|

시장보고서

상품코드

1851790

제조업 블록체인 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Blockchain In Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

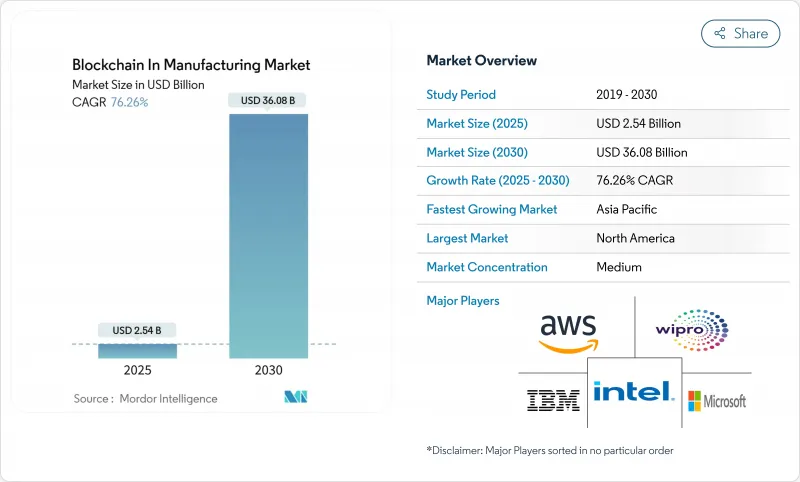

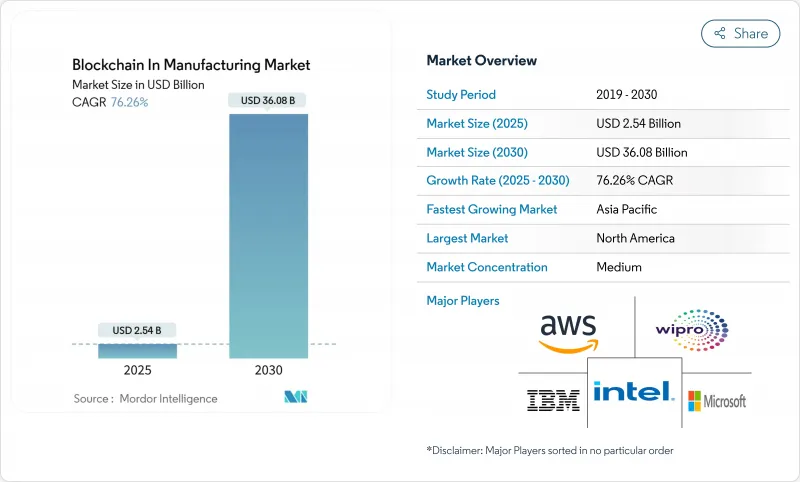

세계의 제조업 블록체인 시장 규모는 2025년 25억 4,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 76.26%로 확대되어, 2030년까지 360억 8,000만 달러에 달할 것으로 예측됩니다.

일괄 증명, 위조 방지, 기기 토큰화를 목적으로 한 불변 장부의 도입이 증가하고 있으며, 파일럿 프로젝트에서 기업 규모의 전개로의 이행이 가속화되고 있습니다. 특히 의약품 공급망 보안법(Drug Supply Chain Security Act)에 근거한 규제 당국의 모니터링을 강화함으로써 제조업자는 직렬화 및 리콜 관리를 자동화하는 분산형 대장을 채용할 수밖에 없게 되었습니다. 또한 클라우드 기반 BaaS(Blockchain-as-a-Service) 플랫폼은 중소규모 공장의 진입 장벽을 낮춥니다. 표준 단편화와 블록체인에 익숙한 운영 기술자의 부족이 단기적인 보급을 막고 있지만 클라우드 하이퍼스케일러와 산업용 OEM의 전략적 파트너십으로 인해 능력 격차가 해소되고 있습니다.

세계 제조업 블록체인 시장 동향과 통찰

이산 제조에서 BaaS 채택 확대

클라우드 제공 BaaS는 현재 이산 제조에서 도입 선호도의 61.8%를 차지하고 있으며, 이 점유율은 전문적인 노드 관리의 필요성을 없애는 턴키 환경에 힘입어지고 있습니다. Microsoft의 Fabric Analytics Suite에 블록체인 텔레메트리를 통합하면 사용자가 엔터프라이즈 데이터와 함께 생산 라인 이벤트를 조회할 수 있어 시스템 통합에 걸리는 시간이 35% 단축되었습니다. 비용 절감과 간소화된 DevOps의 결합으로 BaaS는 신속한 온보딩과 엄격한 가동 시간을 요구하는 자동차, 전자 및 산업 장비 공장에서 확실히 보급됩니다.

공급망 증명 및 추적성 의무화

FDA는 식품 추적성 규칙의 기한을 연장했지만 블록체인이 불변 로트 레벨 보고 요건에 적합하다는 것을 재확인했습니다. EU의 디지털 제품 여권 규칙이 병행하여 제품 수명주기의 각 단계에서 분산 기록의 필요성이 강화되었습니다. 제약, 항공우주 및 가전 제조업체는 리콜 자동화를 위해 시리얼 데이터를 공유 대장에 내장하여 수동 감사 비용을 28% 절감하고 있습니다.

단편화된 표준과 상호 운용성 간극

보편적인 데이터 모델이 없기 때문에 공급업체는 거래 상대방마다 비용이 많이 드는 미들웨어 브리지를 구축해야합니다. GS1과 ISO의 워킹그룹은 공통 스키마를 초안하고 있지만, 채용은 급속히 진행되는 실장 기한에 뒤쳐져 있습니다. 자동차 산업과 화학 산업에서는 컨소시엄 기반의 시험적 노력이 진행되고 있지만, 표준적인 노력이라기 보다는 여전히 작은 노력에 머물고 있습니다.

부문 분석

품질관리 및 컴플라이언스 툴의 2030년까지 CAGR은 77.4%로 예측되고, 2024년의 제조업 블록체인 시장 점유율에서는 후자가 46%를 차지해 물류관리를 웃돌았습니다. FDA 직렬화 테스트를 수행하는 제약 회사는 배치 이력이 분산형 대장에 있는 경우 편차 해결이 30% 빨라질 것으로 보고되었습니다. 감사 인증서를 자동으로 발행하는 스마트 계약 워크플로우는 종이 기록 관리를 대신하여 컴플라이언스에 소요되는 시간을 40% 줄입니다. 제2파 용도에는 예지보전 로그와 보증재정이 포함되며, 불변의 이력은 분쟁률을 저하시킵니다. 고급 화학 태그가 진정성 해시를 공개 대장에 보내 소비자의 신뢰를 높이기 위해 위조품 검출은 여전히 중심적인 역할을 담당하고 있습니다. 이용 사례가 증가함에 따라 제조 시장의 블록 체인은 그린 필드와 브라운 필드 공장 모두에서 큰 견인력이 되었습니다.

품질 시스템은 또한 제로 지식 증명을 통해 기업 비밀을 밝히지 않고 설계 준수를 확인하는 적층 조형에서 새로운 지적 재산 보호 체계의 백본을 형성합니다. 전자 부품 제조업체는 장치의 암호화 서명을 책장에 통합하여 리콜의 정확성을 높입니다. 이와 같이 품질, 컴플라이언스, 위조 방지가 융합됨으로써 상호 운용 가능한 플랫폼에 대한 기업의 관심이 가속화되고 제조 시장의 성장 이야기에서 블록체인이 강화됩니다.

자동차 공장은 광범위한 부품 추적성 의무와 성숙한 Industry 4.0 투자를 반영하여 2024년 매출을 31.2%로 독점했습니다. 그럼에도 불구하고 생명과학 제조업체는 직렬화, 콜드체인 추적, 환자 수준의 실증이 세계적인 의료 규제에서 의무화됨에 따라 2030년까지 연평균 복합 성장률(CAGR) 78.06%로 이 부문 제조업 블록체인 시장 규모를 확대할 것으로 보입니다. IBM 및 Merck와 협력하는 의약품 제조업체는 모의 감사에서 리콜 실행이 25% 빨라졌다고 보고합니다. 항공우주 및 방위 인테그레이터가 3D 프린팅 부품에 안전한 부품 계도 대장을 채용해, 변조 리스크를 경감. 가전 브랜드는 보증 토큰을 제품에 내장하여 애프터 서비스를 간소화하고 식품 및 식품 가공업자는 농장에서 포크까지 추적을 도입하여 지속가능성 감사를 충족합니다. 이러한 수직적 다양화로 인해 제조업 블록체인은 이른 무버의 틀을 넘어서는 퍼짐을 보이고 있습니다.

제조업 블록체인 시장 보고서는 용도별(물류 및 공급망 관리, 위조품 관리, 품질 관리 및 컴플라이언스, 기타), 최종사용자 업계별(자동차, 항공우주 및 방위, 제약 및 생명과학, 기타), 전개 형태별(On-Premise, 클라우드/Blockchain-as-a-Service, 하이브리드 및 에지), 블록체인 유형별(공공, 민간/허가, 기타), 지역별로 구분됩니다.

지역 분석

북미는 FDA의 의무화, 확립된 클라우드 인프라, 대장 신흥 기업에 대한 벤처 캐피탈의 강력한 지원으로 2024년 매출의 44.3%를 차지했습니다. 의약품의 직렬화와 항공우주 부품의 혈통 증명 요건이 초기의 실증을 뒷받침하고, 그 후, 복수 공장 전개로 확대했습니다. 주 수준의 인센티브가 중소기업 채용을 더욱 강화했습니다.

아시아태평양은 2025년부터 2030년까지 CAGR 예측이 78.34%로 가장 높으며, 중국의 산업용 블록체인 시험 운용과 일본의 Society 5.0 스마트 팩토리 로드맵 등의 디지털화 이니셔티브를 반영하고 있습니다. 아시아 개발 은행인 Project Tridecagon은 제조 수출 여신의 흐름에 따라 은행 간 분산 결제에 대한 지역 약속을 제시합니다. 인도의 일렉트로닉스 클러스터와 한국의 배터리 공급 체인 협정이 기세를 높여 Tier 2 공급업체의 채용을 촉진합니다.

유럽은 지속가능성 중시의 채용기업으로 대두하고 디지털 제품 여권을 활용하여 탄소 실적와 순환형 경제 지표를 문서화합니다. 독일 자동차 제조업체 각 회사는 재활용 강재 함량을 추적하기 위해 공동 원장을 채택하고 프랑스 항공우주 선도 기업은 첨가제 제조 분말을 관리하기 위해 블록 체인을 채택합니다. 북유럽 제조업체는 ESG의 기대에 부응하여 수력과 풍력에너지로 허용되는 네트워크에 전력을 공급합니다. 국경을 넘어서는 데이터 공간 프로젝트는 상호 운용성을 촉진하고, 제조 시장에서 블록체인이 세계적으로 성숙함에 따라 지역의 구현이 공통의 거버넌스 하에서 수렴한다는 것을 시사합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 디스크리트 제조업에서 BaaS 채용 확대

- 공급망에서 산지 증명과 추적 가능성 의무화

- 고액 부품에 대한 모방품 대책 수요

- 기기의 서비스화 모델을 가능하게 하는 토큰화

- 안전한 부품 계보를 위한 부가제조와의 통합

- 지재 보호를 위한 프라이버시 보호 제로 지식 증명 및 파일럿

- 시장 성장 억제요인

- 단편화된 표준과 상호 운용성의 갭

- OT 환경에서 블록체인 인재의 한계

- 온체인 추적 가능성을 위한 에너지 사용에 대한 우려 증가

- 포스트 양자 보안 요건의 불확실성

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 유행과 지정 학적 영향 평가

제5장 시장 규모와 성장 예측

- 용도별

- 물류 공급 체인 관리

- 위조품 관리

- 품질관리 및 컴플라이언스

- 예지보전 및 자산추적

- 조달용 스마트 계약

- 기타 용도

- 최종 사용자 업계별

- 자동차

- 항공우주 및 방위

- 제약 및 생명과학

- 소비자 일렉트로닉스

- 산업기계

- 식음료

- 기타 업계별

- 전개 모드별

- On-Premise

- 클라우드/Blockchain-as-a-Service(BaaS)

- 하이브리드/엣지

- 블록체인 유형별

- 공공

- 민간/허가

- 컨소시엄

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 케냐

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향과 파트너십

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Amazon Web Services Inc.

- Accenture PLC

- Wipro Limited

- Infosys Ltd

- Intel Corporation

- Advanced Micro Devices Inc.

- VeChain Technology

- Chronicled Inc.

- SyncFab

- Siemens AG

- Honeywell International Inc.

- General Electric

- R3 LLC

- ConsenSys

- Kaleido

- BlockApps Inc.

제7장 시장 기회와 장래의 전망

JHS 25.11.25The Blockchain In Manufacturing Market size is estimated at USD 2.54 billion in 2025, and is expected to reach USD 36.08 billion by 2030, at a CAGR of 76.26% during the forecast period (2025-2030).

Rising deployment of immutable ledgers for batch provenance, anti-counterfeiting, and equipment tokenization is accelerating the transition from pilot projects to enterprise-wide rollouts. Heightened regulatory scrutiny, especially under the Drug Supply Chain Security Act, is compelling manufacturers to adopt distributed ledgers that automate serialization and recall management. Equipment-as-a-service initiatives are unlocking new revenue streams, while cloud-based Blockchain-as-a-Service (BaaS) platforms lower entry barriers for small and mid-sized factories. Although fragmentation in standards and shortages of blockchain-skilled operational-technology talent temper near-term adoption, strategic partnerships between cloud hyperscalers and industrial OEMs are closing capability gaps.

Global Blockchain In Manufacturing Market Trends and Insights

Escalating Adoption of BaaS Across Discrete Manufacturing

Cloud-delivered BaaS now represents 61.8% of implementation preferences among discrete manufacturers, a share propelled by turnkey environments that eliminate the need for specialized node management. Microsoft's integration of blockchain telemetry into its Fabric analytics suite allows users to query production-line events alongside enterprise data, reducing system-integration time by 35%. Cost savings combine with simplified DevOps to ensure that BaaS gains traction in automotive, electronics, and industrial equipment factories that require rapid onboarding yet stringent uptime.

Supply-Chain Provenance and Traceability Mandates

The FDA extended its Food Traceability Rule deadline yet reaffirmed blockchain's suitability for immutable lot-level reporting requirements. Parallel EU Digital Product Passport rules reinforce the need for distributed records across every product lifecycle phase. Pharmaceutical, aerospace, and consumer electronics producers are embedding serialization data onto shared ledgers to automate recall, thereby trimming manual audit costs by 28%.

Fragmented Standards and Interoperability Gaps

The absence of universal data models forces suppliers to build costly middleware bridges for each trading partner. GS1 and ISO working groups are drafting common schemas, yet adoption lags fast-moving implementation deadlines. Consortium-based pilots in automotive and chemicals signal progress but remain pockets rather than norms.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Counterfeit Mitigation in High-Value Components

- Tokenization Enabling Equipment-as-a-Service Models

- Limited Blockchain Talent in OT Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Quality control and compliance tools are projected to post a 77.4% CAGR to 2030, outpacing logistics management despite the latter's 46% hold on the blockchain in manufacturing market share in 2024. Pharmaceutical firms running FDA serialization pilots report 30% faster deviation resolution when batch histories sit on a distributed ledger. Smart-contract workflows that auto-issue audit certificates replace paper record-keeping, cutting compliance hours by 40%. Second-wave applications include predictive maintenance logs and warranty adjudication, where immutable histories lower dispute rates. Counterfeit detection remains central as luxury-grade chemical tags feed authenticity hashes into public ledgers, enhancing consumer trust. As use cases multiply, the blockchain in the manufacturing market registers significant traction across both greenfield and brownfield plants.

Quality systems also form the backbone for emerging intellectual-property protection schemes in additive manufacturing, where zero-knowledge proofs confirm design compliance without revealing trade secrets. Electronic-component makers integrate on-device cryptographic signatures with the ledger, strengthening recall precision. This convergence of quality, compliance, and anti-counterfeiting accelerates enterprise interest in interoperable platforms, reinforcing the blockchain in the manufacturing market growth narrative.

Automotive factories dominated revenue with 31.2% in 2024, reflecting extensive part traceability obligations and mature Industry 4.0 investments. Nonetheless, life-sciences producers will expand the blockchain in the manufacturing market size for their segment at a 78.06% CAGR through 2030 as serialization, cold-chain tracking, and patient-level provenance become mandatory under global health regulations. Drug makers collaborating with IBM and Merck reported 25% faster recall execution during simulated audits. Aerospace and defense integrators adopt secure part genealogy ledgers for 3D-printed components, mitigating tampering risks. Consumer-electronics brands embed warranty tokens into products to streamline after-sales service, while food and beverage processors deploy farm-to-fork tracking to satisfy sustainability audits. Collectively, vertical diversification broadens the blockchain in the manufacturing industry footprint beyond early movers.

The Blockchain in Manufacturing Market Report is Segmented by Application (Logistics and Supply Chain Management, Counterfeit Management, Quality Control and Compliance, and More), End-User Vertical (Automotive, Aerospace and Defense, Pharmaceutical and Life Sciences, and More), Deployment Mode (On-Premises, Cloud/Blockchain-as-a-Service, and Hybrid/Edge), Blockchain Type (Public, Private/Permissioned, and More), and Geography.

Geography Analysis

North America held 44.3% of 2024 revenue owing to FDA mandates, established cloud infrastructure, and strong venture capital backing for ledger startups. Pharmaceutical serialization and aerospace part pedigree requirements drove early proofs that have since scaled to multi-plant deployments. State-level incentives further supported SME adoption.

Asia Pacific registers the highest 78.34% CAGR forecast between 2025 and 2030, reflecting sweeping digitization initiatives such as China's industrial blockchain pilots and Japan's Society 5.0 smart-factory roadmap. The Asian Development Bank's Project Tridecagon showcases regional commitment to inter-bank distributed settlements that align with manufacturing export-credit flows. India's electronics clusters and South Korea's battery-supply chain agreements add momentum, catalyzing adoption by Tier-2 suppliers.

Europe emerges as a sustainability-centric adopter, leveraging Digital Product Passports to document carbon footprints and circular-economy metrics. Germany's automotive OEMs employ joint ledgers to track recycled steel content, while France's aerospace primes adopt blockchain to manage additive-manufacturing powders. Nordic manufacturers power permissioned networks with hydro and wind energy, addressing ESG expectations. Cross-border data-spaces projects promote interoperability, suggesting that regional implementations will converge under common governance as the blockchain in the manufacturing market matures globally.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Amazon Web Services Inc.

- Accenture PLC

- Wipro Limited

- Infosys Ltd

- Intel Corporation

- Advanced Micro Devices Inc.

- VeChain Technology

- Chronicled Inc.

- SyncFab

- Siemens AG

- Honeywell International Inc.

- General Electric

- R3 LLC

- ConsenSys

- Kaleido

- BlockApps Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating adoption of BaaS across discrete manufacturing

- 4.2.2 Supply-chain provenance and traceability mandates

- 4.2.3 Demand for counterfeit mitigation in high-value components

- 4.2.4 Tokenisation enabling equipment-as-a-service models

- 4.2.5 Integration with additive manufacturing for secure part genealogy

- 4.2.6 Privacy-preserving zero-knowledge-proof pilots for IP protection

- 4.3 Market Restraints

- 4.3.1 Fragmented standards and interoperability gaps

- 4.3.2 Limited blockchain talent in OT environments

- 4.3.3 Rising energy-use concerns for on-chain traceability

- 4.3.4 Uncertainty around post-quantum security requirements

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pandemic and Geopolitical Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Logistics and Supply Chain Management

- 5.1.2 Counterfeit Management

- 5.1.3 Quality Control and Compliance

- 5.1.4 Predictive Maintenance and Asset Tracking

- 5.1.5 Smart Contracts for Procurement

- 5.1.6 Other Applications

- 5.2 By End-user Vertical

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Pharmaceutical and Life Sciences

- 5.2.4 Consumer Electronics

- 5.2.5 Industrial Machinery

- 5.2.6 Food and Beverage

- 5.2.7 Other Verticals

- 5.3 By Deployment Mode

- 5.3.1 On-premises

- 5.3.2 Cloud/Blockchain-as-a-Service (BaaS)

- 5.3.3 Hybrid/Edge

- 5.4 By Blockchain Type

- 5.4.1 Public

- 5.4.2 Private/Permissioned

- 5.4.3 Consortium

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 Amazon Web Services Inc.

- 6.4.6 Accenture PLC

- 6.4.7 Wipro Limited

- 6.4.8 Infosys Ltd

- 6.4.9 Intel Corporation

- 6.4.10 Advanced Micro Devices Inc.

- 6.4.11 VeChain Technology

- 6.4.12 Chronicled Inc.

- 6.4.13 SyncFab

- 6.4.14 Siemens AG

- 6.4.15 Honeywell International Inc.

- 6.4.16 General Electric

- 6.4.17 R3 LLC

- 6.4.18 ConsenSys

- 6.4.19 Kaleido

- 6.4.20 BlockApps Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment