|

시장보고서

상품코드

1851791

기업 거버넌스, 리스크, 컴플라이언스(eGRC) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Enterprise Governance, Risk And Compliance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

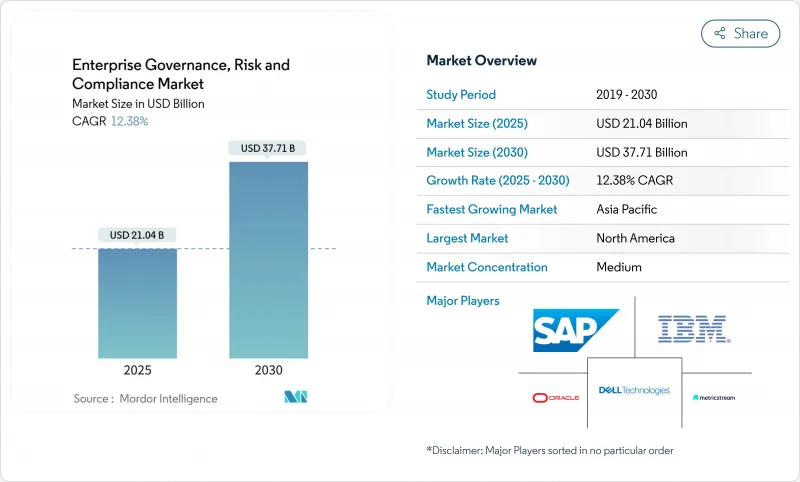

기업 거버넌스, 리스크, 컴플라이언스(eGRC) 시장의 2025년 시장 규모는 210억 4,000만 달러, 2030년에는 377억 1,000만 달러에 이를 것으로 예상되며, 예측 기간 중 CAGR은 12.38%를 나타낼 전망입니다.

조직이 규제상의 의무(특히 디지털 오퍼레이션 탄력성법(DORA))의 급증에 직면하는 한편, 관리의 자동화, 눈에 띄게 변화하는 규칙의 해석, 실시간으로의 이상검출을 위해 AI를 채용함으로써 수요는 가속화되고 있습니다. 통합 제품군은 지금까지 사일로화된 감사, 정책 및 사이버 보안 워크플로우를 단일 진실한 소스로 통합하여 측정가능한 비용 절감과 신속한 문제 해결을 실현하기 위해 플랫폼 구축을 가속화하고 있습니다. 조기 도입 기업은 AI를 활용한 컴플라이언스 분석을 보안 원격 측정에 통합함으로써 오감지를 최대 42% 삭감할 수 있었다고 보고하고 있습니다. 또한 보험 회사가 실시간 GRC 지표를 사용하여 보험료를 가격하고 강력한 거버넌스 성과를 보험료 할인과 경쟁 우위에 연결함으로써 그 기세가 더욱 강해지고 있습니다.

세계의 기업 거버넌스, 리스크, 컴플라이언스(eGRC) 시장 동향 및 인사이트

엄격한 정부 규제와 의무화가 플랫폼 통합을 촉진

2025년 1월에 발효된 DORA는 EU 금융기관에 사고 대응, 탄력성 테스트 및 제3자 모니터링을 다루는 ICT 위험 프레임워크의 통합을 의무화하고 있습니다. 기업은 현재 매일 250개 이상의 규제 변경을 모니터링하고 있으며, 그 속도는 수작업 프로세스를 능가하고 있습니다. 머신러닝 모델은 새로운 법률을 분석하고 관련성을 평가하고 몇 분 이내에 담당 책임자에게 작업을 라우팅함으로써 컴플라이언스 팀은 전략적 위험 분석에 노력을 기울일 수 있습니다. 따라서 여러 관할 구역의 매핑과 자동 업데이트 엔진을 제공하는 공급업체는 기업 후보 목록의 상위에 올랐습니다. 컴플라이언스가 실패하면 심각한 처벌과 호평 피해가 모두 발생할 위험이 있지만, 컴플라이언스에 일찍 일했던 기업은 운영의 탄력성을 보여 투자자의 신뢰를 확보하고 있습니다.

증가하는 사이버 보안 위협이 GRC 기술 통합을 가속화

사이버 사건은 2024년에 75% 급증했으며, CISO는 보안 태세 지표를 단독으로 다루는 것이 아니라 핵심 거버넌스 대시보드에 통합할 필요가 있습니다. 위협의 원격 측정에 정책 검사를 오버레이하는 단일 콘솔은 중복을 줄이고 하이브리드 환경 전체에서 취약성을 복구하는 시간을 단축합니다. AI 지원 GRC 제품군을 채택한 건강 관리 제공업체는 위험 감지율이 37% 향상되었으며 잘못된 감지가 42% 감소한 것으로 컴플라이언스와 보안 데이터를 통합하는 가치를 보여줍니다. 70%의 조직이 현재 클라우드 리스크 할당 프로세스를 비효율적으로 간주하기 때문에 클라우드에 얽매이지 않는 중앙 집중식 관리에 대한 의지가 높아지고 있습니다. 원시 경보가 아닌 실용적인 대시보드를 제공하는 공급업체는 사용자의 피로를 완화하고 전문가가 영향력이 큰 위협에 집중할 수 있도록 지원을 모으고 있습니다.

레거시 시스템의 현대화에는 높은 초기 통합 비용이 과제

주요 스위트 제품의 연간 구독은 5만 달러에서 50만 달러에 이르지만, 도입에는 라이선스 수수료의 2배에서 6배의 비용이 드는 경우가 많고, 노후화된 ERP 백본을 운용하는 기업의 예산을 압박하고 있습니다. SaaS의 인플레이션은 11.3%에 달했으며 직원 수가 늘어났음에도 불구하고 공급업체는 25%의 인상을 부과하므로 가격에 대한 감도가 더욱 높아지고 있습니다. 최신 GRC 도구를 맞춤형 재무, 인사 및 제조 시스템과 통합하려면 사용자 지정 API 및 변경 관리 프로그램이 필요하며 타임라인이 연장되는 경우가 많습니다. 업적 기반 라이선싱과 로우코드 커넥터는 자본 지출을 영업 비용으로 전환하고 정량화 가능한 위험 감소 지표를 통해 투자 회수를 입증함으로써 인기를 끌고 있습니다.

부문 분석

솔루션은 2024년 매출의 67.30%를 차지하며 정책 라이브러리, 감사 추적, 위험 점수 및 사고 대응을 하나의 스택에 통합한 엔드 투 엔드 스위트에 대한 구매자 선호를 부각했습니다. 이러한 이점은 기업이 기업 거버넌스, 리스크, 컴플라이언스(eGRC) 시장의 모든 기능에 대해 단일 공급업체의 책임과 일관된 사용자 환경을 중시하는 방법을 반영합니다. 2030년까지 12.70%의 성장이 예상됩니다. 리스크 관리 및 감사 관리 모듈은 스프레드시트 워크플로우를 대신하여 경영진이 모바일 앱에서 추적할 수 있는 실시간 분석을 제공하므로 가장 빠르게 확산되고 있습니다. 공급망 충격으로 평균 1억 8,400만 달러의 손실이 발생한 후, 비즈니스 연속성 기능에 대한 수요가 급증하고 기업은 계속 계획을 공급업체의 스코어카드에 직접 연결하게 되었습니다.

은행과 병원은 기밀성이 높은 기록을 로컬로 저장해야 하기 때문에 2024년 매출의 54.20%를 On-Premise가 차지했지만 CIO가 AI 워크로드를 위한 탄력적인 컴퓨팅 기능을 선호하기 때문에 클라우드 계약은 2030년까지 매년 13.50% 확대됩니다. 클라우드 플랫폼은 업그레이드를 자동화하고, 배포 주기를 단축하며, 원격 팀을 강화하여 중소기업과 다국적 기업 모두에게 매력적입니다. DORA를 통한 타사 탄력성에 대한 규제 당국의 모니터링을 통해 기업은 외부 클라우드 제공업체에 대한 지속적인 모니터링을 요구합니다. 중요한 데이터를 사내에 남기고 분석을 클라우드로 마이그레이션하는 하이브리드 모델을 통해 위험을 피하는 기업은 레지던시 규칙을 저지하지 않고 클라우드를 사용해 볼 수 있습니다.

공급자는 고객이 관리하는 암호화 키와 현지 규정 준수 시스템에서 인증된 주권 클라우드 지역을 제공함으로써 보안 격차를 완화합니다. 또한 몇 주가 아닌 몇 시간 안에 완벽한 환경을 구축할 수 있는 Infrastructure-as-Code 템플릿을 사용하여 배포를 간소화할 수 있습니다. AI 알고리즘은 대규모 교육 세트와 확장 가능한 GPU를 필요로 하므로 클라우드 구축은 예측적 컴플라이언스 분석을 위한 기본 옵션이 되어 기업 거버넌스, 리스크, 컴플라이언스(eGRC) 시장의 향후 전망에서 클라우드 역할이 강화됩니다.

기업 거버넌스, 리스크, 컴플라이언스(eGRC) 시장은 구성 요소(소프트웨어 및 서비스), 배포 모델(On-Premise 및 클라우드), 조직 규모(중소기업, 대기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 제조업, IT 및 통신, 에너지 및 유틸리티 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 성숙한 규제 생태계와 견조한 기술 예산에 힘입어 2024년 세계 매출의 35.2%를 창출했습니다. 금융기관은 컴플라이언스에 연간 610억 달러를 지출하고 있으며 99%가 비용 증가를 예상하고 있기 때문에 경비율을 낮추는 자동화 솔루션에 대한 수요가 높아지고 있습니다. 연방정부 가이드라인은 자기 신고와 탄력적인 운영을 평가하기 때문에 기업은 GRC에 대한 투자를 경쟁력으로 취급하고 있습니다. ServiceNow와 Visa와 같은 파트너십은 기술 공급업체가 규정 준수를 보장하면서 분쟁 관리를 강화하는 AI 워크플로우를 공동 개발하는 방법을 보여줍니다.

아시아태평양의 CAGR은 13.1%로 세계에서 가장 높을 것으로 예측됩니다. 싱가포르, 호주, 인도의 각 정부는 영국 뇌물 뇌물 법을 반영하는 기업 책임 규칙을 도입했으며 기업은 최신 규정 준수 아키텍처에 투자해야 합니다. 또한 APAC의 은행은 금융범죄의 컴플라이언스 비용 450억 달러에 직면하고 있으며, 그 70%는 2024년에 소프트웨어 지출이 증가한다고 응답했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부의 엄격한 규제와 의무

- 디지털 전환에 수반하는 사이버 보안의 위협 증가

- 통합 리스크 관리 플랫폼으로의 전환

- ESG 보고에 대한 압력과 비재무 정보 공개 규칙

- AI를 활용한 예측 컴플라이언스 분석의 채용

- 실시간 GRC 지표에 대한 보험 인수 의존도

- 시장 성장 억제요인

- 숙련된 GRC 전문가의 부족

- 레거시 환경에 높은 초기 통합 비용

- 멀티클라우드의 데이터 상주와 주권의 복잡성

- 조직적 GRC-피로와 경고 과다

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시경제 요인 평가

제5장 시장 규모와 성장 예측

- 구성 요소별

- 솔루션

- 정책 및 컴플라이언스 관리

- 감사 관리

- 위험 관리

- 사고 관리

- 비즈니스 연속성 및 재해 복구

- 서비스

- 컨설팅

- 통합 및 구현

- 교육 및 지원

- 솔루션

- 배포 모델별

- On-Premise

- 클라우드

- 기업 규모별

- 중소기업

- 대기업

- 최종 사용자 업계별

- BFSI

- 헬스케어 및 생명과학

- 제조

- IT 및 통신

- 에너지 및 유틸리티

- 소매 및 소비재

- 정부 및 공공 부문

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Dell Technologies(incl. RSA Security)

- IBM Corporation

- SAP SE/GRC Suite

- Oracle Corporation

- MetricStream Inc.

- Wolters Kluwer/Enablon

- SAS Institute Inc.

- Software AG

- NAVEX Global

- Thomson Reuters Corp.

- ServiceNow Inc.

- Riskonnect Inc.

- LogicManager Inc.

- OneTrust LLC

- Galvanize(Diligent)

- Ideagen Plc

- SAI Global

- AxiomSL(Adenza)

- Cura Software

- BWise(SandP Global)

- FutureShield Inc.

- Maclear LLC

- RSA Archer Suite

제7장 시장 기회와 향후 전망

KTH 25.11.17The enterprise governance risk compliance market is valued at USD 21.04 billion in 2025 and is set to reach USD 37.71 billion by 2030, advancing at a 12.38% CAGR during the forecast period.

Demand accelerates as organizations confront a surge in regulatory obligations, most notably the Digital Operational Resilience Act (DORA), while adopting AI to automate controls, interpret fast-changing rules, and flag anomalies in real time. Platform uptake intensifies because integrated suites consolidate previously siloed audit, policy, and cybersecurity workflows into a single source of truth, producing measurable cost savings and faster issue resolution. Early adopters report efficiency gains of up to 42% in false-positive reduction after embedding AI-driven compliance analytics alongside security telemetry. Momentum is further reinforced by insurers that now price coverage using real-time GRC metrics, translating strong governance performance into premium discounts and competitive advantage.

Global Enterprise Governance, Risk And Compliance Market Trends and Insights

Stringent government regulations and mandates drive platform consolidation

Heightened rulemaking continues to swell the enterprise governance risk compliance market as DORA, effective January 2025, obliges EU financial entities to embed ICT risk frameworks covering incident response, resilience testing, and third-party oversight. Firms now monitor more than 250 regulatory changes each day, a pace that outstrips manual processes. Machine-learning models parse new statutes, rank their relevance, and route tasks to accountable owners within minutes, enabling compliance teams to redeploy effort toward strategic risk analysis. Vendors offering multijurisdictional mapping and automated update engines have therefore moved to the top of enterprise shortlists. Failure to comply risks both material penalties and reputational damage, whereas early movers secure investor confidence by demonstrating operational resilience.

Rising cybersecurity threats accelerate GRC technology integration

Cyber incidents spiked 75% in 2024, pushing CISOs to embed security posture metrics into core governance dashboards instead of handling them in isolation. A single console that overlays policy checks onto threat telemetry cuts duplication and shrinks time to remediate vulnerabilities across hybrid environments. Healthcare providers adopting AI-enabled GRC suites recorded 37% stronger risk detection rates and 42% fewer false positives, illustrating the value of unifying compliance and security data. Because 70% of organizations label current cloud-risk assignment processes ineffective, appetite for centralised, cloud-agnostic controls has intensified. Suppliers that deliver actionable dashboards-rather than raw alerts-win traction by easing user fatigue and freeing specialists to focus on high-impact threats.

High initial integration costs challenge legacy system modernization

Annual subscriptions for leading suites range from USD 50,000 to USD 500,000, while implementation often costs two to six times the license fees, straining budgets for firms running ageing ERP backbones. SaaS inflation running at 11.3% further heightens price sensitivity as vendors impose 25% hikes despite flat headcount. Integrating modern GRC tools with bespoke finance, HR, and manufacturing systems often demands custom APIs and change-management programmes that extend timelines. Outcome-based licensing and low-code connectors are gaining popularity by shifting capital expenditure to operating expense and demonstrating payback through quantifiable risk-reduction metrics.

Other drivers and restraints analyzed in the detailed report include:

- AI-powered predictive compliance analytics transform risk management

- ESG reporting pressure creates new compliance categories

- Organizational GRC-fatigue impedes platform adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated 67.30% of 2024 revenue, underscoring buyer preference for end-to-end suites that blend policy libraries, audit trails, risk scoring, and incident response into one stack. This dominance reflects how enterprises value single-vendor accountability and consistent user experience across all functions of the enterprise governance risk compliance market. Consulting, integration, and managed services, though smaller in absolute value, are set to grow 12.70% through 2030 as buyers turn to external experts for regulatory interpretation and complex system rollouts. Risk Management and Audit Management modules experience the fastest take-up because they replace spreadsheet workflows and provide real-time analytics that executives can track on mobile apps. Demand for Business Continuity features surged after supply-chain shocks averaged USD 184 million in losses, prompting firms to link continuity plans directly to supplier scorecards.

On-premise installations retained 54.20% of 2024 revenue because banks and hospitals must store sensitive records locally, but cloud subscriptions will expand 13.50% annually through 2030 as CIOs favor elastic compute for AI workloads. Cloud platforms automate upgrades, shorten implementation cycles, and empower remote teams, making them attractive to SMEs and multinationals alike. Regulatory scrutiny on third-party resilience through DORA pushes firms to demand continuous oversight of external cloud providers-a capability that cloud-native GRC suites embed by design. Hybrid models, which keep critical data on-site while shifting analytics to the cloud, enable risk-averse firms to test the waters without breaching residency rules.

Providers mitigate perceived security gaps by offering customer-managed encryption keys and sovereign-cloud regions certified for local compliance regimes. They also streamline deployment through infrastructure-as-code templates that stand up full environments in hours rather than weeks. As AI algorithms require large training sets and scalable GPUs, cloud deployments become the default choice for predictive compliance analytics-cementing their role in the future landscape of the enterprise governance risk compliance market.

Enterprise Governance Risk Compliance Market is Segmented by Component (Software and Services), Deployment Model (On-Premises and Cloud), Organisation Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Manufacturing, IT and Telecom, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 35.2% of global revenue in 2024, supported by mature regulatory ecosystems and robust technology budgets. Financial institutions spend USD 61 billion annually on compliance, and 99% expect costs to rise, reinforcing demand for automated solutions that lower expense ratios. Federal guidelines reward self-reporting and resilient operations, so firms treat GRC investment as a competitive edge. Partnerships such as ServiceNow-Visa illustrate how technology vendors co-create AI workflows that enhance dispute management while ensuring regulatory adherence.

Asia-Pacific is projected to log a 13.1% CAGR, the highest globally. Governments in Singapore, Australia, and India introduce corporate liability rules mirroring the UK Bribery Act, compelling companies to invest in modern compliance architecture. APAC banks also confront USD 45 billion in financial-crime compliance costs, with 70% citing higher software spend in 2024, driving cloud-native uptake that aligns with rapid digitalization.

- Dell Technologies (incl. RSA Security)

- IBM Corporation

- SAP SE / GRC Suite

- Oracle Corporation

- MetricStream Inc.

- Wolters Kluwer / Enablon

- SAS Institute Inc.

- Software AG

- NAVEX Global

- Thomson Reuters Corp.

- ServiceNow Inc.

- Riskonnect Inc.

- LogicManager Inc.

- OneTrust LLC

- Galvanize (Diligent)

- Ideagen Plc

- SAI Global

- AxiomSL (Adenza)

- Cura Software

- BWise (SandP Global)

- FutureShield Inc.

- Maclear LLC

- RSA Archer Suite

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent government regulations and mandates

- 4.2.2 Rising cybersecurity threats with digital transformation

- 4.2.3 Move toward integrated risk-management platforms

- 4.2.4 ESG reporting pressure and non-financial disclosure rules

- 4.2.5 AI-powered predictive compliance analytics adoption

- 4.2.6 Insurance underwriting dependencies on real-time GRC metrics

- 4.3 Market Restraints

- 4.3.1 Lack of skilled GRC professionals

- 4.3.2 High initial integration cost for legacy environments

- 4.3.3 Data-residency and sovereignty complexity in multi-cloud

- 4.3.4 Organisational GRC-fatigue and alert overload

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Policy and Compliance Management

- 5.1.1.2 Audit Management

- 5.1.1.3 Risk Management

- 5.1.1.4 Incident Management

- 5.1.1.5 Business Continuity and Disaster Recovery

- 5.1.2 Services

- 5.1.2.1 Consulting

- 5.1.2.2 Integration and Implementation

- 5.1.2.3 Training and Support

- 5.1.1 Solutions

- 5.2 By Deployment Model

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 By Organisation Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Manufacturing

- 5.4.4 IT and Telecom

- 5.4.5 Energy and Utilities

- 5.4.6 Retail and Consumer Goods

- 5.4.7 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Dell Technologies (incl. RSA Security)

- 6.4.2 IBM Corporation

- 6.4.3 SAP SE / GRC Suite

- 6.4.4 Oracle Corporation

- 6.4.5 MetricStream Inc.

- 6.4.6 Wolters Kluwer / Enablon

- 6.4.7 SAS Institute Inc.

- 6.4.8 Software AG

- 6.4.9 NAVEX Global

- 6.4.10 Thomson Reuters Corp.

- 6.4.11 ServiceNow Inc.

- 6.4.12 Riskonnect Inc.

- 6.4.13 LogicManager Inc.

- 6.4.14 OneTrust LLC

- 6.4.15 Galvanize (Diligent)

- 6.4.16 Ideagen Plc

- 6.4.17 SAI Global

- 6.4.18 AxiomSL (Adenza)

- 6.4.19 Cura Software

- 6.4.20 BWise (SandP Global)

- 6.4.21 FutureShield Inc.

- 6.4.22 Maclear LLC

- 6.4.23 RSA Archer Suite

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment