|

시장보고서

상품코드

1851835

스마트 산소포화도 측정기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Smart Pulse Oximeters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

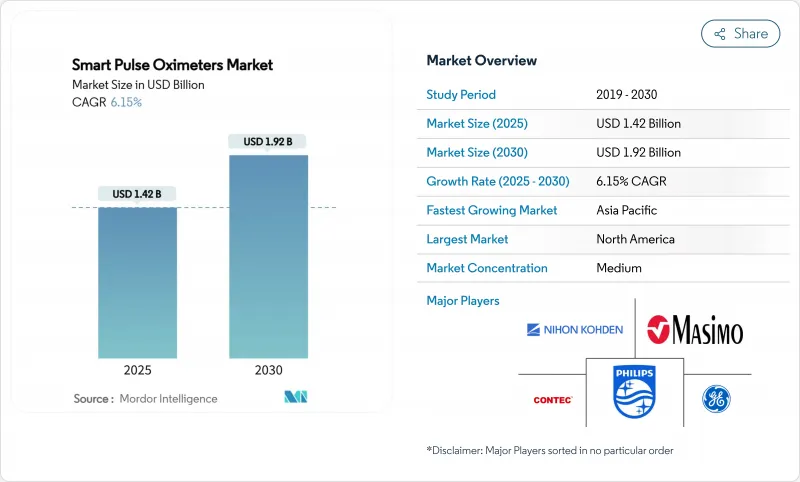

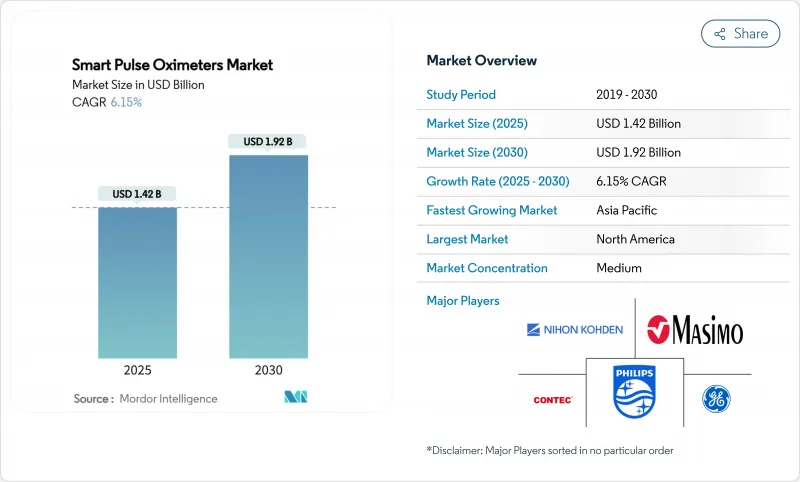

세계의 스마트 산소포화도 측정기 시장 규모는 2025년 14억 2,000만 달러에 달했고, 2030년까지 CAGR 6.15%로 진전해 19억 2,000만 달러에 이를 전망입니다.

디지털 헬스 통합, 재택 모니터링의 보급, 규제의 명확화에 의해 기존 광전식 용적맥파계와 클라우드 기반의 애널리틱스를 융합시킨 제품의 업그레이드가 가속화되고 있습니다. 병원 및 진료소에서 수요는 여전히 왕성하지만, 가전 브랜드는 임상적으로 검증된 센서를 스마트폰이나 웨어러블에 통합함으로써 액세스를 확대하고 있습니다. 모션 아테팩트와 피부색 바이어스를 보정하는 인공지능 알고리즘은 임상적 신뢰성을 높여 원격 환자 모니터링을 위한 상환 코드가 의료 제공업체의 채용을 뒷받침하고 있습니다. 이러한 요인은 스마트 산소포화도 측정기 시장에서 꾸준한 가치 확대와 경쟁 격화를 지원합니다.

세계 스마트 산소포화도 측정기 시장 동향과 통찰

만성 호흡기 질환과 심혈관 질환의 유병률 상승

COPD와 심부전의 증례 수가 증가함에 따라 임상의는 지속적인 SpO2 모니터링에 주력하고 있습니다. COPD 경로에 연결된 옥시미터를 통합한 프로그램은 입원 빈도를 65% 줄이고, 환자 어드히어런스를 88.6% 달성하며, 설득력 있는 이용 사례를 입증하고 있습니다. 밸류 베이스 케어 모델은 이러한 예방적 성과에 보답하는 것으로, 병원은 악화를 조기에 발견하는 예측 분석 기능을 갖춘 기기의 채용을 추진하고 있습니다. 종단적인 SpO2 데이터 위에 구축된 머신러닝 레이어는 적시에 개입을 가능하게 하고 응급실외 진료를 줄여줍니다. 그 결과 만성 질환의 압박은 스마트 산소포화도 측정기 시장을 주변 장치가 아닌 질병 관리 생태계의 중심에 둡니다.

가정 건강 및 원격 환자 모니터링 채택 증가

COVID-19는 가정에서의 산소포화도 측정을 표준화하고, 지불자는 원격 환자 모니터링 서비스를 상환하게 되었습니다. Samsung 스마트폰 센서의 혈액가스에 대한 2.6% RMSD의 임상 검증으로 의료 등급 기능이 1억대 이상의 휴대전화에 탑재되어 극히 작은 한계 비용으로 액세스가 확대되었습니다. 의료 제공업체는 SpO2의 라이브 피드를 집약한 대시보드를 활용하여 여분의 진료 예약 없이 시기 적절한 아웃리치를 가능하게 하고 있습니다. 비용 절감, 환자 만족도 향상, 만성 질환 감시의 용이화로 장비 주문이 가속화되고 원격 모니터링은 스마트 산소포화도 측정기 시장의 구조적 성장의 핵심이 되었습니다.

높은 장비 비용과 일관성 없는 상환 정책

의료 등급 센서의 높은 가격 설정은 소규모 시설과 자기 부담 소비자의 채용을 방해합니다. 상환은 보험 회사와 지역에 따라 크게 다르므로 다기관 개발의 ROI 평가가 복잡해집니다. 원격 모니터링 프로그램은 재입원을 줄임으로써 다운스트림 절약으로 이어지지만, 하드웨어 전복 비용과 불투명한 지불 스케줄은 의사결정 주기를 길게 합니다. 저비용 설계가 시장에 진입하고 있지만 검증 요구와 인증료가 대폭적인 가격 인하를 막아 스마트 산소포화도 측정기 시장 전체의 상업 전략을 압박하고 있습니다.

부문 분석

핑거 유닛은 익숙한 폼 팩터와 트레이닝의 필요성이 낮아 2024년 시장 점유율은 44.56%를 유지했습니다. 반대로, 커넥티드형은 2030년까지 연평균 복합 성장률(CAGR) 8.54%를 나타내고, 일상 케어에 클라우드 텔레메트리와 빅 데이터 분석을 도입합니다. 손목 장착형은 운동이나 수면 건강 틈새에 어필하고, 멀티 파라미터 패치는 외래 모니터링의 미래에 스포트라이트를 맞춥니다. 최근 FDA 승인을 받은 OxiWear의 연속 모니터링 귀 클립은 SpO2 스트림을 중단하지 않는 웨어러블 의료기기에 대한 경로를 보여줍니다. 지속적인 데이터 흐름은 임상의의 견해를 확대하고 예측 케어 알고리즘을 지원하며 무선 카테고리에서 스마트 산소포화도 측정기 시장 규모의 점유율을 확대하고 있습니다.

약진의 배경에는 스마트폰이나 병원의 대시보드와 몇 초 안에 페어링할 수 있는 상호 운용성의 향상이 있습니다. 개발자는 현재 ISO 호환 Bluetooth 저에너지 스택과 암호화 API를 선호하고 의료 기록과의 호환성을 보장합니다. 이러한 사용자 중심의 엔지니어링은 온보딩을 단축하고, 지원 비용을 줄이고, 기관의 조달 주기를 가속화합니다. 그 결과 광범위한 스마트 산소포화도 측정기 시장에서 연결형은 기존의 독립형을 능가합니다.

ICU의 프로토콜은 엄격한 경보 기준을 충족하는 음미된 하드웨어를 필요로 하기 때문에 독립형 모니터는 여전히 55.46%의 판매를 차지합니다. 그럼에도 불구하고 Samsung과 Apple이 카메라 + LED 어레이가 FDA 임계값을 지울 수 있음을 입증했기 때문에 휴대폰 기반 센서는 CAGR 8.87%로 확대될 것으로 보입니다. 개발자는 타사 원격 의료 앱이 암호화된 SpO2 스냅샷을 캐싱할 수 있도록 하는 SDK를 제공하여 소프트웨어 수익 전망을 증가시킵니다. 보험 회사가 원격 모니터링의 CPT 코드를 환불하면 임상의는 점점 앱 기반 옥시메트리를 처방하게 되고, 보급을 촉진하고, 스마트 산소포화도 측정기 시장을 다양화시킵니다.

이와 병행하여 스마트 워치는 의료기기로 승인을 받고 있습니다. Apple 특허의 장애물은 IP 위험을 나타내지만 기술적 실현 가능성은 입증되었습니다. 웨어러블 플랫폼은 지속적인 배경 측정을 지원하고 수면 무호흡 감지 및 운동 회복 분석에 정보를 제공합니다. 표준화된 펌웨어 업데이트는 하드웨어를 교체하지 않고도 알고리즘을 개선하고, 디바이스 수명 주기를 연장하며, 스마트 산소포화도 측정기 산업 내 경상 소프트웨어 수익 루프를 제공합니다.

지역 분석

북미는 상환의 확실성과 실리콘 밸리에서 보스턴에 이르는 혁신적인 클러스터를 배경으로 2024년 44.32%의 매출을 달성했습니다. 미국 상위 10개 병원 중 9개 병원이 ICU 모니터링에 Masimo SET 기술을 표준 채용하고 있어 스마트 산소포화도 측정기 시장의 기업 점유율을 지원하고 있습니다. 캐나다의 가상 병동 시험에 대한 환불과 멕시코 국경을 넘은 무역 정책은 지역의 안정적인 처리 능력을 지원합니다.

한편 아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 7.34%로 예측되어 압도적인 수량 견인국이 되고 있습니다. 중국의 의료기술 생산은 국내 브랜드를 우대하는 까다로운 R&D 세액공제와 병원 조달범위에 도움을 받아 2019년 이후 매년 28% 성장하고 있습니다. 일본의 400억 달러의 의료기기 시장은 초고령층을 관리하기 위한 원격 모니터링을 중심으로 미국의 센서 전문 기업과 제휴하고 있습니다. 인도의 생산 연동형 인센티브는 2030년까지 의료기기 매출액 500억 달러를 목표로 하고 있으며 품질기준 개정 하에 옥시미터 조립을 위한 그린필드 생산능력을 개방합니다. 한국은 첨단 반도체 패키징과 OLED의 전문지식을 조합하여 초박형 반사형 센서를 제조해, 이 지역을 스마트 산소포화도 측정기 시장의 혁신의 도가니로서 확고하게 합니다.

유럽에서는 MDR 하에서 안전성과 컴플라이언스가 우선되고, 견고한 CE 포트폴리오를 가진 기존 기업이 경쟁력을 가지고 있습니다. 독일에서는 대학병원과 중소기업의 연구개발 협력이 추진되고, 프랑스에서는 국민건강보험에 의한 원격 모니터링의 시험적 도입에 자금이 제공됩니다. 브렉시트 후 영국은 MHRA와의 연계를 유지하면서도 독립적인 가속 경로를 설정하고 있습니다. 규제 당국은 규정 준수 위반 온라인 목록을 일상적으로 삭제하고 단속에 대한 경계를 강조합니다. 이러한 정책을 종합하면 세계적인 스마트 산소포화도 측정기 시장의 성장에 기여하는 것은 중간 정도이지만 확실합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 호흡기 질환과 순환기 질환 증가

- 재택 헬스케어와 원격 환자 모니터링의 도입 확대

- 웨어러블 및 커넥티드 펄스 옥시메트리의 기술적 진보

- 디지털 건강과 원격 의료에 대한 정부 지원 증가

- 소비자용 건강기기의 전자상거래 채널 확대

- 유행 후 병원 산소 포화도 모니터링 기준에 주목

- 시장 성장 억제요인

- 높은 의료기기 비용과 일관성이 없는 상환 정책

- 엄격한 규제와 임상 검증 요건

- 다양한 환자 집단에서의 데이터 정밀도에 대한 우려

- 가격 경쟁의 격화와 마진의 압축

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 손가락 산소포화도 측정기

- 핸드헬드 산소포화도 측정기

- 손목 장착형 산소포화도 측정기

- 무선 및 접속형 산소포화도 측정기

- 멀티파라미터 및 스마트 웨어러블(SpO2)

- 플랫폼별

- 독립형 장비

- 스마트폰 내장 센서

- 스마트 워치 내장 센서

- 용도별

- 만성 질환 관리(COPD, CHF 등)

- 응급 및 중환자 케어

- 수술 후 모니터링

- 수면 및 호흡요법

- 스포츠 및 웰니스 추적

- 최종 사용자별

- 병원 및 클리닉

- 외래수술센터(ASC)

- 재택 헬스케어

- 스포츠 및 피트니스 센터

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Masimo Corporation

- Medtronic plc

- Koninklijke Philips NV

- GE Healthcare

- Nonin Medical, Inc.

- Nihon Kohden Corporation

- Halma plc(SunTech Medical)

- Contec Medical Systems

- Omron Corporation

- ICU Medical(Smiths Group plc)

- iHealth Labs

- Apple Inc.

- Samsung Electronics Co.

- Garmin Ltd.

- ResMed Inc.

제7장 시장 기회와 장래의 전망

JHS 25.11.25The smart pulse oximeters market size reached USD 1.42 billion in 2025 and is on track to reach USD 1.92 billion by 2030, advancing at a 6.15% CAGR.

Digital health integration, wider home-monitoring use, and regulatory clarity are accelerating product upgrades that blend traditional photoplethysmography with cloud-based analytics. Demand remains brisk in hospitals and clinics, yet consumer electronics brands are expanding access by embedding clinically validated sensors in smartphones and wearables. Artificial-intelligence algorithms that correct for motion artefacts and skin-tone bias strengthen clinical confidence, while reimbursement codes for remote patient monitoring encourage provider adoption. Together, these factors underpin steady value expansion and intensifying competition within the smart pulse oximeters market.

Global Smart Pulse Oximeters Market Trends and Insights

Rising Prevalence of Chronic Respiratory and Cardiovascular Diseases

Higher COPD and heart-failure caseloads keep clinicians focused on continuous SpO2 surveillance. Programs that embed connected oximeters into COPD pathways cut hospitalization frequency by 65% while achieving 88.6% patient adherence, establishing compelling use-case proof. Value-based-care models reward these preventive outcomes, pushing hospitals to adopt devices with predictive analytics that spot exacerbations early. Machine-learning layers built atop longitudinal SpO2 data enable timely interventions, reducing emergency-department visits. Consequently, chronic-disease pressure makes the smart pulse oximeters market central to disease-management ecosystems rather than a peripheral gadget.

Increasing Adoption of Home Healthcare and Remote Patient Monitoring

COVID-19 normalized at-home pulse oximetry, and payers now reimburse remote patient monitoring services. Clinical validation of Samsung's smartphone sensor at 2.6% RMSD against arterial blood gas has placed medical-grade capability in more than 100 million phones, scaling access at negligible marginal cost. Providers leverage dashboards that aggregate live SpO2 feeds, allowing timely outreach without extra clinic appointments. Cost savings, improved patient satisfaction, and easier chronic-condition surveillance are accelerating device orders, cementing remote monitoring as a structural growth pillar for the smart pulse oximeters market.

High Device Cost and Inconsistent Reimbursement Policies

Premium pricing for medical-grade sensors deters adoption among smaller facilities and self-pay consumers. Reimbursement varies widely by insurer and region, complicating ROI assessments for multi-site rollouts. Although remote-monitoring programs yield downstream savings by reducing readmissions, front-loaded hardware expenses and uncertain payor timelines prolong decision cycles. Lower-cost designs are entering the market, yet validation demands and certification fees constrain dramatic price cuts, pressuring commercial strategies across the smart pulse oximeters market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Wearable and Connected Pulse Oximetry

- Growing Government Support for Digital Health and Telemedicine

- Stringent Regulatory and Clinical Validation Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Finger units retained 44.56% market share in 2024 thanks to familiar form factors and low training needs. Conversely, connected variants are set to post an 8.54% CAGR through 2030, injecting cloud telemetry and big-data analytics into everyday care. Wrist-worn models appeal to athletic and sleep-health niches, and multi-parameter patches spotlight the future of ambulatory monitoring. OxiWear's continuous-monitoring ear clip, recently FDA-cleared, illustrates the pathway to wearable medical devices with uninterrupted SpO2 streams. Continuous data flow expands clinician insight and underpins predictive-care algorithms, securing a rising share of the smart pulse oximeters market size for wireless categories.

Their surge owes much to interoperability advances that let devices pair with smartphones and hospital dashboards in seconds. Developers now prioritize ISO-compliant Bluetooth Low Energy stacks and encrypted APIs, guaranteeing health-record compatibility. That user-centric engineering shortens onboarding, trims support costs, and accelerates institutional procurement cycles. As result, connected formats are outpacing legacy standalone models within the broader smart pulse oximeters market.

Standalone monitors still dominate with 55.46% revenue because ICU protocols require vetted hardware that meets strict alarm standards. Even so, phone-based sensors will expand at an 8.87% CAGR, as Samsung and Apple prove camera-plus-LED arrays can clear FDA thresholds. Developers supply SDKs enabling third-party telehealth apps to cache encrypted SpO2 snapshots, multiplying software revenue prospects. When insurers reimburse remote-monitoring CPT codes, clinicians increasingly prescribe app-based oximetry, fueling adoption and diversifying the smart pulse oximeters market.

In parallel, smartwatches are edging toward medical-device clearance. Apple's patent hurdles show IP risk, yet technical feasibility is proven. Wearable platforms support continuous background readings, informing sleep-apnea detection and exercise recovery analytics. Standardized firmware updates deliver algorithm refinements without hardware swaps, prolonging device life cycles and feeding recurring-software revenue loops inside the smart pulse oximeters industry.

The Smart Pulse Oximeters Market Report is Segmented by Product Type (Finger Pulse Oximeters, and More), Operating Platform (Stand-Alone Devices, and More), Application (Chronic Disease Management, and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 44.32% revenue in 2024 on the back of reimbursement certainty and an innovation cluster spanning Silicon Valley to Boston. Nine of the top 10 US hospitals standardize on Masimo SET technology for ICU monitoring, anchoring corporate share in the smart pulse oximeters market. Canada's reimbursement for virtual-ward pilots and Mexico's cross-border trade policies support steady regional throughput.

Asia-Pacific, meanwhile, is forecast at a 7.34% CAGR through 2030 and has become the dominant volume engine. China's medtech output has grown 28% annually since 2019, aided by generous R&D tax credits and hospital-procurement quotas favoring domestic brands. Japan's USD 40 billion device market centres on telemonitoring to manage its super-aged demographic, with local distributors partnering US sensor specialists. India's production-linked incentives target USD 50 billion in medical-device sales by 2030, opening greenfield capacity for oximeter assembly under revised quality norms. South Korea couples advanced semiconductor packaging with OLED expertise to produce ultra-thin reflective sensors, cementing the region as an innovation crucible for the smart pulse oximeters market.

Europe prioritizes safety and compliance under MDR, giving incumbents with robust CE portfolios a competitive moat. Germany drives R&D collaborations between university hospitals and SMEs, while France funds remote-monitoring pilots via national health insurance. Post-Brexit UK maintains MHRA alignment yet sets independent accelerated-access pathways. Regulators routinely delist non-compliant online listings, underscoring enforcement vigilance. Collectively, these policies sustain moderate yet dependable contribution to global smart pulse oximeters market growth.

- Masimo

- Medtronic

- Koninklijke Philips

- GE Healthcare

- Nonin Medical

- Nihon Kohden

- Halma plc (SunTech Medical)

- Contec Medical Systems

- OMRON

- ICU Medical (Smiths Group plc)

- iHealth Labs

- Apple

- Samsung Electronics Co.

- Garmin

- Resmed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Respiratory and Cardiovascular Diseases

- 4.2.2 Increasing Adoption of Home Healthcare and Remote Patient Monitoring

- 4.2.3 Technological Advancements in Wearable and Connected Pulse Oximetry

- 4.2.4 Growing Government Support for Digital Health and Telemedicine

- 4.2.5 Expansion of E-Commerce Channels for Consumer Health Devices

- 4.2.6 Post-Pandemic Focus on Hospital Oxygen Saturation Monitoring Standards

- 4.3 Market Restraints

- 4.3.1 High Device Cost and Inconsistent Reimbursement Policies

- 4.3.2 Stringent Regulatory and Clinical Validation Requirements

- 4.3.3 Data Accuracy Concerns in Diverse Patient Populations

- 4.3.4 Intensifying Price Competition and Margin Compression

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Finger Pulse Oximeters

- 5.1.2 Hand-held Pulse Oximeters

- 5.1.3 Wrist-worn Pulse Oximeters

- 5.1.4 Wireless/Connected Pulse Oximeters

- 5.1.5 Multi-parameter Smart Wearables (SpO?-enabled)

- 5.2 By Operating Platform

- 5.2.1 Stand-Alone Devices

- 5.2.2 Smartphone-Integrated Sensors

- 5.2.3 Smartwatch-Integrated Sensors

- 5.3 By Application

- 5.3.1 Chronic Disease Management (COPD, CHF, Etc.)

- 5.3.2 Critical & Emergency Care

- 5.3.3 Post-Operative Monitoring

- 5.3.4 Sleep & Respiratory Therapy

- 5.3.5 Sports & Wellness Tracking

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Home Healthcare

- 5.4.4 Sports & Fitness Centers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Masimo Corporation

- 6.3.2 Medtronic plc

- 6.3.3 Koninklijke Philips N.V.

- 6.3.4 GE Healthcare

- 6.3.5 Nonin Medical, Inc.

- 6.3.6 Nihon Kohden Corporation

- 6.3.7 Halma plc (SunTech Medical)

- 6.3.8 Contec Medical Systems

- 6.3.9 Omron Corporation

- 6.3.10 ICU Medical (Smiths Group plc)

- 6.3.11 iHealth Labs

- 6.3.12 Apple Inc.

- 6.3.13 Samsung Electronics Co.

- 6.3.14 Garmin Ltd.

- 6.3.15 ResMed Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment