|

시장보고서

상품코드

1910613

확장현실(XR) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Extended Reality (XR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

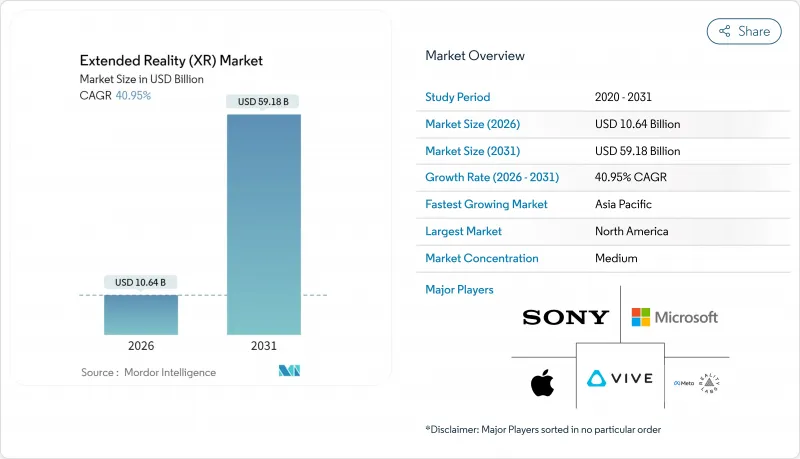

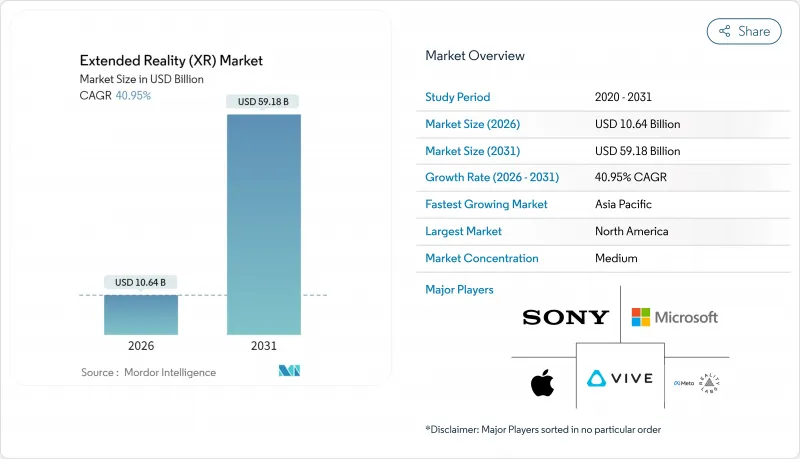

확장현실(XR) 시장의 규모는 2026년에는 106억 4,000만 달러에 달할 것으로 예측되고 있습니다.

이는 2025년 75억 5,000만 달러에서 성장한 수치이며, 2031년에는 591억 8,000만 달러에 이를 것으로 전망되고 있습니다. 2026년부터 2031년까지의 연평균 성장률(CAGR)은 40.95%를 나타낼 전망입니다.

제조업, 의료, 방위 분야 기업의 급속한 도입이 소비자용 엔터테인먼트 분야를 상회하며 XR은 게임 전용의 참신한 기술에서 업무에 불가결한 생산성 향상 툴로 변모하고 있습니다. 5세대 모바일 네트워크와 엣지 컴퓨팅의 조합은 지연 장벽을 해소하고 공장 현장과 수술실에서 밀리초 단위의 정확한 시각화를 실용화하고 있습니다. 공간 컴퓨팅에 통합된 인공지능은 교육 컨텐츠를 개별화하고 실시간 분석이 피드백 루프를 통해 측정 가능한 수익성을 더욱 향상시킵니다. 미국과 중국의 정부 자금 지원과 OpenXR과 같은 개방형 표준이 결합되어 생태계의 성숙을 가속화하고 공급업체 종속 우려를 해소합니다. 공급망의 제약과 부품 가격의 상승은 여전히 과제이지만, 신규 반도체 생산 능력과 대체 재료의 조달원이 생산 단계에 들어가면서 완화되고 있습니다.

세계의 확장현실(XR) 시장의 동향 및 인사이트

5G 커버리지 확대 및 엣지 컴퓨팅의 시너지 효과

에릭슨, AT&T, 드림스케이프, 퀄컴에 의한 시험에서 나타났듯이, 20ms 미만의 저지연으로 인해 백팩형 PC를 필요로 하지 않는 다중 사용자 VR 협업이 가능해졌습니다. 중국철강(CSCC)사의 5G 지원 가상 공장 견학은 85개의 생산 노드에서 실시간 데이터를 통합하여 중공업에서의 가치를 입증합니다. DHL사의 스마트 글래스 시험 운영은 실시간 피킹 지침을 통한 물류 효율 향상을 보여줍니다. 연산 처리가 네트워크 엣지로 이동하면 장치 중량이 줄어들고 작업 시간의 효율이 향상됩니다. 이 때문에 통신사업자는 몰입형 처리량을 유지하기 위해 사용자로부터 50km 이내에 마이크로 데이터센터를 설치하고 있습니다.

XR 기술을 디지털 트윈 및 인더스트리 4.0 프레임워크와 통합

페가트론사의 PEGAVERSE는 NVIDIA Omniverse에 5개의 가상 공장을 구축하여 원격 진단과 시나리오 테스트를 실현하여 가동 중지 시간과 출장을 줄였습니다. BASF사의 AR 대응 플랜트 계획에서는 센서 데이터와 몰입형 가시화를 연계시켜 위험 개소의 특정을 효율화하고 있습니다. 지멘스와 소니는 픽셀 단위의 정확한 설계 협업을 실현하는 엔지니어링 헤드셋 "SRH-S1"을 4,750 달러에 제공하고 있습니다. OpenUSD의 무결성을 통해 다른 CAD, PLM, IoT 피드를 단일 공간 레이어에 통합할 수 있습니다. 플랫폼 공급업체는 단일 라이선스 비용이 아닌 구독 기반 시각화 서비스로 수익을 창출하고 있습니다.

고화질 광학 장비 및 프로세서의 높은 초기 비용

갈륨과 게르마늄의 공급 부족으로 광학 기기의 가격은 최대 25% 상승하고 있습니다. Meta사의 Reality Labs는 2020년 이후 600억 달러의 손실을 기록했지만, 2024년 4분기에는 XR 하드웨어에서 11억 달러의 수익을 달성하여 수익성 과제를 부각시켰습니다. 자본이나 명확한 투자이익률(ROI)이 없는 중소기업은 진입을 망설이고 있습니다. 클라우드 렌더링을 통한 XR은 터미널 부하를 줄이지만 지연이라는 트레이드 오프가 발생하여 이용은 5G가 충분히 정비된 지역으로 제한됩니다.

부문 분석

2024년의 수익 구성비는 하드웨어가 53.2%를 차지했지만, 서비스 부문이 CAGR 42.5%로 가장 빠르게 성장할 전망입니다. 디바이스 소프트웨어 및 관리 지원을 결합한 구독 번들은 설비 투자(CapEx)를 운영 비용(OpEx)으로 변환하는 구조로 재무 부문을 뒷받침합니다. 이러한 전환은 공급업체에게 예측 가능한 지속적인 수익을 창출하고 고객에게는 진입 장벽을 저하시킵니다. Meta사의 플랫폼 전환은 이러한 움직임을 구현하며 하드웨어 업데이트와 병행하여 기업용 구독을 모색하고 있습니다.

매니지드 교육 및 시뮬레이션 서비스는 전문적인 컨텐츠 수요로 높은 단가를 실현합니다. 버텍스 솔루션사 단독으로만 세계에 500대 이상의 군용 등급 시뮬레이터를 출하하여 수직 분야의 전문성을 보여줍니다. 이러한 계약은 수년에 걸친 경우가 많기 때문에 벤더는 높은 평생 가치를 얻을 수 있습니다. 하드웨어 제조업체는 직접 경쟁보다 통합자와 제휴하는 경향이 있으며 서비스 중심의 확장현실(XR) 시장이 성숙하고 있음을 반영합니다.

헤드 마운트 디스플레이는 2024년에 42.7%의 수익을 차지했지만, 성장은 현재 공간 표시 및 홀로그래픽 디스플레이로 이행하고 있어 43.1%의 연평균 복합 성장률(CAGR)을 목표로 하고 있습니다. 공유 뷰잉 월은 개인용 헤드셋에서 볼 수 있는 위생 및 쾌적성의 한계를 극복하고 공동 엔지니어링 검토 및 고객 데모를 지원합니다. 삼성의 'Project Moohan'은 산업 도입에 최적화된 차세대 독립형 유닛의 좋은 예입니다.

안경이 필요 없는 솔루션도 등장하고 있으며, Distance Technologies사는 1,000만 유로(1,173만 달러)를 조달하여 차량의 창을 동적인 복합 현실 캔버스로 전환합니다. 스마트폰 연결형 핸드헬드 장치는 현장 유지보수에서 여전히 널리 사용되고 있으며, 헤드업 디스플레이는 항공기와 자동차 운전석에서 틈새 시장을 확립하고 있습니다. 장기적으로 XPANCEO사의 프로토타입과 같은 스마트 콘택트렌즈는 확장현실 시장을 눈에 보이지 않는 웨어러블 영역으로 확장할 수 있습니다.

확장현실(XR) 시장은 제공 형태(하드웨어, 소프트웨어, 서비스), 디바이스 유형(헤드 마운트 디스플레이(유선 연결형, 독립형), 헤드업 디스플레이 등), 기술(가상현실(VR), 증강현실(AR), 복합현실(MR)), 최종 사용자 산업(게임 및 엔터테인먼트, 의료 및 생명과학 등)에 의해 세분화되며 시장 예측은 금액, 달러 기준으로 제공됩니다.

지역별 분석

북미에서는 의료, 항공우주, 방위 분야에서 꾸준한 조달로 설치 기반이 확대되고 있습니다. Infinite Reality사는 신규 자본 3억 5,000만 달러를 조달하여 Landvault사를 4억 5,000만 달러에 인수했습니다. 이는 공간 컴퓨팅 플랫폼에 대한 투자자의 낙관적인 관점을 뒷받침합니다. 미국 국방부의 혁신 유닛은 공군 기지에 225대의 몰입형 훈련 장치를 도입하여 기업용 XR 이용을 더욱 정착시키고 있습니다. 항공 분야의 대체 인증 규제 지원은 시뮬레이터의 정확도가 물리적 조종석 기준에 가까워짐에 따라 장비 주문을 촉진합니다.

아시아태평양은 가장 빠르게 확대되는 지역입니다. 중국에서만 2024년에 100건 이상의 VR 프로젝트를 개시하였으며, 한국은 거의 전국을 커버하는 5G망을 활용해 삼성의 'Project Moohan' 개시를 준비 중입니다. 인도에서는 Meta와 HCltech와의 정부-민간 공동 인큐베이터가 현지 애플리케이션 개발회사를 육성하고 있습니다. 광범위한 제조거점이 지속적인 가치 실증 파일럿을 지원하고 하드웨어의 양산 경제에서 APAC가 핵심 역할을 담당하고 있습니다. 유럽은 책임있는 혁신 기지로서의 지위를 확립하고 있습니다. Distance Technologies사의 1,000만 유로(약 1,173만 달러) 시드 자금 조달은 자동차 등급의 복합현실(MR) 표면에 대한 수요의 높이를 보여줍니다. BASF, 지멘스, 소니는 엄격한 CE 안전 기준을 준수하는 헤드셋 엔지니어링에서 협력하고 있습니다. EU의 프라이버시 규정은 데이터 처리 아키텍처를 형성하고 세계 공급업체가 GDPR(EU 개인정보보호규정) 지원 분석 모듈을 구축하도록 촉구하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 5G 커버리지의 확대와 엣지 컴퓨팅의 시너지 효과

- XR 기술의 디지털 트윈 및 인더스트리 4.0 프레임워크로의 통합 진전

- 몰입형 원격 트레이닝에 대한 기업 수요 증가

- 일반 스마트폰과 공간 센서의 통합

- 메타버스 관련 연구개발(R&D)에 대한 정부 자금

- 오픈 XR 표준의 도입에 의한 벤더 종속 감소

- 억제요인

- 고화질 광학 기기 및 프로세서의 높은 초기 비용

- 사용자의 동요 및 인체공학적 제약

- 아이트래킹 및 핸드트래킹 분석에서의 데이터 프라이버시 과제

- 단편화된 컨텐츠 작성 툴 에코시스템

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 공급자의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장에 대한 거시경제적 요인 평가

제5장 시장 규모 및 성장 예측

- 제공별

- 하드웨어

- 소프트웨어

- 서비스

- 디바이스 유형별

- 헤드 마운트 디스플레이(유선 연결형, 독립형)

- 헤드업 디스플레이

- 핸드헬드 및 모바일 디바이스

- 기타

- 기술별

- 가상현실(VR)

- 증강현실(AR)

- 복합현실(MR)

- 최종 사용자 산업별

- 게임 및 엔터테인먼트

- 의료 및 생명과학

- 산업 및 제조업

- 소매 및 전자상거래

- 교육 및 트레이닝

- 항공우주 및 방위

- 아키텍처, 엔지니어링 및 건설

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Meta Platforms Inc.(Reality Labs)

- Sony Group Corp.

- Microsoft Corp.

- Apple Inc.

- HTC Corp.(Vive)

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Alphabet Inc.(Google XR)

- Pico Interactive Inc.(ByteDance)

- Varjo Technologies Oy

- Magic Leap Inc.

- Nvidia Corp.

- Unity Technologies Inc.

- Vuzix Corp.

- Lenovo Group Ltd.

- Snap Inc.

- Niantic Inc.

- Ultraleap Ltd.

- HP Inc.

- Immersion Corp.

제7장 시장 기회 및 미래 전망

CSM 26.01.28Extended Reality market size in 2026 is estimated at USD 10.64 billion, growing from 2025 value of USD 7.55 billion with 2031 projections showing USD 59.18 billion, growing at 40.95% CAGR over 2026-2031.

Rapid enterprise adoption across manufacturing, healthcare, and defense now outpaces consumer entertainment, turning XR from a gaming novelty into a mission-critical productivity tool. Five-generation mobile networks paired with edge computing have erased latency barriers, making millisecond-accurate visualization practical on factory floors and in surgical suites. Artificial intelligence embedded in spatial computing personalizes training content while real-time analytics close feedback loops, further raising measurable returns. Government funding in the United States and China, coupled with open standards such as OpenXR, is accelerating ecosystem maturity and reducing vendor lock-in worries. Supply chain constraints and component price inflation remain headwinds but continue to ease as new semiconductor capacity and alternative material sourcing enter production.

Global Extended Reality (XR) Market Trends and Insights

Expanding 5G Coverage and Edge Computing Synergy

Sub-20 ms latency now enables multi-user VR collaboration without tethered backpack PCs, as trials by Ericsson, AT&T, Dreamscape, and Qualcomm have shown. China Steel Corporation's 5G-enabled virtual factory tours integrate live data from 85 production nodes, proving value for heavy industry. DHL smart-glasses pilots illustrate logistics gains from real-time pick guidance. Device weight drops as compute moves to the network edge, boosting shift-length comfort. Telcos therefore place micro-data-centers within 50 km of users to sustain immersive throughput.

Increased Integration of XR into Digital Twin and Industry 4.0 Frameworks

Pegatron's PEGAVERSE builds five virtual factories on NVIDIA Omniverse for remote diagnostics and scenario testing, lowering downtime and travel. BASF's AR-enabled plant planning links sensor data with immersive visualization to streamline hazard identification. Siemens and Sony priced the SRH-S1 engineering headset at USD 4,750 to deliver pixel-accurate design collaboration. OpenUSD alignment lets disparate CAD, PLM, and IoT feeds merge into a single spatial layer. Platform vendors thus monetize subscription-based visualization rather than one-off license fees.

High Upfront Costs of High-Fidelity Optics and Processors

Gallium and germanium shortages have inflated optics prices by up to 25%. Meta's Reality Labs has accumulated USD 60 billion losses since 2020 while selling USD 1.1 billion in Q4 2024 XR hardware, underscoring profitability challenges. Smaller firms hesitate without capital or clear ROI. Cloud-rendered XR lightens devices yet introduces latency trade-offs that limit usage to well-served 5G zones.

Other drivers and restraints analyzed in the detailed report include:

- Rising Enterprise Demand for Immersive Remote Training

- Mass-Market Smartphone Integration of Spatial Sensors

- User Motion-Sickness and Ergonomic Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware controlled 53.2% of revenue in 2024, yet Services is set to grow fastest at 42.5% CAGR. Subscription bundles that combine devices, software, and managed support convert capex into opex, a structure favored by finance departments. The shift drives predictable recurring income for suppliers and lowers barrier-to-entry for customers. Meta's platform pivot illustrates this movement, exploring enterprise-grade subscriptions alongside hardware refreshes.

Managed training and simulation services command premium rates thanks to specialized content needs. Vertex Solutions alone shipped more than 500 military-grade simulators worldwide, highlighting vertical expertise. As these contracts often span multi-year periods, vendors capture higher lifetime value. Hardware makers therefore partner with integrators rather than compete head-on, reflecting a maturing services-led Extended Reality market.

Head-Mounted Displays captured 42.7% revenue in 2024 but growth now shifts to Spatial and Holographic Displays, which head toward a 43.1% CAGR. Shared viewing walls overcome hygiene and comfort limits found in personal headsets, supporting collaborative engineering reviews and customer demonstrations. Samsung's Project Moohan exemplifies next-generation standalone units optimized for industrial deployment.

Glasses-free solutions also emerge, with Distance Technologies raising EUR 10 million (USD 11.73 million) to transform vehicle windows into dynamic mixed-reality canvases. Smartphone-tethered handheld devices remain common in field maintenance, while head-up displays secure niche positions in aviation and automotive cockpits. Longer term, smart contact lenses such as XPANCEO's prototype could push the Extended Reality market into invisible wearables.

Extended Reality (XR) Market is Segmented by Offering (Hardware, Software, Services), Device Type (Head-Mounted Displays (Tethered, Stand-Alone), Head-Up Displays and More), Technology (Virtual Reality (VR), Augmented Reality (AR), Mixed Reality (MR)), End User Industry (Gaming and Entertainment Healthcare and Life Sciences, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's installed base expands through steady healthcare, aerospace, and defense procurement. Infinite Reality closed USD 350 million in new capital and bought Landvault for USD 450 million, underscoring investor optimism in spatial computing platforms. The US Defense Innovation Unit fielded 225 immersive trainers across Air Force sites, further entrenching enterprise XR usage. Regulatory support for alternative certification in aviation spurs equipment orders as simulator fidelity approaches physical cockpit standards.

Asia-Pacific scales fastest. China alone launched more than 100 VR projects in 2024. South Korea readies Samsung's Project Moohan release, leveraging the country's near-universal 5G coverage. India's public-private incubator with Meta and HCLTech cultivates grassroots application developers. Wide manufacturing bases feed continuous proof-of-value pilots, making APAC pivotal to hardware volume economics. Europe positions itself as the responsible innovation hub. Distance Technologies' EUR 10 million (USD 11.73 million) seed illustrates appetite for automotive-grade mixed-reality surfaces. BASF, Siemens, and Sony collaborate on engineering headsets that comply with strict CE safety norms. The EU's privacy regime shapes data-handling architectures, influencing global vendors to build GDPR-ready analytics modules.

- Meta Platforms Inc. (Reality Labs)

- Sony Group Corp.

- Microsoft Corp.

- Apple Inc.

- HTC Corp. (Vive)

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Alphabet Inc. (Google XR)

- Pico Interactive Inc. (ByteDance)

- Varjo Technologies Oy

- Magic Leap Inc.

- Nvidia Corp.

- Unity Technologies Inc.

- Vuzix Corp.

- Lenovo Group Ltd.

- Snap Inc.

- Niantic Inc.

- Ultraleap Ltd.

- HP Inc.

- Immersion Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding 5G coverage and edge computing synergy

- 4.2.2 Increased integration of XR into digital twin and Industry 4.0 frameworks

- 4.2.3 Rising enterprise demand for immersive remote-training

- 4.2.4 Mass-market smartphone integration of spatial sensors

- 4.2.5 Government funding for metaverse-related Rand

- 4.2.6 Adoption of open XR standards lowering vendor lock-in

- 4.3 Market Restraints

- 4.3.1 High upfront costs of high-fidelity optics and processors

- 4.3.2 User motion-sickness and ergonomic limitations

- 4.3.3 Data-privacy gaps in eye- and hand-tracking analytics

- 4.3.4 Fragmented content-authoring tool ecosystem

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Device Type

- 5.2.1 Head-Mounted Displays (Tethered, Stand-alone)

- 5.2.2 Head-Up Displays

- 5.2.3 Handheld and Mobile Devices

- 5.2.4 Others

- 5.3 By Technology

- 5.3.1 Virtual Reality (VR)

- 5.3.2 Augmented Reality (AR)

- 5.3.3 Mixed Reality (MR)

- 5.4 By End-user Industry

- 5.4.1 Gaming and Entertainment

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Industrial and Manufacturing

- 5.4.4 Retail and E-commerce

- 5.4.5 Education and Training

- 5.4.6 Aerospace and Defense

- 5.4.7 Architecture, Engineering and Construction

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Meta Platforms Inc. (Reality Labs)

- 6.4.2 Sony Group Corp.

- 6.4.3 Microsoft Corp.

- 6.4.4 Apple Inc.

- 6.4.5 HTC Corp. (Vive)

- 6.4.6 Qualcomm Technologies Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 Alphabet Inc. (Google XR)

- 6.4.9 Pico Interactive Inc. (ByteDance)

- 6.4.10 Varjo Technologies Oy

- 6.4.11 Magic Leap Inc.

- 6.4.12 Nvidia Corp.

- 6.4.13 Unity Technologies Inc.

- 6.4.14 Vuzix Corp.

- 6.4.15 Lenovo Group Ltd.

- 6.4.16 Snap Inc.

- 6.4.17 Niantic Inc.

- 6.4.18 Ultraleap Ltd.

- 6.4.19 HP Inc.

- 6.4.20 Immersion Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment