|

시장보고서

상품코드

1851845

음향 카메라 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Acoustic Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

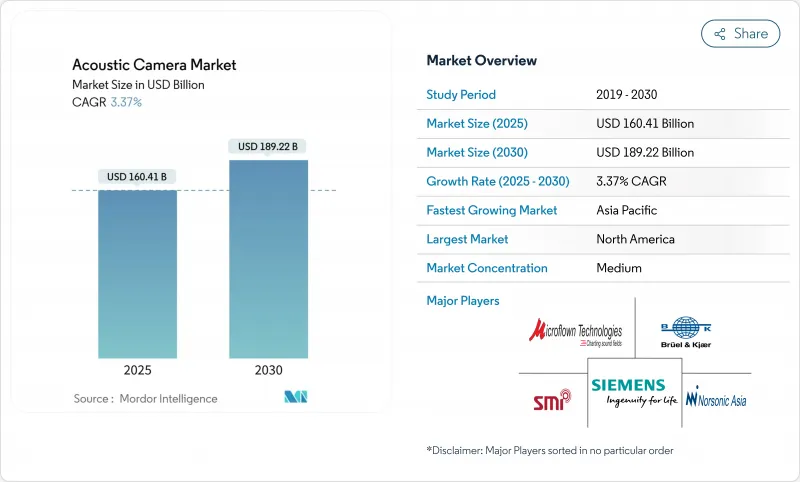

음향 카메라 시장은 2025년에 1,604억 1,000만 달러로 추정되고, 2030년에는 1,892억 2,000만 달러에 이를 전망이며, CAGR 3.37%로 확대될 것으로 예측됩니다.

MEMS 마이크 어레이의 비용 절감과 컴팩트한 엣지 AI 프로세서의 등장으로 시스템 부품비가 5,000달러 이하로 내려가고, 음향 이미징이 실험실에서 공장 플로어나 시가지로 이행하고 있습니다. 지자체는 소음 감시 카메라를 도입하고, 자동차 엔지니어는 전기자동차의 NVH 시험을 디지털화하며, 전력 회사는 빔포밍 모듈 및 예지 보전 플랫폼을 결합합니다. 엣지 애널리틱스는 이제 디바이스에서 실행되고 클라우드 대역폭과 대기 시간을 줄이는 동시에 원격 자산에서 이용 사례를 넓히고 있습니다. 경쟁의 중심은 규모보다 알고리즘 효율과 소프트웨어 에코시스템이며, 틈새 혁신자들이 다양한 테스트 장비 제조업체와 어깨를 나란히 할 수 있습니다.

세계의 음향 카메라 시장 동향 및 인사이트

세계 도시 소음 규제 강화

지자체의 소음 규제는 소음계에 의한 점 측정으로부터, 위반 차량을 특정하는 공간 화상 측정으로 이행하고 있습니다. 유럽과 북미 도시에서는 2024년에 카메라 기반 소음 레이더가 설치되었으며 SoundVue와 같은 솔루션은 법적 증거 요구 사항을 충족하는 클래스 1 정확도를 제공합니다. 유럽 연합(EU)은 2030년까지 운송 소음을 30% 줄이는 것을 목표로 하고 있으며, 견고한 옥외용 음향 카메라의 장기 조달에 박차를 가하고 있습니다. 우선순위는 이동식 트레일러보다 상설적인 로드사이드 유닛으로 이동하고 있으며, 다년간의 하드웨어 수요 및 서비스 계약을 지원하고 있습니다.

E 모빌리티 플랫폼에서 NVH의 급속한 디지털화

전동 파워트레인은 연소의 마스킹을 억제하고 모터, 인버터 및 HVAC 덕트에서 소리의 특징을 드러냅니다. 자동차 제조업체 각사는 2024년 중에 음향 시험 예산을 증액해, 현대 자동차는 내장의 풀 매핑에 3D 스캐닝 리그를 채용했습니다. 실시간 빔포밍을 통해 엔지니어는 실제 주행 시 방사 패턴을 시각화하고 생산 시작 전에 수정 루프를 닫을 수 있습니다. 증가하는 상업용 밴 및 도시 버스 플릿은 편안함과 지역 소음 규제를 충족시키기 위해 동일한 기술을 채택합니다.

3차원 MEMS 어레이 리그의 초기 투자는 고액

수백 개의 위상 매칭 마이크, 고정밀 하우징 및 고대역폭 컨버터가 재료비, 조립 비용을 밀어 올리기 때문에 조사 등급의 3D 구성은 10만 달러를 초과할 수 있습니다. 광학 MEMS 마이크는 현재 80dB의 SNR을 실현하고 있지만, 프로세스 툴과 수율 학습 곡선이 상당한 가격 하락을 선도하고 있습니다. 소규모 기업은 50,000달러 이하의 모듈형 어레이가 보급될 때까지 공유 서비스 실험실을 활용하거나 3D 시스템을 대여합니다.

부문 분석

2D 아키텍처는 입증된 신뢰성과 저렴한 가격으로 2024년 음향 카메라 시장에서 53%의 점유율을 유지했습니다. 공장의 누설조사 및 자동차 부품 검사로 우위를 차지하고 있습니다. 한편, 3D 유닛은 캐빈내의 소음 매핑, 도시에서의 공중 이동 시험, 복잡한 기계의 인클로저로 전수 정위가 요구되기 때문에 CAGR 16.2%로 추이하고 있습니다. 192개의 마이크가 장착된 Octagon 시스템은 20Hz-10kHz 대역에서 분해 능을 발휘합니다. MEMS 비용이 완화됨에 따라 3D 플랫폼의 음향 카메라 시장 규모는 주류 옵션과의 격차를 줄일 것으로 예측됩니다. 인공지능에 의한 패턴 인식은 히트율을 향상시켜, 보다 작은 애퍼처로 종래의 성능에 필적하는 것이 가능하게 됩니다.

시스템 통합자는 CAD 대시보드에 실시간 시각화를 통합하여 엔지니어가 음향 처리를 며칠이 아닌 몇 분 안에 반복할 수 있도록 합니다. 이러한 워크플로우 압축은 항공우주 및 고급 차량 분야에서 프리미엄을 정당화합니다. 프로토타입의 3D 어레이는 2024년에 6만 달러 이하로 출하되었으며, 중견 공급업체와 대학의 실험실 채용이 확산되는 징조를 보이고 있습니다.

니어필드 셋업은 명확한 표준 및 통제된 환경 덕분에 2024년에는 61%의 매출을 기록했습니다. 챔버 테스트, 기어 박스 분석, 벤치 탑 RandD는 여전히 중요한 이용 사례입니다. 원시야 수요는 풍력 터빈의 소음 감사, 스마트 시티의 사운드 매핑, 항공기의 패스바이 시험과 보조를 맞추어 CAGR 14.8%로 상승하고 있습니다. 최소 분산 왜곡이 적은 응답 알고리즘은 배경 교통량이 많음에도 불구하고 50m 이상 떨어진 음원을 분리합니다. 그 결과 장거리 시스템의 음향 카메라 시장 규모는 2030년까지 두배로 될 것으로 예측됩니다. 인프라 관리자는 데이터를 지리공간 대시보드에 통합하고 시설 설계도에 음향 메트릭을 중첩하여 수리 작업자를 신속하게 파견할 수 있습니다.

현장 운영자는 IP65 이상의 견고한 케이스와 4G 또는 LoRaWAN에서 경고를 중계하는 저전력 엣지 프로세서를 높이 평가합니다. 설치의 용이성 및 클라우드 API를 중시하는 벤더는 지자체의 입찰 및 재생에너지 팜으로 낙찰하고 있습니다.

음향 카메라 시장은 어레이 유형별(2-D 어레이, 3-D 어레이), 측정 유형별(니어필드, 퍼필드), 용도별(노이즈 소스 식별, 누설 검출 등), 최종 사용자 산업별(자동차 및 이동성 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

유럽은 2024년에 음향 카메라 시장의 31%를 차지했으며, 까다로운 환경 규제 및 정교한 자동차 공급망에 의해 지원되고 있습니다. 독일의 OEM은 카메라 데이터를 디지털 트윈으로 캐스케이드하는 풀 차량 NVH 프로그램을 실시하고 있으며, 프랑스 지자체는 2030년까지 운송 소음을 30% 삭감하기 위해 여러 해에 걸친 도시 소음 카메라 파일럿을 실시했습니다. Horizon Europe의 자금 조달 수단은 3차원 빔포밍 소프트웨어를 개선하는 산학 컨소시엄을 가속화합니다.

APAC의 CAGR은 14.3%입니다. 중국은 GB/T 37153-2018에 따라 음향 차량 경보 시스템을 법제화하고 티아완 공급업체에게 이미지 툴로 라우드 스피커 시그니처의 검증을 촉구합니다. 심천과 싱가포르의 스마트 시티 프로그램은 교차로에 영구적인 음향 매핑 노드를 설치합니다. 식스 시그마 품질로 알려진 일본의 전자기기 공장은 진공 누출의 히스를 잡기 위해 픽앤플레이스 라인에 카메라를 설치하여 일관된 지역 수주를 추진하고 있습니다. 확대되는 인도의 지하철 철도는 압축 공기 브레이크 시스템에 음향 누출 감지 장치를 지정합니다.

북미는 항공우주 프라임이 FAA 소음 인증을 준수하고 OSHA가 노출 지침을 확대하는 동안 영향력 있는 역할을 유지하고 있습니다. 산업용 최종 사용자는 음향 카메라와 진동, 열 및 전력 품질 센서를 통합 대시보드에 통합합니다. 멕시코 걸프의 석유 및 가스 생산 회사는 저장 탱크 검사를 위해 로봇 크롤러에 카메라를 탑재하여 폐쇄 공간으로의 진입 위험을 줄이고 있습니다.

남미, 중동, 아프리카는 신흥국이지만 미래의 유망한 지역입니다. 칠레 광산업자는 벤트 팬의 공진을 식별하기 위해 휴대용 이미저를 테스트하고 있으며, 멕시코 걸프의 전력 회사는 육안 무인 항공기가 눈부심과 모래에 어려움을 겪는 사막의 송전선로 검사를 위해 카메라를 시험적으로 도입했습니다. 여기서의 보급은 선진 지역보다 2-3년 늦을 것으로 예상되지만, 그래도 세계적인 대수에는 플러스입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 도시 소음 규제 강화

- e-모빌리티 플랫폼에서 NVH의 급속한 디지털화

- 스마트 공장에서 휴대용 소음계로부터 이미지 센서로 이동

- 항공우주 캐빈 컴포트 인증 기준치의 상승

- 엣지 AI 빔포밍 모듈이 5달러 이하의 BOM을 가능하게 하는 음향 카메라 시장

- 자율형 로봇 검사 페이로드에 대한 통합

- 시장 성장 억제요인

- 3D MEMS 어레이 리그의 높은 초기 투자

- 현장 교정용 표준기의 지역간 희소성

- 지연 및 합산 빔 형성 IP 주변의 특허 덤불

- 악천후 유틸리티를 위한 제한된 견고한 옵션

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 어레이 유형별

- 2차원 어레이

- 3차원 어레이

- 측정 유형별

- 니어필드

- 퍼필드

- 용도별

- 음원 탐사

- 누설 검사

- 고장 진단

- 기타(생체 음향, RandD)

- 최종 사용자 업계별

- 자동차 및 이동성

- 항공우주 및 방위

- 일렉트로닉스 및 반도체

- 에너지 및 전력

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Hottinger Brel and Kjr Sound and Vibration Measurement A/S

- gfai tech GmbH

- Teledyne FLIR LLC

- SM Instruments Inc.

- Fluke Corporation

- CAE Software and Systems GmbH

- Norsonic AS

- Microflown Technologies BV

- SINUS Messtechnik GmbH

- Sorama BV

- Polytec GmbH

- Visisonics Corporation

- Signal Interface Group LLC

- NL Acoustics Oy

- Ziegler-Instruments GmbH

- Siemens Digital Industries Software

제7장 시장 기회 및 향후 전망

AJY 25.11.26The acoustic camera market was valued at USD 160.41 billion in 2025 and is forecast to reach USD 189.22 billion by 2030, expanding at a 3.37% CAGR.

Cost reductions in MEMS microphone arrays and the arrival of compact edge-AI processors have lowered system bills-of-materials below USD 5,000, moving acoustic imaging from research laboratories into factory floors and city streets. Municipal authorities are deploying noise-enforcement cameras, automotive engineers are digitizing NVH testing for electric vehicles, and utilities are pairing beamforming modules with predictive-maintenance platforms. Edge analytics now runs on-device, trimming cloud bandwidth and latency while widening use cases in remote assets. Competitive activity centers on algorithm efficiency and software ecosystems rather than scale, allowing niche innovators to stand alongside diversified test-instrument majors.

Global Acoustic Camera Market Trends and Insights

Tightening Global Urban-Noise Regulations

Municipal agencies are moving from point sound-level meters to spatial imaging that links violations to individual vehicles. European and North American cities installed camera-based noise radars during 2024, and solutions such as SoundVue deliver Class 1 accuracy that satisfies legal-evidence requirements. The European Union targets a 30% cut in transport noise by 2030, spurring long-term procurement of rugged outdoor acoustic cameras. Preference is shifting toward permanent roadside units over mobile trailers, anchoring multi-year hardware demand and service contracts.

Rapid NVH Digitalization in E-Mobility Platforms

Electric powertrains silence combustion masking, unveiling tonal signatures from motors, inverters, and HVAC ducts. Automakers boosted acoustic test budgets during 2024; Hyundai adopted 3-D scanning rigs for full interior mapping. Real-time beamforming lets engineers visualize radiation patterns under actual driving, closing corrective loops before start-of-production. Growing fleets of commercial vans and city buses adopt the same methodologies to meet comfort and regional noise-homologation rules.

High Upfront Capex for 3-D MEMS-Array Rigs

Research-grade 3-D configurations can exceed USD 100,000 because hundreds of phase-matched microphones, precision housings, and high-bandwidth converters raise material and assembly costs. Optical MEMS microphones now deliver 80 dB SNR, yet process tooling and yield learning curves postpone sweeping price drops. Small enterprises lean on shared-service laboratories or rent 3-D systems until modular arrays below USD 50,000 proliferate.

Other drivers and restraints analyzed in the detailed report include:

- Shift from Handheld Sound-Level Meters to Imaging Sensors on Smart Factories

- Rising Aerospace Cabin-Comfort Certification Thresholds

- Scarcity of Field-Calibration Standards Across Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

2-D architectures retained 53% share of the acoustic camera market in 2024 owing to proven reliability and lower pricing. They dominate plant leak surveys and automotive component checks. Meanwhile, 3-D units are moving at a 16.2% CAGR as cabin noise mapping, urban-air-mobility trials, and complex machinery enclosures call for full-volume localization. The Octagon system with 192 microphones demonstrates resolution across 20 Hz to 10 kHz bands. As MEMS costs ease, the acoustic camera market size for 3-D platforms is expected to close the gap with mainstream options. Artificial-intelligence pattern recognition is improving hit rates, allowing smaller apertures to match legacy performance.

System integrators embed real-time visualization within CAD dashboards, so engineers iterate acoustic treatments in minutes rather than days. This workflow compression justifies premiums in aerospace and luxury vehicle segments. Prototype 3-D arrays shipped in 2024 at under USD 60,000, signalling a trajectory toward broader adoption among mid-tier suppliers and university labs.

Near-field setups commanded 61% revenue in 2024 thanks to clear standards and controlled environments. Chamber testing, gearbox analysis, and benchtop RandD remain anchor use cases. Far-field demand is climbing at a 14.8% CAGR in step with wind turbine noise audits, smart city sound mapping, and aircraft pass-by trials. Minimum variance distortion less response algorithms now separate sources more than 50 m away despite heavy background traffic. As a result, the acoustic camera market size for long-range systems is projected to double through 2030. Infrastructure managers integrate data into geospatial dashboards that overlay acoustic metrics on facility blueprints for quick dispatch of repair crews.

Field operators value rugged enclosures rated IP65 or higher and low-power edge processors that relay alerts over 4G or LoRaWAN. Vendors emphasizing ease of installation and cloud APIs are winning bids in municipal tenders and renewable-energy farms.

The Acoustic Camera Market Segmented by Array Type (2-D Arrays, 3-D Arrays), Measurement Type (Near-Field, Far-Field), Application (Noise Source Identification, Leak Detection and More), End-User Industry (Automotive & Mobility and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe held 31% of the acoustic camera market in 2024, anchored by stringent environmental regulations and a sophisticated automotive supply chain. German OEMs run full-vehicle NVH programs that cascade camera data into digital twins, while French municipalities engage multi-year urban noise-camera pilots to secure 30% transport noise cuts by 2030. Funding instruments from Horizon Europe accelerate academic-industry consortia that refine 3-D beamforming software.

APAC is set for a 14.3% CAGR. China legislated acoustic vehicle alerting systems under GB/T 37153-2018, pushing tier-one suppliers to validate loudspeaker signatures with imaging tools. Smart-city programs in Shenzhen and Singapore embed permanent acoustic mapping nodes at intersections. Japanese electronics plants, known for Six Sigma quality, fit cameras over pick-and-place lines to catch vacuum-leak hiss, driving consistent regional orders. India's expanding metro-rail footprint is specifying acoustic leak detection on compressed-air braking systems.

North America retains an influential role as aerospace primes comply with FAA noise certification and as OSHA broadens exposure guidelines. Industrial end users integrate acoustic cameras with vibration, thermal, and power-quality sensors in unified dashboards. Oil and gas producers in the Gulf Coast mount cameras on robotic crawlers for storage tank inspections, mitigating confined-space entry risks.

South America and the Middle East and Africa form nascent but promising territories. Mining operators in Chile test portable imagers to pinpoint vent fan resonance, while Gulf utilities trial cameras for desert power-line inspections where visual drones struggle with glare and sand. Uptake here is expected to trail advanced regions by two to three years yet remains additive to global volumes.

- Hottinger Brel and Kjr Sound and Vibration Measurement A/S

- gfai tech GmbH

- Teledyne FLIR LLC

- SM Instruments Inc.

- Fluke Corporation

- CAE Software and Systems GmbH

- Norsonic AS

- Microflown Technologies BV

- SINUS Messtechnik GmbH

- Sorama BV

- Polytec GmbH

- Visisonics Corporation

- Signal Interface Group LLC

- NL Acoustics Oy

- Ziegler-Instruments GmbH

- Siemens Digital Industries Software

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening global urban-noise regulations

- 4.2.2 Rapid NVH digitalisation in e-mobility platforms

- 4.2.3 Shift from handheld sound-level meters to imaging sensors on smart factories

- 4.2.4 Rising aerospace cabin-comfort certification thresholds

- 4.2.5 Edge-AI beamforming modules enable sub-$5 k BOM acoustic camera

- 4.2.6 Integration into autonomous-robot inspection payloads

- 4.3 Market Restraints

- 4.3.1 High upfront capex for 3D MEMS-array rigs

- 4.3.2 Scarcity of field-calibration standards across regions

- 4.3.3 Patent thickets around delay-and-sum beam-forming IP

- 4.3.4 Limited ruggedised options for harsh-weather utilities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Array Type

- 5.1.1 2-D Arrays

- 5.1.2 3-D Arrays

- 5.2 By Measurement Type

- 5.2.1 Near-Field

- 5.2.2 Far-Field

- 5.3 By Application

- 5.3.1 Noise Source Identification

- 5.3.2 Leak Detection

- 5.3.3 Mechanical Fault Diagnostics

- 5.3.4 Others (Bio-acoustics, RandD)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Mobility

- 5.4.2 Aerospace and Defense

- 5.4.3 Electronics and Semiconductor

- 5.4.4 Energy and Power

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 United Arab Emirates

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 South Africa

- 5.5.4.4 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Hottinger Brel and Kjr Sound and Vibration Measurement A/S

- 6.4.2 gfai tech GmbH

- 6.4.3 Teledyne FLIR LLC

- 6.4.4 SM Instruments Inc.

- 6.4.5 Fluke Corporation

- 6.4.6 CAE Software and Systems GmbH

- 6.4.7 Norsonic AS

- 6.4.8 Microflown Technologies BV

- 6.4.9 SINUS Messtechnik GmbH

- 6.4.10 Sorama BV

- 6.4.11 Polytec GmbH

- 6.4.12 Visisonics Corporation

- 6.4.13 Signal Interface Group LLC

- 6.4.14 NL Acoustics Oy

- 6.4.15 Ziegler-Instruments GmbH

- 6.4.16 Siemens Digital Industries Software

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment