|

시장보고서

상품코드

1851810

오토샘플러 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Autosamplers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

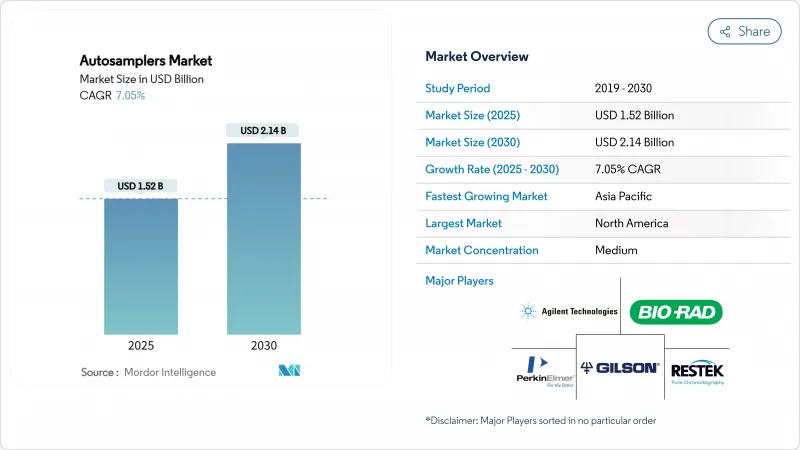

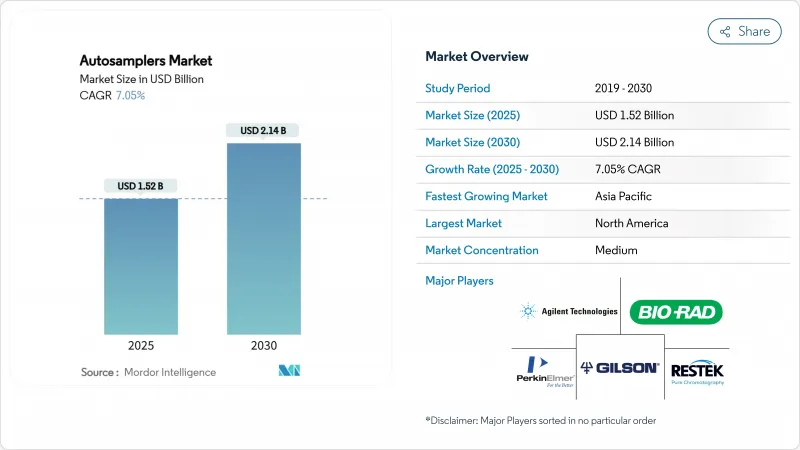

세계의 오토샘플러 시장 규모는 2025년 15억 2,000만 달러, 2030년까지 21억 4,000만 달러에 이를 것으로 추정 및 예측되며, 예측기간 중(2025-2030년) CAGR은 7.05%로 예상됩니다.

제약 품질 관리 실험실의 왕성한 교체 수요와 환경 및 식품 안전 검사량 증가는 안정적인 장비 수익을 지원합니다. FDA와 같은 규제 기관은 현재 상세한 분석법 검증을 요구하고 있으며, 실험실은 운영자의 변동을 없애고 데이터 무결성을 보호하는 자동 샘플 주입 플랫폼을 채택하도록 촉구하고 있습니다. 공급업체는 또한 유지보수 필요성을 예측하고 예기치 않은 다운타임을 줄이는 AI 지원 오토샘플러를 향한 지속적인 업그레이드를 통해 이익을 얻고 있습니다. 수돗물 중의 PFAS 화합물, 농산물 중의 잔류 농약, 신규 화학물질 중의 불순물에 대한 감시의 강화는 용도의 밑단을 더욱 넓혀, 오토샘플러 시장을 보다 높은 처리량과 감도의 향상으로 밀어 올리고 있습니다. 아시아태평양의 제조 거점에 대한 지속적인 설비 투자로 개발 도상국은 미래에 대용량 시스템의 중요한 수량 견인 역할을 할 것입니다.

세계 오토샘플러 시장 동향과 통찰

의약품 승인 워크 플로우에서 크로마토그래피의 역할 진전

FDA는 현재 분석법의 견고성에 대한 보다 엄격한 관리를 의무화하고 있으며, 이 시프트는 바이오 의약품 기업이 데이터 무결성에 대한 기대에 부응하기 위해 샘플 처리의 자동화를 강요하고 있습니다. 자동화된 오토샘플러는 휴먼 오류를 최소화하고 세계 제조 네트워크에서 재현성을 보장합니다. 통합된 샘플링 플랫폼에 의해 작성된 중앙 집중화된 디지털 감사 추적은 규제 당국에 제출 서류 작성을 가속화합니다. 복잡한 생물학적 제형은 다중 레인 크로마토그래피 시퀀싱를 필요로 하지만, 이는 무인 오토샘플러 조작에서만 실용적입니다. 바이오시밀러 개발자는 비교 가능성을 입증하기 위해 동일한 전략을 채택하여 새로운 치료제와 후속 치료제 모두에 대한 수요를 확대합니다. 그 결과, 오토샘플러 시장은 파이프라인을 통과하는 모든 후기 개발 프로그램으로부터 안정적인 양을 확보하고 있습니다.

세계적인 식품안전·환경규제 강화

EU의 Farm-to-Fork 목표와 미국 PFAS의 식수 기준 갱신은 기존의 수동 주입으로는 대응할 수 없는 낮은 검출 한계를 부과하고 있습니다. 따라서 식품 및 환경 실험실은 캐리오버를 억제하면서 고밀도 샘플 배치를 처리할 수 있는 오토샘플러를 통합합니다. 위탁시험기관은 규제 입찰을 이기기 위해 플랫폼을 업그레이드하고 3년에서 5년마다 교체를 촉구합니다. 장비 공급업체는 다양한 용기 유형에 해당하는 유연한 랙을 통합하여 환경과 식품 매트릭스 모두에 하나씩 대응할 수 있도록 하여 가동률을 향상시킵니다. 다국적 소매업체는 이제 공급업체 검증 규칙의 적용을 받고 공인 실험실 파트너를 요청하고 자본 사이클을 강화합니다. 이러한 상호 얽힌 압력은 농업, 물, 포장 산업에 걸친 오토샘플러 시장에 더욱 성장하고 있습니다.

숙련된 크로마토그래피 운영자 부족

많은 상급 분석가들이 대학이 후임을 육성하는 것보다 빨리 퇴직하기 때문에 실험실은 더 적은 전문가에 의존하지 않을 수밖에 없습니다. 기술 격차는 자동화 후에도 전문가의 모니터링이 필요한 방법 개발 프로젝트를 복잡하게 만듭니다. 소규모 실험실에서는 문제 해결을 위한 로컬 지원을 보장할 수 없기 때문에 오토샘플러 구매를 연기하는 경우가 많습니다. 장비 공급업체는 현재 인력 부족을 완화하기 위해 원격 진단 및 인증 교육을 번들로 제공하고 있지만, 여전히 온보딩은 사용을 수개월 지연시킵니다. 아시아태평양 국가들은 검사실의 급속한 확대가 교육 능력을 능가하기 때문에 인력 부족을 가장 통감합니다. 이 노동력 불균형은 운영자 파이프라인이 안정될 때까지 오토샘플러 시장의 잠재 수요의 일부를 억제합니다.

부문 분석

통합 오토샘플러 시스템은 2024년 오토샘플러 시장 점유율의 59.61%를 확보했습니다. 액체 크로마토그래피 모델은 HPLC와 UHPLC가 의약품 출시 시험의 핵심이기 때문에 출하량으로 선도하고 있습니다. 가스 크로마토그래피 시스템은 석유화학 법의학 및 환경 VOC 모니터링에서 관련성을 유지하며 듀얼 모드 설계는 하나의 인클로저에서 두 기술을 모두 지원합니다. 지속적인 펌웨어 업데이트는 원격 교정을 가능하게 하고 유지보수 요구를 20% 줄이고 검증된 생산 라인의 가동 시간을 보장합니다. 바이알, 주사기, 온도 제어 블록과 같은 액세서리는 공급업체가 장비 사이클의 변동에 대응할 수 있도록 정기적인 판매를 촉진합니다. 미량 주입이 가능한 그린 케미스트리 제품은 용매의 사용량을 40% 삭감하고 지속가능성을 중시하는 실험실 관리자에게 매력적인 지표가 됩니다. 예측 기간 동안 헤드스페이스와 SPME 플랫폼은 2030년까지 연평균 복합 성장률(CAGR) 10.64%에서 가장 빠르게 확대됩니다. 이러한 성장 역학은 톱 라인의 기세를 유지하고 오토샘플러 시장을 확대합니다.

소모품 및 모듈식 업그레이드도 전체 설치 기반의 평균 판매 가격을 인상합니다. 1,000개의 마이크로타이터 바이알을 수납할 수 있는 대용량 랙은 바이오 테크놀로지 기업에서의 세포 배양 대사물 스크리닝을 서포트해, 수작업에 의한 샘플 배치 처리를 대신합니다. AI에 의한 바늘 건강 진단은 씰 마모를 예측하고 교체 부품의 저스트 인 타임 주문을 촉진하고 예기치 않은 다운 타임을 줄입니다. 공급업체는 탈이온수 여과 장치와 인라인 탈기 장치를 적극적으로 교차 셀링하여 전체 분석 워크셀의 단일 소스 공급업체로 자리매김하고 있습니다. 이 번들 전략은 고객 유지를 강화하고 장치 1대당 평생 수익을 증대시킵니다. 따라서 핵심 시스템과 액세서리에 걸친 지속적인 기술 혁신은 향후 10년간 건전한 오토샘플러 시장 규모를 지원하고 있습니다.

지역 분석

북미는 2024년에 오토샘플러 시장 규모의 37.36%를 유지, 그 이유는 의약품 파이프라인의 충실, NIH 연구 보조금, EPA에 의한 오염물질 규제의 적극적인 시행에 있습니다. 미국 연구소는 AI를 활용한 오토샘플러를 조기에 채용해 프리미엄 가격을 정당화하는 생산성 향상을 꼽고 있습니다. 토론토와 밴쿠버에 위치한 캐나다 바이오 클러스터는 유전체 의료 시험을 위한 구매를 가속화하고 멕시코의 니어 쇼어 공장은 미국 수입 규정에 따라 분석 방법을 조정합니다. 공급업체의 서비스 네트워크와 소모품의 당일 배송은 지역 전체에서 높은 가동률을 유지합니다.

아시아태평양은 2030년까지 CAGR 12.09%로 예상되며 세계 최고 속도입니다. 중국과 인도는 제제와 활성 성분의 제조를 확대하고 세계 아웃소싱 계약을 획득하기 때문입니다. 선전과 하이데라바드에서는 정부 보조금이 자동화 자본 비용의 최대 30%를 상쇄하여 다중 라인 배치를 촉진합니다. 국내 기기 제조업체가 대기업 브랜드와 제휴해, 저가격 제품을 공동 개발해, 현 레벨의 환경국에 대한 진출을 확대합니다. 한국과 일본은 정밀의료 이니셔티브를 위한 임상진단 자동화를 중시하여 지역 수요를 다양화시킵니다. 이 기세가 함께 오토샘플러 시장은 기존의 서양 틈새 시장이 아니라 진정한 세계 시장으로 재정의됩니다.

유럽에서는 REACH 화학물질 규제와 잔류농약의 엄격한 모니터링을 의무화하는 Farm-to-Fork 전략에 의해 꾸준한 성장을 기록합니다. 독일의 주요 화학 제조 업체는 기업의 탄소 목표 달성을 위해 기존의 QC 실험실을 용제 절약 오토샘플러로 개수합니다. 영국은 EU 이탈 후에도 EU 분석 지령에 병행하여 대응하여 투자의 연속성을 유지합니다. 폴란드와 체코 공화국의 동유럽 CRO 클러스터는 비용 우위성을 살려 생물학적 동등성 시험을 획득하여 장비의 추가 주문에 탄력을 줍니다. 중동 및 아프리카와 남미는 자금 갭과 기술 스킬 부족의 제약을 받으면서도 확대되는 석유화학과 식품 수출 부문에 지지되어 서서히 도입이 진행되고 있습니다. 전반적으로 지역 동향은 오토샘플러 시장의 지역별 판매에 대한 궤도를 강화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의약품 승인 워크플로우에서 크로마토그래피의 역할 진전

- 세계 식품 안전 및 환경 규제 강화

- 분석 처리량 향상을 위한 실험실 자동화 추진

- 오믹스 주도형 임상 진단의 확대

- AI를 활용한 예지보전 오토샘플러 시장

- 그린케미스트리의 마이크로 볼륨 인젝션 디자인

- 시장 성장 억제요인

- 숙련된 크로마토그래피 오퍼레이터 부족

- 중소기업 실험실의 고액 설비투자와 예산 한계

- 엄격한 검증 및 컴플라이언스 타임라인

- 지재의 분단과 특허 소송 리스크

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(단위: 달러)

- 제품별

- 시스템

- 액체 크로마토그래피 오토샘플러 시장

- 가스 크로마토그래피 오토샘플러 시장

- 헤드스페이스 및 SPME 오토샘플러 시장

- 액세서리

- 시스템

- 최종 사용자별

- 제약 및 바이오 제약 기업

- 환경 및 물 시험 실험실

- 학술 및 수탁 연구실

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Agilent Technologies, Inc.

- Thermo Fisher Scientific Inc.

- Shimadzu Corporation

- Waters Corporation

- PerkinElmer Inc.

- Bio-Rad Laboratories Inc.

- Gilson Inc.

- Restek Corporation

- Scion Instruments

- Tecan Group Ltd.

- HTA srl

- KNAUER Wissenschaftliche Gerate GmbH

- CTC Analytics AG

- Trajan Scientific(LEAP)

- GERSTEL GmbH

- DANI Instruments SpA

- LCTech GmbH

- ModuVision Technologies

- Valco Instruments(VICI)

- Ellutia Ltd.

제7장 시장 기회와 장래의 전망

JHS 25.11.25The Autosamplers Market size is estimated at USD 1.52 billion in 2025, and is expected to reach USD 2.14 billion by 2030, at a CAGR of 7.05% during the forecast period (2025-2030).

Strong replacement demand from pharmaceutical quality-control laboratories, together with growing environmental and food-safety testing volumes, sustains steady equipment revenues. Regulatory bodies such as the FDA now require detailed analytical method validation, prompting laboratories to adopt automated sample-injection platforms that eliminate operator variability and safeguard data integrity. Vendors also benefit from continuous upgrades toward AI-ready autosamplers that predict maintenance needs and reduce unplanned downtime. Heightened scrutiny of PFAS compounds in water supplies, pesticide residues in produce, and impurities in new chemical entities further widens the application base, pushing the autosamplers market toward higher throughput and improved sensitivity. Ongoing capital investment in Asia Pacific manufacturing sites positions developing nations as critical future volume drivers for high-capacity systems.

Global Autosamplers Market Trends and Insights

Advancing Role of Chromatography in Drug Approval Workflows

The FDA now mandates tighter controls on analytical method robustness, and that shift forces biopharma companies to automate sample handling to comply with data-integrity expectations. Automated autosamplers minimize human error, thereby ensuring reproducibility across global manufacturing networks. Centralized digital audit trails created by integrated sampling platforms accelerate dossier assembly for regulatory submissions. Complex biologic molecules demand multi-lane chromatography sequences, which are only practical with unattended autosampler operation. Biosimilar developers adopt identical strategies to prove comparability, extending demand across both novel and follow-on therapeutics. In consequence, the autosamplers market secures stable volumes from every late-stage development program moving through the pipeline.

Tighter Global Food-Safety & Environmental Regulations

EU Farm-to-Fork objectives and updated US drinking-water standards for PFAS impose lower detection limits that conventional manual injection cannot meet. Food and environmental laboratories therefore integrate autosamplers capable of processing dense sample batches while holding low carry-over. Contract testing organizations upgrade platforms to win regulatory tenders, driving replacement purchases every three to five years. Equipment vendors embed flexible racks that accept diverse container types, allowing a single unit to address both environmental and food matrices, which improves utilization. Multinational retailers, now subject to supplier-verification rules, demand certified laboratory partners, reinforcing capital cycles. These intertwined pressures add incremental growth to the autosamplers market across agriculture, water, and packaging industries.

Shortage of Chromatography-Skilled Operators

Many senior analysts retire faster than universities can train replacements, pushing laboratories to depend on fewer specialists. The skills gap complicates method-development projects that still require expert oversight even after automation. Small laboratories often postpone autosampler purchases because they cannot guarantee local support for troubleshooting. Equipment suppliers now bundle remote diagnostics and certified training to mitigate the talent deficit, yet onboarding still delays utilization by several months. Asia Pacific nations feel the shortage most acutely due to rapid laboratory expansion outstripping educational capacity. This workforce imbalance suppresses a portion of latent demand in the autosamplers market until operator pipelines stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Lab-Automation Push for Higher Analytical Throughput

- Expansion of Omics-Driven Clinical Diagnostics

- High Capex & Budget Limits at SME Labs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated autosampler systems secured 59.61% of autosamplers market share in 2024 as laboratories favored turnkey combinations that align mechanically and electronically with chromatography instruments. Liquid chromatography models lead volume shipments because HPLC and UHPLC remain the backbone of pharmaceutical release testing. Gas chromatography systems maintain relevance in petrochemical forensics and environmental VOC monitoring, while dual-mode designs support both techniques within one chassis. Continuous firmware updates now enable remote calibration that cuts maintenance calls by 20%, ensuring uptime for validated production lines. The complementary accessories subsegment vials, syringes, temperature-control blocks drives recurring sales that cushion vendors against equipment-cycle swings. Green-chemistry variants with micro-volume injection reduce solvent use by 40%, an attractive metric for sustainability-focused laboratory managers. Over the forecast horizon, headspace and SPME platforms expand fastest at a 10.64% CAGR through 2030, propelled by global rules on aromatic hydrocarbon and organophosphate residues in food and soil. These growth dynamics preserve top-line momentum and broaden the autosamplers market.

Consumables and modular upgrades also lift average selling prices across installed bases. High-capacity racks that hold 1,000 microtiter vials support cell-culture metabolite screening at biotech firms, replacing manual sample batching. AI-driven needle health diagnostics now predict seal wear, triggering just-in-time ordering of replacement parts and reducing unexpected downtime. Vendors actively cross-sell de-ionized water filtration units and in-line degassers, embedding themselves as single-source suppliers for entire analytical workcells. This bundling strategy reinforces customer retention and amplifies lifetime revenues per instrument. Sustained innovation across core systems and accessories therefore underpins a healthy autosamplers market size during the coming decade.

The Autosamplers Market Report is Segmented by Product (Systems [Liquid Chromatography Autosamplers, Gas Chromatography Autosamplers, Headspace & SPME Autosamplers] and Accessories), End User (Pharmaceutical & Biopharmaceutical Companies, Environmental & Water-Testing Labs, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 37.36% of autosamplers market size in 2024 because of deep pharmaceutical pipelines, NIH research grants, and active EPA enforcement of contaminant rules. US laboratories adopt AI-enhanced autosamplers early, citing productivity gains that justify premium pricing. Canadian biotech clusters in Toronto and Vancouver accelerate purchases for genomic medicine trials, while Mexican near-shore plants align analytical methods with US import regulations. Vendor service networks and same-day consumables delivery sustain high uptime across the region.

Asia Pacific posts a 12.09% CAGR through 2030, the fastest worldwide, as China and India expand formulation and active-ingredient manufacturing to capture global outsourcing contracts. Government subsidies in Shenzhen and Hyderabad offset up to 30% of automation capital costs, catalyzing multi-line deployments. Domestic instrument makers partner with leading brands to co-develop low-price variants, expanding reach into county-level environmental bureaus. South Korea and Japan emphasize clinical-diagnostic automation for precision-medicine initiatives, thereby diversifying regional demand. The combined momentum redefines the autosamplers market as a truly global arena rather than a legacy Western niche.

Europe records steady growth driven by REACH chemical regulations and the Farm-to-Fork strategy that mandates rigorous monitoring of pesticide residues. German chemical giants retrofit legacy QC labs with solvent-saving autosamplers to hit corporate carbon targets. The United Kingdom continues parallel compliance with EU analytical directives post-Brexit, preserving investment continuity. Eastern European CRO clusters in Poland and the Czech Republic leverage cost advantages to win bioequivalence studies, fueling additional equipment orders. Middle East & Africa and South America follow with gradual adoption, constrained by financing gaps and technical-skills shortages yet supported by expanding petrochemical and food-export sectors. Overall, geography trends collectively strengthen the autosamplers market trajectory toward diversified regional sales.

- Agilent Technologies

- Thermo Fisher Scientific

- Shimadzu

- Waters Corporation

- PerkinElmer

- Bio-Rad Laboratories

- Gilson

- Restek

- Scion Instruments

- Tecan Group

- HTA s.r.l.

- KNAUER Wissenschaftliche Gerate GmbH

- CTC Analytics AG

- Trajan Scientific (LEAP)

- GERSTEL GmbH

- DANI Instruments SpA

- LCTech GmbH

- ModuVision Technologies

- Valco Instruments (VICI)

- Ellutia Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancing Role of Chromatography in Drug Approval Workflows

- 4.2.2 Tighter Global Food-Safety & Environmental Regulations

- 4.2.3 Lab-Automation Push for Higher Analytical Throughput

- 4.2.4 Expansion of Omics-Driven Clinical Diagnostics

- 4.2.5 Ai-Enabled Predictive-Maintenance Autosamplers

- 4.2.6 Green-Chemistry Micro-Volume Injection Designs

- 4.3 Market Restraints

- 4.3.1 Shortage of Chromatography-Skilled Operators

- 4.3.2 High Capex & Budget Limits at Sme Labs

- 4.3.3 Stringent Validation & Compliance Timelines

- 4.3.4 Fragmented IP & Patent-Litigation Risks

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Systems

- 5.1.1.1 Liquid Chromatography Autosamplers

- 5.1.1.2 Gas Chromatography Autosamplers

- 5.1.1.3 Headspace & SPME Autosamplers

- 5.1.2 Accessories

- 5.1.1 Systems

- 5.2 By End User

- 5.2.1 Pharmaceutical & Biopharmaceutical Companies

- 5.2.2 Environmental & Water-Testing Labs

- 5.2.3 Academic & Contract Research Laboratories

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agilent Technologies, Inc.

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 Shimadzu Corporation

- 6.3.4 Waters Corporation

- 6.3.5 PerkinElmer Inc.

- 6.3.6 Bio-Rad Laboratories Inc.

- 6.3.7 Gilson Inc.

- 6.3.8 Restek Corporation

- 6.3.9 Scion Instruments

- 6.3.10 Tecan Group Ltd.

- 6.3.11 HTA s.r.l.

- 6.3.12 KNAUER Wissenschaftliche Gerate GmbH

- 6.3.13 CTC Analytics AG

- 6.3.14 Trajan Scientific (LEAP)

- 6.3.15 GERSTEL GmbH

- 6.3.16 DANI Instruments SpA

- 6.3.17 LCTech GmbH

- 6.3.18 ModuVision Technologies

- 6.3.19 Valco Instruments (VICI)

- 6.3.20 Ellutia Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment