|

시장보고서

상품코드

1851800

디지털 지도 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Digital Map - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

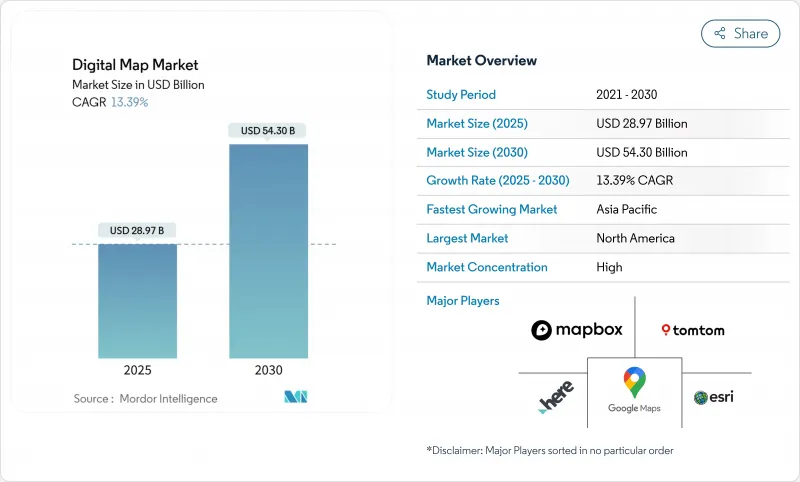

디지털 지도 시장의 2025년 시장 규모는 289억 7,000만 달러로, 2030년에는 543억 달러에 이르고, CAGR 13.39%를 나타낼 것으로 예측됩니다.

성장의 배경으로는 자율주행 차량, 스마트 시티 디지털 트윈, 실시간 지리 정보 시스템을 지원하는 AI를 갖춘 클라우드 네이티브 플랫폼으로의 전환이 있습니다. EU eCall 및 신흥 기업의 Scope 3 탄소 매핑 규칙과 같은 규제 의무화로 기존의 내비게이션 외에도 채택이 확산되고 있습니다.

세계의 디지털 지도 시장 동향과 인사이트

ADAS 및 자율주행 차량용 HD 맵의 급속한 보급

BMW는 2024년 독일 최초의 레벨 3 시스템을 시작해 HERE HD Live Map을 사용해 정위, 진로 계획, 운용 설계 영역의 검증에 17cm 이내의 차선 레벨의 정확도를 실현했습니다. HERE의 고정밀 커버리지는 현재 5,300만대의 차량을 지원하고 있으며, 2023년 대비 40% 증가하고 있으며, 턴키 HD 데이터에 대한 OEM의 의존을 보여주고 있습니다. TomTom의 Orbis Maps 3D는 8,600만km의 도로를 커버하며 차선 기반 내비게이션과 전기자동차 충전 레이어를 통합합니다. 일본의 다이나믹 맵 플랫폼은 2025년 정부의 지원을 받아 레벨 4의 자율주행 트럭을 타겟으로, 공항이나 항만에 HD 맵을 확대합니다. AI 기반의 특징 추출은 업데이트 비용을 낮추고, 지도 작성 주기를 단축하며, 거의 실시간으로 네트워크를 업데이트할 수 있는 공급자에게 경쟁 우위를 제공합니다.

커넥티드카 OTA 지도 갱신 생태계의 폭발적 성장

커넥티드카는 지도를 정적 라이선스에서 정기적인 OTA 서비스로 이동시킵니다. HARMAN의 Smart Delta 기술은 지도 업데이트 파일을 최대 97% 압축하여 소프트웨어 정의 차량의 안전을 유지하면서 데이터 전송 비용을 절감합니다. 전 세계 OEM 10개 중 9개사가 EU 일반 안전 규정을 준수하기 위해 HERE의 지능형 속도 지원 맵을 도입하여 차량 전체 업데이트를 위한 표준화된 OTA 경로를 구축하고 있습니다. 메르세데스 벤츠는 2025년 1월 OTA 릴리스를 통해 전기 인텔리전스와 오프로드 추적 기능을 통합하여 지도 데이터가 판매 후 기능 수익화를 가능하게 하는 방법을 보여줍니다.

지속적인 센티미터 수준 지도 업데이트 비용 상승

도시에서는 공사나 교통량의 변화가 격렬해지기 때문에 차선 레벨의 갱신이 필요해, 운용 비용이 대폭 상승합니다. TomTom은 현재 위성, LiDAR, 차량용 카메라 등의 멀티 센서 데이터를 융합하여 특징 추출의 자동화와 조사 사이클의 단축을 실현하고 있습니다. GetNexar의 AI 비전은 크라우드소싱으로 대시캠 이미지를 수집하여 지도 작성 비용을 절감합니다. 비용의 압력은지도의 정확성을 희생하지 않고 업데이트 속도를 유지하기 위해 제휴 및 선택적 아웃소싱을 촉구합니다.

부문 분석

소프트웨어 솔루션은 2024년 디지털 지도 시장의 61.40%를 차지했습니다. 이는 각 부서의 공간 분석을 통합하는 구성 가능한 API 기반 플랫폼에 대한 기업 수요를 반영합니다. 기능이 풍부한 SDK를 통해 개발자는 지도, 경로, 지오코딩을 이동성, 물류 및 소매 용도에 통합할 수 있습니다. 레거시 GIS를 클라우드 환경으로 마이그레이션하고 관리형 통합, 데이터 품질 튜닝 및 사용자 인에이블먼트 프로그램을 요구하기 때문에 복잡성이 커지고 있습니다. 최신 플랫폼의 AI 모듈은 라인 마크 감지, 라벨 인식, 자산 상태 스코어링을 자동화하여 비즈니스 효율성을 높입니다.

전문 서비스 이용은 위치 데이터 파이프라인 전문가의 감사를 필요로 하는 컴플라이언스의 의무화를 반영합니다. 문서, 동의 관리 도구 및 지오펜싱 정책 엔진은 국경을 넘어 합법적인 배포를 보장하기 위해 배포 프로젝트에 내장되어 있습니다. 기업의 데이터 양이 확대됨에 따라 벤더가 운영하는 관리형 서비스는 캡처, 정규화, 거의 실시간 스트리밍을 처리하고 있으며, 일회성 라이선스 요금에 그치지 않고 지속적인 수익을 확보하게 되었습니다.

클라우드 배포는 2024년 디지털 지도 시장 규모의 65.70%를 차지했고 2030년까지 연평균 복합 성장률(CAGR)은 15.70%를 나타낼 것으로 예측됩니다. 탄력적인 컴퓨팅 및 스토리지는 하루에 수십억 개의 루트 요청에 대해 초 이하의 쿼리 성능을 제공하지만 자동 스케일링은 악천후 및 휴일 시즌의 트래픽 피크를 처리합니다. Edge Injestion 노드는 신선한 프로브 데이터를 중앙 저장소로 푸시하여 라이드 헤일링, 물류 및 응급 상황에서 맵의 신선도를 보장합니다.

방위, 항공, 규제가 심한 금융 분야에서는 On-Premise 도입이 계속되고 있지만, 주권 클라우드 지역, 전용 호스트 옵션, 기밀 컴퓨팅 엔클레이브에 의해 보안상의 반대 의견이 완화됨에 따라 On-Premise 도입은 감소하는 경향이 있습니다. 비용 모델은 설비 투자에서 종량 과금 연산으로 전환되어 AI 실험 및 크로스 도메인 데이터 퓨전에 필요한 자금을 확보합니다. 엔터프라이즈는 맵핑을 단일 GIS 기능이 아닌 보다 광범위한 데이터 플랫폼 전략에서 소비되는 마이크로서비스로 간주합니다.

디지털 지도 시장은 솔루션(소프트웨어, 서비스), 배포(On-Premise, 클라우드), 맵 유형(내비게이션 맵, HD 및 실시간 맵, 토포그래피 및 테마틱 맵), 최종 사용자 산업(자동차, 엔지니어링 및 건설, 통신 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 디지털 지도 시장 점유율 29.6%를 차지해 소프트웨어 정의 차량, 클라우드 GIS, 국방지리공간 프로그램의 조기 도입이 결정수가 되었습니다. 연방 정부 기관은 개방형 공간 프레임워크를 추진하고 있으며, 자동차 제조업체는 자동화를 위한 연구 파이프라인을 개발하고 있습니다. 대규모 인프라 프로젝트는 디지털 지형 모델과 GNSS 머신 컨트롤을 채택하여 건설 사이클을 단축하고 자산의 라이프 사이클 가시성을 높입니다. 차량 텔레매틱스 공급자와 같은 데이터 관리 챔피언은 지역의 지도 정확도를 유지하는 익명화된 프로브 데이터를 지속적으로 제공합니다.

아시아태평양은 2030년까지의 CAGR이 15.4%로 가장 높고, 5G 가입자 증가, 스마트 모빌리티에의 자금 공급, 정부에 의한 디지털 트윈 의무화가 그 원동력이 되고 있습니다. 일본 산업계는 트럭 플래터닝과 대도시권 로보택시 파일럿을 위해 HD 코리도 데이터를 수집하여 HD 매핑 수요를 가속화시킵니다. 중국의 클라우드 제공업체는 전자상거래 물류를 강화하기 위해 대량의 위치 정보 API를 공개하고 인도의 5G 네트워크는 공공 및 농업 전체의 GIS 현대화를 자극합니다. 지역의 하이퍼스케일 데이터센터에 대한 투자도 데이터 주권 규칙에 대응하여 세계 벤더가 국내 엔드포인트를 통해 현지 고객에게 서비스를 제공할 수 있도록 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- ADAS 및 자율주행차용 HD 맵의 급속한 보급

- 커넥티드카의 OTA 지도 갱신 에코시스템의 폭발적 성장

- 클라우드 네이티브 GIS 플랫폼의 주류 채용

- 세계로 확대하는 스마트 시티 디지털 트윈 프로그램

- EU의 e콜 의무화와 차세대 교통안전규제

- 기업 스코프-3 카본 매핑 요건

- 시장 성장 억제요인

- 센티미터 단위의 지도 갱신에 드는 비용의 상승

- 데이터 프라이버시 및 현지화에 관한 법규제 강화(GDPR(EU 개인정보보호규정), PIPL)

- 데이터 제공업체와 OEM 간의 지재 라이선싱 분쟁

- AI가 작성한 지도에 있어서 알고리즘의 바이어스와 책임에 관한 우려

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 솔루션별

- 소프트웨어

- 서비스

- 배포별

- On-Premise

- 클라우드

- 지도 유형별

- 내비게이션 맵

- HD 및 실시간 지도

- 지형 및 주제별 지도

- 최종 이용 산업별

- 자동차

- 엔지니어링 및 건설

- 통신

- 공공 부문 및 방위

- 소매 및 지리 마케팅

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Alphabet(Google Maps, Waze)

- HERE Technologies

- TomTom International BV

- Esri

- Mapbox

- Apple Inc.(Apple Maps)

- Maxar Technologies(DigitalGlobe)

- Collins Bartholomew

- Digital Map Products

- Digital Mapping Solutions

- DMTI Spatial

- Lepton Software

- ThinkGeo

- MapData Services

- NavInfo Co. Ltd.

- AutoNavi(Gaode, Alibaba)

- Baidu Maps

- Nearmap Ltd

- Zenrin Co. Ltd.

- Trimble Inc.

- CARTO

- OpenStreetMap Foundation

- MapQuest(Verizon)

제7장 시장 기회와 향후 전망

KTH 25.11.17The digital map market is valued at USD 28.97 billion in 2025 and is projected to reach USD 54.30 billion by 2030, advancing at a 13.39% CAGR.

Growth stems from the transition toward AI-powered, cloud-native platforms that support autonomous vehicles, smart-city digital twins, and real-time geographic information systems. Regulatory mandates such as EU eCall and emerging corporate Scope 3 carbon-mapping rules broaden adoption beyond conventional navigation.

Global Digital Map Market Trends and Insights

Rapid Uptake of HD Maps for ADAS and Autonomous Vehicles

BMW launched Germany's first Level 3 system in 2024 using HERE HD Live Map that delivers lane-level accuracy within 17 cm for localization, path planning, and operational-design-domain validation. HERE's high-precision coverage now supports 53 million vehicles, a 40% rise over 2023, indicating OEM reliance on turnkey HD data. TomTom's Orbis Maps 3D spans 86 million km of roads and integrates lane-based navigation with electric-vehicle charging layers. Japan's Dynamic Map Platform received government backing in 2025 to expand HD maps to airports and ports, targeting Level 4 autonomous trucks. AI-based feature extraction lowers refresh costs and shortens map-creation cycles, delivering competitive advantage to providers able to update networks in near-real time.

Explosive Growth of Connected-Car OTA Map-Update Ecosystems

Connected vehicles are shifting maps from static licenses to recurring over-the-air services. HARMAN's Smart Delta technology compresses map-update files by up to 97%, cutting data-transfer costs while maintaining software-defined-vehicle safety integrity. Nine of ten global OEMs deploy HERE's Intelligent Speed Assistance Map to address EU General Safety Regulation compliance, creating standardized OTA pathways for fleet-wide updates. Mercedes-Benz integrated electric-intelligence and off-road tracking features via its January 2025 OTA release, illustrating how map data enables post-sale feature monetization.

Escalating Costs of Continuous, Centimeter-Level Map Refresh

Lane-level refresh requirements drive substantial operational costs as construction and traffic changes intensify in urban zones. TomTom now fuses multi-sensor data-satellite, LiDAR, onboard cameras-to automate feature extraction and cut survey cycles. GetNexar's AI vision reduces cartography expense by crowd-sourcing dash-cam imagery, yet capital requirements remain onerous for smaller vendors. Cost pressures encourage alliances and selective outsourcing to maintain update cadence without sacrificing map accuracy.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Adoption of Cloud-Native GIS Platforms

- Smart-City Digital-Twin Programs Scaling Globally

- Heightened Data-Privacy and Localization Statutes (GDPR, PIPL)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions captured 61.40% of the digital map market in 2024, reflecting enterprise demand for configurable, API-driven platforms that consolidate spatial analytics across departments. Feature-rich SDKs allow developers to embed maps, routing, and geocoding into mobility, logistics, and retail applications. Services revenue, growing at 13.50% CAGR, mirrors rising complexity as organizations migrate legacy GIS to cloud environments and seek managed integration, data-quality tuning, and user-enablement programs. AI modules within modern platforms automate line-mark detection, sign recognition, and asset-condition scoring, catalyzing operational efficiencies.

Professional-services uptake also reflects compliance mandates that require expert audits of location-data pipelines. Documentation, consent-management tools, and geo-fencing policy engines are bundled into implementation projects to ensure lawful deployment across borders. As enterprise data volumes scale, vendor-operated managed services increasingly handle ingestion, normalization, and near-real-time streaming, locking in recurring revenue beyond one-time license fees.

Cloud deployment held 65.70% share of the digital map market size in 2024 and is forecast to expand at 15.70% CAGR through 2030. Elastic compute and storage enable sub-second query performance for billions of daily route requests while auto-scaling manages traffic peaks during severe-weather or holiday seasons. Edge ingestion nodes push fresh probe data into centralized repositories, ensuring map freshness for ride-hailing, logistics, and emergency response.

On-premise installations persist in defense, aviation, and highly regulated finance but trend downward as sovereign-cloud regions, dedicated host options, and confidential-computing enclaves mitigate security objections. Cost models shift from capex to pay-as-you-go opex, freeing capital for AI experimentation and cross-domain data fusion. Enterprises increasingly view mapping as a micro-service consumed within broader data-platform strategies rather than a standalone GIS function.

Digital Map Market is Segmented by Solution (Software, Services), Deployment (On-Premise, Cloud), Map Type (Navigation Maps, HD and Real-Time Maps, Topographic and Thematic Maps), End User Industry (Automotive, Engineering and Construction, Telecommunications and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 29.6% digital map market share in 2024, anchored by early adoption of software-defined vehicles, cloud GIS, and defense geospatial programs. Federal agencies promote open spatial frameworks, and automotive OEMs maintain deep research pipelines for automation. Large-scale infrastructure projects employ digital terrain models and GNSS machine-control to shorten build cycles and enhance asset lifecycle visibility. Data-monetization champions such as fleet telematics providers continuously feed anonymized probe data that sustain regional map accuracy.

Asia-Pacific delivers the highest 15.4% CAGR through 2030, powered by 5G subscriber growth, smart-mobility funding, and government-backed digital-twin mandates. Japan's industry collects HD corridor data for truck platooning and metropolitan robo-taxi pilots, accelerating HD mapping demand. China's cloud providers expose high-volume location APIs to power e-commerce logistics, while India's 5G networks stimulate GIS modernization across utilities and agriculture. Investments in regional hyperscale data centers also address data-sovereignty rules, enabling global vendors to serve local customers via in-country endpoints.

- Alphabet (Google Maps, Waze)

- HERE Technologies

- TomTom International B.V.

- Esri

- Mapbox

- Apple Inc. (Apple Maps)

- Maxar Technologies (DigitalGlobe)

- Collins Bartholomew

- Digital Map Products

- Digital Mapping Solutions

- DMTI Spatial

- Lepton Software

- ThinkGeo

- MapData Services

- NavInfo Co. Ltd.

- AutoNavi (Gaode, Alibaba)

- Baidu Maps

- Nearmap Ltd

- Zenrin Co. Ltd.

- Trimble Inc.

- CARTO

- OpenStreetMap Foundation

- MapQuest (Verizon)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid uptake of HD maps for ADAS and autonomous vehicles

- 4.2.2 Explosive growth of connected-car OTA map-update ecosystems

- 4.2.3 Mainstream adoption of cloud-native GIS platforms

- 4.2.4 Smart-city digital-twin programs scaling globally

- 4.2.5 Mandatory EU eCall and next-gen road-safety regulations

- 4.2.6 Corporate Scope-3 carbon mapping requirements

- 4.3 Market Restraints

- 4.3.1 Escalating costs of continuous, centimetre-level map refresh

- 4.3.2 Heightened data-privacy and localization statutes (GDPR, PIPL)

- 4.3.3 IP-licensing disputes among data providers and OEMs

- 4.3.4 Algorithmic bias and liability concerns in AI-generated maps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Map Type

- 5.3.1 Navigation Maps

- 5.3.2 HD and Real-time Maps

- 5.3.3 Topographic and Thematic Maps

- 5.4 By End-use Industry

- 5.4.1 Automotive

- 5.4.2 Engineering and Construction

- 5.4.3 Telecommunications

- 5.4.4 Public Sector and Defense

- 5.4.5 Retail and Geomarketing

- 5.4.6 Other End User

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alphabet (Google Maps, Waze)

- 6.4.2 HERE Technologies

- 6.4.3 TomTom International B.V.

- 6.4.4 Esri

- 6.4.5 Mapbox

- 6.4.6 Apple Inc. (Apple Maps)

- 6.4.7 Maxar Technologies (DigitalGlobe)

- 6.4.8 Collins Bartholomew

- 6.4.9 Digital Map Products

- 6.4.10 Digital Mapping Solutions

- 6.4.11 DMTI Spatial

- 6.4.12 Lepton Software

- 6.4.13 ThinkGeo

- 6.4.14 MapData Services

- 6.4.15 NavInfo Co. Ltd.

- 6.4.16 AutoNavi (Gaode, Alibaba)

- 6.4.17 Baidu Maps

- 6.4.18 Nearmap Ltd

- 6.4.19 Zenrin Co. Ltd.

- 6.4.20 Trimble Inc.

- 6.4.21 CARTO

- 6.4.22 OpenStreetMap Foundation

- 6.4.23 MapQuest (Verizon)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment