지출을 전환하도록 촉구합니다. 그 결과, 서비스 카테고리는 하드웨어 업데이트 사이클을 넘어 인원 계수 시스템 시장의 다양화에 기여하고 있습니다.

적외선 빔 센서는 좁은 문 설치에서의 신뢰성을 배경으로 2024년 인원 계수 시스템 시장 점유율의 36.5%를 차지했습니다. 그러나 ToF 3D 센서는 CAGR 14.4%로 확대될 전망입니다. 빛 비행 시간을 깊이 맵으로 변환함으로써 ToF는 사람과 장바구니와 반려동물을 구별하고 조명이 변경 되더라도 정확도를 유지합니다. 이 시프트는 GDPR(EU 개인정보보호규정)을 포함하는 로직을 통합할 수 있는 고유한 ToF ASIC을 가진 공급업체에게 좋은 징조입니다. 비디오 기반 접근법은 개인 이미지를 제거하는 온 에지 추론으로 중심을 옮기는 것으로 생존하지만, 일부 구매자는 신중한 자세를 무너뜨리지 않습니다. 열화상은 온도 스크리닝과 인원수가 융합된 병원에서 틈새 시장을 차지합니다. ToF 센서와 관련된 인원 계수 시스템 시장 규모는 컴포넌트의 비용 곡선이 감소함에 따라 2030년까지 적외선 수익을 초과할 것으로 예측됩니다.

침입 지점에 ToF를 배치하고 개방 영역에 Wi-Fi 프로브를 배치하는 하이브리드 배포는 멀티모달 정확도에 대한 관심을 높인다는 것을 알 수 있습니다. Qualcomm이 확장 가능한 깊이 추정에 대한 특허를 획득한 것은 ToF의 성능을 가파르게 유지하기 위한 광범위한 기술 스택에 대한 투자를 명확하게 보여줍니다. 채용이 확대됨에 따라 규모의 경제에 따라 가격대가 더욱 낮아지고 전환의 기세가 강해집니다.

지역 분석

아시아태평양은 2024년 31.4%의 매출을 차지했으며, 이는 정부 출자 스마트 시티의 틀과 단가를 억제하는 현지 생산 센서 하드웨어가 뒷받침하고 있습니다. 싱가포르의 MRT는 카메라 업그레이드와 표 데이터를 혼잡 경보 푸시에 적용하고, 홍콩은 LiDAR에 뒷받침된 가장자리 AI를 철도의 안전하게 통합하고 있습니다. 일본의 JR East은 약 600개 역에 걸친 Suica의 거래 로그를 처리하여 통근객의 흐름을 모델화하고, 교통 계획과 점포 배치 모두에 활용하고 있습니다. 중국의 2급 도시에서는 도시화가 진행되고, 군중 관리 키트의 대량 주문이 늘어나, 동남아시아의 공항에서는 ToF 카운터를 도입해 보안 라인을 가속하고 있습니다. 이러한 협력적인 인프라 목표는 이 지역의 인원 계수 시스템 시장에서 장기적인 우위를 확고히 하고 있습니다.

중동은 CAGR 14.2%에서 가장 빠르게 성장하는 지역입니다. Vision 2030 프로그램은 사우디아라비아, UAE, 카타르에서 대규모 센서 배포를 지원합니다. Bold Technologies는 모빌리티, 헬스케어, 에너지 데이터를 하나의 AI 레이어에 융합하는 아이온센티아의 인지 시티 플랫폼에 25억 달러를 충당합니다. 두바이는 거리 센서에 의한 도시 전체의 디지털 트윈을 목표로 클라우드 분석 제공업체의 비즈니스 기회를 확대합니다. MENA의 애널리틱스 신흥 기업으로의 벤처 캐피탈 유입은 현지 공급 능력 증가를 보여줍니다.

북미에서는 소매점 리프레시 사이클과 연방 정부 시설 의무화로 채택이 유지되고 있습니다. 2025년에는 미국의 쇼핑몰에 쇼핑객이 돌아오기 때문에 직원 대 쇼핑객의 차별화 기능에 대한 의욕이 높아집니다. 유럽의 GDPR(EU 개인정보보호규정) 시스템은 프라이버시에 중점을 둔 ToF와 최첨단 비디오 솔루션을 홍보하고 새로운 배포보다 업그레이드를 촉구합니다. 남미는 SMB의 가격 감각을 고민하고 있지만, 아프리카의 신흥 스마트 시티 계획은 보다 장기적인 업사이드를 가져옵니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미와 유럽에서 실시간 고객 수 분석의 스마트 소매 수요

- COVID 후의 점유 컴플라이언스 의무가 시설의 활성화를 촉진(EU, 미국)

- 스마트 시티의 교통 허브가 아시아 전역에 인류 센서를 전개

- AI를 활용한 비디오 분석으로 TCO를 삭감해, 정밀도 상승

- 상업 건물의 가동률 통합에 의한 HVAC 에너지 최적화

- 벤처 캐피탈이 MENA의 Footfall-as-a-Service 플랫폼에 참가

- 시장 성장 억제요인

- GDPR(EU 개인정보보호규정)/CCPA 프라이버시 컴플라이언스가 EU와 CA에서 카메라 베이스 채용을 저해

- 구매자의 신뢰를 저하시키는 오픈 에리어 카운트의 정밀도 격차(경기장)

- 신흥 시장에서 레거시 BMS 통합의 복잡성

- 남미 중소소매기업의 가격 감응도

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 기술 스냅샷

- 유선 센서

- 무선(Wi-Fi, BLE, LoRa)

- 열화상 센서

- 비행 시간형 3D 센서

- 기타 기술(압력 매트, 자기, LiDAR)

제5장 시장 규모와 성장 예측

- 제공별

- 하드웨어

- 소프트웨어

- 서비스

- 센서 기술별

- 적외선 빔

- 열화상(IR)

- 비디오 베이스(모노럴, 스테레오, AI)

- 비행 시간(3D)

- 압력 및 자기

- Wi-Fi/BLE 프로브

- 전개 모드별

- On-Premise

- 클라우드

- 접속성별

- 유선(이더넷, PoE)

- 무선(Wi-Fi)

- LP-WAN(LoRa, Zigbee, BLE)

- 업계별

- 소매점포

- 쇼핑몰 및 하이퍼마켓

- 교통 허브(공항, 지하철, 버스)

- 호스피탈리티 및 레저(호텔, 카지노, 테마파크)

- 스포츠 및 엔터테인먼트 회장

- 은행 및 금융기관

- 기업 및 관공청 빌딩

- 의료시설

- 스마트 시티 및 공공 공간

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 북유럽(스웨덴, 노르웨이, 덴마크, 핀란드)

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- RetailNext Inc.

- Sensormatic Solutions(ShopperTrak)

- Axis Communications AB

- Teledyne FLIR Systems Inc.

- HELLA Aglaia Mobile Vision GmbH

- IEE SA

- InfraRed Integrated Systems Ltd.(IRISYS)

- Traf-Sys Inc.

- FootfallCam Ltd.

- V-Count Inc.

- Xovis AG

- iris-GmbH infrared and intelligent sensors

- DILAX Intelcom GmbH

- Eurotech SpA

- SensMax Ltd.

- Countlogic LLC

- Dor Technologies Inc.

- Density Inc.

- Cognimatics AB

- Megvii Technology Ltd.

제7장 시장 기회와 장래의 전망

JHS 25.11.25The People Counting System Market size is estimated at USD 1.45 billion in 2025, and is expected to reach USD 2.67 billion by 2030, at a CAGR of 13.02% during the forecast period (2025-2030).

Steady demand comes from smart-city spending, post-pandemic occupancy requirements, and the continuing shift toward AI-enabled sensor fusion that raises accuracy while lowering operating costs. Adoption accelerates as Time-of-Flight (ToF) sensors deliver 99.8% accuracy and integrate privacy-by-design features that help owners meet GDPR and CCPA mandates. Energy-saving tie-ins with HVAC systems underline a move from point analytics to portfolio-wide optimization, with documented commercial-building pilots posting 12.5% energy reductions. Smart-transport projects across Asia Pacific, metro expansion in the Middle East, and mall traffic rebounds in the United States sustain multi-vertical momentum. At the same time, semiconductor supply disruption and heightened compliance costs create price tension that smaller retailers must navigate.

Global People Counting System Market Trends and Insights

Smart-retail demand for real-time footfall analytics in North America and Europe

Retailers rely on anonymized footfall data to raise conversion and calibrate staffing; evidence from U.S. malls shows 5-15% revenue uplift after analytics rollouts. Link Retail's LinkVision camera software leverages existing CCTV to surpass 95% accuracy, lowering retrofit costs for European chains. Telstra's 2024 deployment across Australian stores underscores global reach, pairing >95% accuracy with on-device processing that addresses privacy risk. By enriching traffic counts with demographic metadata, retailers adjust layouts and execute targeted promotions without data-sharing exposure. These traction points reinforce the People Counting System market as a core pillar of omnichannel strategy.

Post-COVID occupancy compliance mandates fueling installations (EU, US)

Revised building codes now require live head-counting to support emergency egress and indoor-air-quality monitoring, spurring adoption in health facilities and public offices. The GSA Oklahoma City Federal Building linked occupancy sensors to its BMS and cut energy use 41%, proving ROI to government buyers. GDPR-aligned designs from FootfallCam anonymize data at chip level, preventing storage of personal imagery while sustaining counting fidelity. Homeland Security's 2024 survey that endorsed 15 crowd-analysis tools confirms the technology's relevance to public-safety readiness. Heightened compliance requirements therefore work as both catalyst and filter, rewarding vendors with defensible privacy credentials.

GDPR/CCPA privacy compliance hindering camera-based adoption in EU and CA

Stringent consent rules compel vendors to embed anonymization and local processing, raising bill-of-materials and legal consultancy costs. Aura Vision's on-device analytics avoid image storage, satisfying regulators yet still capturing directional counts. ToF sensors emerge as a substitute, providing >95% accuracy without identifiable frames, easing certification hurdles. Vendors that can verify end-to-end compliance are increasingly favored in public tenders, which shapes competitive dynamics within the People Counting System market.

Other drivers and restraints analyzed in the detailed report include:

- Smart-city transportation hubs deploying crowd-flow sensors across Asia

- AI-enabled video analytics cutting TCO and boosting accuracy

- Accuracy gaps in open-area counting reducing buyer confidence (stadiums)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware continues to dominate People Counting System market revenue, holding 64% share in 2024. Capital outlays concentrate on ToF and LiDAR sensors installed across retail thresholds, airport terminals, and public facilities. Managed services, however, are climbing at a 13.7% CAGR as operators seek outsourced analytics, compliance auditing, and continuous calibration. The migration from one-off installs to subscription models transforms revenue visibility and underpins sustainable growth. People Counting System industry participants leverage cross-selling-pairing sensor upgrades with dashboard training-to lock in multi-year contracts. Software platforms move toward micro-services that ingest third-party data, supporting predictive staffing and energy-optimization use cases.

Integration depth raises complexity, positioning services firms as orchestrators that align IT security, facilities management, and marketing. Projects that join occupancy data with HVAC schedules demonstrate tangible opex gains, encouraging building owners to shift spending from fixed assets to outcome-based agreements. As a result, the services category helps diversify the People Counting System market beyond hardware refresh cycles.

Infrared beam sensors captured 36.5% of People Counting System market share in 2024 on the back of reliability in narrow-door installations. Yet ToF 3D sensors are set to expand at a 14.4% CAGR, catalyzed by privacy laws that favor non-imaging depth measurement. By converting light-flight time into depth maps, ToF differentiates people from carts and pets, sustaining accuracy under changing lighting. The shift bodes well for vendors with proprietary ToF ASICs that can embed GDPR-inclusive logic. Video-based approaches survive by pivoting to on-edge inference that strips personal imagery, but some buyers remain cautious. Thermal imaging occupies a niche in hospitals where temperature screening merges with head counts. The People Counting System market size tied to ToF sensors is projected to eclipse infrared revenues before 2030 as component cost curves decline.

Hybrid deployments that blend ToF at entry points with Wi-Fi probes in open zones demonstrate rising interest in multimodal precision. Qualcomm's patent work on scalable depth estimation underscores wider tech-stack investment that will keep ToF on a steep performance trajectory. As adoption broadens, economies of scale further compress price points, reinforcing switch-over momentum.

People Counting System Market Report is Segmented by Offering (Hardware, Software, Services), Sensor Technology (Infrared Beam, Thermal Imaging, Video-Based and More), Deployment Mode (On-Premise, Cloud), Connectivity (Wired, Wireless, LP-WAN), End-User Vertical (Retail, Malls, Transportation, Hospitality and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific holds a 31.4% revenue stake in 2024, propelled by government-funded smart-city frameworks and locally manufactured sensor hardware that compresses unit costs. Singapore's MRT applies camera upgrades and ticket data to push crowdedness alerts, while Hong Kong integrates LiDAR-backed edge AI for railway safety. Japan's JR East processes Suica transaction logs across ~600 stations to model commuter flow, feeding both transport planning and retail placement. China's tier-two city urbanization fuels bulk orders for crowd-management kits, and Southeast Asian airports deploy ToF counters to speed security lines. These coordinated infrastructure goals cement the region's long-term dominance within the People Counting System market.

The Middle East emerges as the fastest-growing geography at a 14.2% CAGR. Vision 2030 programs back large-scale sensor rollouts in Saudi Arabia, the UAE, and Qatar. Bold Technologies allocates USD 2.5 billion to the Aion Sentia cognitive-city platform that fuses mobility, healthcare, and energy data on one AI layer. Dubai targets a city-wide digital twin via street-level sensors, expanding opportunities for crowd analytics providers. Venture-capital flows into MENA analytics startups indicate rising local supply capacity.

North America sustains adoption through retail refresh cycles and federal facility mandates. The return of U.S. mall shoppers in 2025 renews appetite for staff-versus-shopper differentiation features. Europe's GDPR regime fosters privacy-centric ToF and on-edge video solutions, stimulating upgrades rather than greenfield sales. South America grapples with SMB affordability, while Africa's nascent smart-city schemes provide longer-dated upside.

- RetailNext Inc.

- Sensormatic Solutions (ShopperTrak)

- Axis Communications AB

- Teledyne FLIR Systems Inc.

- HELLA Aglaia Mobile Vision GmbH

- IEE S.A.

- InfraRed Integrated Systems Ltd. (IRISYS)

- Traf-Sys Inc.

- FootfallCam Ltd.

- V-Count Inc.

- Xovis AG

- iris-GmbH infrared and intelligent sensors

- DILAX Intelcom GmbH

- Eurotech S.p.A.

- SensMax Ltd.

- Countlogic LLC

- Dor Technologies Inc.

- Density Inc.

- Cognimatics AB

- Megvii Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smart-Retail Demand for Real-Time Footfall Analytics in North America and Europe

- 4.2.2 Post-COVID Occupancy Compliance Mandates Fueling Installations (EU, US)

- 4.2.3 Smart-City Transportation Hubs Deploying Crowd-Flow Sensors Across Asia

- 4.2.4 AI-Enabled Video Analytics Cutting TCO and Boosting Accuracy

- 4.2.5 HVAC Energy-Optimization via Occupancy Integration in Commercial Buildings

- 4.2.6 Venture-Capital Surge into MENA Footfall-as-a-Service Platforms

- 4.3 Market Restraints

- 4.3.1 GDPR/CCPA Privacy Compliance Hindering Camera-Based Adoption in EU and CA

- 4.3.2 Accuracy Gaps in Open-Area Counting Reducing Buyer Confidence (Stadiums)

- 4.3.3 Legacy BMS Integration Complexity in Emerging Markets

- 4.3.4 Price Sensitivity of SMB Retailers in South America

- 4.4 Regulatory and Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Technology Snapshot

- 4.6.1 Wired Sensors

- 4.6.2 Wireless (Wi-Fi / BLE / LoRa)

- 4.6.3 Thermal Imaging Sensors

- 4.6.4 Time-of-Flight 3-D Sensors

- 4.6.5 Other Technologies (Pressure Mats, Magnetic, LiDAR)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Sensor Technology

- 5.2.1 Infrared Beam

- 5.2.2 Thermal Imaging (IR)

- 5.2.3 Video-Based (Mono / Stereo / AI)

- 5.2.4 Time-of-Flight (3-D)

- 5.2.5 Pressure and Magnetic

- 5.2.6 Wi-Fi / BLE Probe

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Connectivity

- 5.4.1 Wired (Ethernet / PoE)

- 5.4.2 Wireless (Wi-Fi)

- 5.4.3 LP-WAN (LoRa, Zigbee, BLE)

- 5.5 By End-User Vertical

- 5.5.1 Retail Stores

- 5.5.2 Shopping Malls and Hypermarkets

- 5.5.3 Transportation Hubs (Airports / Metro / Bus)

- 5.5.4 Hospitality and Leisure (Hotels, Casinos, Theme Parks)

- 5.5.5 Sports and Entertainment Venues

- 5.5.6 Banks and Financial Institutions

- 5.5.7 Corporate and Government Buildings

- 5.5.8 Healthcare Facilities

- 5.5.9 Smart Cities and Public Spaces

- 5.5.10 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics (Sweden, Norway, Denmark, Finland)

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Southeast Asia

- 5.6.4.6 Australia

- 5.6.4.7 New Zealand

- 5.6.4.8 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 RetailNext Inc.

- 6.4.2 Sensormatic Solutions (ShopperTrak)

- 6.4.3 Axis Communications AB

- 6.4.4 Teledyne FLIR Systems Inc.

- 6.4.5 HELLA Aglaia Mobile Vision GmbH

- 6.4.6 IEE S.A.

- 6.4.7 InfraRed Integrated Systems Ltd. (IRISYS)

- 6.4.8 Traf-Sys Inc.

- 6.4.9 FootfallCam Ltd.

- 6.4.10 V-Count Inc.

- 6.4.11 Xovis AG

- 6.4.12 iris-GmbH infrared and intelligent sensors

- 6.4.13 DILAX Intelcom GmbH

- 6.4.14 Eurotech S.p.A.

- 6.4.15 SensMax Ltd.

- 6.4.16 Countlogic LLC

- 6.4.17 Dor Technologies Inc.

- 6.4.18 Density Inc.

- 6.4.19 Cognimatics AB

- 6.4.20 Megvii Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment